Subscription Billing Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

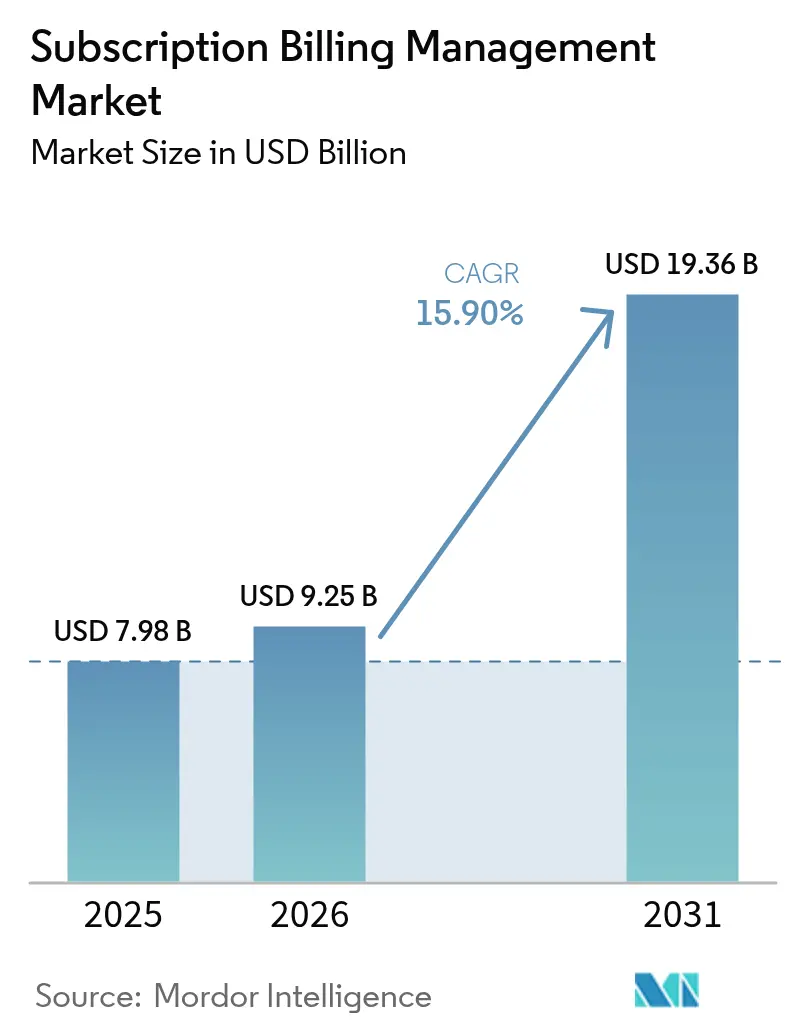

| Market Size (2026) | USD 9.25 Billion |

| Market Size (2031) | USD 19.36 Billion |

| Growth Rate (2026 - 2031) | 15.90% CAGR |

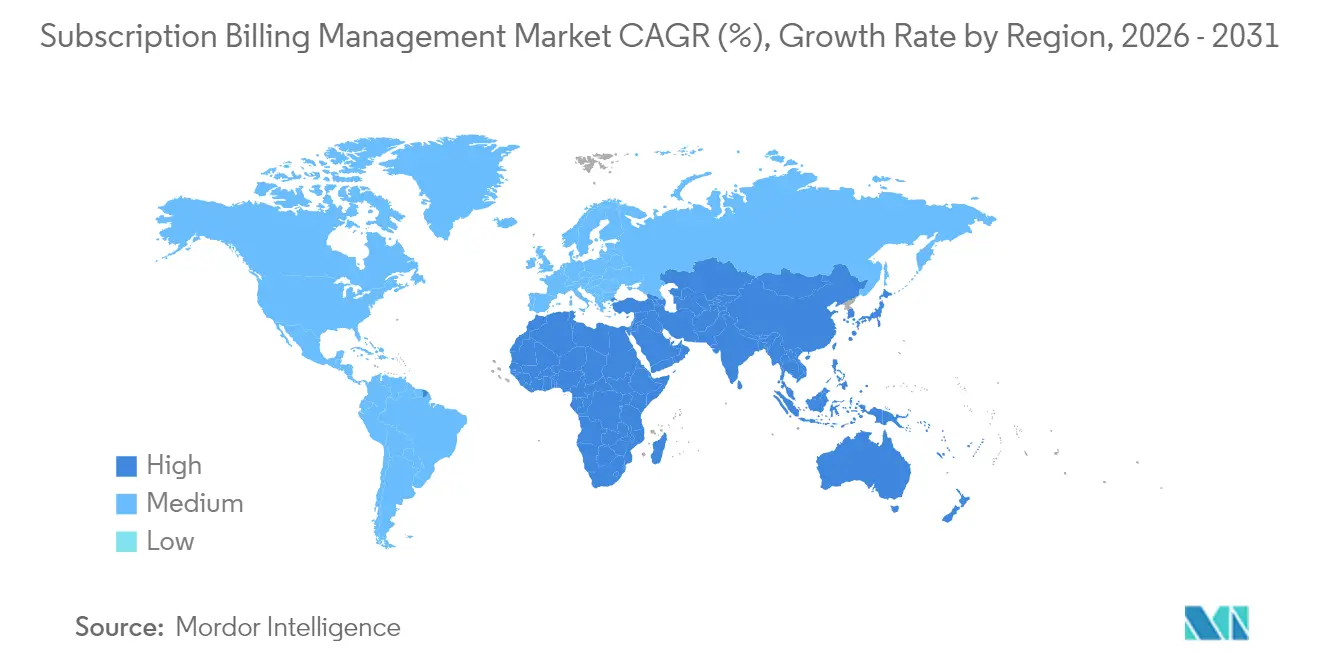

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

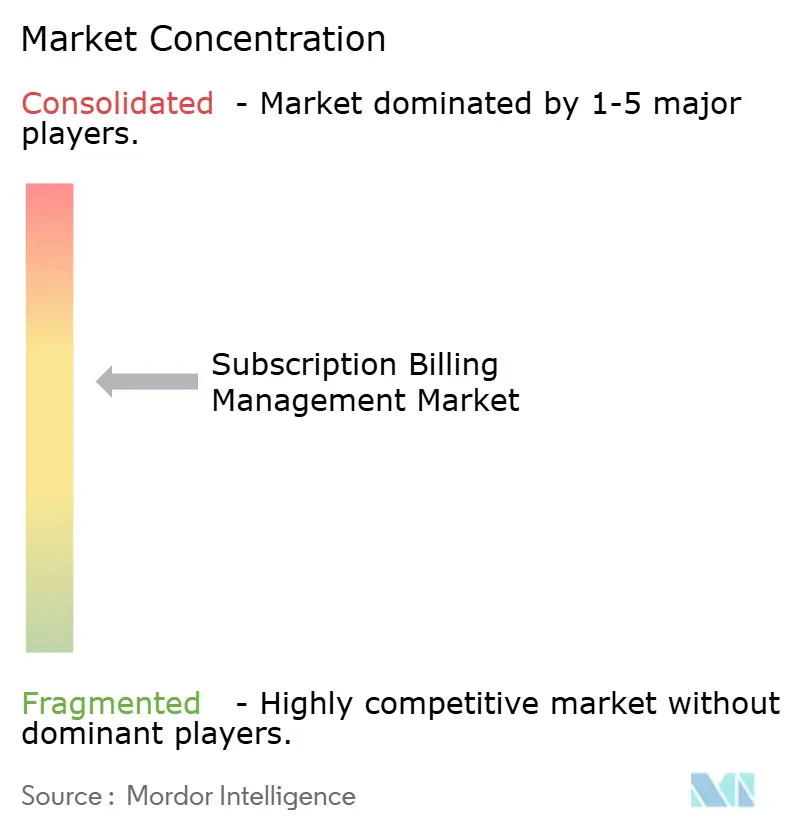

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Subscription Billing Management Market Analysis by Mordor Intelligence

Subscription billing management market size in 2026 is estimated at USD 9.25 billion, growing from 2025 value of USD 7.98 billion with 2031 projections showing USD 19.36 billion, growing at 15.9% CAGR over 2026-2031. The surge comes from the rapid pivot to recurring-revenue frameworks, expanded consumption-based pricing among cloud providers, and regulations that require transparent invoice practices. Cloud deployment holds centre stage as enterprises retire on-premise stacks in favour of elastic, maintenance-free billing engines that integrate easily with global payment networks. Usage-aligned models are expanding fastest in telecom, infrastructure-as-a-service, and e-commerce, all of which demand real-time metering, multi-factor authentication, and embedded fraud controls. Competitive intensity remains high as enterprise software majors such as Oracle and SAP defend their installed bases against digital-native specialists such as Stripe, Zuora, Chargebee, and Recurly. Long-term tailwinds outweigh near-term headwinds from payment-fraud escalation, data-sovereignty mandates, and integration complexity, signalling a structural rather than cyclical growth profile.

Key Report Takeaways

- By deployment mode, cloud delivery commanded 75.35% of the subscription billing management market share in 2025; hybrid cloud is advancing at an 18.05% CAGR through 2031.

- By component, platform software held an 79.40% revenue share in 2025, while services are forecast to expand at a 19.05% CAGR through 2031.

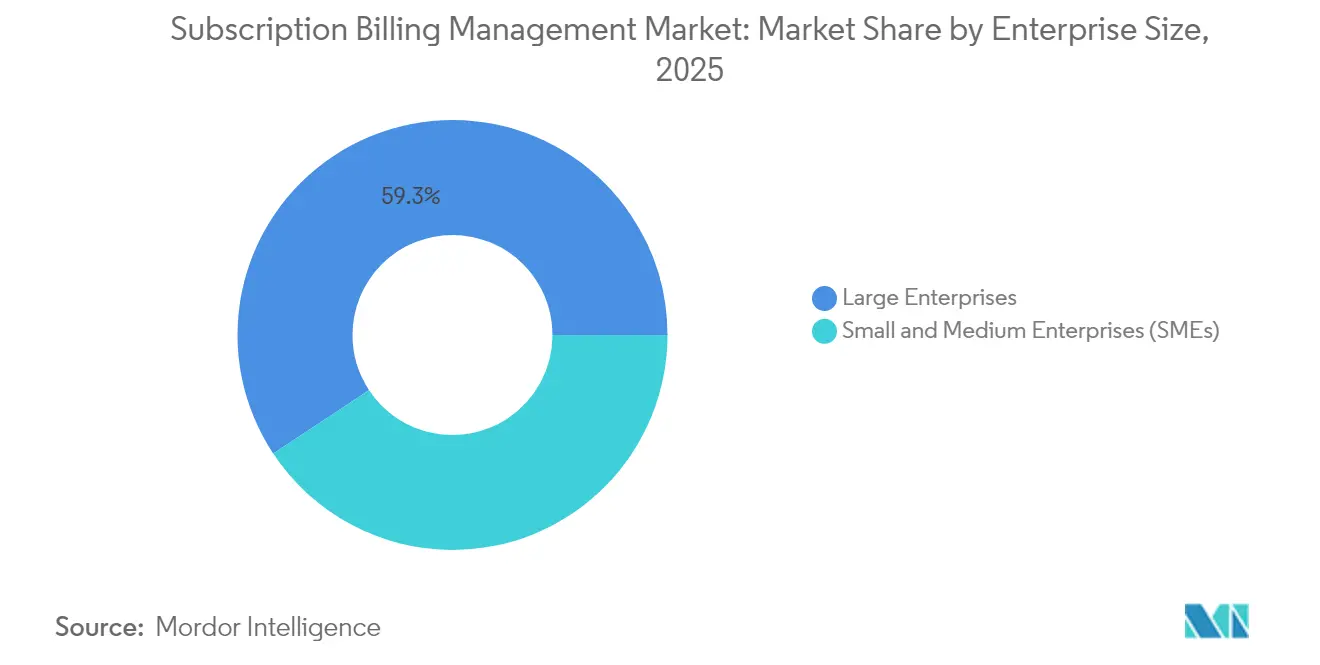

- By enterprise size, large enterprises accounted for 59.30% of the subscription billing management market size in 2025, whereas SMEs are growing fastest at a 20.25% CAGR through 2031.

- By end-user industry, IT and telecom retained 29.70% share in 2025; retail and e-commerce is projected to rise at a 21.35% CAGR to 2031.

- By geography, North America led with 39.60% share in 2025, while Asia–Pacific is set to climb at a 21.05% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Subscription Billing Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acceleration of as-a-Service monetization in telecom and media in North America | +3.2% | North America, spill-over to EU | Medium term (2-4 years) |

| Emergence of consumption-based pricing among cloud infrastructure vendors | +4.1% | Global, led by North America and APAC | Short term (≤ 2 years) |

| Regulatory push for transparent recurring billing under EU PSD2-SCA | +2.8% | EU core, expanding to MEA | Long term (≥ 4 years) |

| Digital-wallet and real-time-payment integration driving retail subscriptions in Asia | +3.7% | APAC core, spill-over to Latin America | Medium term (2-4 years) |

| Shift from perpetual licensing to SaaS in industrial software verticals | +2.6% | Global, early gains in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

As-a-Service monetization accelerates telecom revenue diversification

Telecom groups are pairing 5 G connectivity with entertainment, IoT, and edge-compute bundles, using unified billing engines to orchestrate multi-party revenue splits and hybrid usage plus subscription fees. T-Mobile’s Netflix-inclusive plans and Verizon’s entertainment bundles illustrate the pivot to experience-centric offerings. Modular platforms cut time-to-cash by automating rating, mediation, and partner settlement, supporting predictable cashflows while enabling micro-services experimentation. Emerging tools such as Evergent’s Digital Commerce Bridge allow operators to layer promotions and upsells dynamically, widening average revenue per user. [1]Evergent, “Evergent Launches Digital Commerce Bridge,” evergent.com

Consumption-based pricing transforms cloud infrastructure economics

AWS, Azure, and Google Cloud normalised pay-as-you-use billing, prompting enterprise clients to demand minute-level metering, threshold-based alerts, and post-usage invoicing. Snowflake’s success with usage-aligned contracts illustrates the revenue flywheel effect when customer consumption scales in lockstep with value delivered. Modern billing stacks ingest billions of usage events, apply tiered or burst prices, and reconcile taxes across regions in real time. Vendors report higher customer retention because smaller entry commitments reduce buyer friction, while upsell paths are embedded in data-driven price curves.

EU PSD2-SCA mandates reshape payment authentication standards

Strong Customer Authentication now requires two security factors for recurring payments, tightening fraud prevention but adding friction at checkout. Merchants achieving low chargeback ratios and ticket values under EUR 30 qualify for exemptions, yet they must demonstrate real-time risk scoring to issuers. [2]ProcessOut, “PSD2 SCA Guide for Recurring Payments,” processout.com Global SaaS providers have overhauled their billing APIs to invoke step-up verification only when risk thresholds trip, protecting conversion rates while complying with audits. Investments in risk-based authentication are rising, with leading payment gateways integrating machine-learning fraud scoring into subscription token vaults.

Digital-wallet integration accelerates Asian subscription adoption

Alipay+, PayNow, and UPI enable instant domestic and cross-border micropayments, lowering the cost of monthly or even daily subscription charges. India processed 129.3 billion real-time transactions in 2023, far ahead of any other market, setting a scalable template for bundled content, education, and micro-insurance offers. Unified QR-code frameworks across ASEAN markets and government support for data-protection parity are smoothing compliance for regional-wide billing rollouts. Merchants embed wallet-native checkout buttons that pre-fill KYC data and authorise auto-debit mandates, reducing churn from failed card renewals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising payment-fraud and charge-back cost in cross-border recurring payments | -2.1% | Global, acute in cross-border markets | Short term (≤ 2 years) |

| Legacy ERP/CRM integration complexity for large enterprises | -1.8% | North America and EU enterprise markets | Medium term (2-4 years) |

| Data-sovereignty rules limiting centralized billing in EU and MEA | -1.4% | EU core, expanding to MEA | Long term (≥ 4 years) |

| High switching costs curbing SMB migration from home-grown systems | -1.2% | Global SME markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Payment-fraud escalation threatens cross-border subscription models

Global fraud losses hit USD 485 billion in 2023, with authorised push-payment scams surging as consumers are tricked into approving legitimate-looking transfers. [3]European Payments Council, “Payment Threats and Fraud Trends Report 2024,” europeanpaymentscouncil.eu Subscription merchants must balance frictionless renewal flows with strong anti-fraud layers, funding AI-powered pattern-recognition tools that cut false positives and retain customer trust. Regulatory responses such as the UK reimbursement mandate shift liability to payment firms, intensifying investment in adaptive risk engines and network-wide anomaly detection.

Legacy integration complexity delays enterprise billing modernisation

Multinational companies often sit on decades-old ERP and CRM suites that require custom connectors, data cleanses, and workflow re-engineering before subscription engines can go live. Projects stretch 12–18 months and entail high professional-services costs, limiting rollout velocity. Europe’s cloud users have flagged unfair legacy licensing practices that added EUR 560 million (USD 607 million) in incremental costs for Office 365 users alone, underscoring the hidden expense of migration. Manufacturers moving from one-time CAPEX sales to SaaS demand billing systems capable of multi-year contracts, multi-entity taxation, and channel partner splits, adding further complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud infrastructure dominates migration

Cloud deployment contributed 75.35% of 2025 revenue, underpinned by demand for auto-scaling, globally distributed billing engines that offload maintenance overheads. The subscription billing management market size for cloud deployment is expanding at an 18.05% CAGR through 2031, reflecting enterprise confidence in public-cloud security certifications and the appeal of usage-based cost structures. Stripe Billing, delivered entirely as a managed service, surpassed a USD 500 million annual run rate by supporting leading technology firms with granular metering and automated reconciliation. On-premise installations persist in highly regulated industries that require data residency guarantees, yet improved encryption and private-cloud options erode this niche.

Migration momentum is reinforced by vendor commitment to weekly release cadences, zero-downtime upgrades, and native integrations with over 40 payment gateways. Hybrid architectures—where sensitive data stays in a private environment while rating and invoicing happen in the cloud—act as transitional bridges for cautious enterprises. As cloud penetration rises, vendors invest in observability tooling that lets finance teams trace every usage event from source to invoice, mitigating audit risk and supporting Sarbanes–Oxley compliance.

By Component: Platform software leads service integration

Platform software retained 79.40% revenue share in 2025, supplying core metering, rating, and revenue management capabilities. Services, however, are growing at a 19.05% CAGR as enterprises seek advisory, integration, and managed-operations support. Vendors bundle accelerator kits, pre-built connectors, and regulatory change packs to shorten time-to-value, while partners run configuration-as-code pipelines that embed billing logic in DevOps workflows.

Consultative engagements cover pricing-model design, go-to-market readiness, and RevRec compliance, areas that finance and product teams often lack specialist resources for. The rise of low-code configuration and composable APIs widens addressable demand, but complexity spikes when firms blend tiered subscriptions with consumption overages and channel reseller margins. This services uptrend illustrates that success in the subscription billing management market depends as much on domain expertise as on software feature breadth.

By Enterprise Size: SME adoption accelerates

Large enterprises still control 59.30% revenue, yet SMEs represent the fastest-growing cohort at a 20.25% CAGR. Mobile-first consoles, preset tax rules, and pay-as-you-grow pricing remove the historical barriers that kept sophisticated billing out of reach for smaller operators. Cloud providers bundle billing modules in their marketplace stacks, enabling micro-SaaS founders to launch global subscription offers in days rather than months.

Regulatory clarity also benefits SMEs: the United States Federal Trade Commission’s Negative Option Rule, effective May 2025, obliges clear opt-out mechanisms and transparent renewals, reducing compliance guesswork. As new entrants capture niche verticals—legal-tech, creator economy, and micro-e-commerce—they fuel long-tail diversification in the subscription billing management industry, while enterprise volumes continue to underpin overall revenue stability.

By End-User Industry: Retail transformation drives growth

IT and telecom’s 29.70% share stems from 5 G monetisation and edge-compute packaging, yet retail and e-commerce is set to outpace all other verticals with a 21.35% CAGR to 2031. The segment’s adoption of buy-once-own-forever options alongside replenishment subscriptions reshapes cart economics, converting sporadic buyers into predictable lifetime value streams. Merchants integrate wallet-native one-click checkouts, loyalty-point subscriptions, and BNPL-linked memberships to lift repeat purchase frequency.

Beyond retail, BFSI institutions pilot usage-dependent digital banking fees, while utilities evaluate time-of-day pricing overlays. Healthtech platforms move from per-consultation charges to hybrid subscription plus outcome-based reimbursements, broadening the subscription billing management market footprint. Collectively, vertical diversification cushions the sector against cyclicality in any single industry.

Geography Analysis

North America generates 39.60% of global revenue, buoyed by mature SaaS penetration, established card networks, and an investor ecosystem that rewards annual recurring revenue over one-time sales. The region’s regulatory environment encourages experimentation: the California Consumer Privacy Act clarifies consent requirements without prescribing specific billing architectures, allowing vendors to innovate freely. U.S. champions such as Stripe, Zuora, and Chargebee export their platforms worldwide, with Stripe Billing alone processing subscriptions for Atlassian and OpenAI.

Asia–Pacific is the fastest-growing geography at a 21.05% CAGR. Payment innovation, notably India’s UPI and Singapore’s PayNow, lowers transaction costs and supports micro-subscription models that debit wallets in sub-USD 1 increments. ASEAN governments coordinate cross-border QR frameworks and harmonise data-protection statutes, driving regional rollouts by global merchants. China’s domestic technology stack supports vast subscription ecosystems across e-commerce, streaming, and in-game economies, though vendors must localise tax, invoicing, and data-hosting arrangements.

Europe maintains a pivotal role in shaping compliance standards through PSD2-SCA and the forthcoming EU Data Act, whose sovereignty clauses influence architecture decisions even outside the bloc. Implementation costs for U.S. vendors are projected between USD 22 billion and USD 50 billion, encouraging a shift toward distributed data-storage nodes and configurable data-sharing dashboards. Emerging regions in Latin America, the Middle East, and Africa trail in absolute value yet post double-digit growth rates as mobile penetration climbs and real-time payment rails mature.

Mordor Intelligence provides coverage of the subscription billing management market across other key regional markets, including Latin America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The subscription billing management market is moderately concentrated. Enterprise software incumbents such as Oracle, SAP, and Salesforce embed subscription modules within broader finance clouds, leveraging installed-base stickiness. Pure-play specialists Zuora, Chargebee, Recurly, and Paddle differentiate via agile roadmaps, vertical accelerators, and freemium entry tiers that resonate with high-growth digital natives. Public-cloud providers position billing as an ancillary feature—AWS Billing Console, Microsoft Azure Plan—yet they rarely extend metering to third-party services, leaving room for independent vendors.

Strategic moves cluster around three plays. First, platform consolidation: Zuora agreed in October 2024 to be acquired by GIC and Silver Lake for USD 1.7 billion, signalling that private equity sees value in combining subscriber data, pricing engines, and analytics at scale (Zuora press release). Second, vertical specialisation: Evergent targets telecom and media while Ordway courts B2B SaaS. Third, horizontal expansion: Stripe layers revenue recognition, tax, and fraud modules onto its billing rails, striving for an end-to-end monetisation suite.

Technology differentiation now centres on AI. Recurly’s February 2025 launch of machine-learning subscriber-growth tools reflects an industry-wide race to cut involuntary churn, optimise pricing, and forecast lifetime value. Vendors embed explainable AI into dashboards so finance leaders can justify price adjustments and forecast cash positions under multiple consumption scenarios. Competitive intensity is therefore defined not just by features shipped but by the pace of intelligent automation delivered.

Subscription Billing Management Industry Leaders

Salesforce.com, Inc.

SAP SE

Oracle Corporation (Netsuite)

Apttus Corporation

Amazon Web Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Recurly appointed Priya Lakshminarayanan as Chief Product Officer and unveiled AI-driven subscriber-growth modules that predict churn and recommend offers.

- January 2025: Stripe Billing surpassed a USD 500 million annual run rate, underscoring the scalability of cloud-native subscription infrastructure.

- October 2024: Zuora completed its USD 1.7 billion acquisition by GIC and Silver Lake, enabling deeper investment in global expansion and AI product roadmaps.

- October 2024: Chargebee closed a late-stage financing round, bringing cumulative funding to USD 480 million to bolster product integration and market reach (company statement).

Global Subscription Billing Management Market Report Scope

Subscription billing management enables businesses to automate their billing and invoicing processes and automatically renew their customers' subscriptions on time. It helps subscription-based businesses meet the growing demand for a reduction in billing errors by simplifying and automating the complex monetization process and establishing a new subscription billing and recurring revenue management capability.

The subscription billing management market is segmented by deployment mode (on-premise, on-cloud), size of the organization (small and medium enterprises, large enterprises), end-user industry (retail and e-commerce, BFSI, IT, and telecom, media, and entertainment, public sector, and utilities), and geography (North America, Europe, Asia-Pacific, Latin America, the Middle East, and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Software |

| Services |

| On-Premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Retail and E-commerce |

| BFSI |

| IT and Telecom |

| Media and Entertainment |

| Public Sector and Utilities |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Mode | On-Premise | ||

| Cloud | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-user Industry | Retail and E-commerce | ||

| BFSI | |||

| IT and Telecom | |||

| Media and Entertainment | |||

| Public Sector and Utilities | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the subscription billing management market and how fast is it growing?

The market is valued at USD 9.25 billion in 2026 and is forecast to rise to USD 19.36 billion by 2031, reflecting a 15.90% CAGR.

Which deployment model leads adoption in subscription billing?

Cloud deployment leads with 75.35% share in 2025 because enterprises prefer elastic, maintenance-free infrastructure that scales with usage and simplifies compliance.

Which industries are adopting subscription billing the fastest?

Retail and e-commerce show the quickest uptake at a 21.35% CAGR through 2031, driven by wallet-based checkouts and real-time payments; IT and telecom presently hold the largest share at 29.70%.

What regions present the strongest growth opportunities?

Asia–Pacific is expanding at a 21.05% CAGR as mobile-wallet penetration exceeds 90% and regulators harmonise cross-border payment standards.

What are the main challenges enterprises face when modernising billing systems?

Key obstacles include rising cross-border payment fraud, complex legacy ERP/CRM integrations that can stretch 12–18 months, and data-sovereignty rules that discourage centralised architectures.

How concentrated is the competitive landscape?

The top five vendors control roughly 60% of segment revenue, indicating moderate concentration that still leaves room for specialised and regional providers.

Page last updated on: