Talent Management In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

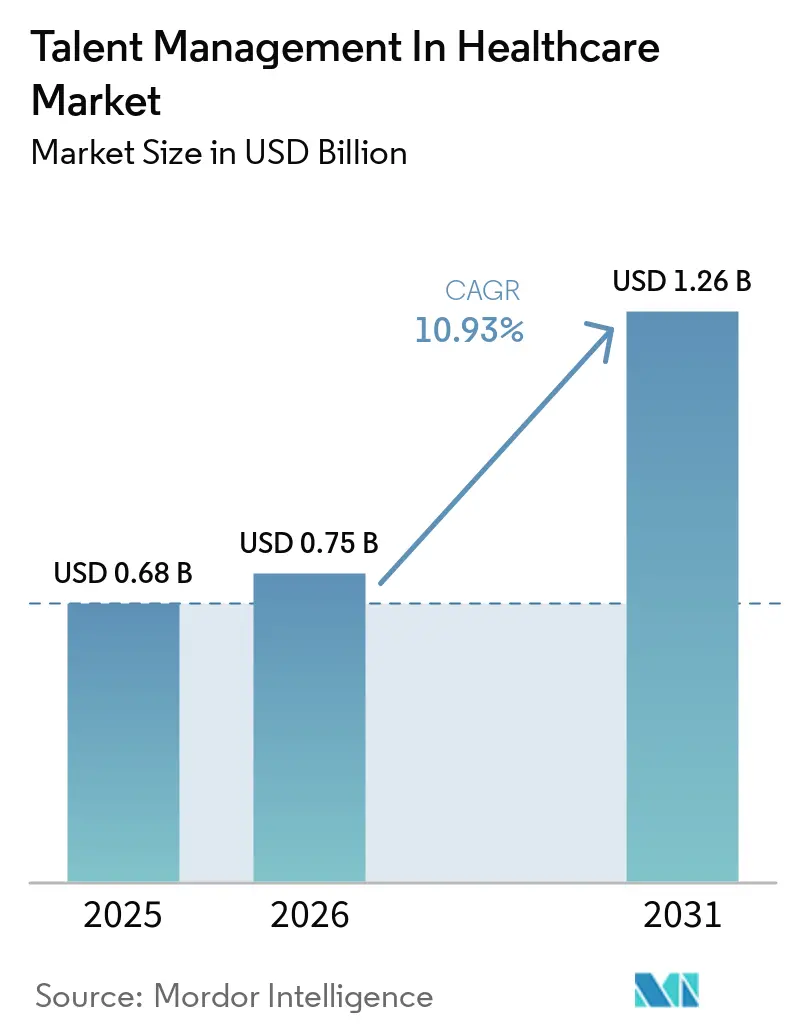

| Market Size (2026) | USD 0.75 Billion |

| Market Size (2031) | USD 1.26 Billion |

| Growth Rate (2026 - 2031) | 10.93% CAGR |

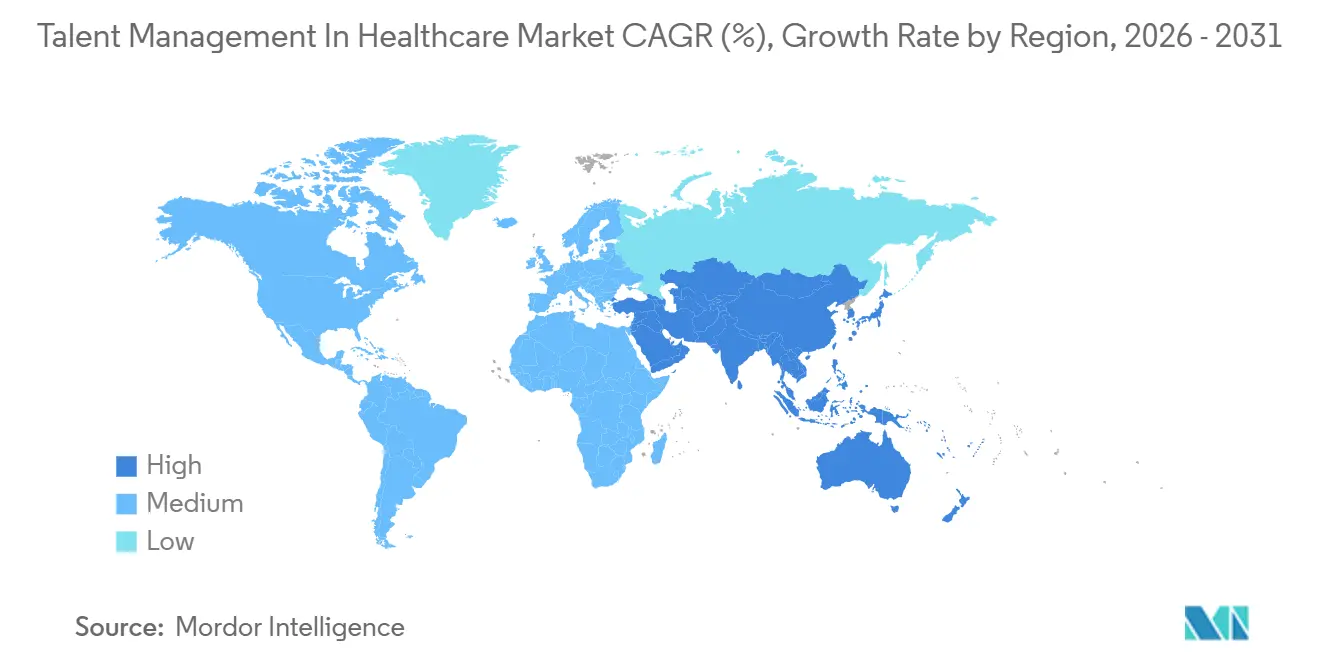

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Talent Management In Healthcare Market Analysis by Mordor Intelligence

The talent management in healthcare market size was valued at USD 0.68 billion in 2025 and estimated to grow from USD 0.75 billion in 2026 to reach USD 1.26 billion by 2031, at a CAGR of 10.93% during the forecast period (2026-2031). The talent management in healthcare market is benefiting from a durable spending case because provider organizations are still dealing with vacancy gaps, long hiring cycles, and heavy turnover costs after the labor disruption that followed the pandemic. Demand is also moving beyond basic hiring support, as health systems now need tools that connect workforce data with clinical operations, compliance tracking, and care quality requirements. Generative AI has started to change competition inside the talent management in healthcare market because leading platforms are adding AI agents across recruiting, performance, succession, and internal mobility modules, which narrows feature gaps for smaller vendors. Consolidation is rising as broader human capital management vendors absorb healthcare-focused point solutions to secure scheduling, credentialing, and workforce planning capabilities. Adoption still slows in smaller and rural provider settings because fragmented IT environments and privacy compliance reviews lengthen deployment cycles, yet those issues do not remove the underlying need for digital workforce systems.

Key Report Takeaways

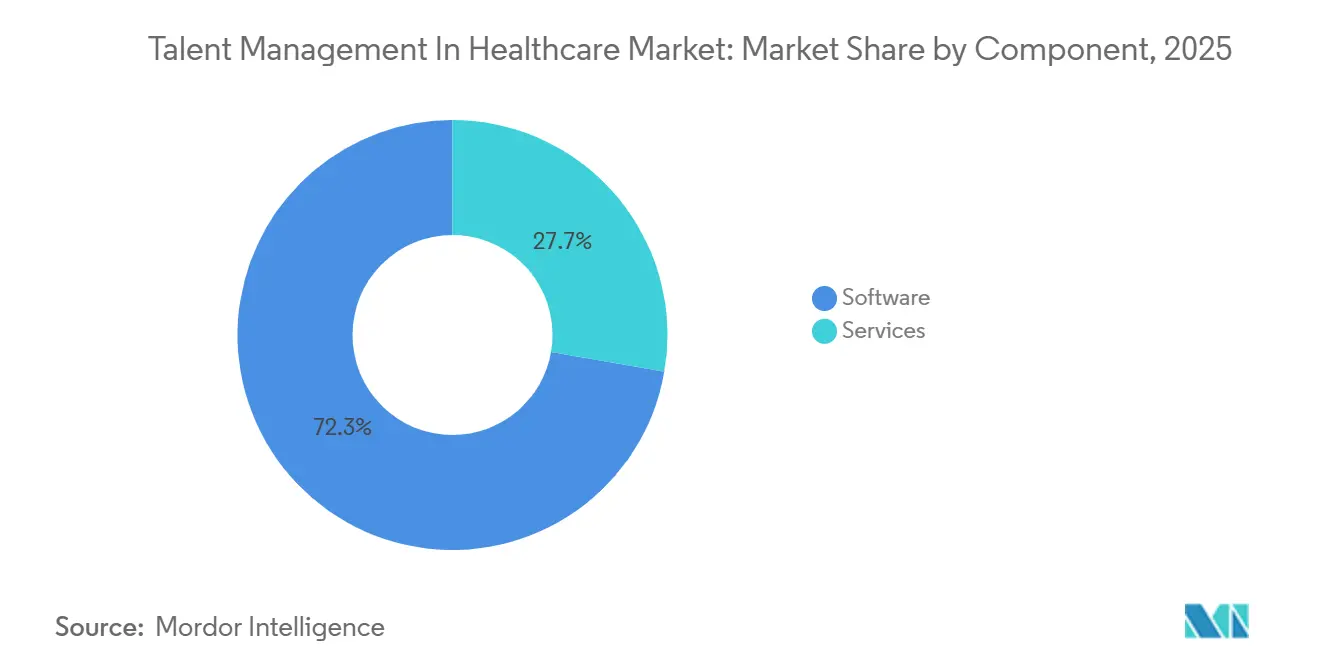

- By component, software led with 72.28% revenue share in 2025 in the talent management in healthcare market, while services recorded the highest projected CAGR at 12.43% through 2031.

- By deployment mode, cloud held 68.31% share in 2025 and also posted the fastest projected CAGR at 13.47% through 2031.

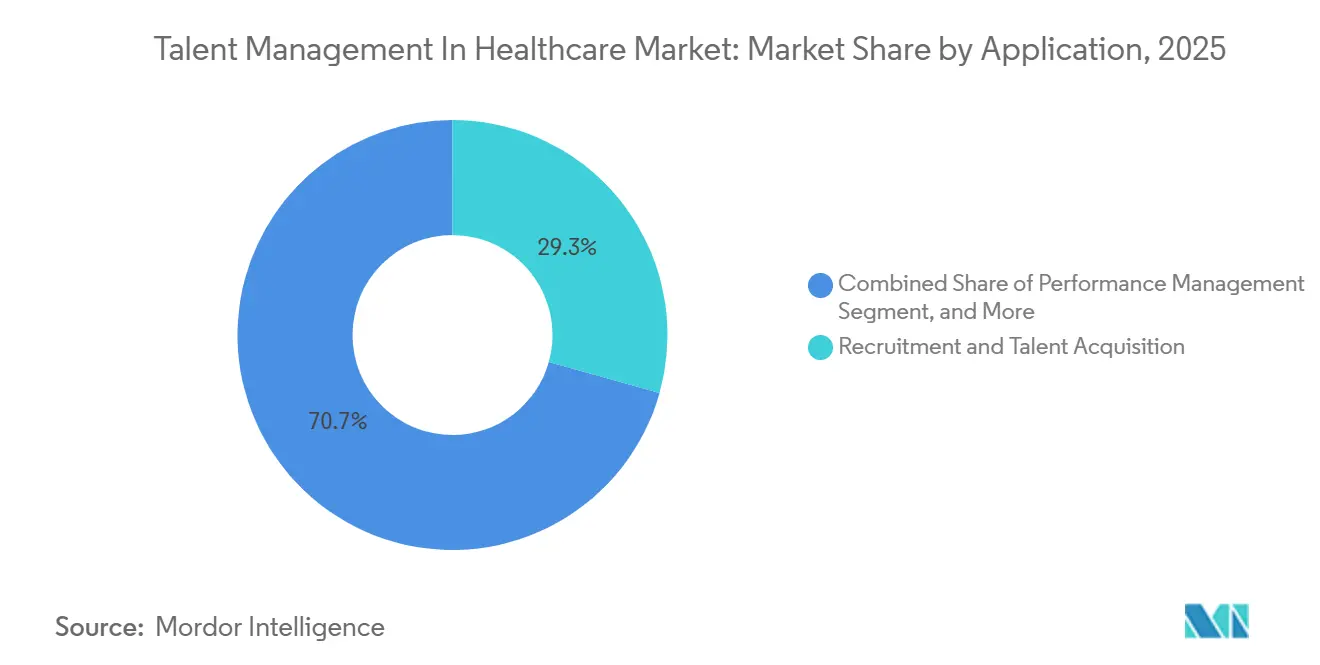

- By application, recruitment and talent acquisition accounted for 29.34% share in 2025, while learning and development is projected to expand at 14.26% CAGR through 2031.

- By end user, hospitals and health systems represented 46.29% share in 2025, while home healthcare agencies are projected to grow at 15.66% CAGR through 2031.

- By geography, North America held 39.42% share in 2025, while the Asia-Pacific is forecast to expand at 13.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Talent Management In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Acute Nursing Staff Shortage Intensifying Competition For Talent | +3.2% | Global, with acute intensity in North America, United Kingdom, and Australia | Short term (≤ 2 years) |

| Clinician Burnout Led Retention Focus Driving Investment in Engagement Platforms | +2.4% | Global, highest in North America and Western Europe | Short term (≤ 2 years) |

| Competency Tracking Mandates For Clinical Staff Requiring Digital Systems | +1.8% | North America and EU, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Shift to Value Based Care Demanding Workforce Upskilling | +1.2% | North America primarily, with early gains in Germany, Netherlands, and Australia | Medium term (2-4 years) |

| AI Driven Candidate Matching Efficiencies Accelerating Recruiter Productivity | +0.8% | Global, fastest adoption in North America and Asia-Pacific core | Short term (≤ 2 years) |

| Telehealth Expansion Creating Remote Workforce Needs and New Role Profiles | +0.6% | North America, with spill-over to India, Southeast Asia, and Southern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acute Nursing Staff Shortage Intensifying Competition For Talent

The ongoing shortage of registered nurses (RNs) is driving significant demand for talent management platforms within the acute care sector. By early 2026, more than 33% of hospitals reported RN vacancy rates exceeding 10%, with the national shortage estimated at 158,600 RNs. On average, hospitals are managing 43 unfilled RN positions, highlighting the critical nature of this issue. This shortage is not evenly distributed, as certain specialties, such as telemetry and step-down units, are experiencing complete staff turnover approximately every 4.5 years. Such high turnover rates make manual human resource tracking both inefficient and costly. As a result, healthcare organizations are increasingly adopting advanced talent management solutions. These platforms, which offer features like pipeline analytics, internal mobility tracking, and predictive attrition modeling, are no longer viewed as optional tools. Instead, they are becoming essential for mitigating financial risks and ensuring operational stability. This trend underscores the growing reliance on technology to address workforce challenges in the healthcare market, further propelling the adoption of talent management systems.

Clinician-burnout-led Retention Focus

Burnout remains a material talent cost even as peak-pandemic rates ease. A 2024 AMA survey of nearly 18,000 physicians across 43 states found that 43.2% still reported at least one burnout symptom, while job satisfaction rose to 76.5%, signaling that improvements in engagement are achievable through organizational intervention. The strategic insight for talent management vendors is that the marginal return on well-being programs is measurable: organizations with stronger shared-governance models, better workload-control features, and active internal-recognition tools showed statistically lower burnout odds in a 2025 multicenter study across 50 Magnet-status US hospitals. Health systems have begun requiring talent platforms to include clinician-specific engagement analytics, monitoring workload intensity, career stagnation signals, and recognition frequency, beyond traditional employee satisfaction surveys. A 2026 Prolink survey of over 400 travel healthcare professionals identified burnout (29%), declining morale (21%), and workforce retention (20%) as the top perceived threats to healthcare in 2026, reinforcing that retention tooling tied to engagement data is a current, not aspirational, purchasing priority.

Competency-tracking Mandates for Clinical Staff

Regulatory accreditation standards are quietly transforming competency management from a departmental tracking exercise into an enterprise software requirement in the talent management in healthcare market. The Joint Commission and its international counterparts mandate documented proof of staff competency across clinical procedures, equipment operation, and infection control, and the NAHQ Healthcare Quality Competency Framework, covering 28 competencies across 8 domains, is now embedded in health systems and higher-education curricula as a recognized standard.[1]National Association for Healthcare Quality, “Healthcare Quality Competency Framework,” NAHQ, nahq.org China's National Health Commission similarly requires public hospitals to maintain digital professional-technical archives under Level 2 of its Smart Management Graded Evaluation Standard, effectively mandating software adoption across a market of approximately 35,000 hospitals. The compliance-driven nature of this demand is a key reason the competency management application sub-segment shows above-average retention relative to economic cycles. Systems that integrate competency documentation with scheduling and payroll, so that only credentialed staff are deployed to qualifying procedures, represent the emerging architecture that accreditation auditors are increasingly expecting to find.

Shift to Value-based Care Demanding Upskilling

Value-based reimbursement is transforming the talent management in healthcare market by redefining the clinical competencies that drive revenue and those that pose financial risks. The CMS 2026 Medicare Physician Fee Schedule Final Rule incentivizes participation in qualifying Alternative Payment Models by offering a higher conversion factor compared to non-participants. This creates a strong financial imperative for health systems to ensure their workforce is equipped to document, monitor, and demonstrate value-based performance effectively. As a result, talent management in healthcare is experiencing significant growth, with learning and development modules within talent platforms being repurposed to comply with payer-mandated care protocols rather than focusing solely on continuing-education credits. This shift is driving the adoption of advanced talent management solutions, enabling healthcare organizations to align workforce capabilities with the requirements of value-based care. Consequently, learning and development has emerged as the fastest-growing application segment, projected to grow significantly during the forecast period.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented IT Infrastructure in Mid Tier Providers Slowing System Integration | -1.8% | Global, most severe in rural North America, South Asia, and Southeast Asia | Medium term (2-4 years) |

| Data Privacy Concerns Around Staff Credential Records and HR Data | -1.2% | North America and EU, spill-over to Asia-Pacific as GDPR equivalent regulations expand | Medium term (2-4 years) |

| Limited HR Tech Budgets in Rural Healthcare Settings | -0.9% | Rural North America, Sub-Saharan Africa, South Asia | Long term (≥ 4 years) |

| Union Resistance to Algorithmic Performance Scoring | -0.6% | Western Europe, Canada, and the organized labor-dense United States urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented IT Infrastructure In Mid Tier Providers

A 2026 CHIME Leadership Pulse Survey of healthcare technology leaders found that 76% cited tool sprawl and fragmentation as making operations harder, with some organizations managing over 100 enterprise tools, while 85% identified financial limitations as the primary barrier to technology modernization. The most consequential challenge for talent management vendors is integration complexity: 74% of survey respondents require new platforms to offer seamless connectivity with existing EHR systems, a threshold many mid-tier talent management solutions cannot clear without substantial professional services investment. For providers below the 200-bed threshold, the problem compounds, as these organizations typically lack dedicated interface engineering teams to manage API integrations across clinical scheduling, credentialing, and payroll systems. Independent critical access hospitals demonstrated substantially lower EHR interoperability than system-affiliated peers in federal monitoring data, and the same structural gap applies to HR technology. Vendors that fail to offer pre-built, certified integrations with dominant EHR platforms risk a protracted sales cycle in the mid-market, which represents a significant volume of potential accounts.

Data Privacy Concerns Around Staff Credential Records And HR Data

Healthcare talent management platforms increasingly hold a dual-risk data profile: clinical credential records that trigger state licensing board obligations in the talent management in healthcare market and, when platforms include benefits administration, plan-sponsored health data that activates HIPAA's privacy, security, and breach notification rules. The U.S. Department of Health and Human Services enforces civil penalties on a tiered scale for breaches of unsecured protected health information, with penalties applicable to covered entities and their business associates, a designation that talent technology vendors accept the moment they execute a Business Associate Agreement. The April 2024 HIPAA Privacy Rule update further expanded protections for reproductive health information, adding a new layer of compliance complexity for HR platforms that capture medical accommodation data.[2]U.S. Department of Health and Human Services, “HIPAA Privacy, Security, and Breach Notification Guidance,” HHS, hhs.gov In Europe, GDPR Article 9 classifies health data as a special category subject to explicit consent requirements and maximum fines of EUR 20 million (approximately USD 22 million) or 4% of global annual turnover, a compliance burden that German healthcare HR vendors like Personizer must explicitly address in their architecture to serve the market. These regulatory compliance obligations add implementation timeline and legal review costs that slow purchasing decisions, particularly among organizations without dedicated compliance counsel.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Shifting As Services Scale

Across the component segmentation, software held a 72.28% revenue share of the talent management in healthcare market in 2025, reflecting the platform-centric buying pattern of large health systems that invest in multi-module enterprise suites and capitalize the initial license outlay. The services segment is forecast to grow at 12.43% CAGR from 2026 to 2031, outpacing the overall market, as providers of all sizes recognize that configuration, workflow redesign, and change management often determine whether a talent platform delivers measurable outcomes. Professional services, which encompass implementation consulting and customization, contribute the largest share within the services segment, while support and maintenance services are gaining traction as organizations move away from time-limited deployment contracts toward continuous platform optimization. The strategic implication is that vendors who have historically competed on software features are now building out or acquiring services capabilities to defend annual contract value and reduce churn.

A niche dynamic amplifying services revenue growth is the increasing demand for healthcare-specific configuration expertise. General-purpose HCM implementations require extensive customization to handle nurse licensure tracking, multistate compact licensure and JCAHO-required competency documentation. Vendors like HealthStream have responded by building AI-assisted configuration tooling and pre-built healthcare content libraries, such as the HealthStream Learning Experience platform launched in January 2025, that accelerate time-to-value and reduce implementation services cost for clients, while still generating recurring revenue through content subscriptions. The competitive implication is that the line between software and services revenue will continue to blur as AI automates routine implementation tasks and vendors bundle managed-service tiers into subscription pricing.

By Deployment Mode: Cloud Consolidates Lead, Hybrid Remains Relevant

Cloud deployment held 68.31% share of the talent management in healthcare market in 2025 and is simultaneously the fastest-growing mode at 13.47% CAGR through 2031, an unusual combination indicating that this segment is both dominant and still in active expansion, driven by migration from on-premise and hybrid environments. The cloud-first preference among health systems is reinforced by accelerating mobile workforce dynamics: 5.3% of all US registered nurses worked as travel nurses in 2024, and approximately 20% changed work settings in the same year, creating distributed credential and scheduling complexity that is difficult to manage on locally hosted infrastructure. IHH Healthcare's May 2026 deployment of Oracle Fusion Cloud HCM across 89 hospitals in 10 countries illustrates how major multi-national healthcare groups are leveraging cloud platforms to achieve workforce visibility at scale that on-premise systems structurally cannot deliver.

On-premise deployment, while declining in share, retains relevance for government-owned hospital systems in countries with strict data sovereignty requirements, particularly in China, India, and the Middle East, where national health data regulations can restrict cross-border cloud transfers. Hybrid deployment is emerging as an intermediate architecture that allows organizations to maintain sensitive staff data on-premises while leveraging cloud-based analytics and AI capabilities, a configuration particularly valued in systems that have made substantial EHR infrastructure investments and cannot absorb the capital disruption of a full platform migration. Regulatory compliance frameworks in Germany, including the Federal Labor Court's 2022 mandatory time-tracking ruling reaffirmed by administrative courts in 2024, are creating compliance-driven demand for digitized HR tools regardless of deployment model, keeping hybrid viable in European enterprise accounts.

By Application: Recruitment Leads, Learning And Development Accelerates

Recruitment and talent acquisition held the largest application share at 29.34% in 2025, reflecting acute near-term hiring pressure as health systems compete for a contracting clinical labor pool. The average time to fill an experienced registered nurse reached 78 days in 2026, with some specialties like telemetry requiring as long as 87 days, driving investment in AI-powered sourcing and automated screening tools that can compress the funnel. Vendors are deploying large language model-powered candidate matching against verified licensure databases: Vivian Health's October 2025 launch of its AI Assistant for healthcare recruiters achieved a 4-times increase in candidate responsiveness and a 10-15% improvement in application-to-placement conversion rates in beta deployments, illustrating that AI-native ATS investment is generating measurable operational return, not merely automation for its own sake.

Learning and development is the fastest-growing application at 14.26% CAGR through 2031, driven by the value-based care upskilling imperative described above and by the increasing sophistication of platform AI recommendations. GE Healthcare's deployment of Cornerstone's Learning Experience Platform processed 122 million training assignments and 138 million completions in 2024, with a notable mix shift toward development-oriented learning reducing the compliance-only proportion from 92% to 86%. Performance management, workforce planning, succession planning, and compensation management represent important mid-tier applications with steady demand, while employee engagement and career development tools are gaining share as organizations recognize that internal career pathing reduces external attrition costs more economically than repeated external recruitment. Other talent management applications, including onboarding automation and position management, complement the core suite and are increasingly bundled rather than purchased as standalone modules in the talent management in healthcare market.

By End User: Hospitals Anchor Revenue, Home Health Scales Fastest

Hospitals and health systems accounted for 46.29% of the talent management in healthcare market revenue in 2025, driven by their scale, regulatory complexity, and budgetary capacity. Large integrated delivery networks operate clinical workforces across hundreds of departments, dozens of facilities, and multiple licensure jurisdictions, generating scheduling, credentialing, and performance data complexities that only enterprise-grade talent platforms can manage. Hospital-focused vendors like UKG, which serves nearly 90% of the largest US health systems across 3,500 hospitals, have embedded healthcare-specific scheduling extensions that forecast staffing needs against patient acuity, a capability that directly links talent management investment to patient safety outcomes.[3]UKG Team, “Healthcare Workforce Management and Rapid Hire Case Material,” UKG, ukg.com Ambulatory and specialty clinics represent the second-largest end-user group, benefiting from the growing deployment of cloud-based solutions scaled for smaller organizations.

Home healthcare agencies are the fastest-growing end-user segment, with a 15.66% CAGR through 2031, a trajectory driven by two converging forces. First, CMS payment policy expansions under the 2026 Physician Fee Schedule permanently broadened virtual supervision and telehealth-delivered care, creating workforce configurations that require digital credential tracking for geographically dispersed workers. Second, the structural migration of care delivery from inpatient to home settings is intensifying: home health aides represented 602,061 workers in HRSA's national workforce dataset, with 87.7% female and a significant cohort in mid-career age brackets that exhibit retention drivers different from those of hospital-based staff. Long-term care and rehab centers and other provider types are adopting talent platforms at a measured pace, constrained by thin operating margins but increasingly motivated by state-level staffing minimum regulations that require documented workforce planning data.

Geography Analysis

North America dominated the talent management in healthcare market with a 39.42% share in 2025, driven by the United States' unmatched density of acute-care facilities, a mature SaaS procurement infrastructure, and sustained regulatory pressure from CMS value-based care mandates and Joint Commission accreditation standards. The United States alone carries an estimated 158,600 RN shortage as of 2026, with hospital RN turnover costs averaging USD 60,090 per bedside nurse, creating a powerful financial incentive for technology investment. Canada and Mexico represent smaller but growing sub-markets: Canada is experiencing similar burnout-linked attrition dynamics, while Mexico's expanding private hospital sector is beginning to invest in cloud-based HR platforms. The CMS Rural Health Transformation Program, a USD 50 billion initiative launched in January 2026, is channeling capital into workforce technology for underserved US communities, with states like Colorado allocating USD 255.5 million specifically for telehealth and technology integration. This federal program is expected to pull previously technology-resistant rural providers into the addressable market over the forecast period.

Europe accounted for a meaningful share of market revenue in 2025, led by Germany and the United Kingdom, where mandatory digital time-tracking regulations and national health service staffing crises are converting previously paper-based HR processes into platform-enabled ones. Germany's Federal Labor Court ruling on mandatory working-hours tracking, reaffirmed by Hamburg administrative courts in August 2024, created a compliance-driven stimulus for digitized workforce management, particularly among the approximately 430,000 medical assistants, nearly 50% of whom work part-time, generating scheduling complexity that manual systems cannot accurately capture. The United Kingdom's NHS remains a major demand generator, with NHS Management reporting a 10-day reduction in time-to-hire and USD 2.2 million in new annual revenue after deploying UKG Rapid Hire. France, Italy, and the rest of Europe are at earlier stages of enterprise HR platform adoption in healthcare, offering a mid-term expansion opportunity for vendors with multilingual product configurations.

Asia-Pacific is the fastest-growing region at 13.89% CAGR through 2031, reflecting healthcare infrastructure investment, hospital digitization mandates, and a structurally under-served talent management software market. India's government-run AIIMS network reported approximately 2,316 faculty and 15,525 non-faculty vacancies as of March 2026, representing roughly 36% and 26% of sanctioned posts respectively, and the Union Health Minister linked AI-enabled diagnostics with faster faculty recruitment as co-equal priorities in February 2026, signaling that workforce technology is entering the national policy conversation. China's National Health Commission Smart Management Graded Evaluation Standard mandates digital HR modules from Level 2 certification onwards, affecting public hospitals across a system of approximately 35,000 registered facilities and driving adoption of domestic vendors such as Yanfang Software and Medrun. A January 2026 survey of healthcare leaders at the Hospital Management Asia 2025 conference identified workforce and talent management as the most prevalent systemic challenge facing the region, ahead of both financial constraints and digital transformation.[4]Hospital Management Asia Team, “Hospital Management Asia 2025 Survey Findings,” Hospital Management Asia, hospitalmanagementasia.com The Middle East and Africa, led by Saudi Arabia and the UAE, are investing in healthcare workforce technology as part of broader Vision 2030-aligned digital transformation programs, while South America, principally Brazil, shows early-stage demand concentrated in large private hospital groups.

Competitive Landscape

The talent management in healthcare market is moderately fragmented at the enterprise end and highly fragmented in the mid-market and point-solution tier. The top cohort, Oracle Corporation, SAP SE (SuccessFactors), Workday, Inc., and UKG Inc., commands a significant share through breadth of functionality and deep integration with financial and EHR systems, but no single vendor holds a dominant position across all segments and geographies. Oracle's November 2025 recognition as an Overall Leader and the only provider named a Leader in all seven categories of the ISG Buyers Guide for Workforce Management Healthcare reflects the advantage that clinical-administrative integration, enabled through its acquisition of Cerner, can confer, but also the high implementation complexity that keeps displacement cycles long. Healthcare-vertical specialists like HealthStream, HealthcareSource, and OnShift occupy defensible niches through deep content libraries, accreditation-ready workflows, and post-acute-specific scheduling logic that general HCM platforms struggle to replicate cost-effectively.

The most consequential strategic pattern in 2025 and 2026 is acquisition-led consolidation at the workforce management and talent acquisition layers. Viventium's acquisition of Apploi in February 2026 created a healthcare-exclusive HCM platform serving over 9,000 organizations by unifying recruiting, credentialing, onboarding, and payroll into a single post-acute-native system, displacing fragmented multi-vendor stacks that had previously served the long-term care sector. symplr's July 2025 acquisition of AMN Healthcare's Smart Square scheduling software added a Best in KLAS-rated workforce management module to its enterprise operations platform, illustrating that clinical scheduling is becoming a critical integration layer vendors must own rather than partner around. The white-space opportunity lies in mid-market providers, community hospitals, ambulatory networks, and home health agencies, where purpose-built, API-first platforms with pre-configured Joint Commission and HIPAA Security Rule-compliant workflows can displace legacy systems at a lower total cost of ownership than enterprise suite migrations. AI-native disruptors are competing on recruiter productivity metrics: QGenda's May 2026 certified integration with Workday HCM enables healthcare organizations to align scheduling, time tracking, and payroll data within a unified ecosystem, representing the interoperability architecture that buyers increasingly demand as a baseline.[5]QGenda Team, “Certified Workday HCM Integration Announcement,” QGenda, qgenda.com

Talent Management In Healthcare Industry Leaders

Oracle Corporation

SAP SE

IBM Corporation

Cornerstone OnDemand, Inc.

Workday, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: QGenda announced a certified integration with Workday Human Capital Management, available on the Workday Marketplace, enabling healthcare organizations to align clinical scheduling, HR data, time tracking, and payroll within a unified ecosystem, directly reducing the manual reconciliation burden that affects an estimated most of fragmented health system IT environments.

- May 2026: IHH Healthcare, operating 89 hospitals across 10 countries, initiated deployment of Oracle Fusion Cloud HCM to consolidate its enterprise HR and workforce management systems, targeting improved workforce planning visibility and AI-driven operational insights across its international network.

- May 2026: Cross Country Healthcare announced a 36-month exclusive partnership to integrate Strategic Systems International's Optimé workforce strategy solution into its Intellify cloud platform, adding advanced forecasting and analytics to match workforce supply with patient demand and reduce labor cost per unit of service. The deal positions Cross Country as a technology-enabled workforce intelligence partner rather than a traditional staffing vendor.

- February 2026: Viventium completed its acquisition of Apploi, creating a nationally scaled, healthcare-exclusive HCM platform serving over 9,000 healthcare organizations and nearly 800,000 employees, the combined platform integrates recruiting, credentialing, onboarding, payroll, and scheduling specifically for post-acute and long-term care providers.

- January 2026: IntelyCare acquired CareRev to create a unified acute and post-acute clinical labor platform, combining CareRev's 35,000-plus acute-care professionals with IntelyCare's post-acute network, enabling management of permanent, contingent, and on-demand clinical staff from a single dashboard for health systems covering over 25 million covered lives.

Global Talent Management In Healthcare Market Report Scope

Talent management in healthcare refers to the strategic approach of attracting, recruiting, developing, and retaining skilled medical and administrative professionals. This process enhances workforce stability and ensures high-quality patient care by maximizing employee potential, minimizing burnout, and encouraging continuous professional development.

The Talent Management in Healthcare Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premise, and Hybrid), Application (Performance Management, Learning and Development, Recruitment, and Other Talent Management Applications), End User Industry (Hospitals, Clinics, Long-Term Care, Home Healthcare, and Other End User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | |

| Services | Professional Services |

| Support and Maintenance Services |

| Cloud |

| On-premise |

| Hybrid |

| Performance Management |

| Learning and Development |

| Succession Planning |

| Compensation Management |

| Recruitment and Talent Acquisition |

| Workforce Planning |

| Employee Engagement and Career Development |

| Other Talent Management Applications |

| Hospitals and Health Systems |

| Ambulatory and Specialty Clinics |

| Long-Term Care and Rehab Centers |

| Home Healthcare Agencies |

| Other End User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Software | ||

| Services | Professional Services | ||

| Support and Maintenance Services | |||

| By Deployment Mode | Cloud | ||

| On-premise | |||

| Hybrid | |||

| By Application | Performance Management | ||

| Learning and Development | |||

| Succession Planning | |||

| Compensation Management | |||

| Recruitment and Talent Acquisition | |||

| Workforce Planning | |||

| Employee Engagement and Career Development | |||

| Other Talent Management Applications | |||

| By End User Industry | Hospitals and Health Systems | ||

| Ambulatory and Specialty Clinics | |||

| Long-Term Care and Rehab Centers | |||

| Home Healthcare Agencies | |||

| Other End User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and forecast for talent management in healthcare?

The talent management in healthcare market was valued at USD 0.68 billion in 2025, is estimated at USD 0.75 billion in 2026, and is projected to reach USD 1.26 billion by 2031 at a 10.93% CAGR.

What is driving adoption of workforce platforms in healthcare organizations?

Persistent RN shortages, burnout-related retention pressure, competency tracking requirements, and value-based reimbursement are pushing providers to invest in digital hiring, learning, and workforce planning systems.

Which component leads spending in this space?

Software led with 72.28% of revenue in 2025 because large health systems still prefer broad enterprise platforms that combine multiple talent workflows in one environment.

Which application is growing the fastest through 2031?

Learning and development is the fastest-growing application, with a projected 14.26% CAGR, because providers are shifting from vacancy response toward structured upskilling and compliance-based training.

Which end users are creating the strongest growth opportunity?

Hospitals and health systems remain the largest buyers, but home healthcare agencies are growing the fastest at 15.66% CAGR as care shifts into community and virtual settings.

Which region offers the best near-term expansion potential?

North America remains the largest regional market, while Asia-Pacific offers the strongest growth outlook with a projected 13.89% CAGR through 2031.

Page last updated on: