Tenant Billing Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

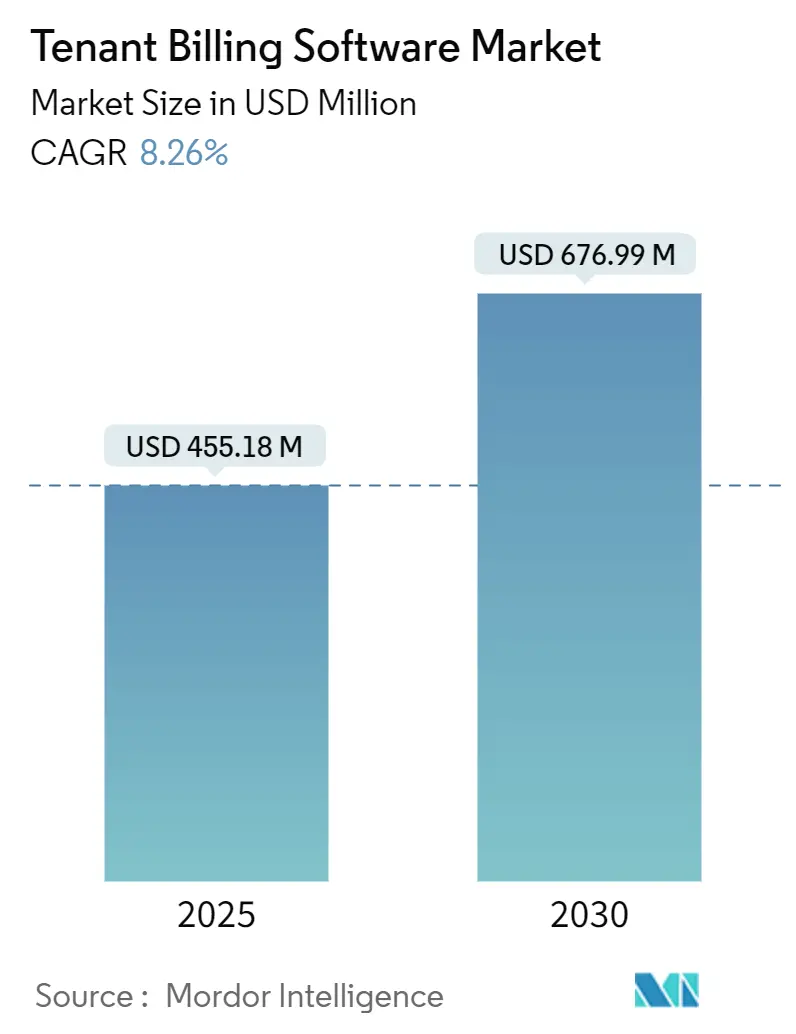

| Market Size (2025) | USD 455.18 Million |

| Market Size (2030) | USD 676.99 Million |

| Growth Rate (2025 - 2030) | 8.26% CAGR |

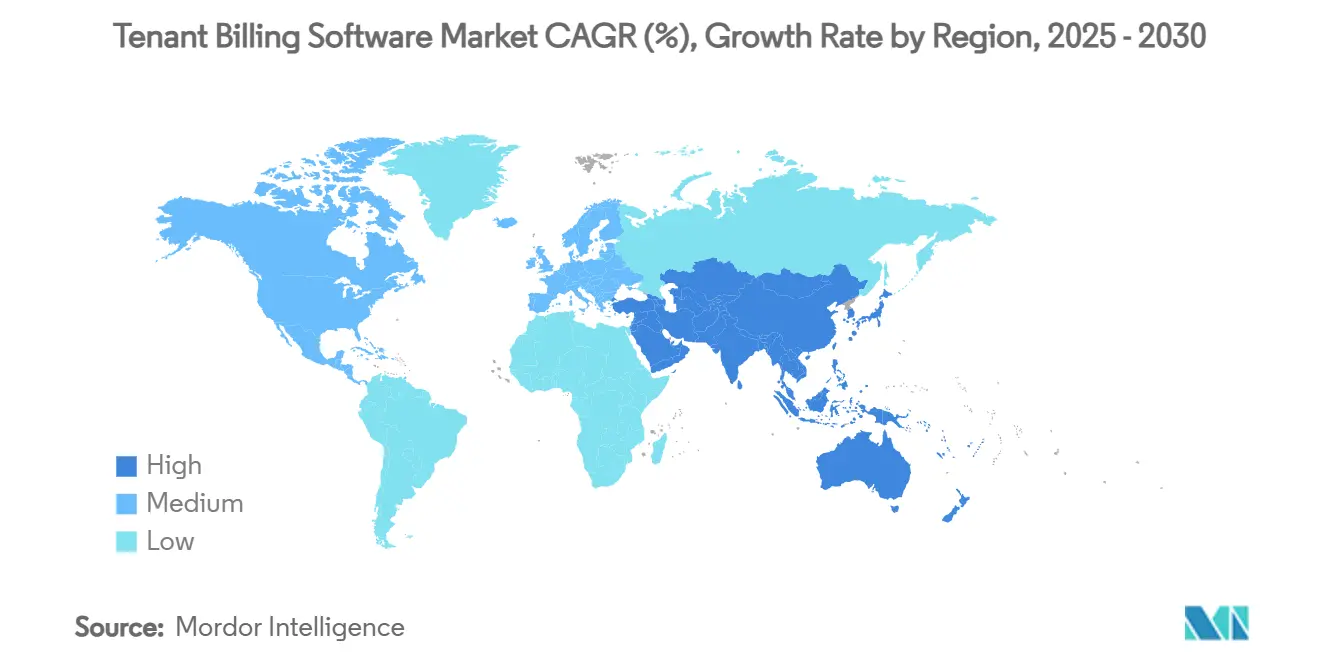

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tenant Billing Software Market Analysis by Mordor Intelligence

The tenant billing software market size is valued at USD 455.18 million in 2025 and is projected to reach USD 676.99 million by 2030, reflecting an 8.26% CAGR during the forecast period. Growing regulatory demands for transparent utility cost recovery, rapid cloud adoption across property-management stacks, and rising institutional ownership of rental assets collectively shape an environment where automated billing platforms have become critical for operational efficiency. Property managers now view compliance functionality as a competitive differentiator because penalties for inaccurate allocations rise alongside municipal oversight. Venture-capital inflows into PropTech continue to finance sophisticated analytics engines that identify billing anomalies and reduce dispute costs, while artificial intelligence tools shorten reconciliation cycles and improve tenant satisfaction. The market trajectory also mirrors broader real-estate digital transformation trends, with cloud-native ecosystems enabling platform interoperability and mobile self-service, thereby easing tenant onboarding and reducing administrative overhead.

Key Report Takeaways

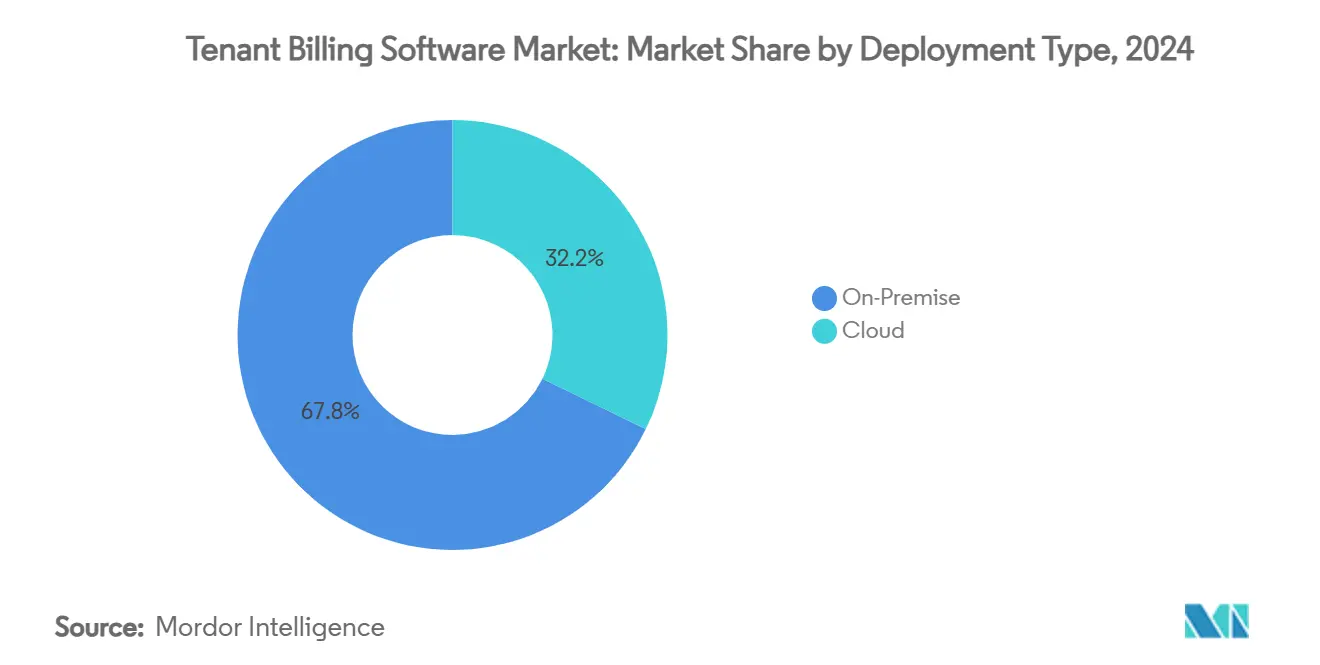

- By deployment type, on-premise solutions commanded 67.8% of the tenant billing software market share in 2024, while cloud platforms are advancing at a 10.1% CAGR to 2030.

- By pricing model, subscription-based SaaS held 58.1% share of the tenant billing software market size in 2024; hybrid and tiered models record the highest projected CAGR at 9.5% through 2030.

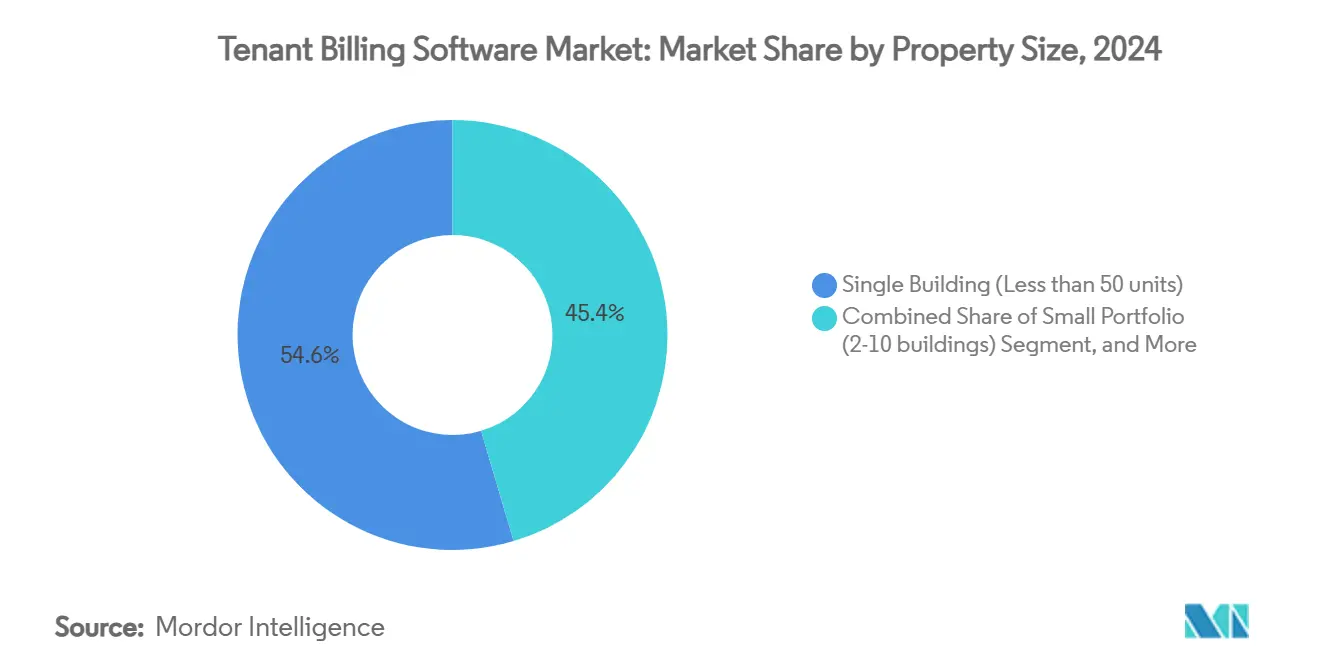

- By property size, single-building operators accounted for 54.6% of the tenant billing software market size in 2024, whereas portfolio managers with more than 10 buildings are growing at 9.2% CAGR through 2030.

- By end user, residential property managers held 49.8% share of the tenant billing software market in 2024 and co-living or co-working operators are advancing at an 8.7% CAGR to 2030.

- By geography, North America led with 36.5% revenue share of the tenant billing software market in 2024, whereas Asia-Pacific is forecast to expand at an 8.4% CAGR through 2030.

Global Tenant Billing Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift of property-management stacks to cloud ecosystems | +1.5% | Global, early adoption in North America and EU | Medium term (2–4 years) |

| Widening regulatory mandates on utility cost recovery and transparency | +1.8% | North America and EU core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Growing VC funding into PropTech billing platforms | +1.2% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| Integration of AI-based billing analytics reducing dispute costs | +1.1% | North America and EU with spill-over to Asia-Pacific | Medium term (2–4 years) |

| Demand from co-living and flexible workspace operators | +0.9% | Global, urban centers | Medium term (2–4 years) |

| Expansion of Energy-as-a-Service models requiring granular invoicing | +0.7% | North America and EU, early Asia-Pacific uptake | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift of Property-Management Stacks to Cloud Ecosystems

Property managers accelerated cloud migration to enable remote collaboration when on-site access became restricted in 2024. Operators cite lower infrastructure overhead, automatic security patches, and seamless disaster recovery among the reasons on-premise servers are being phased out. Cloud deployment also simplifies integration with payment processors, smart-meter feeds, and resident portals, improving data accuracy while reducing manual reconciliations. As procurement teams recognize predictable subscription fees as operating rather than capital expenditures, purchasing cycles shorten even for mid-market firms. Legacy vendors are responding with hybrid rollouts that keep sensitive ledgers on-premise while shifting tenant-facing modules to secure public clouds, yet user preference continues to tilt toward fully hosted models that eliminate maintenance costs.

Widening Regulatory Mandates on Utility Cost Recovery and Transparency

Jurisdictions ranging from California to Seattle require upfront disclosure of all mandatory billing fees, compelling landlords to present itemized statements that withstand audit scrutiny. Arizona stipulates separate disclosure of administrative utility fees, whereas Virginia now mandates clear fee descriptions in rental agreements.[1]Arizona Legislature, “Utility Charges; Submetering; Ratio Utility Billing,” azleg.gov Compliance complexity magnifies when portfolios span multiple states, prompting owners to adopt software that embeds jurisdiction-specific rules directly in invoice logic. Municipal oversight is backed by rising penalty schedules that elevate compliance from an operational detail to a board-level concern. As the transparency trend broadens to Asia-Pacific markets, platforms able to generate multi-lingual statements and maintain immutable audit trails become indispensable.

Growing VC Funding into PropTech Billing Platforms

Global PropTech funding topped USD 1.491 billion in Q1 2024, with investors channeling resources toward mature billing solutions that scale rapidly across geographies. Late-stage rounds favor providers embedding predictive analytics because these features boost retention by cutting dispute-handling costs. Capital availability enables smaller innovators to acquire niche compliance engines or penetrate emerging markets faster than organic growth would allow. As cost of capital normalizes, platforms demonstrating clear paths to profitability gain leverage in partnership negotiations with large property operators. Continued investment therefore sustains a healthy pipeline of feature enhancements that elevate user expectations across the tenant billing software market.

Integration of AI-Based Billing Analytics Reducing Dispute Costs

Artificial intelligence now predicts which invoices will be contested by analyzing historic utility data, socioeconomic factors, and seasonal consumption anomalies. Platforms report raising collection rates from 97.6% to 99.6% after embedding machine-generated recommendations that flag inconsistencies before invoices post. Generative chat interfaces guide residents through self-service queries and automate documentation of any adjustments, creating comprehensive audit trails without human intervention. The resulting decline in manual dispute resolution frees on-site teams to focus on resident experience while reducing operating expenses at portfolio scale. These performance gains justify premium license tiers and accelerate the transition away from commoditized legacy systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented compliance standards across municipalities | –0.8% | Global, especially North America | Long term (≥ 4 years) |

| Landlord resistance to SaaS subscription fee escalation | –0.6% | Global, stronger in emerging markets | Medium term (2–4 years) |

| Cyber-security concerns around tenant payment data | –0.5% | Global, high-regulation markets | Short term (≤ 2 years) |

| Slow digital adoption among small multi-family owners in emerging nations | –0.4% | Asia-Pacific, Latin America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Compliance Standards Across Municipalities

Regulatory fragmentation forces vendors to embed hundreds of rule variations into billing engines, inflating development budgets and prolonging update cycles.[2]Public Utility Commission of Texas, “Tenant Guide to Allocated Water/Wastewater Service,” puc.texas.gov Multi-state landlords often juggle multiple solutions because no single platform covers every local ordinance, undercutting desired economies of scale. Continuous monitoring of municipal council agendas has become a core product-management function for software firms, reducing resources available for new feature innovation. Smaller vendors lacking legal-affairs teams struggle most, which accelerates industry consolidation but also slows overall feature rollout velocity. The result is an uneven adoption curve, especially in secondary markets where landlords perceive compliance risk as lower.

Landlord Resistance to SaaS Subscription Fee Escalation

Recurring fees that rise faster than inflation draw scrutiny among owners operating with compressed margins, leading some to postpone upgrades or revert to manual invoicing. When annual software spend exceeds 2% of gross rent, procurement officers initiate competitive reviews that favor lower-cost entrants. Vendors counter resistance by unbundling premium analytics into optional modules, yet this approach can fracture user experience and complicate support. In emerging markets where local landlords rely on cash collections, the perceived value of automated billing remains low until regulatory imperatives force modernization, slowing uptake in price-sensitive segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Acceleration Despite On-Premise Dominance

On-premise deployments held 67.8% of tenant billing software market size in 2024, but cloud platforms are scaling at a 10.1% CAGR that will narrow the gap by 2030.Large institutional landlords increasingly use hybrid configurations that store rent ledgers locally while enabling tenant self-service through cloud portals. In the mid-market, cost avoidance for server upkeep drives straight-to-cloud migrations, and vendors offering migration toolkits remove friction. Compliance modules update automatically in hosted environments, eliminating version lags that once exposed owners to penalties. Smaller operators benefit from pay-as-you-grow pricing and minimal IT overhead, reinforcing the long-term pivot toward hosted services across the tenant billing software market.

Rising cyber-security standards favor cloud providers that certify to SOC 2 and ISO 27001, credentials smaller on-premise installations rarely hold. Cloud ecosystems also integrate with IoT devices that capture live utility data, a requirement for Energy-as-a-Service partnerships. These integrations future-proof properties by enabling usage-based tariffs that tenants increasingly demand. As 5G connectivity proliferates, real-time data ingestion will strengthen use cases for predictive analytics, further positioning cloud deployments as the strategic default for new construction and major retrofits.

By Pricing Model: SaaS Leadership with Hybrid Growth Momentum

Subscription contracts controlled 58.1% tenant billing software market share in 2024, reflecting buyer preference for predictable annual budgets. Hybrid structures that layer usage fees atop a base subscription are expanding at 9.5% CAGR because they align costs with unit counts and seasonal occupancy. Transaction-based pricing resonates with flexible workspace operators that experience material fluctuations in invoice volumes. Enterprise landlords increasingly negotiate gain-share components where vendors receive incentives tied to dispute-rate reductions, deepening alignment on performance outcomes within the tenant billing software market size context.

Price-sensitive owners employ tiered plans that cap feature usage, but compliance obligations often push them toward higher tiers over time. Vendors therefore design modular upgrades that unlock jurisdictional rule libraries or AI anomaly detection as optional add-ons. This upsell pathway boosts average revenue per user while keeping entry prices attractive. Competitors that fail to articulate transparent cost escalators risk churn as procurement teams benchmark alternative suppliers.

By Property Size: Single-Building Prevalence with Portfolio Consolidation

Single-building owners captured 54.6% of the tenant billing software market size in 2024, underscoring the sector’s fragmentation. Yet managers of more than 10 buildings are expanding at 9.2% CAGR as institutional investment consolidates units into large funds that favor standardized platforms. Portfolio operators maximize scale economies by centralizing utility procurement and automating allocations across thousands of tenants, elevating their willingness to purchase AI-driven analytics. Mid-sized landlords bridge manual processes and enterprise solutions, making them prime targets for vendors promoting bundled onboarding services.

Investor appetite for build-to-rent continually injects new large-scale assets that deploy billing software from day one rather than retrofitting later. In parallel, regulatory tightening increases the compliance burden for single-building owners, compelling them to adopt light-weight SaaS in order to avoid fines. Consequently, every size category remains addressable, although value perception and feature prioritization differ markedly across cohorts.

By End User: Residential Focus with Co-Living Acceleration

Residential managers represented 49.8% of tenant billing software market demand in 2024, reflecting the massive apartment and single-family rental inventory across mature economies. Co-living and co-working operators, however, are scaling revenue fastest at 8.7% CAGR because their flexible lease structures necessitate granular, usage-based invoicing. These operators often integrate access-control data to allocate costs precisely, pushing software capabilities beyond traditional square-footage formulas.

Student housing, senior living, and mixed-use campus developers also require specialized billing logic, including prorated, mid-term move-ins and shared utility zones. Vendor roadmaps therefore prioritize configurable tariff engines and real-time consumption dashboards. Commercial landlords remain a stable but less dynamic segment, primarily leveraging billing modules to automate triple-net pass-throughs rather than competitive differentiation. Utility companies and Energy-as-a-Service firms are emerging secondary customers adopting the software to manage tenant-level settlements for distributed generation assets.

Geography Analysis

North America maintained 36.5% tenant billing software market share in 2024, propelled by strict transparency statutes and investor expectations for data-rich asset performance dashboards. Federal antitrust challenges to RealPage underline the policy spotlight on pricing practices, encouraging property managers to pivot toward platforms that foreground compliance safeguards. The region’s leadership in machine-learning adoption translates into early deployment of predictive dispute resolution, reinforcing the competitive moat for vendors with robust AI roadmaps.

Asia-Pacific posts the highest regional CAGR at 8.4%, driven by urbanization, government-backed build-to-rent projects, and private-credit funding that accelerates ground-up development.[3]Herbert Smith Freehills, “APAC Real Estate Sector Insights Q4 2024,” hsfkramer.com Countries such as Australia and Japan introduce energy-efficiency disclosure mandates that require meter-level billing, boosting demand for cloud platforms that integrate with smart-building systems. Localization needs—multi-language interfaces and region-specific payment rails-create entry barriers that global vendors address through partnerships or acquisitions.

Europe advances steadily as GDPR compliance and tenant-protection directives favor providers with mature security frameworks. Many continental landlords embrace hybrid deployments that keep personal data on EU servers while exploiting public-cloud elasticity for analytics. South America and the Middle East & Africa contribute smaller revenue slices yet offer long-term upsides as connectivity gaps close and institutional investors expand holdings. Nigerian reforms to digitize land records, for instance, foreshadow future momentum once broadband coverage improves.

Competitive Landscape

The tenant billing software market remains moderately fragmented. Yardi Systems, RealPage, and MRI Software hold scale advantages via integrated property-management suites that bundle rent collections, maintenance, and resident engagement. Their extensive customer bases create high switching hurdles; nevertheless, Department of Justice litigation against RealPage catalyzes a search for alternative platforms. New entrants focus on transparency, open APIs, and AI-native architectures to differentiate from incumbents perceived as monolithic.

AppFolio’s 2024 release of Realm-X illustrates how conversational AI elevates user experience and commands premium pricing tiers. Specialized challengers like Azibo and Hemlane target small-portfolio landlords through simplified onboarding and free basic plans that convert to paid tiers as unit counts grow. Venture-backed innovators invest in compliance engines that auto-update municipal rule sets, a capability especially attractive to multi-state landlords wary of regulatory drift.

Strategic alliances also influence market dynamics. SmartRent leverages smart-home installations to embed billing directly into connected devices for seamless tenant engagement. Meanwhile, energy-service companies partner with billing vendors to manage tenant shares of performance-based contracts, signaling ecosystem convergence between sustainability tech and traditional property software. Competitive intensity is expected to rise as consolidation accelerates and compliance expectations scale across regions.

Tenant Billing Software Industry Leaders

SAP SE

Oracle Corporation

Yardi Systems, Inc.

RealPage, Inc.

MRI Software LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The U.S. Department of Justice filed an amended complaint expanding antitrust allegations against RealPage, citing additional anticompetitive practices in billing software.

- August 2024: DOJ filed a comprehensive antitrust suit against RealPage, alleging rental pricing collusion facilitated by its algorithms.

- April 2024: A surge in global searches for property-management software highlighted accelerating digital transformation in real estate.

- January 2024: AppFolio unveiled Realm-X, the first generative AI conversational interface for property management workflows.

Global Tenant Billing Software Market Report Scope

| Cloud |

| On-Premise |

| Subscription (SaaS) |

| Per-Invoice / Usage-Based |

| Hybrid / Tiered |

| Single Building (Less than 50 units) |

| Small Portfolio (2-10 buildings) |

| Large Portfolio (More than 10 buildings) |

| Residential Property Managers |

| Commercial Property Managers |

| Co-living / Co-working Operators |

| Utility Companies and ESCOs |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Deployment Type | Cloud | |

| On-Premise | ||

| By Pricing Model | Subscription (SaaS) | |

| Per-Invoice / Usage-Based | ||

| Hybrid / Tiered | ||

| By Property Size | Single Building (Less than 50 units) | |

| Small Portfolio (2-10 buildings) | ||

| Large Portfolio (More than 10 buildings) | ||

| By End-User | Residential Property Managers | |

| Commercial Property Managers | ||

| Co-living / Co-working Operators | ||

| Utility Companies and ESCOs | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the tenant billing software market size in 2025?

The tenant billing software market size is valued at USD 455.18 million in 2025.

What CAGR is forecast for the tenant billing software market between 2025 and 2030?

The market is projected to expand at an 8.26% CAGR during the 2025-2030 period.

Which region is growing fastest in the tenant billing software market?

Asia-Pacific is the fastest-growing region, advancing at an 8.4% CAGR through 2030.

Which deployment model is gaining share despite on-premise dominance?

Cloud-based platforms are accelerating at a 10.1% CAGR while on-premise still holds the largest share.

Which end-user segment shows the highest growth momentum?

Co-living and co-working operators exhibit the strongest growth at an 8.7% CAGR owing to their need for granular, usage-based invoicing.

How concentrated is the competitive landscape in tenant billing software?

The market earns a concentration score of 6 because the top three vendors hold roughly 45% combined share, leaving room for numerous regional and niche providers.

Page last updated on: