Climate Change Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

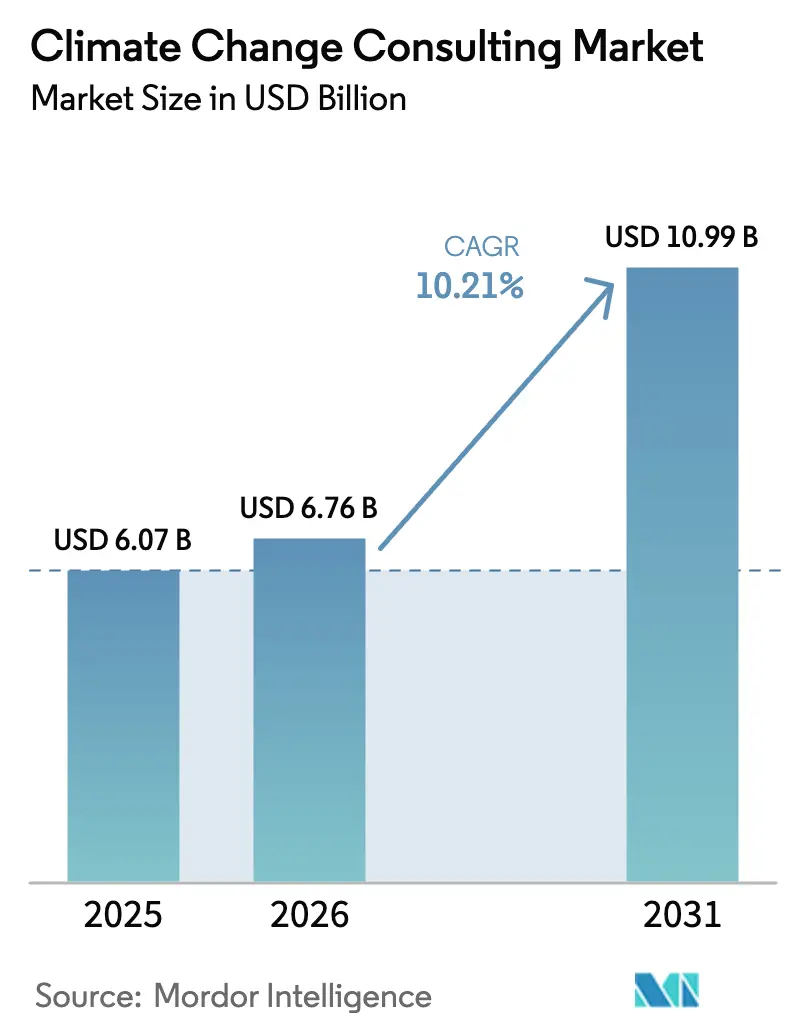

| Market Size (2026) | USD 6.76 Billion |

| Market Size (2031) | USD 10.99 Billion |

| Growth Rate (2026 - 2031) | 10.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Climate Change Consulting Market Analysis by Mordor Intelligence

The climate change consulting market size is expected to increase from USD 6.07 billion in 2025 to USD 6.76 billion in 2026 and reach USD 10.99 billion by 2031, growing at a CAGR of 10.21% over 2026-2031. Mandatory disclosure rules in the United States and European Union have transformed advisory spending from optional to essential, while the rapid rise of sustainability-linked finance instruments has embedded independent verification into capital-raising processes. Large enterprises are driving near-term revenue as they race to meet accelerated reporting deadlines, yet small and medium enterprises are fast catching up because supply-chain scorecards now link contract renewals to verified decarbonization road maps. Consulting firms that fuse climate science, finance, and digital engineering skills are enjoying premium margins, and they are using AI-based scenario tools to compress project timelines and strengthen value propositions. Meanwhile, investors enforcing shadow carbon audits has created recurring demand for portfolio-level analytics, nudging the climate change consulting market toward double-digit expansion through mid-decade.

Key Report Takeaways

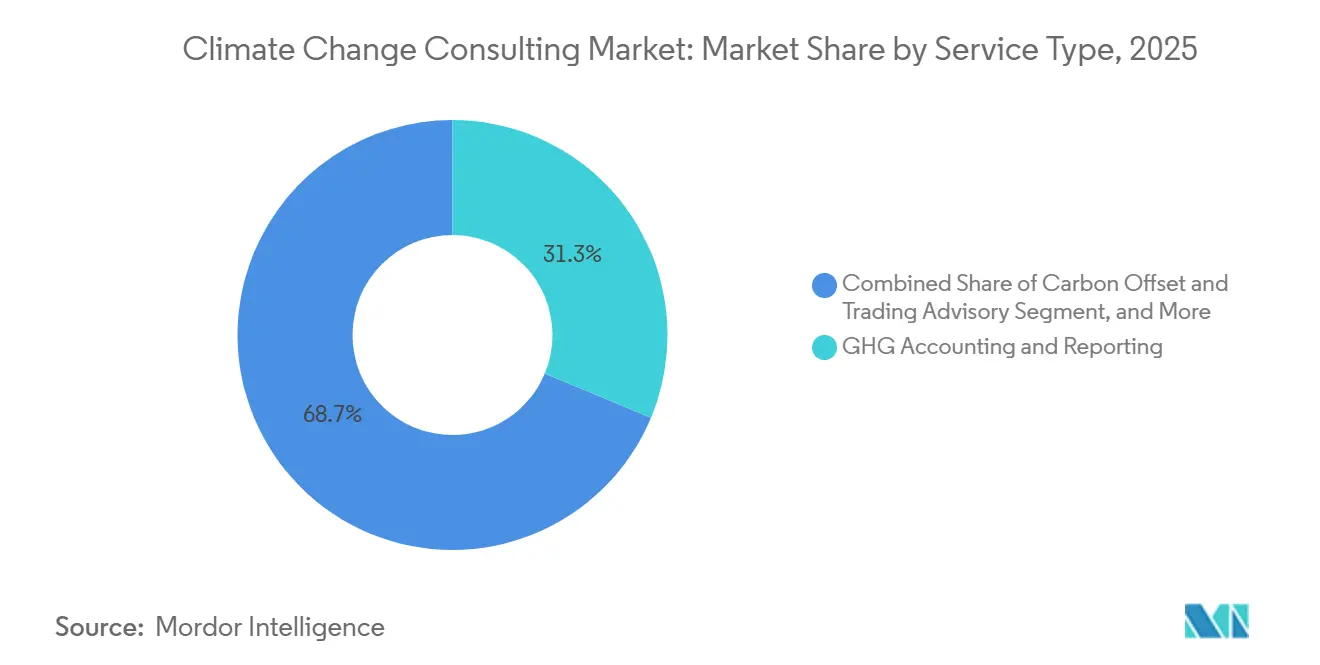

- By service type, GHG accounting and reporting led with 31.28% of revenue in 2025, while climate adaptation and resilience planning is projected to grow at an 11.40% CAGR through 2031.

- By end-user industry, energy and power captured 28.53% of 2025 spending, whereas mining and metals are forecast to advance at a 10.61% CAGR by 2031.

- By organization size, large enterprises accounted for 66.75% of market value in 2025, but small and medium enterprises are expected to expand at a 10.84% CAGR during 2026-2031.

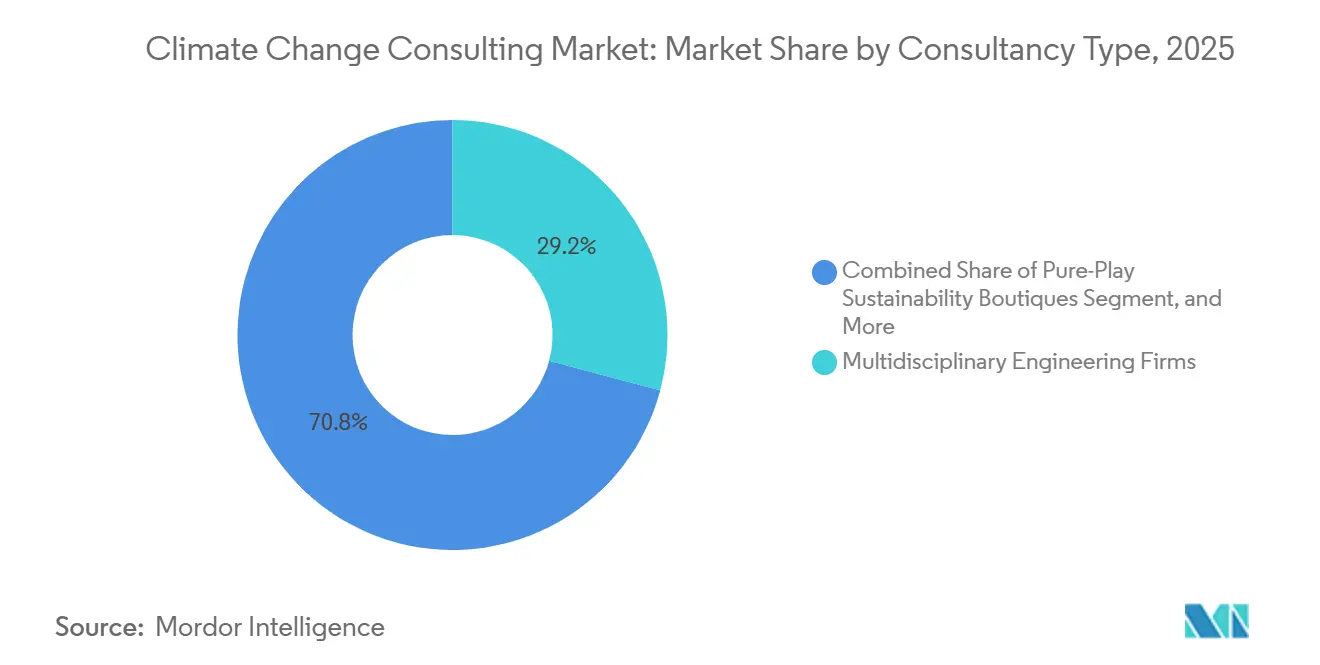

- By consultancy type, multidisciplinary engineering firms held a 29.16% share in 2025, while pure-play sustainability boutiques are set to record an 11.18% CAGR to 2031.

- By delivery mode, on-site advisory represented 52.74% of revenue in 2025, yet hybrid engagements are poised to increase at an 11.29% CAGR through 2031.

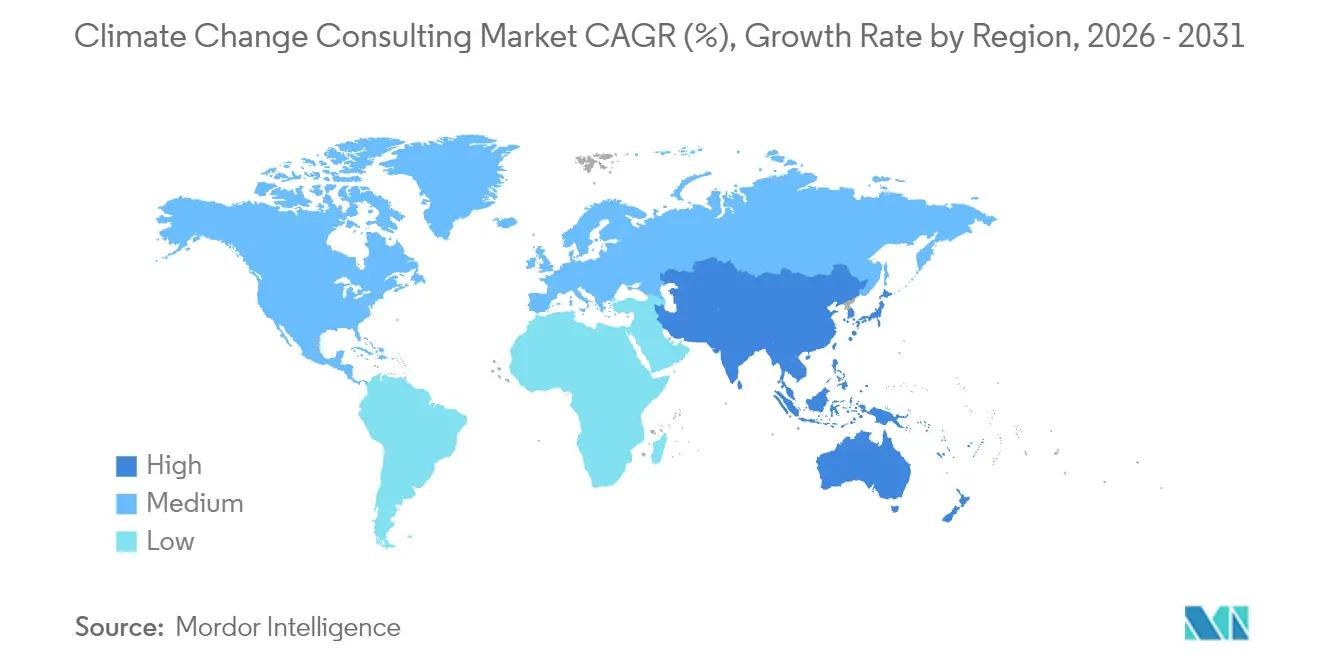

- By geography, North America commanded 37.33% of 2025 sales, and Asia-Pacific is anticipated to register an 11.07% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Climate Change Consulting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory ESG Disclosures Tightening Worldwide | +2.80% | Global, with early enforcement in North America and Europe | Short term (≤ 2 years) |

| Corporate Carbon-Shadow Audits Demanded by Investors | +1.90% | North America, Europe, Asia-Pacific financial hubs | Medium term (2-4 years) |

| Rapid Scaling of Sustainability-Linked Finance Instruments | +2.10% | Global, concentrated in OECD markets | Medium term (2-4 years) |

| Supply-Chain Decarbonization Pressures from OEMs | +1.60% | Global, strongest in automotive and electronics supply chains | Long term (≥ 4 years) |

| Breakthroughs in AI-Driven Climate-Risk Analytics | +1.40% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Growing Demand for Nature-Based Carbon Removal Advisory | +1.20% | Global, with pilot projects in South America and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory ESG Disclosures Tightening Worldwide

Rulemaking by the U.S. Securities and Exchange Commission in 2024 and the European Union’s Corporate Sustainability Reporting Directive in the same year triggered a wave of baseline emission assessments and internal-control upgrades.[1]U.S. Securities and Exchange Commission, “SEC Adopts Rules to Enhance and Standardize Climate-Related Disclosures,” SEC.gov The International Sustainability Standards Board harmonized reporting through IFRS S1 and S2, removing jurisdictional arbitrage and raising the rigor bar.[2]IFRS Foundation, “IFRS S1 and S2 Sustainability Disclosure Standards,” IFRS.org Consultants now design data architectures, run double-materiality analyses, and prepare audit-ready files that satisfy phased deadlines rolling from 2025 to 2028. Because disclosures require third-party assurance, advisory demand persists beyond first filings, creating multi-year revenue visibility for the climate change consulting market.

Corporate Carbon-Shadow Audits Demanded by Investors

Asset managers overseeing USD 130 trillion under the Net Zero Asset Managers initiative began ordering portfolio companies to publish financed-emission pathways in 2024. The Partnership for Carbon Accounting Financials standardized Scope 3 calculations, compelling banks and insurers to audit holdings and remediate laggards. Private-equity sponsors now embed climate covenants into management agreements that can adjust earn-outs. Consultants secure dual mandates, serving investors with portfolio screens and investees with deep dive decarbonization road maps, reinforcing recurring revenue for the climate change consulting market.

Rapid Scaling of Sustainability-Linked Finance Instruments

Cumulative issuance of sustainability-linked loans and bonds hit USD 1.2 trillion in 2025. Updated 2024 ICMA principles tightened ambition and verification thresholds, obligating borrowers to hire advisers for target setting and annual reporting.[3]International Capital Market Association, “Sustainability-Linked Bond Principles 2024,” Icmagroup.org Banks now insist on independent technical opinions before underwriting, expanding pre-issuance advisory layers. A shortage of ISO 14097-accredited verifiers has prompted engineering groups to acquire certification firms, aligning assurance and advisory and deepening the climate change consulting market penetration.

Supply-Chain Decarbonization Pressures from OEMs

Automotive leaders announced that supplier Scope 3 emissions would influence scorecards by 2026, putting non-compliant vendors at risk of delisting. CDP recorded 23,000 supplier disclosures in 2025, yet fewer than 20% had science-based targets.[4]CDP, “Supply Chain Report 2025,” CDP.net Electronics brands applied similar demands, catalysing advisory uptake among Asia-Pacific SMEs that lack in-house expertise. Consultants navigate allocation-method disputes and run supplier workshops, locking in long-horizon engagements that buoy the climate change consulting market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of Verifiable Scope 3 Emissions Data | -1.30% | Global, most acute in emerging markets and complex supply chains | Short term (≤ 2 years) |

| Inconsistent Regional Carbon-Pricing Mechanisms | -0.90% | Global, with divergence between EU ETS, California, and voluntary markets | Medium term (2-4 years) |

| Talent Shortage at the Climate Science–Finance Interface | -1.10% | North America, Europe, select Asia-Pacific hubs | Long term (≥ 4 years) |

| Green-Washing Litigation Risk Discouraging Advisory Uptake | -0.70% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarcity of Verifiable Scope 3 Emissions Data

Scope 3 often represents 70%-90% of a company’s footprint, yet supplier data remain fragmented, forcing reliance on spend-based proxies that can deviate by more than 50%. The International Sustainability Standards Board has only started consultations on better methodologies, delaying standardization until at least 2027. Automotive and electronics supply chains are particularly exposed, where multinationals source from over 50 countries. Persistent data gaps frustrate clients and postpone multi-year commitments, tempering expansion within the climate change consulting market.

Inconsistent Regional Carbon-Pricing Mechanisms

EU ETS allowances cost EUR 85 per metric ton (USD 96) in January 2026, while California’s cap-and-trade cleared at USD 38 and voluntary offsets traded at USD 12-25. China extended trading to steel and cement in 2025 but handed out free allowances that muted price signals. Variability complicates internal pricing models that consultants build for multinationals. Clients often split mandates by region, raising coordination costs and elongating decision cycles, thus shaving growth off the climate change consulting market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Reporting Dominance Yields to Adaptation Planning

The climate change consulting market size for GHG accounting and reporting reached USD 1.90 billion in 2025, equal to 31.28% of total revenue. Companies prioritized baseline inventories to satisfy new disclosure laws, positioning this service as the entry point for most engagements. As physical risk becomes financially material, climate adaptation and resilience planning is projected to grow at an 11.40% CAGR, the fastest among service types. This shift reallocates spend toward flood modelling, heat stress mapping, and resilience investment road maps. The interplay of disclosure, risk quantification, and financing has created bundled offerings that integrate scenario analysis with adaptation capex planning, reinforcing cross-selling opportunities in the climate change consulting market.

Decarbonization strategy services have moved beyond marginal-abatement cost curves to evaluate hydrogen, carbon capture, and electrification options. Advisors increasingly integrate sustainable finance structuring, tying investment road maps to green bonds or sustainability-linked loans. Carbon offset and trading advisory remains modest because integrity reviews invalidated many forestry credits, but demand persists for high-quality nature-based removal projects, especially where clients pursue net-zero claims that require residual offsetting. Biodiversity and circular-economy consulting, presently niche, is expanding as forthcoming European due-diligence rules widen the definition of environmental impact, promising incremental revenue for specialized firms within the climate change consulting market.

By End-User Industry: Mining and Metals Outpace Energy Transition

Energy and power generated USD 1.73 billion in 2025, representing 28.53% of climate change consulting market revenue. Utilities faced immediate disclosure deadlines and cap-and-trade obligations, driving heavy spend on baseline audits and road maps. Mining and metals, while smaller, will expand at a 10.61% CAGR to 2031 as investors push for credible Scope 1 and 2 pathways that align with sector net-zero commitments. Consultants advise on electrified haul trucks, green hydrogen direct-reduced iron, and renewable power integration, fostering robust demand for techno-economic analysis.

Public-sector demand is rising because multilateral climate-finance channels require feasibility studies before disbursing funds. Manufacturing, spanning automotive to chemicals, is embedding decarbonization into capital-planning cycles, generating multi-disciplinary mandates that blend process engineering with climate finance guidance. Financial-services institutions need portfolio-level risk analytics to comply with central-bank stress tests. ICT and telecom operators hire advisers for data-center energy optimization and supply-chain footprint reductions. Agriculture, food, transportation, and logistics are broadening the base of the climate change consulting market, each with distinct service requirements from soil-carbon measurement to fleet electrification scenarios.

By Organization Size: SMEs Accelerate Under Supply-Chain Mandates

Large enterprises commanded two-thirds of 2025 spending, but SME engagements are rising because OEM scorecards now link contract awards to verified science-based targets. The climate change consulting market size for SMEs is projected to reach USD 1.87 billion by 2031, expanding alongside platform-based advisory models that lower unit costs. Consultants serving SMEs often bundle carbon accounting with financing referrals to development-bank green-loan windows, accelerating uptake among capital-constrained suppliers.

Large-enterprise programs remain deeper and broader, featuring enterprise resource planning integrations and board-level scenario modelling. Premium pricing prevails in these bespoke mandates, but project durations are lengthening because clients navigate cross-border disclosure complexity. Advisory firms are segmenting their go-to-market strategies accordingly, either scaling standardized SME platforms or doubling down on relationship-driven enterprise practices, a trend that shapes competitive dynamics in the climate change consulting market.

By Consultancy Type: Boutiques Gain Share Through Specialization

Multidisciplinary engineering firms held 29.16% of 2025 revenue. Their site experience in infrastructure and heavy industry underpins competitive strength in adaptation planning and facility-level decarbonization. Pure-play sustainability boutiques, though more fragmented, will post the highest growth at 11.18% CAGR. Their edge lies in specialized offerings such as nature-based carbon removal and science-based target validation, areas where clients value deep expertise over scale.

Big Four accounting firms dominate assurance-led engagements, leveraging audit relationships yet remaining constrained by independence rules. Management consultancies integrate climate with corporate strategy, bundling transformation road maps with cost savings and growth initiatives. Think tanks and NGOs occupy a hybrid niche, supplying credibility and mission alignment for public-sector and philanthropic clients. Acquisition activity is intensifying as larger platforms buy boutiques to shore up capability gaps, a dynamic that will continue to redefine the climate change consulting market landscape.

By Delivery Mode: Hybrid Models Optimize Cost and Expertise

On-site advisory retained 52.74% of 2025 billings as facility audits, workshops, and board presentations benefit from physical presence. However, hybrid models mixing remote analytics with targeted site visits will expand at 11.29% CAGR, driven by 40%-60% travel cost savings and faster turnaround times. Remote-only advisory thrives for standardized reviews and training, yet satisfaction dips for complex strategy mandates.

Digital workspaces and AI-based scenario dashboards allow consultants to iterate with clients asynchronously, but engagement plans now spell out which milestones require on-site validation to secure project robustness. Regional preferences also shape delivery: Asia-Pacific clients lean toward in-person engagement, whereas North America and Europe increasingly accept hybrid and remote formats. This delivery diversification adds resilience to the climate change consulting market.

Geography Analysis

North America produced 37.33% of global revenue in 2025, anchored by the SEC disclosure rule and California’s cap-and-trade program that cover thousands of issuers and industrial plants. Canada’s carbon-pricing backstop, which rose to CAD 80 per metric ton (USD 59) in 2025, stimulated advisory demand in energy, mining, and manufacturing. Mexico’s pilot emissions-trading system, although narrow, sets the stage for future engagements. Regulatory litigation in the United States introduces execution risk, leading some firms to phase spending until legal clarity emerges, but the sheer depth of capital markets sustains baseline demand for financed-emission analytics, bolstering the climate change consulting market.

Europe ranks second in revenue, propelled by the Corporate Sustainability Reporting Directive, EU Taxonomy Regulation, and Carbon Border Adjustment Mechanism that jointly constitute the world’s strictest disclosure and pricing framework. Germany’s EUR 30 billion (USD 34 billion) subsidy program for green hydrogen and electrification fuels feasibility studies, while the United Kingdom’s transition-plan rules require forward-looking scenario reports. France’s Article 29 obligations drive portfolio analytics, and Nordic corporates pursue nature-based removal projects for net-zero claims. These overlapping mandates generate high-value, multi-jurisdictional advisory work that reinforces the region’s influence on the climate change consulting market.

Asia-Pacific is the fastest-growing region at an 11.07% CAGR. China expanded its national emissions trading system to eight sectors in 2025 and linked dual-carbon goals to provincial action plans, spawning city-level consulting contracts. India finalized its green taxonomy and tightened energy-efficiency standards, compelling hard-to-abate industries to seek advisory. Japan’s Green Transformation League is channelling USD 150 billion into low-carbon projects, while South Korea’s carbon-neutrality framework mandates sectoral road maps. Southeast Asian countries vie for climate-finance inflows, but local consulting capacity remains thin, creating entry opportunities for global players eager to enlarge their footprint in the climate change consulting market.

South America and Middle East and Africa are smaller but quickening. Brazil’s regulated carbon market, expected in 2027, already motivates pre-compliance audits. Sovereign wealth funds in the Middle East are allocating capital to renewables, and national oil companies need transition strategies aligned with UAE’s net-zero pledge. These developments are laying the groundwork for an increasingly diversified climate change consulting market across emerging regions.

Competitive Landscape

The climate change consulting market remains moderately fragmented; the top five providers hold about 35% combined share. Big Four auditors leverage assurance expertise, engineering firms capitalize on technical depth, and pure-play boutiques win high-complexity mandates. Technology investment is the new battleground. Deloitte deployed an AI scenario platform that halves analysis time, WSP bought a geospatial analytics company to refine physical-risk models, and AECOM partnered with a cloud provider to run digital twins for industrial facilities.

Meanwhile, software-as-a-service start-ups that automate carbon accounting threaten to commoditize entry-level work, prompting incumbents to focus on transformation programs where strategic insight carries pricing power.

Regulatory independence rules cap audit-related cross-selling, giving boutiques room to flourish. South Pole’s 2025 acquisition by private equity underscores investor belief in voluntary carbon markets. Talent scarcity persists; senior consultant hiring cycles exceed 90 days, and compensation tops USD 200,000 in North America and Europe. Firms court specialists with equity stakes and mission branding. Consolidation is likely as large platforms acquire niche players to plug capability gaps, a trend that will elevate competitive pressure yet gradually raise market concentration within the climate change consulting market.

Climate Change Consulting Industry Leaders

Jacobs Solutions Inc.

AECOM

WSP Global Inc.

Stantec Inc.

Ramboll Group A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Deloitte acquired a European climate-risk analytics firm for EUR 120 million (USD 136 million), adding 200 scientists and data engineers to its global sustainability practice.

- December 2025: WSP Global secured a five-year, USD 85 million contract with the Asian Development Bank to deliver climate-adaptation planning across 12 Asia-Pacific countries.

- November 2025: PwC launched an AI-enabled sustainability-linked finance advisory platform, winning 15 mandates totalling USD 3 billion in green-bond issuances within one quarter.

- October 2025: AECOM partnered with a leading cloud-computing provider to roll out digital twins for industrial decarbonization across North America and Europe.

Global Climate Change Consulting Market Report Scope

The Climate Change Consulting Market Report is Segmented by Service Type (Risk Assessment and Scenario Analysis, GHG Accounting and Reporting, Decarbonization Strategy and Road-Mapping, Climate Adaptation and Resilience Planning, Carbon Offset and Trading Advisory, Sustainable Finance and ESG Integration, Other Service Types), End-User Industry (Energy and Power, Mining and Metals, Public Sector, Manufacturing, Financial Services, ICT and Telecom, Agriculture and Food, Transportation and Logistics, Other Industries), Organization Size (Large Enterprises, Small and Medium Enterprises), Consultancy Type (Multidisciplinary Engineering Firms, Pure-Play Sustainability Boutiques, Big Four Accounting Firms, Management Consulting Firms, Think Tanks and NGOs), Delivery Mode (On-Site Advisory, Remote or Virtual Advisory, Hybrid Engagements), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Risk Assessment and Scenario Analysis |

| GHG Accounting and Reporting |

| Decarbonisation Strategy and Road-Mapping |

| Climate Adaptation and Resilience Planning |

| Carbon Offset and Trading Advisory |

| Sustainable Finance and ESG Integration |

| Other Service Types |

| Energy and Power |

| Mining and Metals |

| Public Sector |

| Manufacturing |

| Financial Services |

| ICT and Telecom |

| Agriculture and Food |

| Transportation and Logistics |

| Other End-User Industry |

| Large Enterprises |

| Small and Medium Enterprises |

| Multidisciplinary Engineering Firms |

| Pure-Play Sustainability Boutiques |

| Big Four Accounting Firms |

| Management Consulting Firms |

| Think Tanks and NGOs |

| On-Site Advisory |

| Remote / Virtual Advisory |

| Hybrid Engagements |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Israel |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Service Type | Risk Assessment and Scenario Analysis | ||

| GHG Accounting and Reporting | |||

| Decarbonisation Strategy and Road-Mapping | |||

| Climate Adaptation and Resilience Planning | |||

| Carbon Offset and Trading Advisory | |||

| Sustainable Finance and ESG Integration | |||

| Other Service Types | |||

| By End-User Industry | Energy and Power | ||

| Mining and Metals | |||

| Public Sector | |||

| Manufacturing | |||

| Financial Services | |||

| ICT and Telecom | |||

| Agriculture and Food | |||

| Transportation and Logistics | |||

| Other End-User Industry | |||

| By Organisation Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Consultancy Type | Multidisciplinary Engineering Firms | ||

| Pure-Play Sustainability Boutiques | |||

| Big Four Accounting Firms | |||

| Management Consulting Firms | |||

| Think Tanks and NGOs | |||

| By Delivery Mode | On-Site Advisory | ||

| Remote / Virtual Advisory | |||

| Hybrid Engagements | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Israel | |

| Saudi Arabia | |||

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the climate change consulting market by 2031?

The market is forecast to reach USD 10.99 billion by 2031.

Which service type will grow fastest through 2031?

Climate adaptation and resilience planning is poised to expand at an 11.40% CAGR.

Why are small and medium enterprises increasing their spending on consulting?

OEM supply-chain scorecards now link contract renewals to verified decarbonization road maps, pushing SMEs to hire advisers.

Which region is expected to record the highest CAGR?

Asia-Pacific is projected to grow at an 11.07% CAGR during 2026-2031.

How concentrated is the competitive landscape?

The top five firms hold about 35% share, indicating a moderately fragmented market.

What delivery model is gaining popularity?

Hybrid engagements combining remote analytics with selective on-site visits are growing at an 11.29% CAGR.

Page last updated on: