Talent Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

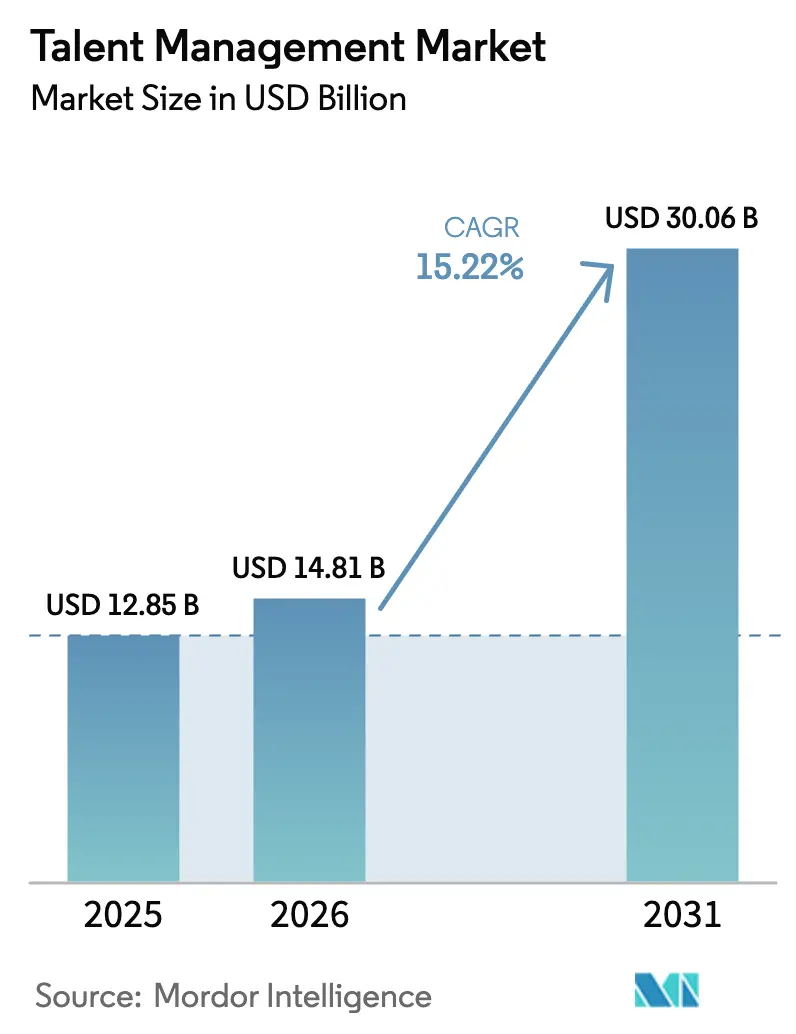

| Market Size (2026) | USD 14.81 Billion |

| Market Size (2031) | USD 30.06 Billion |

| Growth Rate (2026 - 2031) | 15.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Talent Management Market Analysis by Mordor Intelligence

The talent management market size was valued at USD 12.85 billion in 2025 and estimated to grow from USD 14.81 billion in 2026 to reach USD 30.06 billion by 2031, at a CAGR of 15.22% during the forecast period (2026-2031). The acceleration reflects enterprise recognition that talent is the most strategic asset in an AI-driven economy and that integrated cloud platforms can close urgent skills gaps. Generative AI is now embedded across recruiting, learning and performance workflows, tilting competitive advantage toward vendors able to combine data breadth with prescriptive analytics. North America commanded 38.50% 2024 revenue, but Asia-Pacific is expanding at 18.90% CAGR due to large-scale digital transformation programs in India, China and Southeast Asia. Learning & Training Management held the largest 2024 slice at 28.30%, while Generative-AI Talent Analytics led growth at 24.80% CAGR, underscoring the shift from static HR reporting to predictive workforce intelligence.[1]Workday Inc., “Form 10-K FY 2025,” workday.com

Key Report Takeaways

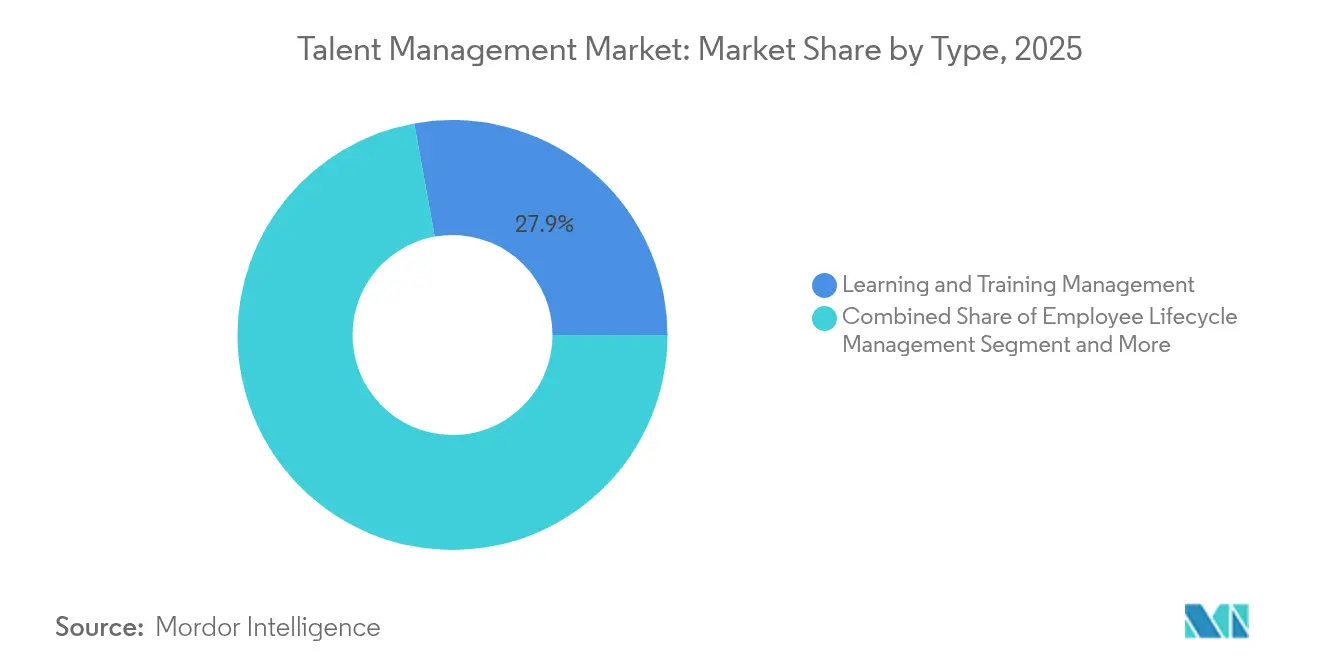

- By type, Learning & Training Management controlled 27.85% of the talent management market share in 2025, whereas Generative-AI Talent Analytics is advancing at 23.65% CAGR through 2031.

- By deployment model, the cloud segment captured 71.05% of the talent management market size in 2025 and is growing at 17.55% CAGR to 2031.

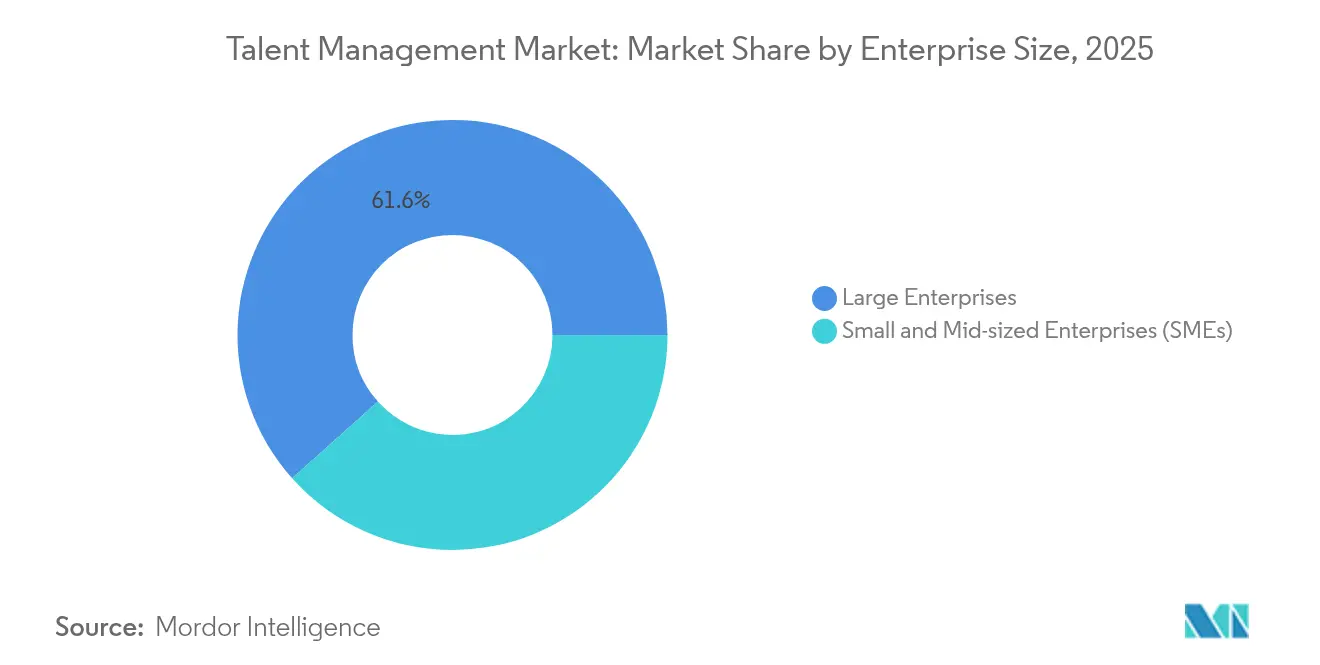

- By enterprise size, large enterprises held 61.60% revenue share in 2025, while SMEs post the fastest 16.95% CAGR outlook.

- By end-user, IT & Telecom led with 24.55% share of the talent management market in 2025; Retail & E-commerce is projected to surge at 20.65% CAGR.

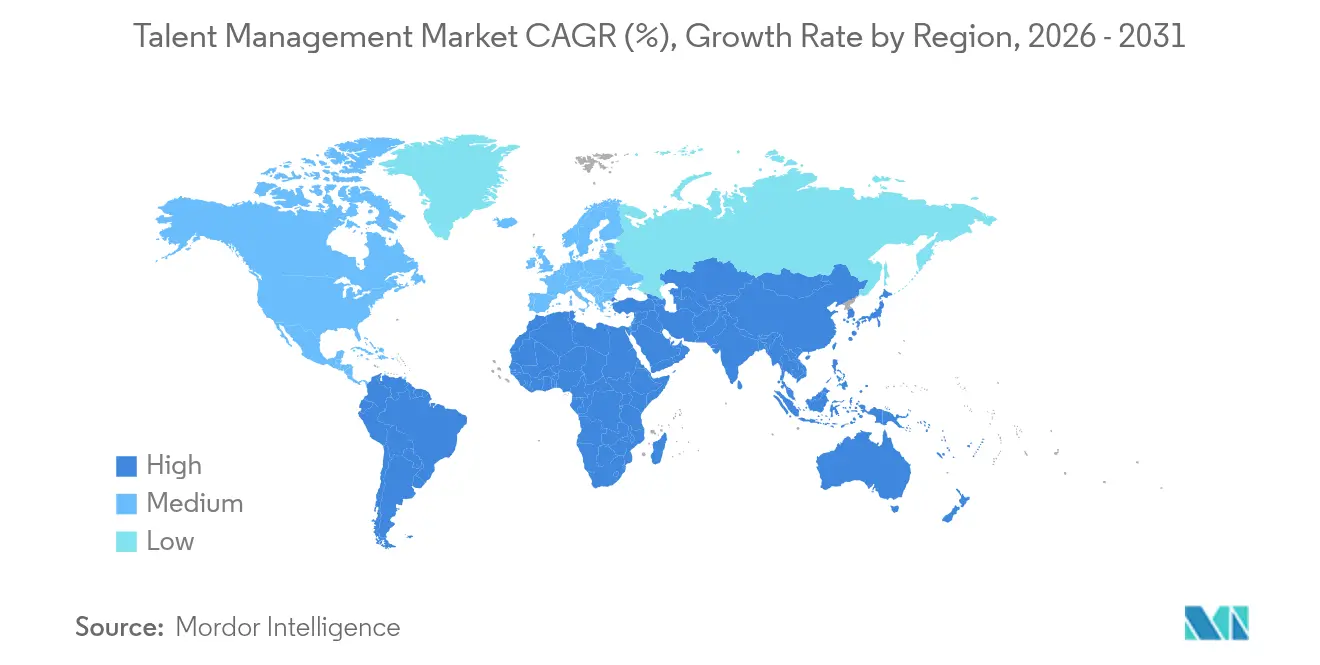

- By geography, Asia-Pacific represents the fastest-growing region at 18.35% CAGR, though North America retains leadership with 38.10% 2025 revenue.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Talent Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-augmented skills matching | 3.20% | Global, with early adoption in North America & Europe | Medium term (2-4 years) |

| Generative-AI copilots for HR workflows | 4.10% | North America & EU leading, APAC following | Short term (≤ 2 years) |

| Cloud-first HCM platform consolidation | 2.80% | Global, accelerated in Asia-Pacific | Long term (≥ 4 years) |

| Demand for skills-based workforce planning | 3.50% | Global, particularly strong in IT & Financial Services | Medium term (2-4 years) |

| Compliance-driven pay-equity analytics | 1.90% | EU, North America, expanding to APAC | Long term (≥ 4 years) |

| Employee-centric EX architecture | 2.10% | Global, with premium adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-Augmented Skills Matching

Skills-based orchestration is displacing credential-focused hiring as firms confront persistent talent shortages. Johnson & Johnson boosted voluntary learning by 20% after introducing AI skills inference that mines work patterns and project outcomes to form dynamic profiles, closing identification gaps that left 87% of executives uncertain about real workforce deficiencies. Cisco’s predictive planning cut new-hire time-to-productivity by 35% by linking project requirements to inferred capabilities, demonstrating strategic value for large portfolios. Natural-language processing now scans job posts, reviews and learning data to surface transferable competencies, making internal mobility faster and reskilling spend more targeted.

Generative-AI Copilots for HR Workflows

The share of HR leaders using AI tools rose to 38% in 2025 from 19% in 2023, and analysts calculate up to 67% value potential across recruiting, performance and people analytics activities. Workday’s recent releases feature conversational agents that handle interview scheduling, candidate messaging and learning curation; 30% of Q4 2024 expansions contained at least one AI module. These copilots shift HR staff from repetitive tasks to strategic design, though governance layers are essential to maintain communication quality and avoid errant decisions.

Cloud-First HCM Platform Consolidation

Oracle’s cloud revenue jumped 27% year-on-year in Q1 2025, with Cloud ERP up 34%, reflecting widespread migration from siloed HR modules to unified suites. SAP echoed the pattern as its cloud backlog reached EUR 18.2 billion, surging 28%, showing buyers prefer integrated data structures that span recruiting, learning and analytics. Consolidation lets enterprises phase out disparate vendors, gain consistent data models and support skills-based planning at scale, but pressures point-solution providers to broaden capabilities or seek acquisition.

Demand for Skills-Based Workforce Planning

IBM’s pivot to skills-centric planning halved time-to-hire and raised employee engagement 20% by matching internal capabilities with growth priorities. WEF forecasts that 50% of global workers need reskilling by 2027, directing HR budgets toward analytics that identify adjacent skills and link learning to business growth. LinkedIn’s natural-language job matching illustrates sector best practice, aligning candidates with openings even without exact role matches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Algorithmic bias & DEI litigation risk | -2.30% | North America & EU primarily, expanding globally | Short term (≤ 2 years) |

| Data-sovereignty regulations (e.g., EU, India) | -1.80% | EU leading, APAC following, limited US impact | Medium term (2-4 years) |

| Legacy HRIS integration debt | -1.40% | Global, particularly acute in large enterprises | Long term (≥ 4 years) |

| Plateauing HR tech budgets in SMBs | -1.10% | Global, most pronounced in cost-sensitive markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Algorithmic Bias & DEI Litigation Risk

The Mobley v. Workday ruling confirmed that providers can face direct liability for discriminatory outcomes, accelerating vendor investments in bias detection and audit tooling. California’s July 2025 civil-rights updates require bias audits and applicant notices for automated hiring, while New York’s AI Act grants opt-out rights. These mandates raise compliance overheads and may slow rollouts of new AI features until audit frameworks mature.

Data-Sovereignty Regulations

The EU AI Act (effective August 2024) introduces mandatory risk assessments and transparency obligations for high-risk HR applications. India and several ASEAN states are drafting localization rules that compel regional data storage, generating demand for multi-tenant architectures capable of isolating data by jurisdiction. Smaller vendors lacking global infrastructure face disproportionate burden, hastening consolidation toward larger providers able to absorb compliance costs. [2]U.S. District Court N.D. Cal., “Mobley v. Workday,” courtlistener.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Learning Platforms Drive AI Integration

Learning & Training Management produced 27.85% of the talent management market revenue in 2025 as enterprises prioritized continuous development over episodic courses. The segment’s scale highlights the urgency of reskilling when 50% of workers may need new capabilities by 2027. Generative-AI Talent Analytics, the fastest-growing subsegment at 23.65% CAGR, extends analytics from descriptive dashboards to predictive insights that guide workforce planning. Recruiting Management continues steady uptake amid global talent shortages, while Compensation Management gains momentum on pay-equity mandates.

Cornerstone OnDemand’s launch of the AI-powered Cornerstone Galaxy platform illustrates the pivot toward personalized learning journeys that adapt to usage patterns. Service revenue is rising as enterprises seek implementation, change-management and governance support to realise platform value. Generative AI permeates each product line, but responsible-AI demands force providers to build robust audit trails and explainability functions that satisfy regulators and corporate ethics boards.

By Deployment Model: Cloud Acceleration Continues

Cloud deployments accounted for 71.05% of 2025 spending, and the segment is scaling at 17.55% CAGR as organizations pursue flexibility and real-time insights. The COVID-19 era proved remote talent management feasible, prompting enterprises to migrate still-on-prem HR suites to SaaS. Workday’s unified architecture and Oracle’s multicloud roadmap showcase the momentum.

On-prem deployments persist in highly regulated sectors, yet the segment is contracting as zero-trust and regional cloud zones ease data-sovereignty fears. Multi-cloud strategies are emerging to avoid vendor lock-in, creating demand for middleware and integration specialists. Scalable AI services-such as real-time sentiment analytics-are now viable only in cloud contexts, reinforcing the shift.

By Enterprise Size: SME Adoption Accelerates

Large enterprises still generated 61.60% of 2025 revenue by exploiting platform breadth to manage complex global workforces. They also spearhead AI adoption: Workday recorded AI modules in 30% of Q4 2024 expansions. Yet SMEs represent the fastest trajectory at 16.95% CAGR because SaaS economics now bring enterprise-grade analytics to smaller budgets.

UKG’s 72% jump in SMB bookings reflects pent-up demand for modern HR capabilities that simplify compliance and improve retention. Lightweight interfaces from BambooHR and others resonate with resource-constrained teams, while integration to finance and collaboration tools reduces duplication. Inflated labour competition forces SMEs to professionalize talent management, escalating platform penetration.

By End-User: IT Sector Leads Digital Transformation

IT & Telecom held 24.55% of 2025 spend owing to early AI adoption and fierce competition for cloud, cybersecurity and data science skills. Retail & E-commerce is accelerating at 20.65% CAGR, driven by high turnover, seasonal spikes and omnichannel expansion. McKinsey estimated 2.5 million more US retail openings than job seekers in 2024, amplifying demand for scalable scheduling, onboarding and analytics tools.

BFSI buyers emphasise audit trails and risk scoring, while governments pursue modernization mandates such as the US Office of Personnel Management’s goal to cut time-to-hire below 80 days. Education institutions adopt platforms to mitigate IT talent shortages and modernize faculty development paths. These varied needs spur verticalized product roadmaps and ecosystem collaborations.

Geography Analysis

North America retained 38.10% of 2025 revenue, supported by early cloud maturity, stringent bias-mitigation regulations and heavyweight vendors headquartered in the region. Federal modernization programs, including efforts to streamline public-sector hiring, create a dependable pipeline of large contracts. State-level AI rules add compliance complexity that favors suppliers with mature governance playbooks. Private-sector buyers deepen investments in predictive analytics to unlock productivity gains and differentiate employee experiences.

Asia-Pacific is posting an 18.35% CAGR through 2031, the fastest globally, as India, China and fast-growing ASEAN economies swap legacy HRIS for cloud suites. ILO projects 1.7% employment growth in 2025, yet 66% of employment remains informal, signalling vast headroom for formalization. Governments incentivize digital skills, and soaring demand for AI engineers heightens platform uptake. Japan’s aging workforce intensifies internal-mobility initiatives, while evolving data-localization rules spark demand for in-region cloud capacity.

Europe blends moderate expansion with the world’s toughest compliance landscape. The EU AI Act and Pay Transparency Directive require bias audits, human oversight and salary disclosure, raising costs for vendors but also creating pull for compliance-grade analytics offerings. Multi-lingual, multi-currency complexity drives demand for localized user experiences. Brexit’s regulatory divergence means software updates must account for UK-specific guidance alongside EU law, increasing development cycles.

The Middle East and Africa demonstrate early-stage but rising adoption, especially among Gulf Cooperation Council firms pursuing economic diversification that relies on attracting skilled expatriate talent. South America likewise grows from a smaller base; Brazil’s Equal Pay Law mandates biannual transparency reports, sparking interest in pay analytics modules. Together these regions expand the global addressable market beyond mature economies.

Competitive Landscape

The talent management market shows moderate concentration. Workday led with USD 8.446 billion fiscal-2025 revenue on 16.4% annual growth, leveraging a unified data core to cross-sell AI modules. Oracle capitalizes on its ERP footprint to embed talent workflows and recorded 27% cloud revenue growth in Q1 2025. SAP drove AI into half of Q4 2024 HCM deals, while UKG surpassed USD 1 billion quarterly revenue through verticalized suites.

Differentiation is shifting to AI governance. The Mobley case underscored liability risk, so leading vendors tout bias-detection, audit registries and explainability layers. New entrants such as Eightfold AI and Gloat focus on talent intelligence and internal mobility, forcing incumbents to accelerate roadmap delivery or buy niche specialists. Platform breadth encourages buyers to consolidate contracts, pressuring point solutions to diversify or seek mergers. Private-equity interest persists, illustrated by CVC backing World of Talents, signaling confidence in operational upside achievable through technology integration.

Strategic moves include Oracle expanding multicloud options with Microsoft Azure integration, Workday’s HiredScore acquisition to sharpen AI-driven recruiting, and Cornerstone’s bid for SumTotal to widen learning content catalogs. Vendors also bundle pay-equity analytics to meet EU mandates and deliver region-specific data residency controls as localisation laws spread. Overall, price competition is moderate due to high switching costs and embedded data, but innovation pace is intense as providers race to infuse safe, value-adding AI across the suite. [4]Gloat, “Talent Marketplace Adoption Case Studies,” gloat.

Talent Management Industry Leaders

Workday Inc.

Oracle Corporation

SAP SE

ADP Inc.

Ultimate Kronos Group (UKG Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Cornerstone OnDemand entered a definitive agreement to acquire SumTotal from Skillsoft, expanding enterprise learning capabilities.

- January 2025: Paychex agreed to buy Paycor HCM for USD 4.1 billion, targeting USD 80 million cost synergies and amplified AI investment.

- January 2025: UKG appointed Arlen Shenkman as President and CFO, signalling a fresh operational focus.

- April 2024: Cornerstone OnDemand launched the AI-powered Cornerstone Galaxy workforce agility platform.

Global Talent Management Market Report Scope

Talent management is a process used by companies to optimize how they recruit, train and retain employees. Through human resources processes, such as strategic workforce planning, companies can anticipate their needs and goals and attempt to hire a workforce that reflects those needs.

The talent management market is segmented by type (solution, services), by deployment (cloud, on-premises), by enterprise size (SMEs, large enterprises), by end-user (BFSI, IT and telecom, retail and e-commerce, government, education, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Solutions | Recruiting Management |

| Compensation Management | |

| Employee Lifecycle Management | |

| Learning and Training Management | |

| Performance Management | |

| Other Solutions | |

| Services |

| Cloud |

| On-Premises |

| Small and Mid-sized Enterprises (SMEs) |

| Large Enterprises |

| Banking, Financial Services and Insurance (BFSI) |

| IT and Telecom |

| Retail and E-commerce |

| Government |

| Education |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Solutions | Recruiting Management |

| Compensation Management | ||

| Employee Lifecycle Management | ||

| Learning and Training Management | ||

| Performance Management | ||

| Other Solutions | ||

| Services | ||

| By Deployment Model | Cloud | |

| On-Premises | ||

| By Enterprise Size | Small and Mid-sized Enterprises (SMEs) | |

| Large Enterprises | ||

| By End-User | Banking, Financial Services and Insurance (BFSI) | |

| IT and Telecom | ||

| Retail and E-commerce | ||

| Government | ||

| Education | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the talent management market?

The talent management market stands at USD 14.81 billion in 2026 and is forecast to reach USD 30.06 billion by 2031.

Which segment accounts for the largest talent management market share?

Learning & Training Management leads with 27.85% 2025 revenue.

How fast is the cloud deployment segment growing?

Cloud deployments are expanding at an 17.55% CAGR through 2031.

Which region shows the fastest growth?

Asia-Pacific is the fastest-growing region, advancing at 18.35% CAGR.

What is driving demand for generative-AI talent analytics?

Organizations seek predictive insights to align workforce skills with rapid technology shifts, lifting the subsegment at 23.65% CAGR.

How are regulations affecting vendor strategies?

Rules such as the EU AI Act and bias-audit mandates compel providers to invest in governance, making compliance a key differentiator.

Page last updated on: