Packaging Machinery Retrofitting And Upgrading Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 9.45 Billion |

| Market Size (2030) | USD 13.34 Billion |

| Growth Rate (2025 - 2030) | 7.14% CAGR |

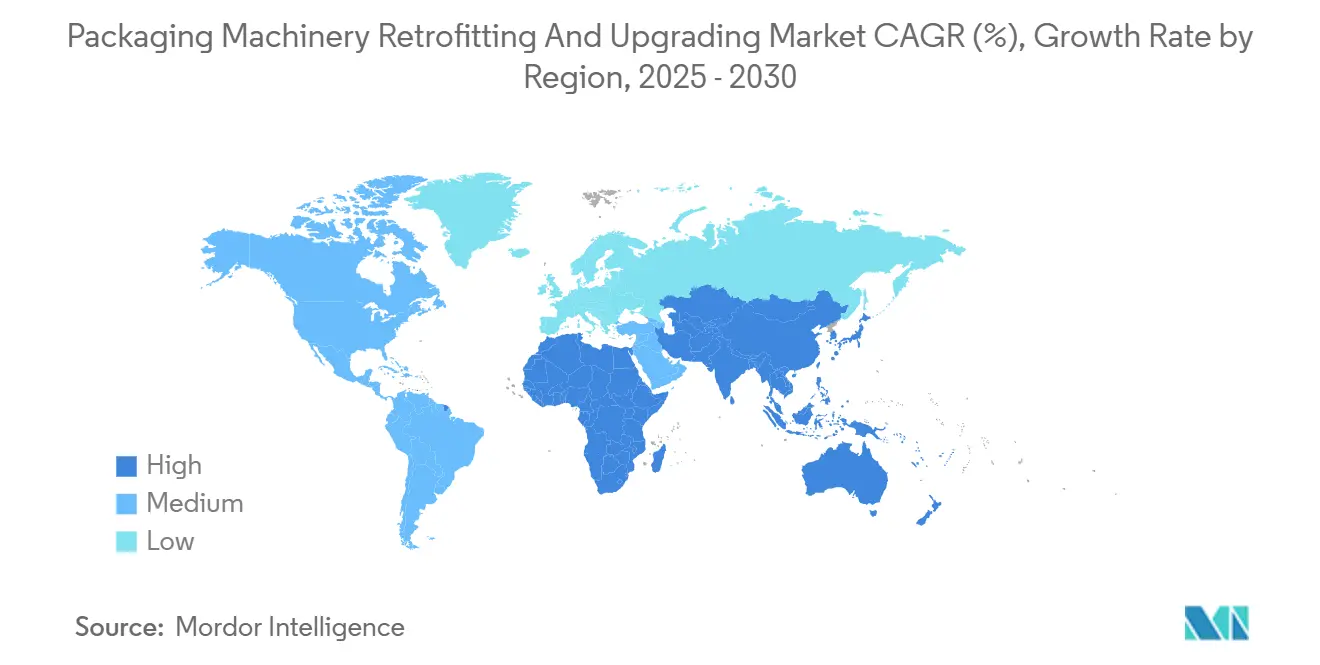

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Packaging Machinery Retrofitting And Upgrading Market Analysis by Mordor Intelligence

The packaging machinery retrofitting and upgrading market size reached USD 9.45 billion in 2025 and is projected to rise at a 7.14% CAGR to USD 13.34 billion by 2030. Growth rests on three pillars: aging industrial assets, intensifying regulatory oversight, and the pursuit of digital efficiency gains that delay full equipment replacements. Manufacturers increasingly view modular upgrades as a route to higher overall equipment effectiveness, shorter payback periods, and lower carbon footprints. The Asia-Pacific region holds the largest regional share and sets the pace for adoption, while service offerings centered on control-system upgrades accelerate the most rapidly. Across all regions, retrofit providers that minimize line downtime gain a decisive edge, as every unplanned hour can cost manufacturers up to USD 50,000, making operational continuity a primary buying criterion.[1]International Association of Packaging Research Institutes, “Global Packaging Equipment Age Analysis 2024,” IAPRI.ORG

Key Report Takeaways

- By machine type, the filling machines segment captured 27.67% of the Packaging Machinery Retrofitting and Upgrading Market share in 2024.

- By service type, the Packaging Machinery Retrofitting and Upgrading Market size for control-system upgrades is projected to grow at an 8.78% CAGR between 2025–2030.

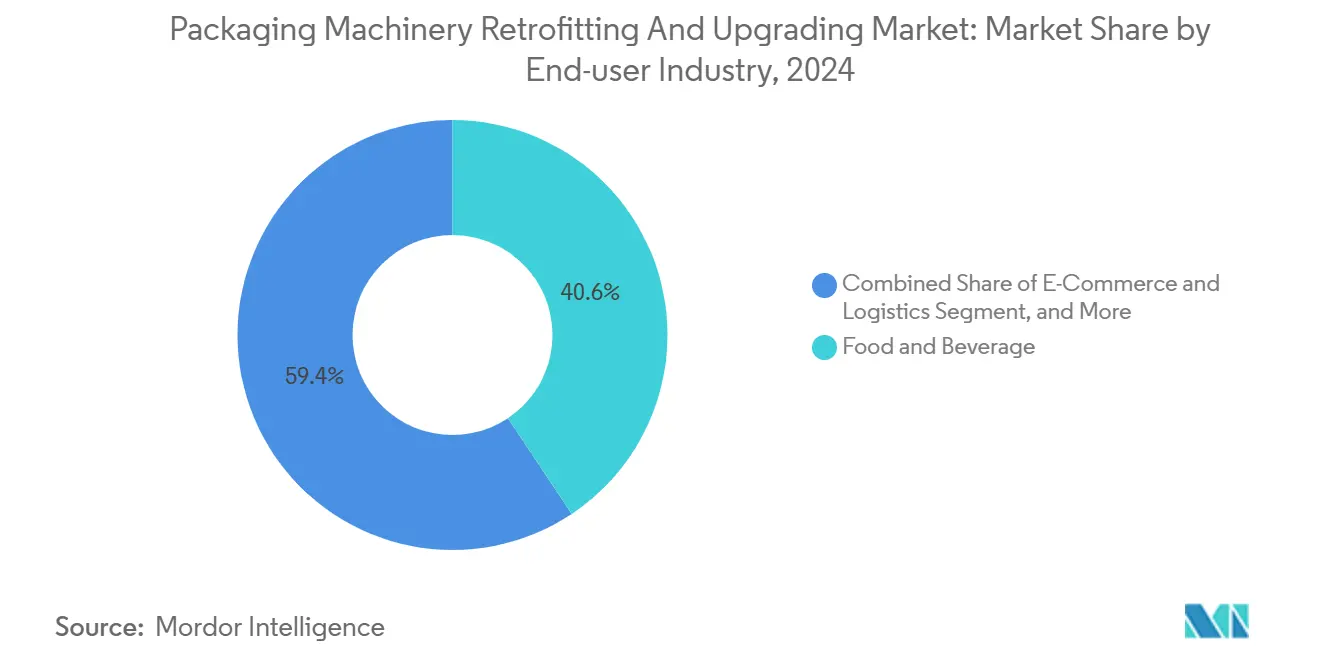

- By end-user industry, the food and beverage applications segment captured 40.64% of the Packaging Machinery Retrofitting and Upgrading Market share in 2024.

- By geography, the Packaging Machinery Retrofitting and Upgrading Market size for Asia-Pacific is projected to grow at a 9.28% CAGR between 2025–2030.

Global Packaging Machinery Retrofitting And Upgrading Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging global installed base of packaging lines | +1.8% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Demand for higher energy efficiency in plants | +1.2% | Global, strongest in EU and North America | Long term (≥ 4 years) |

| Compliance with stricter food-safety regulations | +1.0% | Global, led by FDA and EU regulatory zones | Short term (≤ 2 years) |

| Modular retrofit kits accelerating upgrade cycles | +0.9% | Asia-Pacific core, spillover to Middle East and Africa | Medium term (2-4 years) |

| Government decarbonization incentives for Industry 4.0 | +0.7% | EU, North America, select Asia-Pacific markets | Long term (≥ 4 years) |

| AI-enabled predictive maintenance retrofits | +0.6% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ageing Global Installed Base of Packaging Lines

Most packaging lines in service today average 12-15 years of operation, exceeding recommended modernization thresholds and creating a large pool of candidates for refurbishment. In Europe, equipment in many food plants is approximately 18 years old, while North American pharmaceutical lines exhibit similar vintage levels. Retrofitting unlocks 70-80% of a new machine's performance for only 60-70% of the cost, making it a financially compelling alternative to full replacement. Deferred upgrades erode operational efficiency by 15-20% each year, so line owners increasingly view modernization as unavoidable. As capital budgets tighten, retrofit packages that can be executed in phases without stopping production are gaining preference.

Demand for Higher Energy Efficiency in Plants

Energy now represents 8-12% of packaging plant operating expenses, rising faster than other cost lines, especially in Europe, under the Energy Efficiency Directive target of 32.5% reduction by 2030. Servo motor retrofits and variable-frequency drives reduce electricity use by up to 30% compared to pneumatic systems, while upgraded heat-recovery loops significantly reduce thermal waste. Many EU utilities also link tariffs to kilowatt reduction targets, making compliance both an environmental and financial necessity. Eligible projects receive tax credits or low-interest loans in several EU member states, accelerating adoption. Facilities that combine mechanical improvements with digital power-management software typically recover their investment within two years, a timeframe that aligns with CFO payback expectations.

Compliance with Stricter Food-Safety Regulations

The implementation of the Food Safety Modernization Act in the United States accelerated in 2024, with tightened requirements for traceability, hygienic design, and automated cleaning validation. Similar momentum in the European Union and Canada compels processors to retrofit older machines with advanced sensors, stainless-steel contact parts, and data-logging modules. Non-compliance can trigger penalties of USD 2-5 million per incident. Consequently, demand for quick-install sanitation kits and software that automates audit reporting has surged. Equipment vendors offering turnkey validation documentation gain a commercial advantage by shortening the time required to requalify lines after an upgrade.

AI-Enabled Predictive Maintenance Retrofits

Machine-learning algorithms now enable the prediction of equipment failure several weeks in advance by analyzing vibration, temperature, and power signatures. Siemens documented a 45% reduction in unplanned downtime after deploying its MindSphere IoT suite on retrofitted filling and capping lines in 2024.[2]Siemens AG, “MindSphere IoT Platform Performance Report 2024,” SIEMENS.COM Payback arrives within 12-18 months through lower spare parts inventory, shorter maintenance windows, and fewer emergency callouts. Adequate staff training remains the primary hurdle, as technicians must interpret analytics dashboards and adjust maintenance schedules accordingly. Vendors are increasingly packaging cloud subscriptions, edge hardware, and technical training into a single monthly fee, which simplifies budgeting and lowers entry barriers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front capital outlay for complex retrofits | -1.4% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Downtime risk during line conversions | -1.1% | Global, critical in continuous production | Short term (≤ 2 years) |

| Shortage of retrofit-skilled technicians | -0.8% | Global, severe in North America and Europe | Medium term (2-4 years) |

| Cyber-security concerns in control-system upgrades | -0.6% | Global, heightened in critical industries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Capital Outlay for Complex Retrofits

Full retrofits can cost USD 500,000 to USD 3 million per line, a daunting figure for small and mid-sized enterprises. Unanticipated scope creep during disassembly often inflates budgets by 20-30%. In emerging markets, where interest rates are higher and credit access is more limited, the financing gap is stark. Traditional equipment leases cater to new purchases rather than upgrade services, so manufacturers rely on short-term working-capital loans that carry unfavorable terms. The capital hurdle also delays multi-line projects, forcing firms to modernize one cell at a time, which extends payback periods. Retrofit suppliers that introduce outcome-based contracts or pay-as-you-save models are starting to differentiate themselves.

Shortage of Retrofit-Skilled Technicians

Roughly 40,000 technician roles focused on retrofitting remained vacant worldwide at the end of 2024, with the tightest bottlenecks in North America and Europe. These specialists must merge knowledge of legacy mechanics with modern robotics, PLC coding, and cybersecurity best practices, a blend not taught in conventional trade programs. Wait times for complex line conversions can stretch beyond six months, inflating project costs by 15-25% as overtime accrues and schedules slip. Industry associations have responded by funding accelerated curricula; however, graduate volumes still trail demand. Retention is further challenged by aggressive recruitment from high-tech sectors that offer higher salary ceilings for similar digital skills.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Dominance of Filling Machines and Rise of Palletizing Systems

The filling segment remained the largest in 2024, accounting for 27.67% of the packaging machinery retrofitting and upgrading market size. Food processors and pharmaceutical firms favor upgrading their filling machines because newer dosing valves and hygienic seals facilitate compliance with stricter safety mandates. Demand also rises for multi-format fillers that handle small-batch product lines without extensive changeover downtime, a priority for nutraceutical startups and craft beverage brands. Retrofitted form-fill-seal systems are increasingly integrating vision sensors to eliminate misaligned seals in real-time, thereby curbing material waste and recalls.

Accelerating faster than any other machine type, palletizers are projected to post a 9.64% CAGR through 2030. E-commerce fulfillment centers rely on robotic palletizers to absorb surging parcel throughput and to offset warehouse labor shortages. These robots reduce workplace injuries by automating manual lifting tasks and trim cycle times through high-speed end-of-line automation. The packaging machinery retrofitting and upgrading market share held by palletizers is therefore set to enlarge as distribution hubs prioritize modular robot cells capable of fit-to-order case stacking. Retrofit kits that enable traditional in-line palletizers to integrate collaborative robots without altering the conveyor layout further accelerate adoption.

By Service Type: Mechanical Retrofits Hold Share While Control Systems Advance

Mechanical retrofits accounted for 31.78% of the packaging machinery retrofitting and upgrading market share in 2024 and remain pivotal because motor swaps, guide-rail adjustments, and precision part replacements can add 8-12 years of service life. Yet the control-system upgrade category grows quickest at an 8.78% CAGR as manufacturers race to embed cybersecurity layers, industrial Ethernet connectivity, and real-time analytics. Modern PLCs and HMIs enable remote service that slashes on-site technician visits, particularly valued by multinational plant networks.

Software-centric enhancements, such as AI-driven inline optimization, digital twins, and recipe management systems, raise overall equipment effectiveness by 15-25% and help standardize performance across geographically dispersed sites. Energy-efficiency services attract attention where government grants fund servo conversions and power-factor correction. Meanwhile, safety-and-compliance retrofit packages bundle vision inspection, automatic reject mechanisms, and audit-ready documentation to simplify FDA or EMA validation cycles. The packaging machinery retrofitting and upgrading market size tied to services is therefore shifting from commodity parts replacement toward consultative offerings that blend operational technology with information technology.

By End-user Industry: Consumer Peaks and Logistics Momentum

Food and beverage processors represented 40.64% of the packaging machinery retrofitting and upgrading market size in 2024 because hygiene upgrades and allergen-control capabilities are non-negotiable. Processors migrate to stainless-steel contact zones, automatic clean-in-place subsystems, and digital traceability to stay audit-ready. Demand continues to grow for multi-pack flexibility to serve omnichannel grocery formats and single-serve convenience.

E-commerce and logistics are the fastest-growing end-user sectors, with a 9.15% CAGR forecast to 2030. Fulfillment centers require rapid box-on-demand erection, smart labeling, and robotic palletizing to satisfy tight ship-cutoff times. Retrofitting existing equipment with dimensioning scanners and variable-data printers helps carriers minimize void fill and avoid volumetric shipping penalties. As last-mile delivery innovations proliferate, parcel hubs seek upgrade packages that integrate with route-optimization software, anchoring strong future demand for the packaging machinery retrofitting and upgrading market.

Geography Analysis

The Asia-Pacific region accounted for 35.61% of the packaging machinery retrofitting and upgrading market share in 2024 and is expected to post the highest CAGR of 9.28% from 2024 to 2030. China’s Made in China 2025 program earmarked CNY 1.04 trillion (USD 150 billion) for smart manufacturing subsidies, pushing factories to layer sensors and automation atop legacy lines.[3]China State Council, “Made in China 2025 Progress Report,” GOV.CN India’s Production Linked Incentive scheme channels INR 73 billion (USD 877 million) into pharmaceutical and food-processing upgrades. Southeast Asian exporters quickly adapt to meet the strict food-safety standards imposed by importing regions, sustaining robust demand among Thai, Vietnamese, and Indonesian producers. Access to competitively priced local engineering labor further compresses implementation timelines.

North America and Europe form the mature core of installed equipment, which is aged well beyond its optimal life. European processors invested EUR 2.8 billion (USD 3.1 billion) in retrofit projects in 2024 to meet the EU Green Deal's requirements and counter rising power prices. The FDA’s heightened Good Manufacturing Practice enforcement likewise triggered USD 1.9 billion in pharmaceutical packaging upgrades across the United States and Canada. Shrinking skilled labor pools intensify adoption of automation-heavy retrofits that brighten safety profiles and cut dependency on scarce technicians.

South America, the Middle East, and Africa together register lower current shares, but modernization is accelerating in export-oriented niches. Brazil’s food sector alone invested BRL 2.1 billion (USD 420 million) in 2024 to secure export certifications, while Mexican maquiladora plants retrofit to align with U.S. retailer specifications. Gulf pharmaceutical packagers pursue halal qualification and temperature-controlled logistics, lifting demand for retrofit kits that embed cold-chain sensors. South Africa and Nigeria serve as early adopters on the continent, although financing barriers slow broad deployment elsewhere. Overall, regional uptake maps closely to trade access aspirations and government incentives, not merely economic scale.

Competitive Landscape

The market remains moderately fragmented, with no single player accounting for more than a double-digit share of revenue. Global OEMs, such as Syntegon Technology, Krones AG, and GEA Group, leverage their longstanding equipment footprints and offer all-inclusive upgrade contracts that bundle hardware, software, and lifecycle services. Retrofit revenue now accounts for 25-35% of their sales mix, up from under 20% five years ago. Digital integration prowess rather than mechanical superiority defines leadership; firms with cloud-enabled analytics platforms and validated cybersecurity frameworks secure repeat business.

Middle-tier contenders differentiate themselves by focusing on high-growth niches, such as pharmaceutical serialization, sustainable material retrofits, and flexible palletizing cells for e-commerce hubs. Patent activity surrounding predictive maintenance, vision-guided robotics, and digital twins rose 23% in 2024. Independent service providers fill geographic gaps where OEM coverage is thin, particularly across emerging Asia and Latin America, although they contend with scale limitations.

Strategic moves in 2024 underscore the shift toward service-centric value propositions. Syntegon rolled out phased upgrade programs that maintain production during the installation process. Krones invested EUR 45 million (USD 50 million) in regional centers to expand digital-twin support. GEA’s acquisition of a controls specialist augments its software bench strength, while Sidel’s partnership with Microsoft integrates Azure IoT into retrofit packages. Financing innovations also surface as Barry-Wehmiller launched a retrofit-specific lending product aimed at midsize manufacturers. Collectively, these actions demonstrate a shift in the industry toward data-driven services that foster long-term customer relationships.

Packaging Machinery Retrofitting And Upgrading Industry Leaders

Syntegon Technology GmbH

Krones AG

Sidel Group

GEA Group AG

Ishida Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: GEA Group unveiled a cloud-native retrofit monitoring suite, scheduled for global rollout in Q3 2025.

- October 2024: Syntegon Technology launched its comprehensive retrofit program targeting pharmaceutical packaging lines, offering modular upgrades for serialization compliance.

- September 2024: Krones AG announced a EUR 45 million (USD 50 million) expansion of its retrofit service network with new Asia-Pacific hubs.

- August 2024: GEA Group completed the acquisition of a specialized control-systems company to bolster food-safety upgrade capabilities.

Global Packaging Machinery Retrofitting And Upgrading Market Report Scope

| Filling Machines |

| Wrapping and Bundling Machines |

| Labeling Machines |

| Form-Fill-Seal Machines |

| Cartoning and Case Packing Machines |

| Palletizing Machines |

| Other Machine Types |

| Mechanical Retrofit |

| Software and Automation Upgrade |

| Energy-Efficiency Retrofit |

| Safety and Compliance Upgrade |

| Control System Upgrades |

| Other Service Types |

| Food and Beverage |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| Consumer Goods |

| E-Commerce and Logistics |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Machine Type | Filling Machines | ||

| Wrapping and Bundling Machines | |||

| Labeling Machines | |||

| Form-Fill-Seal Machines | |||

| Cartoning and Case Packing Machines | |||

| Palletizing Machines | |||

| Other Machine Types | |||

| By Service Type | Mechanical Retrofit | ||

| Software and Automation Upgrade | |||

| Energy-Efficiency Retrofit | |||

| Safety and Compliance Upgrade | |||

| Control System Upgrades | |||

| Other Service Types | |||

| By End-user Industry | Food and Beverage | ||

| Pharmaceuticals | |||

| Cosmetics and Personal Care | |||

| Consumer Goods | |||

| E-Commerce and Logistics | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the global packaging machinery retrofitting and upgrading market?

The market reached USD 9.45 billion in 2025 and is forecast to climb to USD 13.34 billion by 2030.

Which machine category is attracting the most investment for retrofitting?

Filling machines lead in share at 27.67% because hygiene and dosing accuracy upgrades align with tightening food-safety rules.

Why are control-system upgrades growing faster than mechanical refurbishments?

Modern PLCs, IoT connectivity, and cybersecurity layers drive an 8.78% CAGR as plants seek digital insights and remote service.

Which region offers the strongest growth outlook?

Asia-Pacific combines a 35.61% current share with a projected 9.28% CAGR, supported by government incentives for smart manufacturing.

How do manufacturers justify the capital cost of retrofits?

Upgrades typically provide 70-80% of new-machine performance at 60-70% of the cost and often pay back within two years through efficiency gains.

What emerging trend will most influence retrofit strategies through 2030?

AI-enabled predictive maintenance, which can cut unplanned downtime by up to 45%, is poised to reshape maintenance budgets and service models.

Page last updated on: