Microbiome Sequencing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.94 Billion |

| Market Size (2031) | USD 2.68 Billion |

| Growth Rate (2026 - 2031) | 6.63% CAGR |

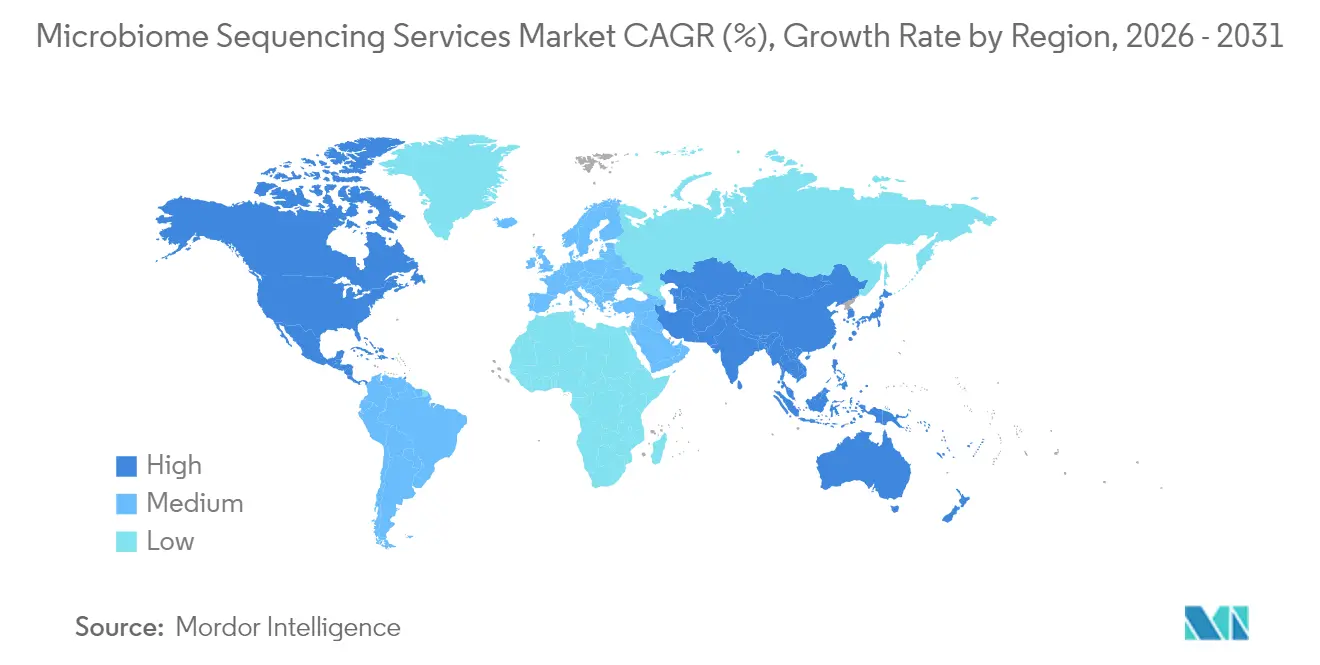

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

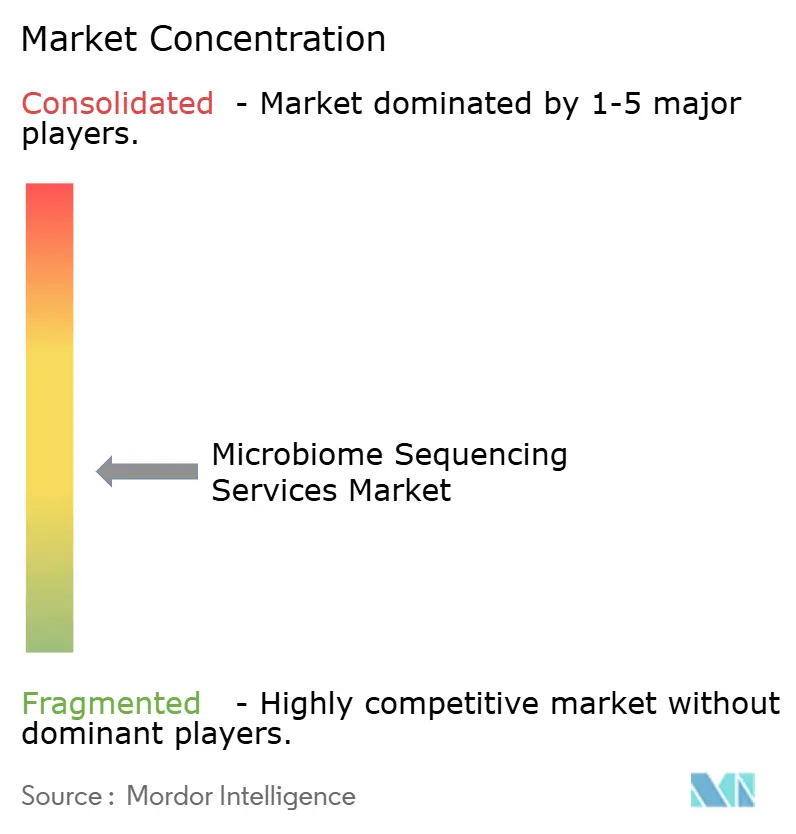

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Microbiome Sequencing Services Market Analysis by Mordor Intelligence

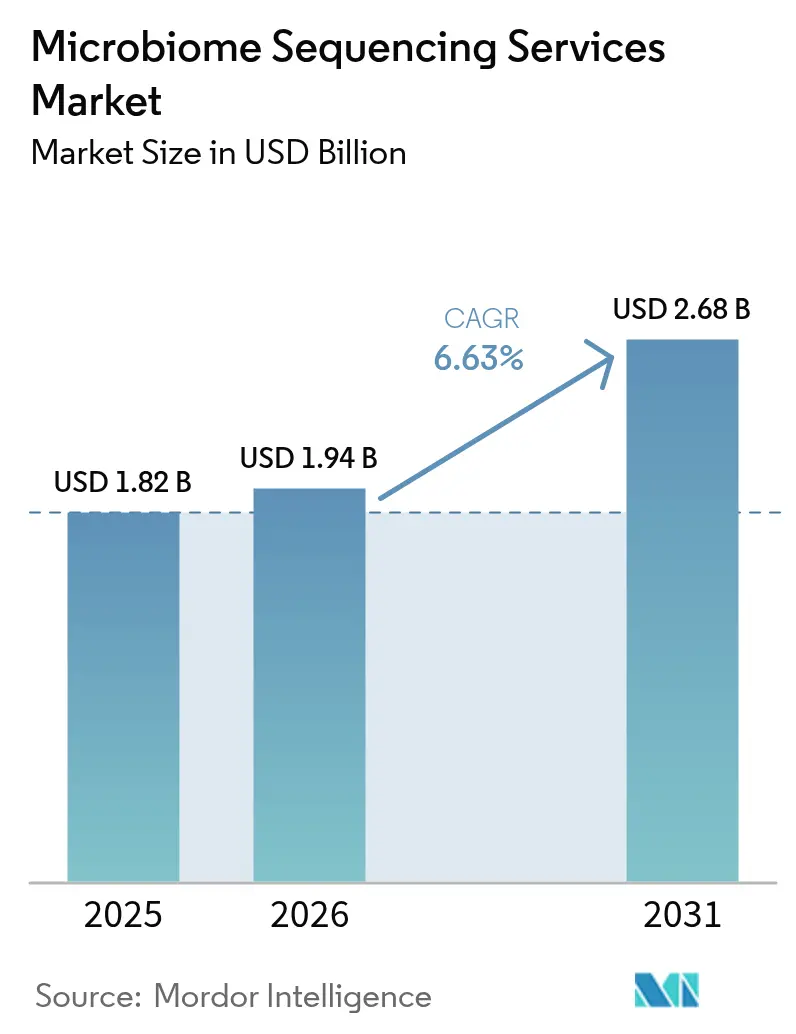

Microbiome Sequencing Services Market size in 2026 is estimated at USD 1.94 billion, growing from 2025 value of USD 1.82 billion with 2031 projections showing USD 2.68 billion, growing at 6.63% CAGR over 2026-2031.

Consistent adoption of microbiome profiling in clinical trials, therapeutic discovery, and precision-medicine workflows underpins this expansion, while steadily falling next-generation sequencing (NGS) costs further widen access for both academic and commercial users [1]Yishay Pinto, "Sequencing-based analysis of microbiomes," Nature Reviews Genetics, nature.com. Investment momentum around live-biotherapeutic products, companion diagnostics, and national biobank initiatives is translating directly into higher sample volumes and recurring analytical contracts. Competitive differentiation is shifting from pure sequencing capacity toward integrated bioinformatics, regulatory-grade quality systems, and multi-omic data interpretation. At the same time, data-sovereignty rules and a persistent shortage of multi-omic bioinformaticians moderate the market’s growth potential in the near term, prompting larger providers to invest aggressively in compliance infrastructure and automation.

Key Report Takeaways

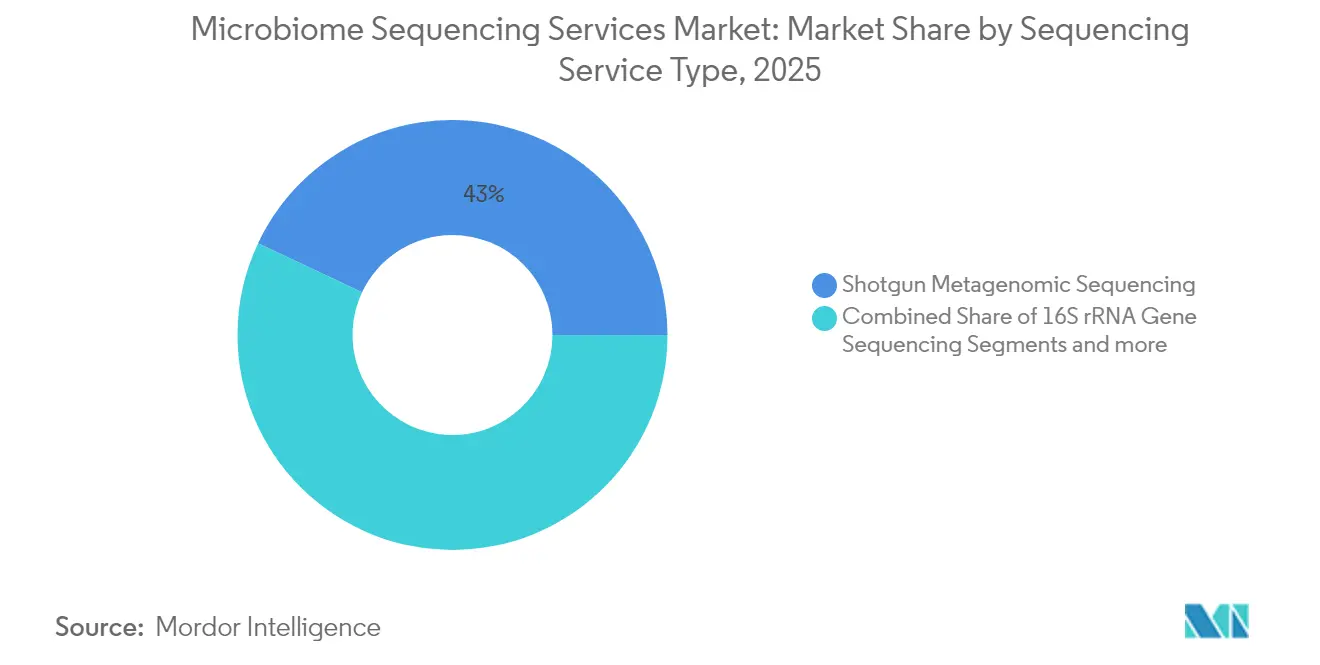

- By sequencing service type, shotgun metagenomic sequencing led with 42.98% of the microbiome sequencing services market share in 2025, whereas whole-genome and metatranscriptomic sequencing is projected to expand at a 7.48% CAGR to 2031.

- By technology, sequencing-by-synthesis captured 40.78% revenue share in 2025, while sequencing-by-ligation is expected to post the fastest 7.38% CAGR through 2031.

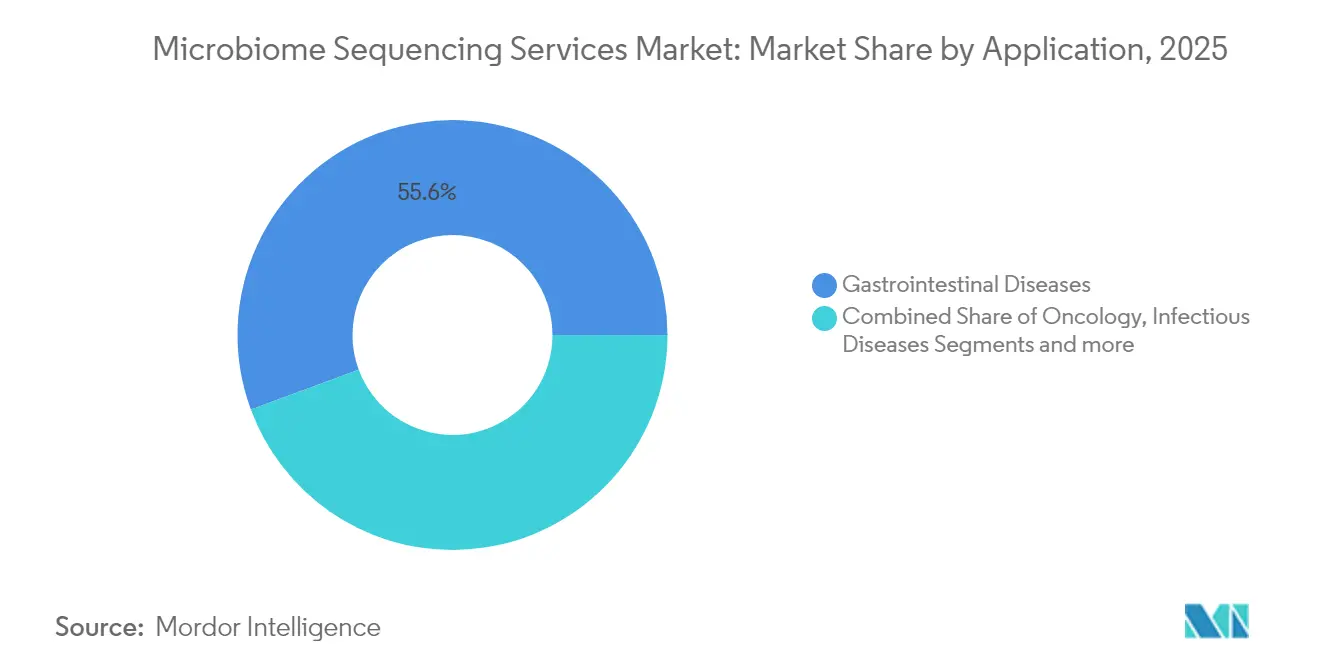

- By application, gastrointestinal diseases accounted for 55.64% of the microbiome sequencing services market size in 2025 and oncology is advancing at a 7.27% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies held 34.96% share of the microbiome sequencing services market size in 2025, but contract research organizations record the highest projected 7.35% CAGR to 2031.

- By geography, North America led with a 42.31% revenue share in 2025, whereas Asia-Pacific is set to grow at a 7.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Microbiome Sequencing Services Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in clinical trial outsourcing to specialized microbiome CROs | +1.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Declining NGS cost per Gb | +1.5% | Global | Short term (≤ 2 years) |

| Growing venture capital funding in microbiome-based therapeutics | +1.2% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Pharmaceutical demand for microbiome-based companion diagnostics | +1.0% | Global, led by North America | Long term (≥ 4 years) |

| National biobank programs adding longitudinal microbiome arms | +0.8% | Europe, North America, expanding to APAC | Long term (≥ 4 years) |

| Growing prevalence of chronic and infectious diseases | +0.9% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Clinical-Trial Outsourcing to Specialized Microbiome CROs

Pharmaceutical developers are transferring complex microbiome workstreams to contract research organizations because CROs retain specialized sampling, engraftment, and bioinformatic expertise that remains scarce in-house. The U.S. FDA’s approvals of REBYOTA and VOWST validated regulatory pathways and unlocked bigger late-phase pipelines, encouraging further outsourcing to firms that can compress timelines and manage protocol standardization. CROs, able to pool projects across sponsors and leverage economies of scale, now represent the fastest-rising end-user cohort at a 7.55% CAGR to 2030. Their integrated offerings—spanning sample logistics, wet-lab workflows, and submissions-ready reporting—are particularly attractive during costly Phase 2 and Phase 3 studies, where speed and reproducibility translate into material savings [2]SGS SA, "Designing Effective Clinical Trials for Microbiome-Based Products," sgs.com. Strategic alliances between big CROs and sequencing technology vendors also amplify market reach, reinforcing the outsourcing cycle that underpins a +1.8% boost to the overall microbiome sequencing services market CAGR.

Declining NGS Cost per Gb

The cost of sequencing a human genome has collapsed from USD 100 million in 2001 to near-USD 500 by 2023, with sub-USD 10 projections now credible in specialized R&D environments [3]World Intellectual Property Organization, “Next-Generation Sequencing Cost Trends,” wipo.int . Such decline democratizes shotgun and long-read metagenomic studies, making the microbiome sequencing services market accessible to smaller biotechnology firms and large academic consortia alike. Yet as raw sequencing becomes commoditized and margins tighten, providers are compelled to differentiate via advanced analytics, quality management, and end-to-end workflow integration. Those focusing on multi-omic interpretation and clinical-grade reporting sustain premium pricing, whereas pure “per-Gb” providers encounter mounting price pressure. Consequently, cost deflation contributes a positive 1.5 percentage-point effect on the market CAGR, but only vendors that couple low-cost generation with value-added interpretation will fully capture the upside.

Growing Venture-Capital Funding in Microbiome-Based Therapeutics

Recent multimillion-dollar rounds—such as 32 Biosciences securing USD 119 million in NIH support and Vedanta Biosciences winning USD 3.9 million from CARB-X—signal robust investor confidence in live-biotherapeutic platforms. Commercial launches like VOWST, which recorded USD 10.1 million during its first quarter on the market, illustrate clear monetization paths. With capital inflows, therapeutics developers intensify discovery, characterization, and clinical validation programs, driving direct demand for strain-level sequencing, stability studies, and companion-diagnostic assays. This VC-backing cycles back to service providers because each funded IND or pivotal trial triggers steady sequencing contracts, adding roughly 1.2 percentage points to the microbiome sequencing services market CAGR.

Pharmaceutical Demand for Microbiome-Based Companion Diagnostics

Oncology, autoimmunity, and metabolic drug programs increasingly require companion assays that stratify patients by gut microbial signatures. Illumina’s partnership with Microba Life Sciences illustrates how sequencing vendors and clinical laboratories co-develop compliant pipelines tailored to pharmaceutical partners. FDA guidance for live-biotherapeutic products now expects rigorous analytical validation, thus elevating providers that meet CLIA, CAP, and ISO 15189 requirements. While high regulatory thresholds raise costs, they also create durable moats around providers who master good clinical practice and reproducible bioinformatics. As more immu notherapy and small-molecule pipelines integrate microbiome readouts, sequencing contracts migrate from exploratory research toward regulated diagnostics, a shift projected to add 1.0 percentage point to market growth.

Restraints Impact Analysis of Microbiome Sequencing Services Market*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ethical & legal issues around human microbiome data ownership | -1.2% | Global, with varying intensity by jurisdiction | Medium term (2-4 years) |

| Shortage of bioinformaticians skilled in multi-omic integration | -0.9% | Global, most acute in APAC and emerging markets | Short term (≤ 2 years) |

| High failure rate of probiotic therapeutic pipelines reducing service demand volatility | -0.7% | Global | Medium term (2-4 years) |

| Data-sovereignty laws restricting cross-border sample export | -1.0% | Global, particularly affecting US-China, EU-US flows | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ethical & Legal Issues Around Human Microbiome Data Ownership

Jurisdictions differ on whether microbial genetic material associated with a person constitutes personal data subject to biomedical privacy laws. China’s human-genetic resource rules demand in-country processing, while the Nagoya Protocol extends access-and-benefit-sharing to microorganisms whose provenance may span borders. The U.S. Department of Justice has proposed labeling microbiomic data as a controlled category, potentially limiting cloud processing with perceived-adversary nations. Each divergence imposes compliance overhead—from local servers to granular consent forms—that disproportionately burdens small and mid-size providers. Cross-border clinical trials, where samples traverse multiple regulatory regimes, now incur delays and incremental legal costs that subtract an estimated 1.2 percentage points from the microbiome sequencing services market CAGR.

Shortage of Bioinformaticians Skilled in Multi-Omic Integration

Complexity spikes when shotgun metagenomics merges with metatranscriptomics, metabolomics, and host genomics. Yet universities still graduate too few specialists conversant in statistics, immunology, and microbial ecology. Bioprocess facilities migrating toward digital twins similarly compete for coding talent versed in Python and R. Service providers consequently face rising wages, protracted recruitment, and potential project delays, especially in APAC where demand growth outpaces training. Automation and standardized workflows mitigate only part of the gap, leaving a 0.9 percentage-point drag on market expansion until labor supply equilibrates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Microbiome Sequencing Services Market Segment Analysis

By Sequencing Service Type:

Shotgun Dominance Drives Comprehensive ProfilingShotgun metagenomic sequencing held 42.98% of the microbiome sequencing services market share in 2025, underscoring its status as the primary method for strain-level and functional characterization. The approach generates expansive datasets that reveal resistance genes, virulence factors, and metabolic pathways, thereby supporting drug-discovery screens and biomarker identification. Continued cost declines and automation improve turnaround times, reinforcing shotgun’s appeal for both exploratory and regulated projects. Yet targeted 16S rRNA sequencing retains a foothold in cost-sensitive diagnostics and large epidemiological screens where taxonomic breadth suffices. Growth therefore materializes from service bundling, where providers layer full shotgun profiling onto initial 16S screens.

Whole-genome and metatranscriptomic sequencing is projected to rise at a 7.48% CAGR, driven by functional-omics demand in therapeutic design and regulatory submissions. As sponsors seek mechanistic insight beyond taxonomy, providers offering combined DNA/RNA and metabolite workflows capture higher-margin engagements. Targeted panel sequencing serves specialized needs such as antimicrobial-resistance surveillance, while other innovative services like spatial microbiomics emerge in surgical oncology and dermatology. Cumulatively, these trends support steady diversification of the microbiome sequencing services market, ensuring providers hedge against any single modality’s margin erosion.

By Technology:

Synthesis-Based Leadership Faces Ligation ChallengeSequencing-by-synthesis accounted for 40.78% of the microbiome sequencing services market revenue in 2025, benefiting from established chemistry that delivers high accuracy and throughput suitable for large clinical cohorts. Providers leveraging this platform enjoy mature reagent supply chains and software ecosystems, making synthesis a de-facto standard for regulated work. Nonetheless, sequencing-by-ligation is expected to record the fastest 7.38% CAGR, mainly because its chemistry handles fragmented or damaged DNA prevalent in fecal and environmental samples. As ligation-based platforms improve speed and output, providers are adopting hybrid fleets that pair synthesis for high-accuracy needs with ligation for more challenging matrices.

Nanopore sequencing gains mindshare for its real-time long-read capability, enabling rapid pathogen detection and structural-variant analysis. While still facing accuracy hurdles, iterative pore designs and machine-learning base-calling are narrowing the gap. Elsewhere, single-molecule methods and semiconductor detectors continue to advance, though their microbiome applications remain niche. Providers consequently operate multi-technology laboratories, selecting the optimal platform per sample type to sustain client retention amid an increasingly competitive microbiome sequencing services market.

By Application:

GI Dominance Challenged by Oncology ExpansionGastrointestinal diseases commanded 55.64% of the microbiome sequencing services market size in 2025 as therapeutics against recurrent C. difficile infection gained real-world traction. Post-market safety monitoring and real-world evidence programs require periodic sequencing that feeds long-term service contracts. However, oncology leads incremental demand, expanding at a 7.27% CAGR because microbiome composition is now recognized as a determinant of checkpoint-inhibitor efficacy and toxicity. Immuno-oncology trials increasingly embed stool or oral-microbiome arms, and companion-diagnostic projects in melanoma, colorectal, and lung cancers drive regulated sequencing volumes.

Infectious-disease applications leverage rapid metagenomics for hospital infection control, while CNS and neurodegeneration studies explore gut-brain signaling but remain largely pre-commercial. Dermatology, metabolic syndrome, and autoimmunity complete the “other” bucket, diversifying the client base as evidence matures. For service providers, portfolio breadth across applications mitigates cyclical volatility and positions them to capitalize on future regulatory approvals.

By End User:

Pharma Leadership Pressured by CRO GrowthPharmaceutical and biotechnology companies retained 34.96% share of the microbiome sequencing services market size in 2025 through direct investment in product pipelines and companion-diagnostic programs. Their sequencing spend covers discovery, preclinical toxicology, and clinical biomarker validation. Nevertheless, contract research organizations represent the fastest-growing customer group at 7.35% CAGR. CROs centralize specialized talent, standardized assays, and regulatory documentation, making them an efficient conduit for multiple sponsors. As mid-cap biotechs prioritize capital efficiency, outsourcing momentum intensifies, prompting sequencing vendors to forge preferred partnerships or embed facilities within CRO campuses.

Academic institutions remain vital contributors of exploratory projects and novel method development, while hospitals expand clinical sequencing to inform infection control and personalized medicine. Governmental and agricultural agencies round out demand, bringing microbial ecology and food-safety projects into scope. Together, these segments anchor a resilient client mix that shields the microbiome sequencing services market from downturns in any single sector.

Geography Analysis

North America Microbiome Sequencing Services Market

North America sustained its 42.31% revenue lead in 2025, anchored by FDA-recognized regulatory pathways, dense pharmaceutical clusters, and long-standing NIH funding streams. Live-biotherapeutic approvals, vendor collaborations, and venture-capital inflows all converge to keep sample volumes high, even as cost pressures encourage outsourcing to specialized CRO hubs. Proposed U.S. rules classifying microbiomic data as sensitive may constrain offshore analytics but are also prompting domestic providers to invest in secure cloud environments and FedRAMP-aligned pipelines, further entrenching local capacity.

Europe Microbiome Sequencing Services Market

Europe combines pan-EU regulatory harmonization with national-level biobank programs, sustaining diversified demand across academic, clinical, and commercial settings. New regulations on substances of human origin, which expressly include human microbiomes, create both compliance work and market opportunities for providers equipped with ISO 20387 biobank certification. The region’s tradition of rigorous data-protection frameworks incentivizes in-region analysis, benefiting providers with GDPR-compliant facilities and robust consent-management systems.

APAC Microbiome Sequencing Services Market

Asia-Pacific offers the fastest growth at 7.56% CAGR, reflecting China’s large-scale genomics investments and Japan’s structured national microbiome databases. Although data-sovereignty constraints complicate cross-border sequencing, domestic capacity investments by BGI, MGI, and local CROs keep project momentum strong. Governments in South Korea, Singapore, and Australia also expand precision-medicine budgets, underwriting longitudinal microbiome projects that funnel work to regional sequencing centers. Providers must navigate heterogeneous regulations, but successful localization strategies unlock large, under-served sample pools.

MEA and South America Microbiome Sequencing Services Market

The Middle East, Africa, and South America present nascent yet promising landscapes. Limited sequencing infrastructure and funding hamper immediate uptake; however, pilot national microbiome initiatives and technology park investments suggest growing interest. Providers partnering with local universities and public-health agencies can establish early footholds and shape future regulatory standards. Collectively, these geographies contribute incremental volumes that diversify the global microbiome sequencing services market and position it for sustained long-term growth.

Competitive Landscape

The microbiome sequencing services market remains moderately fragmented. Platform manufacturers such as Illumina dominate hardware supply but increasingly move upstream through clinical partnerships like the Microba Life Sciences alliance, which bundles sequencing kits with curated reference databases and AI-driven reporting. Specialized service firms differentiate by focusing on end-to-end study design, sample logistics, and multi-omic data fusion. For example, Oxford Nanopore’s PromethION 2 Integrated system furnishes rapid long-read capacity that service laboratories exploit for structural-variant detection and strain-resolved assemblies.

Consolidation is accelerating. Mapmygenome’s 2025 acquisition of Microbiome Insights brought a CAP-accredited lab and 600-client roster under one roof, illustrating how regional players scale footprint and intellectual property quickly. Venture-backed entrants aim at niche, high-value services such as AI-assisted strain identification or GMP-grade microbial banking. Success hinges on robust quality systems, regulatory savvy, and talent retention strategies that offset the industry-wide bioinformatics shortage.

Strategic collaborations also shape competitive dynamics. Sequencing vendors partner with CROs to embed platforms within clinical-trial networks, while diagnostics companies co-develop assays requiring dual regulatory submissions. Providers deploying cloud-native analysis pipelines compliant with HIPAA, GDPR, and regional data-sovereignty rules enjoy a defensible edge. As customers prioritize insight over data volume, firms offering integrated interpretation and clear clinical reporting are best positioned to claim recurring revenue and command premium pricing.

Microbiome Sequencing Services Industry Leaders

-

Merieux Nutrisciences Corporations

-

Microbiome Insights Inc.

-

MR DNA

-

Baseclear BV

-

Clinical Microbiomics AS

- *Disclaimer: Major Players sorted in no particular order

Microbiome Sequencing Services Market Companies Covered in this Report

- Illumina

- Baseclear

- CosmosID

- Zymo Research Corp.

- Clinical Microbiomics A/S

- Microba Life Sciences

- Microbiome Insights

- MR DNA (Molecular Research LP)

- Novogene Co., Ltd.

- BGI

- Pacific Bioscience

- Oxford Nanopore Technologies

- Rancho Biosciences

- Metabiomics Corp.

- Locus Biosciences

- uBiome Legacy Assets (Psomagen)

- ZIFO RnD Solutions

- Norgen Biotek

- Shanghai Realbio Technology Co., Ltd.

- Eurofins

- Merieux Nutrisciences

Market Opportunities and Future Outlook

Clinical-grade microbiome testing remains a key whitespace area versus research-use profiling, with demand pull from GI and oncology programs but uneven agreement on routine clinical utility. In Europe, the EU In Vitro Diagnostic Regulation (IVDR 2017/746) is tightening the separation between RUO workflows and validated diagnostic claims, which supports sequencing service providers that can pair assay performance packages with regulated bioinformatics and quality systems. Sequentia Biotech’s April 2026 CE-IVD marking for its MICK Clinical solution under IVDR is a concrete signal that service and software stacks are being packaged for diagnostic deployment, rather than stand-alone sequencing output.

On the technology and operations side, opportunity concentrates in cost-down and scale-up levers that make large cohorts and longitudinal sampling more practical for sponsors and biobanks. New library-prep strategies such as CUPID-seq (introduced May 2026) target higher multiplexing and lower preparation cost, aligning with the market shift from commodity per-Gb sequencing toward integrated, high-throughput study execution. At the same time, continued progress in long-read and real-time methods (including nanopore basecalling and R10.4 chemistry advances reported in 2026) supports finer amplicon variant resolution, expanding service menus beyond taxonomy into strain-level and functional readouts. For pharmaceutical and CRO customers, these offerings become more compelling when paired with submissions-ready reporting.

Recent Industry Developments in Microbiome Sequencing Services Market

- March 2026: BaseClear announced an expanded role in the Trillion Gene Atlas program and deployed the Ultima Genomics UG200 platform, positioning throughput to process more than 60,000 human genomes per year at 30x coverage. The announcement reinforces the market shift toward industrialized sequencing operations that can handle very large cohort volumes and sustain recurring analytics demand.

- December 2025: BaseClear introduced a Mycoplasma GMP testing service validated to European Pharmacopeia, ICH Q2, and ISO 17025-aligned guidelines. Adding regulated QC testing alongside genomics supports pharmaceutical and bioprocess clients that bundle microbiome sequencing, release testing, and documentation with a single supplier.

- November 2024: Cmbio launched as a unified brand bringing together Clinical Microbiomics, CosmosID, MS-Omics, DNASense, and Microba's Research Services unit. This consolidation broadened bundled microbiome and metabolomics service coverage across regions, strengthening end-to-end offerings spanning wet-lab sequencing and multi-omics interpretation.

Microbiome Sequencing Services Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers revenue earned from outsourced microbiome sequencing services, where biological samples are processed through sequencing workflows and the client receives usable outputs such as sequence data and related reporting.

Scope exclusions: Excluded from this sizing are sales of sequencing instruments and consumables when they are sold as products rather than delivered as a paid service.

Segments Covered in This Report

-

By Sequencing Service Type

- 16S rRNA Gene Sequencing

- Shotgun Metagenomic Sequencing

- Targeted Gene Panel Sequencing

- Whole Genome and Metatranscriptomic Sequencing

- Other Services

-

By Technology

- Sequencing by Synthesis

- Nanopore Sequencing

- Sequencing by Ligation

- Others

-

By Application

- Gastrointestinal Diseases

- Infectious Diseases

- Oncology

- CNS and Neurodegenerative Disorders

- Others

-

By End User

- Academic & Research Institutes

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations (CROs)

- Hospitals & Diagnostic Laboratories

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand pool and the service supply chain so the math stays tied to real research activity. We used public sources such as the National Institutes of Health funding databases, the National Library of Medicine for publication trends, the US FDA for relevant guidance and public records, and the World Health Organization for disease and surveillance context. To keep the service angle grounded, we also reviewed association and standards bodies such as the American Society for Microbiology, along with university lab portals and open protocol repositories that signal workflow preferences.

On the commercial side, we cross-checked company filings, investor presentations, press releases, and reputable news coverage to understand service mix shifts and regional expansion patterns. Where useful, paid subscriptions that track company financials, patent filings, and shipment level trade data were referenced to validate directional moves like capacity additions and cross-border sample logistics. The sources named above are illustrative only, and many other public documents and datasets were also used for data collection and validation.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions that most often move market value, especially pricing ranges, sample volumes, and what is counted as a billable sequencing service versus an adjacent lab activity. We spoke with service providers, lab operations leaders, and end-user teams in biopharma and research institutes across APAC, EMEA, and the Americas so regional utilization and procurement patterns could be compared on like terms.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | APAC: 38% |

| Mid tier: 43% | Functional/Unit leaders: 39% | EMEA: 37% |

| Smaller Players: 21% | Managers: 49% | Americas: 25% |

Market-Sizing & Forecasting

Our core build uses top-down reconstruction from the global microbiome research activity base, which is translated into expected sequencing service demand using adoption and outsourcing rates. After the first total is formed, it is corroborated with selective bottom-up checks such as sampled provider capacity, typical project throughput, and average selling price (ASP) ranges by service type, which helps us adjust outliers before finalizing totals.

Key model inputs include microbiome-related publication growth, funded project counts, the share of studies using shotgun versus targeted approaches, typical read depth and rerun rates that affect billable workloads, and regional lab capacity utilization signals. Pricing is not treated as a single average because ASPs differ by turnaround time, bioinformatics add-ons, and sample complexity, so we use ranges and then apply mix weights gathered through interviews. For forecasting, scenario analysis is used to reflect how funding cycles, clinical translation pace, and sequencing cost curves can shift demand, and then the scenario path is cross-checked against expert consensus for realism. When a country has limited direct signals, proxy indicators from research intensity and imports of lab inputs are used and then moderated through primary feedback.

Data Validation & Update Cycle

Validation is done by checking the modeled totals against independent signals such as research spending direction, publication and trial activity, and visible capacity expansion announcements, and then variances are investigated until the driver is understood. A second analyst reviews the model logic, formulas, and assumptions, followed by a final read-through that focuses on whether the outputs align with the stated scope and units.

If a large variance is seen during review, or if new information changes price or utilization assumptions, we re-contact relevant respondents to confirm the change before sign-off. Reports are refreshed on an annual cycle, and interim updates are made when material events occur such as policy changes, major funding shifts, or meaningful service capacity expansions. Before delivery, a fresh update pass is completed so clients receive the most current view available.

Mordor Intelligence's Microbiome Sequencing Services Market Estimate Compared With Other Published Estimates

Published market sizes for microbiome sequencing services often diverge because firms do not count the same revenue items, and they also use different base years, pricing logic, and forecasting windows. Gaps can widen when a study combines product sales with service revenue, or when regional coverage does not match how labs and studies actually source sequencing.

Sequencing instruments and consumables are kept outside Mordor Intelligence's scope here, which can pull the total down versus estimates that bundle kits, library prep, or platform revenue into the same number. Other differences typically come from how ASP changes are assumed over time, whether bioinformatics is included only when billed as part of the service, and how quickly newer clinical and pharma use cases are scaled in the forecast.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.94 B (2026) | |

| Global Consultancy A | USD 1.63 B (2024) | Uses an earlier base year and a shorter, near-term demand view that can understate newer outsourcing uptake, and it is not always clear how bundled analysis and bioinformatics fees are treated in the service value. |

| Industry Publisher B | USD 1.71 B (2024) | Runs on a different forecast window and may apply a uniform pricing progression, which can miss mix shifts between targeted and shotgun projects that change the effective ASP per study. |

The comparison mainly shows that year alignment and what gets counted as billable service work explain most of the spread. By anchoring the model to observable research activity and then checking it with provider level capacity and pricing ranges, the final estimate stays traceable to inputs that can be revisited and updated in a repeatable way.

Key Questions Answered in the Report

What is the current value of the microbiome sequencing services market?

The Microbiome Sequencing Services Market is valued at USD 1.94 billion in 2026 and is projected to reach USD 2.68 billion by 2031.

Which sequencing service type holds the largest market share?

Shotgun metagenomic sequencing leads with 42.98% market share, reflecting its comprehensive profiling capabilities.

Why are contract research organizations growing faster than pharmaceutical companies as end users?

Pharmaceutical firms increasingly outsource complex microbiome work to specialized CROs, driving the latter’s 7.35% CAGR through 2031.

Which geographical region is projected to grow the fastest?

Asia-Pacific is forecast to expand at a 7.56% CAGR, propelled by large-scale genomics investments and precision-medicine initiatives.

What are the main restraints limiting market growth?

Data-sovereignty laws, a shortage of bioinformaticians, ethical considerations around ownership of microbiome data, and the high failure rate of probiotic pipelines collectively temper the market’s expansion.

How are providers differentiating themselves amid falling sequencing costs?

Successful vendors focus on integrated bioinformatics, regulatory-grade quality systems, and multi-omic data interpretation rather than commodity sequencing capacity.

Page last updated on: