Long Read Sequencing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

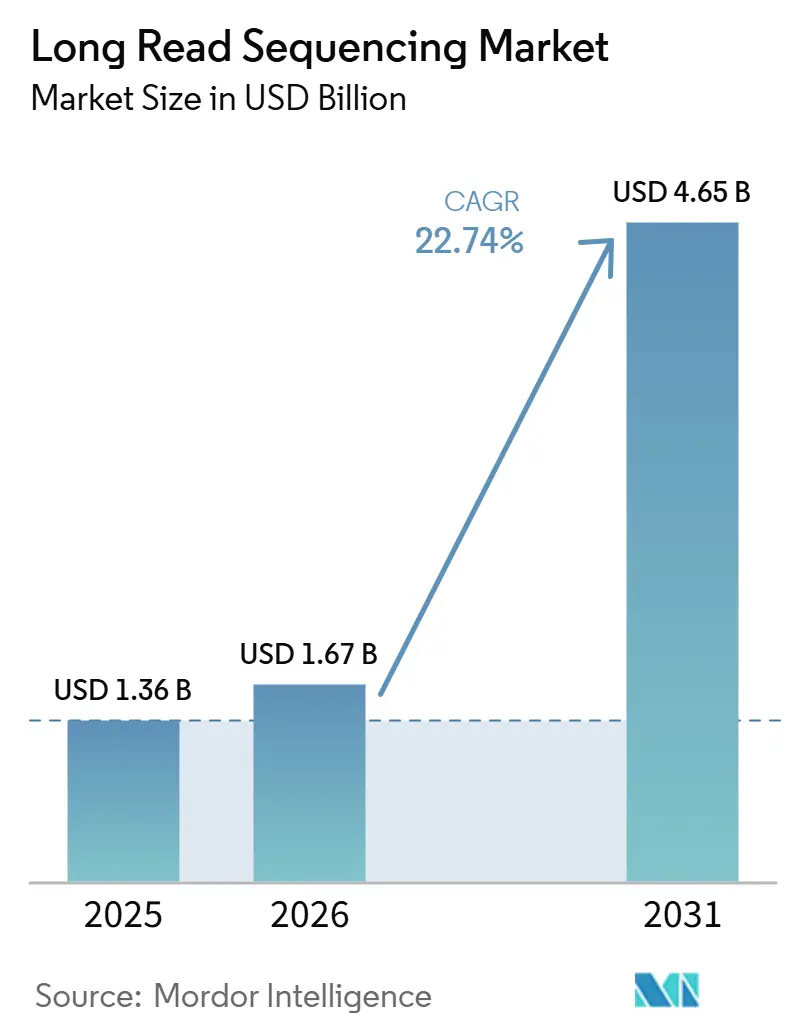

| Market Size (2026) | USD 1.67 Billion |

| Market Size (2031) | USD 4.65 Billion |

| Growth Rate (2026 - 2031) | 22.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Long Read Sequencing Market Analysis by Mordor Intelligence

The Long Read Sequencing Market size is expected to increase from USD 1.36 billion in 2025 to USD 1.67 billion in 2026 and reach USD 4.65 billion by 2031, growing at a CAGR of 22.74% over 2026-2031.

Cost-per-genome reductions, accuracy gains that now exceed 99.9% in duplex mode, and a widening clinical evidence base have combined to push the technology from research laboratories into mainstream diagnostics. Adoption is boosted further by cloud-native informatics pipelines, which lower the onboarding barrier for small laboratories and emerging healthcare systems. Modest capital intensity relative to previous-generation platforms and the prospect of rapid payback on consumables reinforce the business case for institutions that handle complex genetic cases. Meanwhile, governments are embedding population-scale programs into public-health strategies, expanding reimbursement, and accelerating infrastructure investments.

Key Report Takeaways

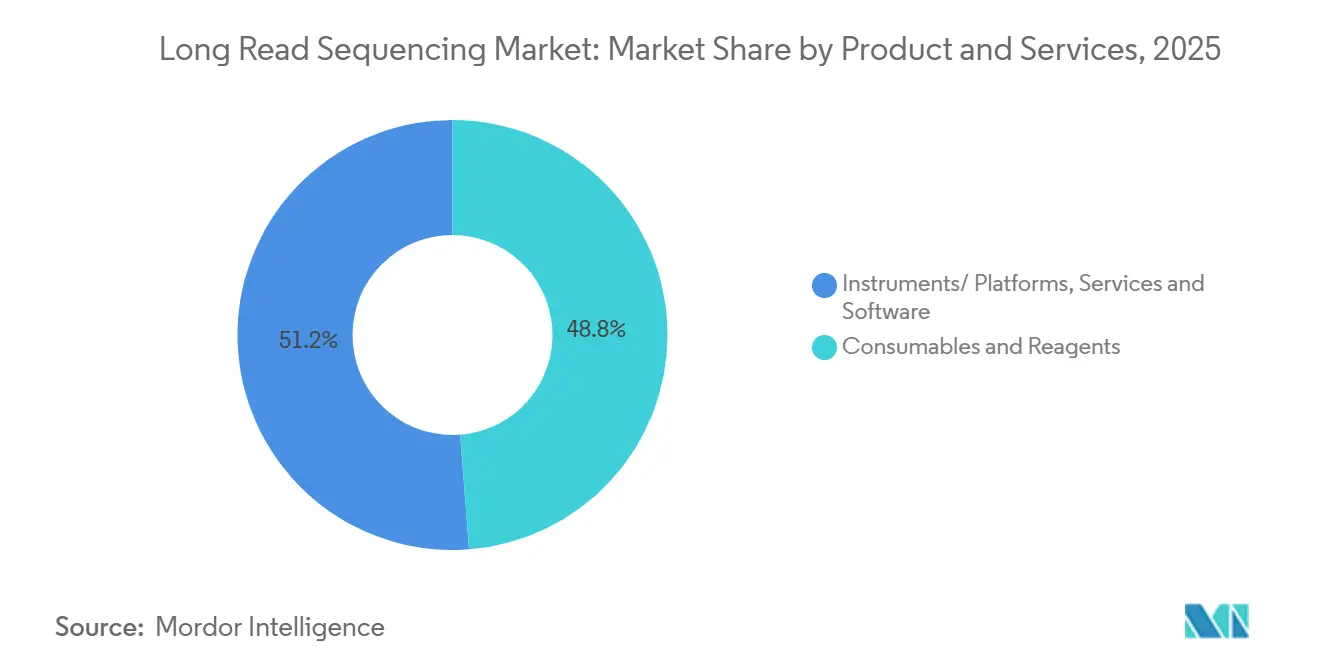

- By product category, consumables and reagents led with 48.78% revenue share in 2025, while services and software are forecast to expand at a 24.35% CAGR through 2031.

- By technology platform, SMRT HiFi sequencing held 58.92% of the long read sequencing market share in 2025; nanopore sequencing is projected to post the fastest growth at 24.68% CAGR to 2031.

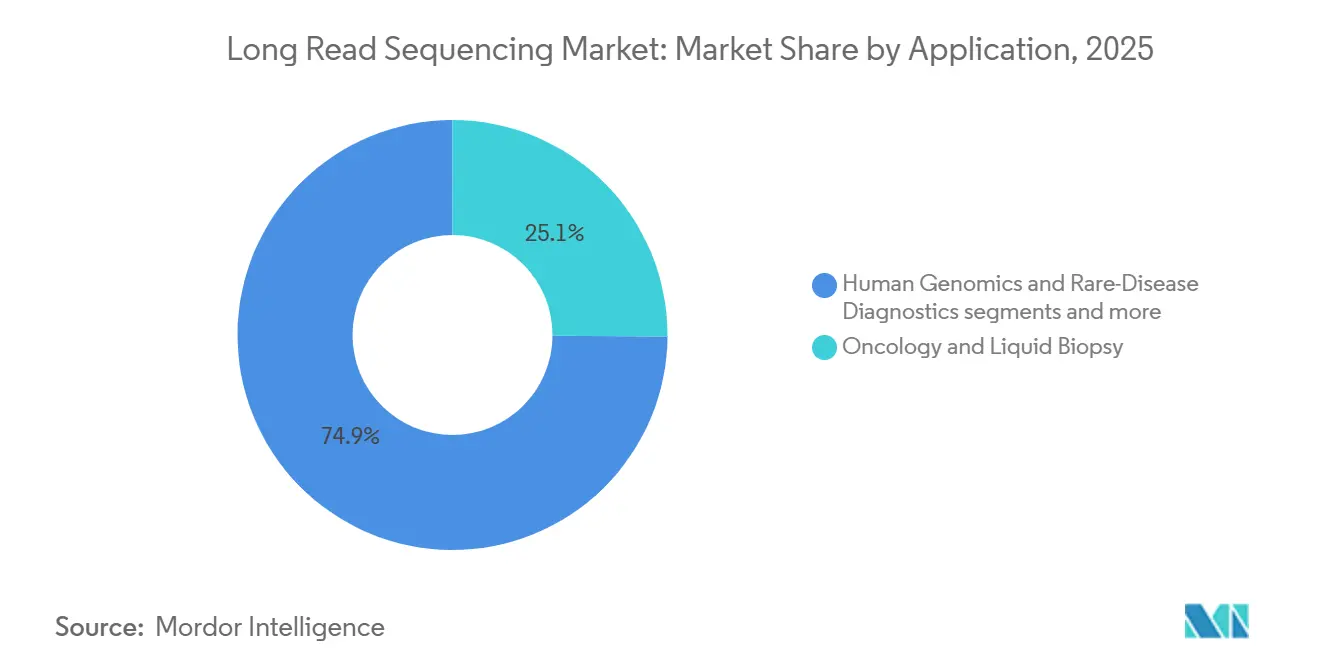

- By application, oncology accounted for a 25.12% share of the long read sequencing market size in 2025, whereas rare-disease diagnostics is advancing at a 24.96% CAGR through 2031.

- By end-user, academic and government institutes captured 31.45% of spending in 2025; clinical and diagnostic laboratories record the highest projected CAGR at 25.12% to 2031.

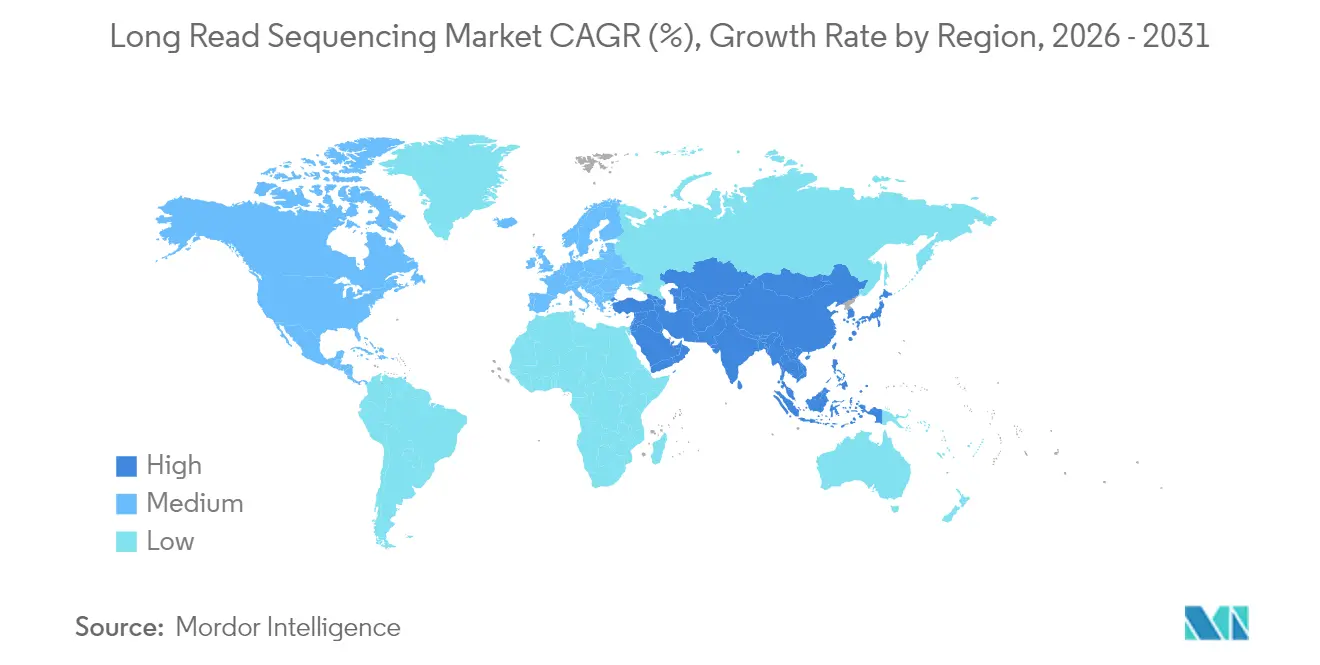

- By geography, North America dominated with 50.10% revenue share in 2025; Asia-Pacific is forecast to grow at 25.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Long Read Sequencing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Decline in Per-Base Sequencing Cost | 2.80% | Global | Medium term (2–4 years) |

| Growing Clinical Uptake for Rare-Disease Diagnostics | 2.20% | North America & EU, with spill-over to APAC | Medium term (2–4 years) |

| Accuracy & Throughput Leap via HiFi/Duplex Chemistries | 1.90% | Global, led by North America & EU | Short term (≤ 2 years) |

| AI-Enabled Base-Calling & Methylation Analytics | 1.60% | Global, early gains in North America & China | Long term (≥ 4 years) |

| Portable Real-Time Sequencing for Bio-Security Surveillance | 1.20% | Global, with emphasis on government-heavy markets in APAC & MEA | Short term (≤ 2 years) |

| National Genomic-Sovereignty Initiatives Funding Long-Read Programs | 1.00% | APAC core (China, India, South Korea), EU | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rapid Decline in Per-Base Sequencing Cost

Human whole-genome sequencing now costs less than USD 500 on PacBio’s Revio using SPRQ chemistry, a ten-fold reduction since 2020. Oxford Nanopore’s increased flow-cell output is set to top 1 million units annually, widening supply and compressing price points. Lower capital outlays encourage mid-tier hospitals to move complex cases in-house, eroding the historic referral model that favored centralized sequencing hubs.

Growing Clinical Uptake for Rare-Disease Diagnostics

Studies show that long read sequencing detects an additional 8.33% of pathogenic variants over short-read techniques in neurodevelopmental cohorts. Children’s Mercy Kansas City recently introduced HiFi-based testing, reducing diagnostic odysseys and influencing private-payer coverage policy in the United States. Similar clinical roll-outs are now underway in several EU reference laboratories under the emerging LDT rule.

Accuracy & Throughput Leap via HiFi/Duplex Chemistries

Oxford Nanopore’s duplex mode posts Q30-equivalent accuracy above 99.9% while preserving ultra-long read lengths. With PromethION 48 delivering capacity for 10,000 genomes per year, the technology finally meets both precision and volume thresholds required for national screening programs.

AI-Enabled Base-Calling & Methylation Analytics

Dorado base-calling, powered by neural networks, now processes raw signals in real time and simultaneously quantifies methylation at the CG, CHG and CHH contexts. PacBio’s agreement with The Chinese University of Hong Kong extends machine-learning pipelines to epigenetic variant calling in oncology, trimming manual curation time and facilitating regulated workflows

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Operating Costs of Long-Read Platforms | -0.021 | Global, acute in MEA & Latin America | Medium term (2–4 years) |

| Bioinformatics & Data-Storage Complexity | -0.015 | Emerging markets; APAC ex-China, MEA | Medium term (2–4 years) |

| Reagent-Grade Nanopore Membrane Supply-Chain Fragility | -0.008 | Global, with heightened exposure in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Intensifying IP Litigation Among Platform Vendors | -0.005 | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital & Operating Costs of Long-Read Platforms

Even at discounted launch pricing, a fully configured Revio or PromethION bundle requires a high-six-figure investment, and flow-cell replenishment remains the largest recurring expense for moderate-throughput laboratories. Hospitals with fewer than 300 complex cases per year often delay procurements until payer codes broaden or national grants defray acquisition costs.

Bioinformatics & Data-Storage Complexity

A single human HiFi run can generate more than 1 TB of raw data, overwhelming on-premises servers and straining V-NET connectivity for cloud transfers. Skilled analysts versed in haplotype phasing, structural variant annotation, and methylation calling remain scarce, hindering rapid case turn-around in provincial or community centers. Automated interpretive engines are in development but will take two to four years to close the expertise gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Service: Recurring Consumables Dominate, Software Scales

Consumables and reagents accounted for almost half of 2025 revenue and form the backbone of most vendor business models. Subscription-style reagent plans lock customers into predictable spending and offset initial capital concessions granted on large instrument deals. PacBio reported consumables revenue of USD 20.1 million in Q1 2025, up 26% year-over-year despite softer instrument placements. Services and software, however, register the steepest growth as laboratories prioritize turnkey informatics over bare-metal hardware. Cloud licenses bundled with AI-curated variant interpretation enable small clinics to jump straight into accredited testing pathways, a trend that underpins the expected 24.35% CAGR.

Progressively, data analytics platforms such as QIAGEN Digital Insights are embedding multi-omic knowledge graphs that link structural variants to phenotypes and drug targets, turning consumables datasets into subscription revenue streams. The shift suggests that reagent volumes will remain a revenue bedrock, yet software contracts may carry a higher margin and greater lock-in, reshaping competitive levers in the long read sequencing market.

By Technology Platform: HiFi Retains Lead as Nanopore Accelerates

HiFi sequencing captured 58.92% of 2025 revenue, backed by consistent Q30 accuracy that satisfies regulated clinical protocols. In parallel, nanopore devices grow off a smaller base but deliver the strongest 24.68% CAGR courtesy of pocket-sized MinION and desktop GridION units, which enable near-patient testing in infectious-disease outbreaks.

Competition is converging on hybrid strategies. Roche’s Sequencing by Expansion (SBX) aims to decouple chemistry from detection, potentially dropping entry prices and forcing incumbents to sharpen value-added features such as methylation profiling at no extra run time Roche. Over the medium term, platform differentiation will move beyond raw read length toward integrated analytics, assay portfolio breadth, and service-level guarantees.

By Application: Oncology Still Largest, Rare Diseases Surging

Oncology retained 25.12% revenue share in 2025 as comprehensive genomic profiling and liquid biopsy panels shift toward long reads to resolve large structural events. These panels produce incremental biomarker information, improving trial stratification and companion-diagnostic precision Nature Genetics. Rare-disease diagnostics, however, is the fastest riser, advancing at 24.96% CAGR on the back of mounting evidence that long reads close roughly half of previously undiagnosed cases.

Transcriptomics, metagenomics and pangenome projects are also scaling. Direct RNA isoform tracing helps characterize alternative splicing in neurodegeneration, while high-fidelity assemblies underpin microbiome surveillance in antimicrobial-resistance programs. Diverse use cases buffer cyclic demand in any single therapeutic area, supporting long-term revenue resilience.

By End-User: Academics Anchor Installed Base, Clinics Fuel Next Wave

Academic and public-sector labs represent 31.45% of 2025 outlays and often act as early adopters that validate workflows and train next-generation operators. Government grant cycles, including NIH and Horizon Europe calls, typically finance instrument procurement, sustaining academic dominance European Commission. Yet clinical laboratories are set to expand at 25.12% CAGR to 2031 as clarity around the FDA LDT rule reduces implementation risk.

Pharmaceutical and biopharma companies are running increasingly large functional-genomics screens to link structural variants with compound efficacy, thereby doubling demand for long read services from contract research organizations. Combined, these trends mean that while academic sites remain influential opinion leaders, future volume growth will skew toward regulated medical environments.

Geography Analysis

North America delivered 50.10% of 2025 revenue, underpinned by mature reimbursement structures and abundant venture capital that sustains start-ups focused on AI genomics tooling. NIH-funded initiatives, such as the Center for Alzheimer’s and Related Dementias, regularly deploy PromethION for multi-omic profiling, reinforcing regional leadership. Canada’s CAD 200 million National Genomics Data Initiative further enlarges data-generation capacity and encourages cross-border research consortia. Despite leadership, growth moderates as saturated major academic centers transition to replacement rather than expansion budgets.

Asia-Pacific logs the fastest 25.52% CAGR on the back of public-sector programs that embed population genomics into disease-prevention strategies. Japan’s RIKEN delivered a landmark 3,200-individual long read dataset in 2025, providing a reference panel for East Asian precision medicine. China’s industrial policy grants drive large-scale factory builds for flow-cell components, ensuring supply security and cost competitiveness. Australia is piloting newborn genome screening, positioning long read sequencing as a frontline diagnostic for severe early-onset disorders.

Europe benefits from coordinated efforts such as Genome of Europe, a USD 48 million initiative connecting 51 institutes across 27 nations to generate a continent-wide pangenome. Germany’s lonGER project integrates Oxford Nanopore workflows into national rare-disease clinics, accelerating diagnostic pipelines and creating training hubs for surrounding EU member states. While GDPR compliance challenges slow cross-border data federation, progressive regulatory sandboxes in Finland and Estonia suggest pragmatic routes to maintain privacy without stifling discovery.

Competitive Landscape

The long read sequencing market is moderately concentrated around two technology anchors: PacBio and Oxford Nanopore. PacBio stakes its advantage on HiFi accuracy that aligns with regulated clinical assays, whereas Oxford Nanopore bets on real-time analytics and device portability, protecting field-deployable niches. Illumina has signaled entry with Constellation-based long read chemistry, due 2026, that may pool existing short-read optics with modified sample prep to accelerate adoption inside its extensive installed base.

Roche’s forthcoming SBX platform aims to segment chemistry and sequencing stages across two devices, promising capital efficiency that could disrupt current list prices. Meanwhile, strategic tie-ups multiply. Oxford Nanopore partnered with bioMérieux on infectious-disease kits, and with Tecan for automated sample prep, erecting ecosystem barriers for would-be entrants. Litigation also heats up, exemplified by Illumina’s patent filing against Element Biosciences over flow-cell fundamentals.

Manufacturing scale is becoming a decisive differentiator: Oxford Nanopore’s automated UK facility targets over 1 million flow-cells per year, a volume that could compress unit economics beyond smaller vendors’ reach. PacBio counters with 25 ploid commercial service labs offering Revio-based diagnostic workflows, reinforcing its clinical moat through network effects. Software remains an open frontier cloud-native interpretation suites may allow new entrants to carve share without bearing instrument P&L risk.

Long Read Sequencing Industry Leaders

Illumina, Inc.

F. Hoffmann-La Roche Ltd.

PacBio

Oxford Nanopore Technologies plc.

Agilent Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Roche unveiled Sequencing by Expansion (SBX) chemistry, aiming for 7 human 30× genomes per hour on a dual-instrument workflow, with market launch planned for 2026.

- January 2025: Illumina formed a strategic alliance with NVIDIA to merge DRAGEN pipelines and AI inference engines for accelerated multi-omic analyses.

Global Long Read Sequencing Market Report Scope

As per the report's scope, long read sequencing is a cutting-edge genomic technology that produces long, contiguous reads of DNA or RNA sequences, often spanning thousands to millions of base pairs. It provides a comprehensive view of the genome and spans repetitive regions, structural variations, and complex genomic areas.

The long read sequencing market is segmented into product, technology, workflow, application, end user and geography. By product, the market is segmented into instruments, consumables, and services. Based on technology, the market is segmented into single molecule real-time (SMRT) sequencing, nanopore sequencing and synthetic long read sequencing. The market is segmented by workflow into pre-sequencing, sequencing, and data analysis. The market is segmented by application into whole genome sequencing (WGS), whole exome sequencing (WES), targeted gene sequencing, metagenomics, epigenetics, and others. By end-user, the market is segmented into academic & research institutes, pharmaceutical & biotechnology companies, hospitals & clinics, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The report also offers the market size and forecasts for 17 countries across the region. The market sizing and forecasts were made for each segment based on value (USD).

| Instruments / Platforms |

| Consumables & Reagents |

| Services & Software |

| SMRT HiFi Sequencing |

| Nanopore Sequencing |

| Synthetic Long-Read / Linked-Read |

| Hybrid & Other Emerging |

| Human Genomics & Rare-Disease Diagnostics |

| Oncology & Liquid Biopsy |

| Metagenomics & Microbiome |

| Transcriptomics (Iso-Seq, Direct RNA) |

| Agrigenomics & Plant/Animal Breeding |

| Others |

| Academic & Government Research Institutes |

| Clinical & Diagnostic Laboratories |

| Pharmaceutical & Biopharma Companies |

| CROs & Service Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product & Service | Instruments / Platforms | |

| Consumables & Reagents | ||

| Services & Software | ||

| By Technology Platform | SMRT HiFi Sequencing | |

| Nanopore Sequencing | ||

| Synthetic Long-Read / Linked-Read | ||

| Hybrid & Other Emerging | ||

| By Application | Human Genomics & Rare-Disease Diagnostics | |

| Oncology & Liquid Biopsy | ||

| Metagenomics & Microbiome | ||

| Transcriptomics (Iso-Seq, Direct RNA) | ||

| Agrigenomics & Plant/Animal Breeding | ||

| Others | ||

| By End-User | Academic & Government Research Institutes | |

| Clinical & Diagnostic Laboratories | ||

| Pharmaceutical & Biopharma Companies | ||

| CROs & Service Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the long read sequencing market and how fast is it growing?

The market is valued at USD 1.67 billion in 2026 and is projected to reach USD 4.65 billion by 2031, reflecting a 22.74% CAGR

Which sequencing platform commands the largest share today?

PacBio’s SMRT HiFi technology holds 58.92% of the long read sequencing market share in 2025, owing to its clinical-grade Q30 accuracy

Which region is expected to grow the fastest over the forecast period?

Asia-Pacific is forecast to expand at a 25.52% CAGR through 2031, driven by population-scale genomic initiatives in Japan, China and India

How low have whole-genome sequencing costs fallen with long read chemistries?

PacBio’s SPRQ chemistry enables a human HiFi genome for less than USD 500, representing a ten-fold reduction since 2020.

Page last updated on: