Workforce Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

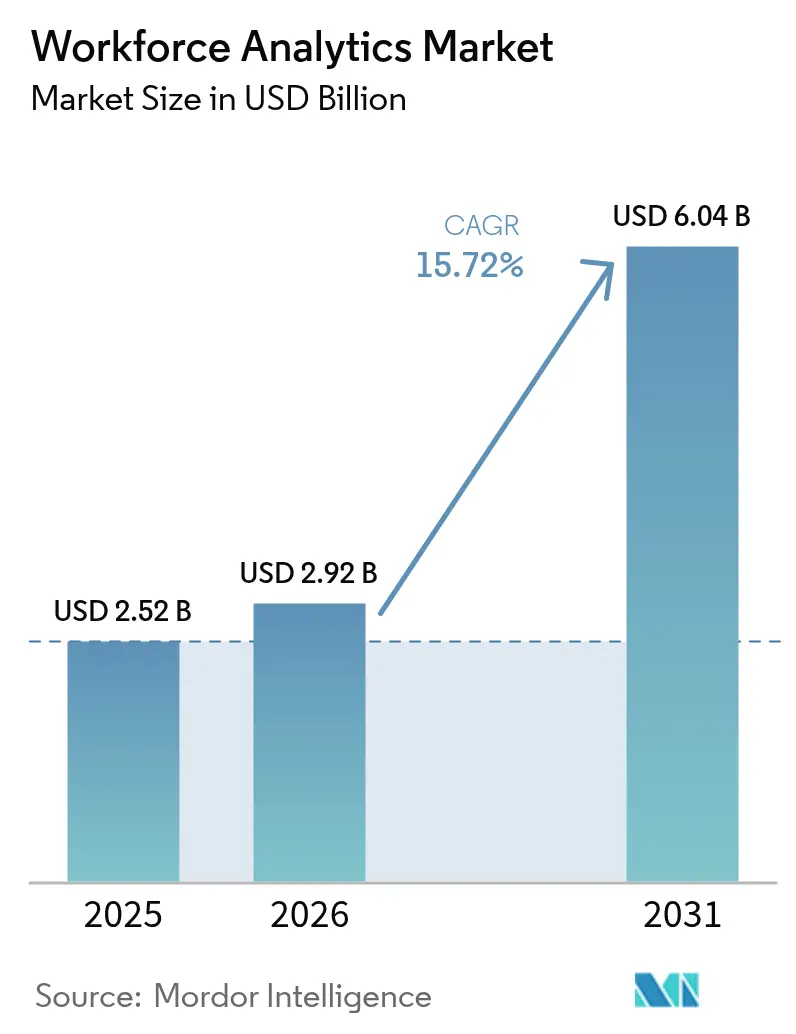

| Market Size (2026) | USD 2.92 Billion |

| Market Size (2031) | USD 6.04 Billion |

| Growth Rate (2026 - 2031) | 15.72% CAGR |

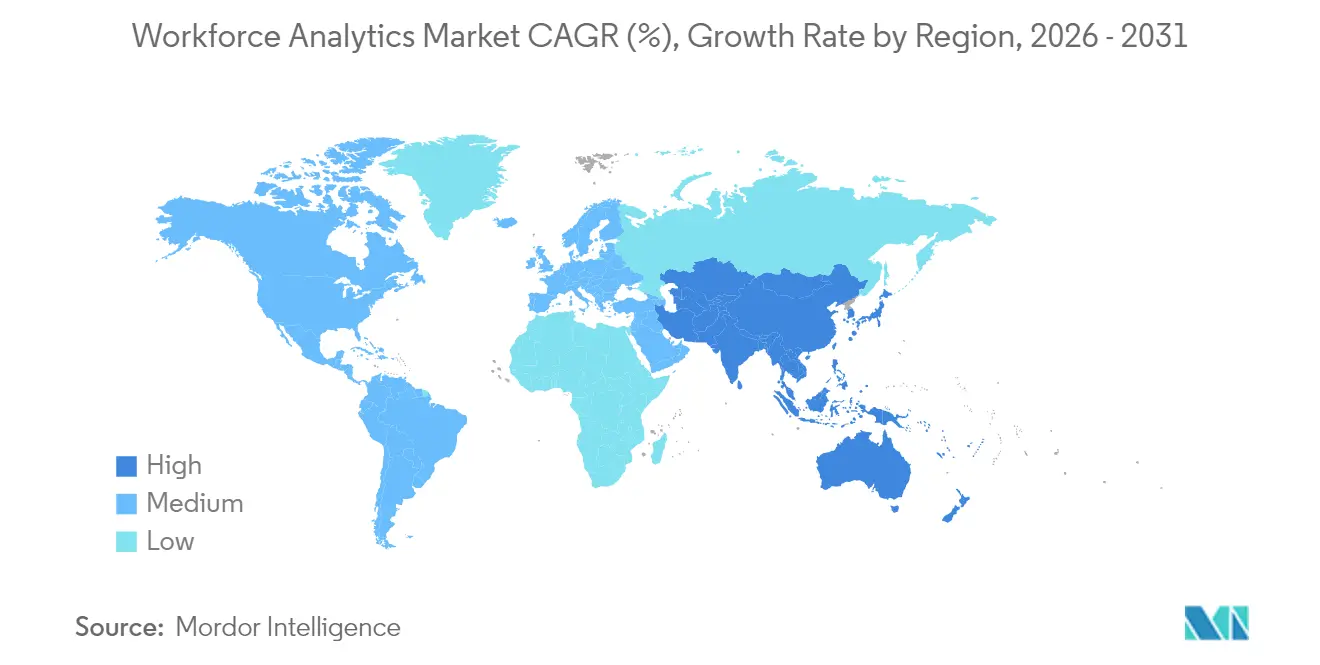

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Workforce Analytics Market Analysis by Mordor Intelligence

The workforce analytics market size in 2026 is estimated at USD 2.92 billion, growing from 2025 value of USD 2.52 billion with 2031 projections showing USD 6.04 billion, growing at 15.72% CAGR over 2026-2031. Growth stems from organizations moving rapidly toward data-driven talent decisions, hybrid-work optimization, and AI-powered analytics. Heightened focus on predictive planning, real-time insights, and cost optimization keeps demand robust even in cautious economic climates. Cloud-based deployments expand quickly as integration with HCM suites multiplies data volumes and unlocks use cases, while sector-specific needs in healthcare and manufacturing accelerate adoption. Regional momentum is striking: North America commands early enterprise uptake, yet Asia-Pacific’s digital transformation programs create the fastest expansion path. Competitive dynamics stay moderately intense as HCM platform leaders fold analytics into core offerings and pure-play vendors pursue strategic funding rounds, acquisitions, and partnerships to build scale.

Key Report Takeaways

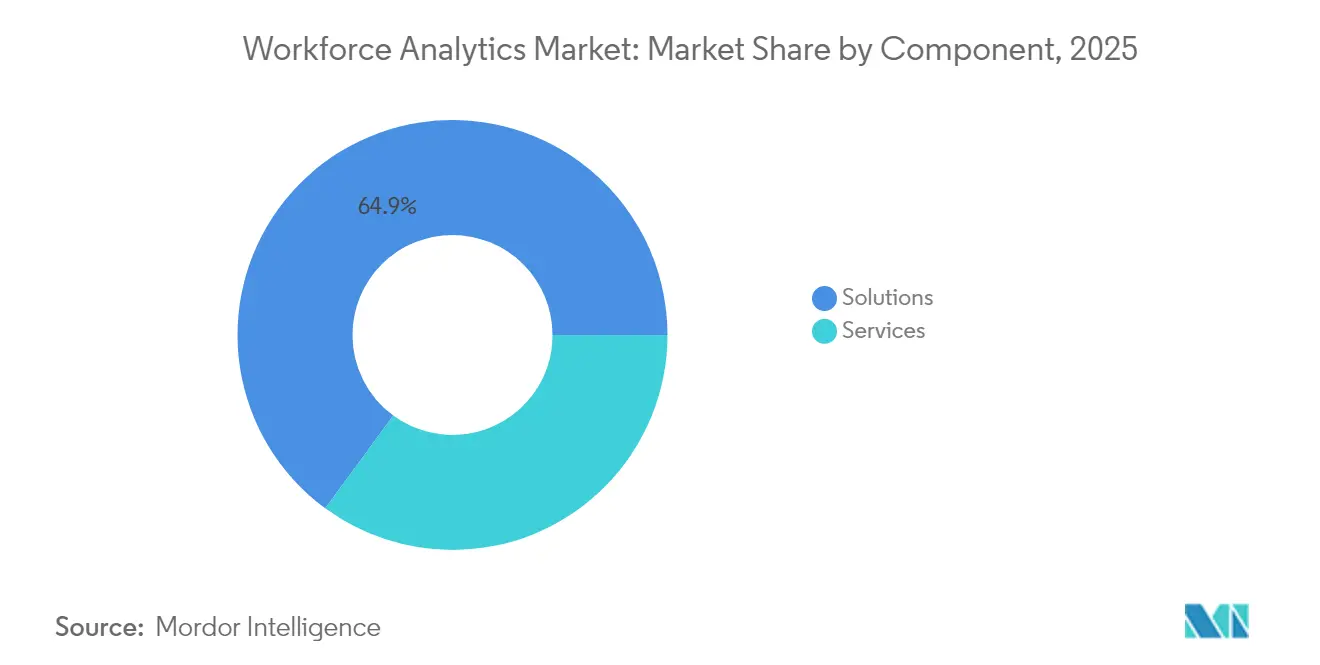

- By component, solutions led with 64.92% of the workforce analytics market share in 2025; services are projected to rise at 16.74% CAGR through 2031.

- By deployment, cloud models accounted for 58.62% share of the workforce analytics market in 2025, while hybrid cloud exhibits the quickest 16.32% CAGR to 2031.

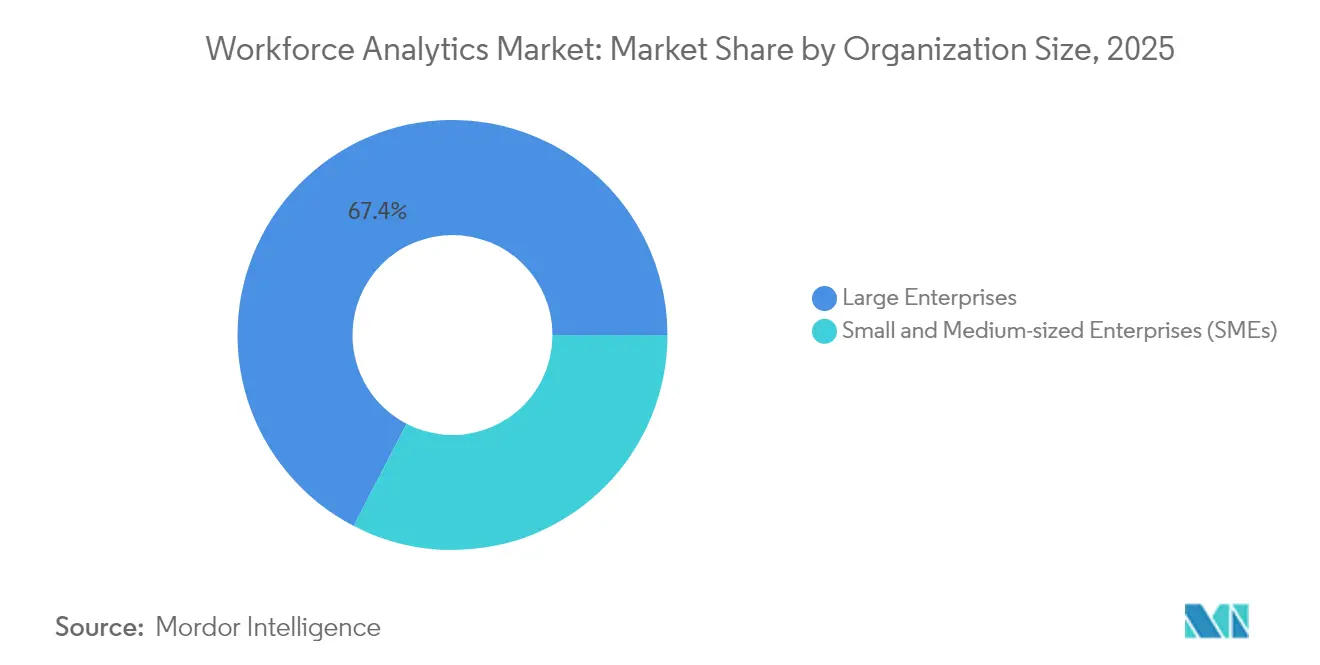

- By organization size, large enterprises held 67.40% share in 2025, whereas SMEs post the highest 17.25% CAGR over the forecast period.

- By end-user industry, BFSI led with 27.08% revenue share in 2025; healthcare is set to expand at an 17.66% CAGR to 2031.

- By geography, North America captured 25.45% of the workforce analytics market size in 2025, while Asia-Pacific advances at a 16.05% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Workforce Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing need for data-driven talent decisions in hybrid workplaces | +3.2% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| Proliferation of HR data from cloud HCM suites | +2.8% | Global, accelerated in Asia-Pacific | Short term (≤ 2 years) |

| Adoption of AI/ML for predictive people analytics | +4.1% | North America and Europe leading | Medium term (2-4 years) |

| Workforce cost optimization amid economic uncertainty | +2.5% | Global, stronger in developed economies | Short term (≤ 2 years) |

| Shift to skills-based talent marketplaces | +1.9% | North America and Europe expanding globally | Long term (≥ 4 years) |

| ESG and diversity-reporting mandates | +1.5% | Europe and North America, rising in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-Powered Predictive Analytics Transforms Workforce Decision-Making

Enterprise adoption of machine-learning models allows HR teams to predict talent gaps, refine allocation, and lift retention. Johnson & Johnson’s AI skills-inference framework, which builds taxonomies and passive assessments, improved learning alignment and hiring accuracy. Manufacturing illustrates urgency: 42% of plants plan to raise AI/ML use within five years, with 50% deploying quality-control AI in the coming year.[1]Rockwell Automation, “State of Smart Manufacturing Report 2025,” rockwellautomation.com Managers shift roles as 70% view workforce transformation as critical to performance. These factors collectively stimulate enterprise demand across the workforce analytics market.

Cloud HCM Integration Drives Data Proliferation and Analytics Adoption

Cloud HCM suites such as Oracle Fusion HCM Analytics and SAP SuccessFactors Workforce Analytics offer real-time metrics on composition, compensation, and skills, empowering HR leaders to match capabilities to business goal. [2]Oracle Corporation, “Fusion HCM Analytics Product Sheet 2025,” oracle.com Integration platforms like One Model standardize data from multiple HCM sources and enrich it with predictive insights on attrition and pay equity. Municipal deployments highlight scale: the City of Los Angeles runs Workday for 50,000 staff, with AI guiding resume screening and skill tagging. Cloud ubiquity therefore accelerates use-case volume across the workforce analytics market.

Skills-Based Talent Marketplace Evolution Requires Advanced Capability Mapping

Organizations pivot from job-centric designs to skills-focused structures that support dynamic deployment and career mobility. TechWolf’s USD 43 million investment and Microsoft’s Copilot People Skills tool signal heightened interest in AI-driven skills inference. Mercer reports 70% of firms have skills libraries and 23% link skills to rewards, validating strategic readiness. PwC and Workday’s alliance on Skills Cloud shows consultancy-platform collaboration to bridge capability gaps. Skills emphasis broadens the addressable base for the workforce analytics market.

Economic Uncertainty Accelerates Workforce Cost Optimization Strategies

Volatile macro conditions push companies to deploy analytics that balance cost control with engagement. Randstad stresses data-enabled agility to cross-train staff and shape contingency plans. Manufacturers face 75% labor shortages and anticipate recession impacts, reinforcing demand for advanced planning . Visier’s research proves redeployment and overtime reduction can replace layoffs, highlighting ROI from analytics. Fiscal discipline keeps analytics popularity high across the workforce analytics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and compliance complexity | -2.1% | Europe leading, global adoption | Medium term (2-4 years) |

| High implementation cost and change-management burden | -1.8% | Global, cost-sensitive markets | Short term (≤ 2 years) |

| Algorithmic-bias and ethics concerns | -1.3% | Primarily developed markets | Long term (≥ 4 years) |

| Fragmented data silos in gig ecosystems | -1.1% | Global, service economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Regulatory Compliance Complexity Constrains Market Growth

The EU AI Act, effective August 2024, designates many HR-AI applications high-risk, demanding risk assessments and transparency.[3]RemoFirst, “EU AI Act: Implications for HR,” remofirst.com GDPR obligations deepen as firms integrate large language models, mandating explainable AI and privacy-by-design workflows. In North America, CCPA and state AI laws leave 42% of HR managers uncertain about compliance. These overlapping mandates slow decision cycles and elevate total cost of ownership for the workforce analytics market.

High Implementation Costs and Change Management Complexity Limit Adoption

Hospitals, where labor now forms nearly 50% of costs, need analytics yet must fund sizeable platform and change-management programs. Manufacturers show ambition 89% intend to add AI but only 16% achieve scale due to process and people hurdles. Budget scrutiny in SMEs forces phased rollouts and ROI justification. These pressures temper the otherwise strong outlook for the workforce analytics industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: AI-Enhanced Solutions Sustain Market Leadership

Solutions represented 64.92% of the workforce analytics market in 2025, reflecting pervasive demand for comprehensive platforms that embed predictive algorithms. Talent acquisition and development optimization solutions enjoy strong momentum as enterprises fill skills gaps; Huntington Ingalls Industries recorded 25% faster hiring and 30% higher retention by deploying AI-native tools. Performance and engagement analytics also expand as El Camino Health reduced RN turnover by 7 points, saving USD 840,000 annually. Services, although smaller, post 16.74% CAGR as firms secure implementation, managed-service, and training support. Professional services guide complex data migrations, while managed services allow HR teams to focus on strategy. The introduction of generative AI assistants such as Visier’s “Vee” sharpens competitive differentiation and sustains solution growth.

Training and support fetch mounting interest: 31% of manufacturers cite upskilling needs to realize analytics initiatives. Providers that bundle learning and change-management modules thereby capture incremental share within the workforce analytics market.

By Deployment Type: Cloud Ascendancy Continues

Cloud platforms held 58.62% share in 2025 and will grow at 15.86% CAGR as organizations chase lower upfront costs and seamless upgrades. One Model proves value by abstracting data from Workday and SAP SuccessFactors into analytics-ready frameworks. Large public-sector clients such as Los Angeles showcase scale and security when managing tens of thousands of employees on cloud stacks.

On-premises retains relevance where data sovereignty dictates, especially in BFSI and defense. Hybrid deployment emerges as a compromise, storing sensitive data locally while running analytics compute in the cloud. Vendors strengthen encryption and permission models: SAP and Oracle both add role-based controls and compliance attestations. The workforce analytics market therefore skewers decisively toward cloud without abandoning localized models.

By Organization Size: SME Uptake Accelerates

Large enterprises controlled 67.40% revenue in 2025 by virtue of complex global structures demanding granular insights. They account for many marquee wins, such as a Fortune 500 manufacturer boosting AI proficiency by 54% after analytics-driven upskilling. However, SMEs record the highest 17.25% CAGR thanks to SaaS pricing and simplified interfaces. Pre-configured dashboards, automated insights, and low-code customization let smaller firms deploy analytics without heavy IT support.

Visier’s partnership with Le Lab RH extends enterprise-class platforms to French start-ups, underlining vendor strategy to penetrate the long-tail customer base. As a result, the workforce analytics market becomes more democratized, widening total addressable demand.

By End-User Industry: Healthcare Surges Ahead of BFSI Stronghold

BFSI retained 27.08% of total revenue in 2025 due to regulatory reporting and intensive data footprints. A Fortune 100 insurer slashed dashboard build time from three weeks to one day using Workday Prism Analytics, sharpening manager access to self-service insights. More than 87% of BFSI firms intend further AI spend, targeting personalization and productivity.

Healthcare, however, is on track to post an 17.66% CAGR, fastest among all verticals, as hospitals fight acute nurse shortages that could reach 450,000 by 2025. INTEGRIS Health saved USD 30 million by halving contingent staff reliance through analytics-guided scheduling. Manufacturing, IT-Telecom, retail, public sector, and energy also deepen use cases, but healthcare’s pressing workforce shortages keep it in the spotlight of the workforce analytics market.

Geography Analysis

North America held 25.45% of the workforce analytics market in 2025, supported by SEC disclosure mandates that push granular workforce metrics. The City of Los Angeles demonstrates advanced maturity by automating hiring and payroll for 50,000 staff through Workday’s AI features, lowering processing times materially. Canada capitalizes on public-sector digitization, while Mexico rides near-shoring to embed analytics in manufacturing HR programs.

Asia-Pacific shows the fastest 16.05% CAGR through 2031. India’s Tata Steel Kalinganagar plant saved USD 4 million annually by training 130 staff in analytics and boosting strike rates from 60% to 90%. China invests aggressively to align automation and worker reskilling, while Japan and South Korea blend analytics with aging-workforce strategies. Australia and New Zealand apply analytics to retain healthcare professionals, where only 41% stay more than two years in non-metro areas.

Europe grows steadily on the back of GDPR and the AI Act, which both demand transparent algorithms and human oversight. Germany, the United Kingdom, and France implement at scale, with French start-ups benefiting from Visier and Le Lab RH collaboration. The Netherlands sees robust adoption among multinationals, whereas Southern Europe lags because of limited analytics talent supply. Middle East and Africa constitute early-stage opportunities: UAE and Saudi Arabia weave analytics into Vision 2030 programs, and South Africa begins public-sector pilots focused on skills mapping.

Regulatory Landscape

Workforce analytics platforms sit at the intersection of privacy and AI-governance regimes because they ingest sensitive employee data and can affect decisions across hiring, promotion, performance, and termination. In the European Union, Regulation (EU) 2024/1689 (the EU AI Act) explicitly treats several employment-related AI use cases as high-risk (Annex III), which triggers obligations around transparency to users (Article 13), automatic logging and record-keeping (Article 12), and post-market monitoring (Article 72). The AI Act entered into force on August 1, 2024, and the timetable for full application of high-risk obligations is linked to the availability of harmonized standards, increasing the weight of compliance-ready product documentation in vendor selection.

In the United States, regulation is more fragmented across privacy and employment rules. New York City Local Law 144 requires annual bias audits when automated employment decision tools are used for hiring or promotion, with enforcement beginning July 5, 2023. This is pushing buyers to seek auditability and explainability from vendors. California privacy requirements under the CPRA, enforced by the California Privacy Protection Agency (CPPA), extend employee data rights (access, correction, deletion) and increase governance needs for analytics programs that blend HR, payroll, and collaboration data. Together, these requirements raise demand for privacy-by-design, model governance, and documented controls across cloud, hybrid, and on-premises deployments.

Competitive Landscape

The workforce analytics market exhibits moderate concentration. Established HCM vendors—Workday, SAP, Oracle, UKG—bundle analytics natively into HR suites, while specialists such as Visier, ChartHop, and CultureAmp differentiate through depth of analytics and AI features. Visier raised USD 125 million (Series E) and bought Yva.ai to widen organizational-network insights, then joined with The Josh Bersin Company for richer benchmarks.

Consolidation accelerates: Workday acquired HiredScore for AI-optimized hiring and Cornerstone Galaxy absorbed SkyHive to reinforce skills-based management. TalentNeuron purchased HRForecast to merge internal employee data with external labor intelligence, forming an end-to-end planning engine. Partnerships proliferate as integrators seek ecosystem breadth: Workday allies with Randstad for AI-enabled recruiting, UKG taps Lightcast for skills data, and Paycor embeds Visier analytics.

Workforce Analytics Industry Leaders

Accenture plc

ADP, Inc.

BambooHR LLC

Capgemini SE

Ceridian HCM Holding Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace is translating workforce analytics outputs into defensible business outcomes and connecting those results to finance systems, especially as organizations scale AI-enabled work. Lanai's June 2026 AI Labor Report points to a measurement gap: many large organizations track the financial impact of AI-generated work, but only a smaller portion keeps clear outcome records, and a large share lacks consistent attribution methodology. That gap creates room for workforce analytics vendors and integrators to productize ROI attribution, linking people, skills, and productivity signals to ledger-ready metrics and the governance artifacts needed for auditability requirements.

Opportunities also expand in workforce planning, skills inference, and workflow automation inside HCM ecosystems, where enterprises are prioritizing unified data foundations and automation. Dresner Advisory Services (February 2026) cited workforce planning and analysis as a high priority, and also highlighted growing interest in agentic AI for process automation and issue identification. This supports packaged planning, scenario modeling, and skills-based deployment capabilities as buyers look for integrated execution within HR workflows. Real-world implementation examples in the report, including the City of Los Angeles running Workday for around 50,000 employees and Johnson & Johnson using AI-driven skills inference, show how scale, integration, and skills frameworks enable adoption. As compliance expectations tighten, vendors that pair planning and skills analytics with built-in logging, transparency, and bias-monitoring features have clearer paths to enterprise procurement in regulated industries such as BFSI and public sector.

Recent Industry Developments

- June 2026: ADP released its Future of Pay 2026 report, emphasizing expanded use of payroll data for workforce planning and retention decisions, including strong stated adoption or implementation intent for predictive analytics among surveyed organizations in India. The findings reinforce payroll as a high-frequency data backbone for workforce analytics use cases and support demand for integrated payroll-to-planning analytics within HCM ecosystems.

- March 2026: ADP launched an AI Agent Hub within ADP Marketplace, enabling organizations to deploy specialized AI agents that integrate with ADP systems to automate reporting and analytics-related workflows. This shifts competitive focus from passive dashboards toward AI-driven orchestration that can reduce manual HR operations while keeping analytics embedded in core platforms.

- November 2025: ADP launched a unified global workforce management suite designed to work across HCM platforms, broadening the addressable base for standardized time, attendance, and workforce data capture. More consistent operational data across regions and systems improves downstream analytics quality and supports enterprise rollouts across hybrid cloud and multi-vendor HR stacks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the workforce analytics market covers software and related services used to collect, organize, and analyze workforce data, so organizations can make decisions on hiring, performance, scheduling, payroll monitoring, and retention.

Scope exclusions: standalone payroll processing, general HRIS recordkeeping without analytics, and pure IT consulting that is not tied to workforce analytics product or service revenue are excluded.

Segmentation Overview

- By Component Type

- Solutions

- Talent Acquisition and Development Optimization

- Payroll and Workforce Monitoring

- Performance and Engagement Analytics

- Turnover and Retention Analytics

- Risk and Compliance Analytics

- Services

- Professional Services

- Managed Services

- Training and Support Services

- Solutions

- By Deployment Type

- Cloud

- On-premises

- By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

- By End-user Industry

- Banking, Financial Services and Insurance (BFSI)

- Manufacturing

- IT and Telecom

- Healthcare and Life Sciences

- Retail and e-Commerce

- Government and Public Sector

- Energy and Utilities

- Transportation and Logistics

- Other Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Netherlands

- Rest of Europe

- Asia_Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public sources that describe workforce digitization and enterprise software spending direction. We used materials such as U.S. Bureau of Labor Statistics employment series, Eurostat labor market indicators, OECD labor and productivity datasets, World Bank macro indicators, and ILOSTAT workforce statistics to anchor the demand backdrop by region.

To convert that backdrop into a tech market view, we reviewed company filings, earnings transcripts, investor presentations, product documentation, and reputable press coverage to extract pricing cues and adoption narratives. We also used paid subscriptions for company financials and intelligence, plus patent databases, to cross-check product focus areas and the timing of new capabilities. These references are illustrative, and there were many other sources consulted for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary checks were used to stress-test adoption and spending assumptions across large enterprises and SMEs, since usage patterns vary based on workforce size and compliance needs. We spoke with solution owners, service partners, and end-user teams across APAC, EMEA, and the Americas to confirm what is counted as workforce analytics, how modules are bundled in practice, and how cloud versus on-premises mixes are shifting.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 15% | APAC: 38% |

| Mid tier: 46% | Functional/Unit leaders: 31% | EMEA: 35% |

| Smaller Players: 15% | Managers: 54% | Americas: 27% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where enterprise software spending patterns, workforce digitization intensity, and HR and operations analytics adoption are used to reconstruct the addressable demand pool by region, then allocated into workforce analytics. After that first pass, we corroborated using selective bottom-up checks, including sampling module price points, typical seat counts for user groups, and service attachment rates, and then adjusted totals where the checks were consistently off.

Key inputs included the pace of cloud migration for HR and analytics stacks, hiring and attrition cycles that affect demand for planning and retention analytics, compliance-driven reporting needs that raise the use of payroll and monitoring analytics, average contract duration and renewal behavior, and the split of professional versus managed support services. Where company disclosures were not detailed enough, gaps were handled by using peer ranges validated in interviews and then applying conservative mid-points until stronger evidence was available.

Forecasting relied on scenario analysis supported by expert views on enterprise budget cycles, AI feature adoption in analytics workflows, and regional IT spending sensitivity. Growth rates were applied at the regional level and rolled up, followed by a final check that the implied revenue per customer stayed realistic over time.

Data Validation & Update Cycle

Outputs were validated through multiple passes comparing modeled totals with independent signals, including enterprise software spend direction, cloud adoption momentum, and hiring and productivity indicators. When a variance looked large, assumptions were reopened, the math was rechecked end to end, and targeted follow-up questions were sent back to interviewees to confirm or correct the driver.

Before sign-off, the full model and narrative are reviewed by another analyst to catch inconsistent definitions, currency timing issues, and segment totals that do not reconcile. The study is refreshed annually, and interim updates are made when material events affect adoption or pricing. Right before delivery, a final pass is completed so the numbers and story reflect the latest available information.

Mordor Intelligence's Workforce Analytics Market Size Compared Against Other Published Estimates

It is normal to see different market sizes for workforce analytics, because publishers do not always count the same revenue streams or apply the same timing for base year and currency conversion. Differences also come from how each model treats services, bundled suites, and whether adjacent HR analytics spending is pulled into the total.

The main gap comes from whether broader HR analytics and experience platforms are included, where Mordor Intelligence counts only workforce analytics solutions and related services tied to talent optimization and payroll monitoring, which keeps totals from absorbing wider HR software revenue that is not analytics-led.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.92 B (2026) | |

| Global Consultancy A | USD 2.35 B (2024) | Uses an earlier base year and a shorter forecast window, and the scope appears to emphasize software revenue more than services, which can pull the total down when service attachment is material. |

| Industry Publisher B | USD 3.12 B (2024) | Reports a higher 2024 level that likely includes a wider set of HR analytics use cases and a different treatment of suite bundling, which can lift the counted revenue beyond workforce analytics-only deployments. |

The spread in the table is mainly explained by what is counted as workforce analytics, and how suites and services are treated in the revenue build. By keeping definitions explicit, checking pricing and adoption with practitioners, and then reconciling the model to practical demand signals, the final number stays traceable to clear assumptions that can be repeated and updated.

Key Questions Answered in the Report

What is the current size of the workforce analytics market?

The workforce analytics market reached USD 2.92 billion in 2026 and is projected to grow to USD 6.04 billion by 2031 at a 15.72% CAGR.

Which deployment model leads the workforce analytics market?

Cloud platforms dominate with 58.62% share in 2025, while hybrid cloud is forecast to post the fastest 16.32% CAGR through 2031, driven by lower capital costs and easier integration.

Which industry segment is growing the fastest?

Healthcare is the quickest-growing vertical, advancing at an 17.66% CAGR as hospitals address severe nurse shortages and rising labor expenses through analytics.

How are SMEs benefiting from workforce analytics?

SMEs leverage SaaS subscriptions, pre-configured dashboards, and low-code interfaces to capture data-driven insights without heavy IT investments, driving a 17.25% CAGR in the SME segment.

Page last updated on: