Talent Intelligence Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

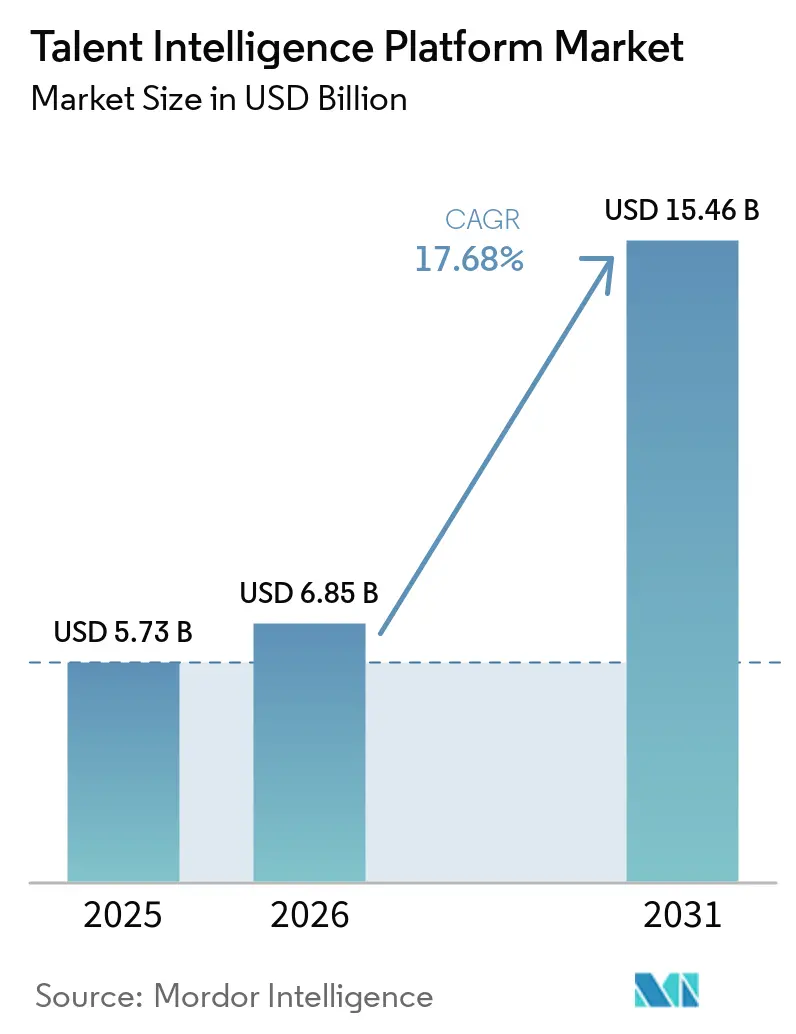

| Market Size (2026) | USD 6.85 Billion |

| Market Size (2031) | USD 15.46 Billion |

| Growth Rate (2026 - 2031) | 17.68% CAGR |

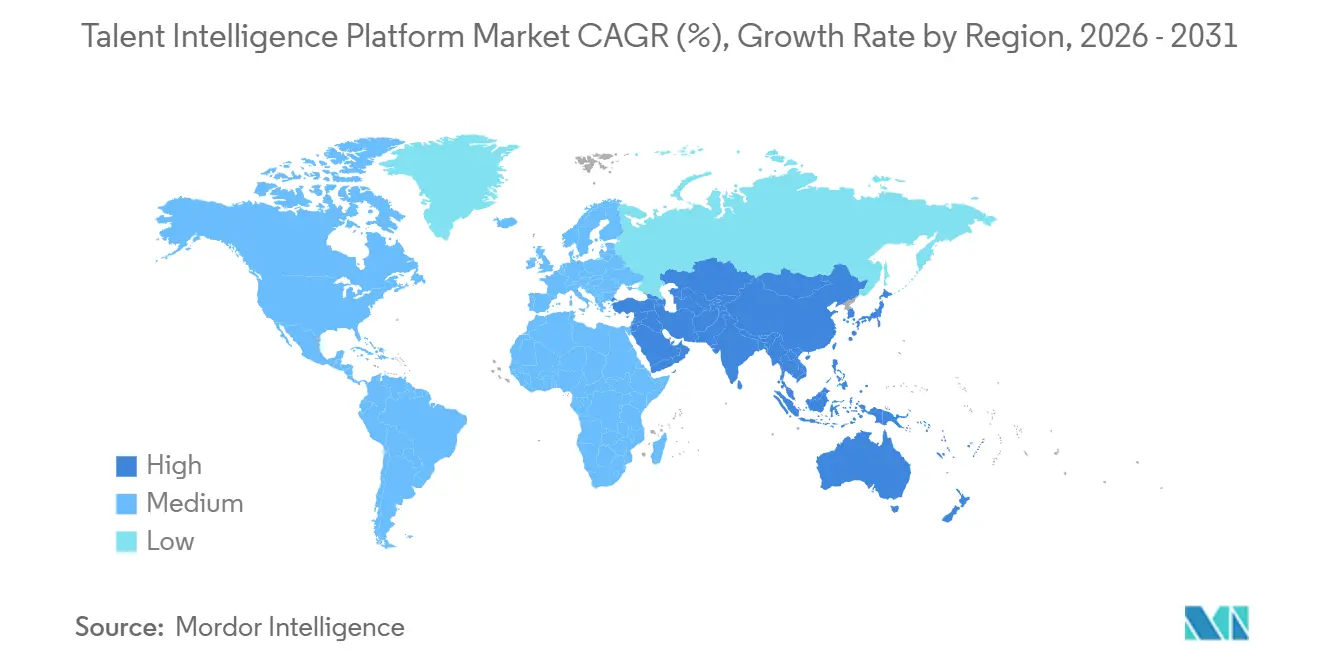

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

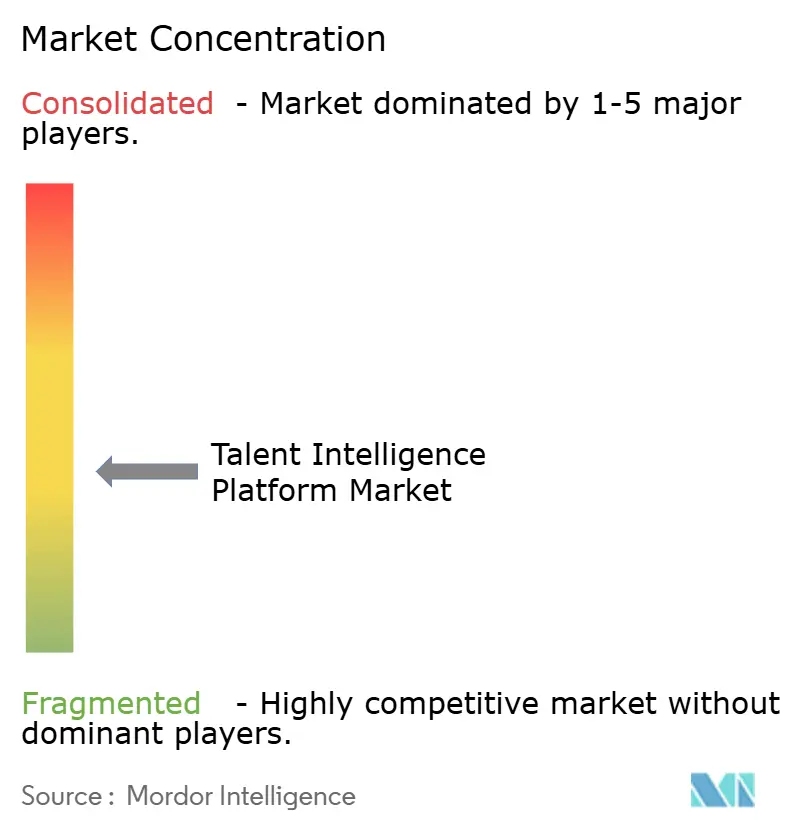

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Talent Intelligence Platform Market Analysis by Mordor Intelligence

The talent intelligence platform market size was valued at USD 5.73 billion in 2025 and estimated to grow from USD 6.85 billion in 2026 to reach USD 15.46 billion by 2031, at a CAGR of 17.68% during the forecast period (2026-2031). Growth in the talent intelligence platform market reflects a broader change in how employers manage workforce risk, because skills shortages, AI-led role changes, and weak static HR systems have pushed workforce intelligence into core business planning. AI use in HR workflows has moved from limited pilots to wider adoption, and workforce analytics has become one of the most common use cases, which supports stronger spending on connected talent systems. The talent intelligence platform market is also benefiting from demand for platforms that combine talent acquisition, internal mobility, skills mapping, and workforce planning in one intelligence layer rather than in separate tools. Competitive pressure is increasing as large enterprise software vendors expand AI-native capabilities while specialist providers compete on skills graph quality and automation depth. The market also faces a stricter operating environment, because fragmented regulation and faster skill obsolescence reward vendors that can refresh taxonomies quickly, maintain auditable models, and support enterprise governance at scale.

Key Report Takeaways

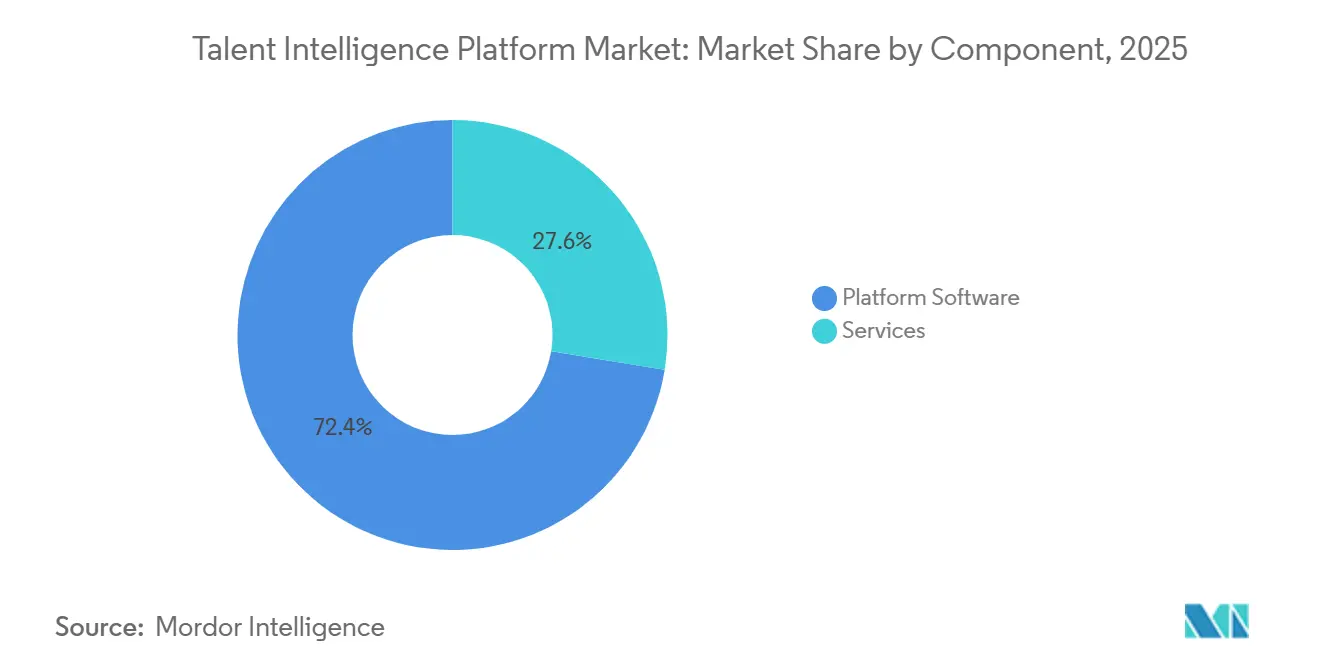

- By component, platform software held 72.41% of the talent intelligence platform market share in 2025, while services are projected to expand at an 18.68% CAGR through 2031.

- By deployment model, cloud-based implementations accounted for 68.92% of the talent intelligence platform market size in 2025 and are expected to advance at a 22.73% CAGR through 2031.

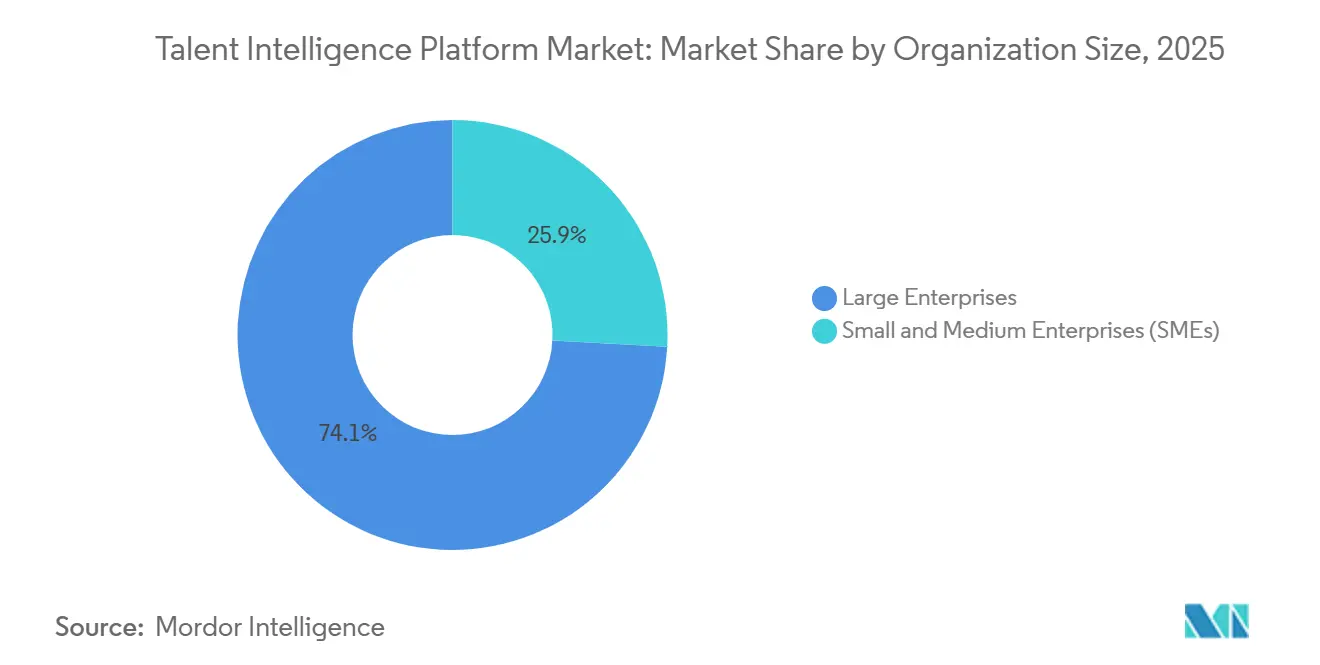

- By organization size, large enterprises held 74.13% share in 2025, while SMEs are projected to grow at a 21.53% CAGR through 2031.

- By end-user industry, IT and telecommunications led with 24.82% share in 2025, while healthcare and life sciences are projected to expand at a 24.12% CAGR through 2031.

- By geography, North America held 41.61% share in 2025, while the Asia-Pacific is expected to record a 22.41% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Talent Intelligence Platform Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Shift to Skills-Based Workforce Planning | +4.2% | Global, with early-mover concentration in North America and Northern Europe | Medium term (2-4 years) |

| Expansion of Internal Talent Marketplace Adoption | +3.5% | North America and Western Europe, accelerating in Asia-Pacific enterprise segment | Medium term (2-4 years) |

| Enterprise Adoption of Generative AI and Agentic HR | +3.8% | Global, EMEA AI adoption leads North America | Short term (≤ 2 years) |

| Need For Unified Internal and External Talent Data | +2.4% | Global, most acute in large-enterprise IT and BFSI sectors | Medium term (2-4 years) |

| AI Auditability and Explainability Requirements | +1.1% | EU and North America primary, with spillover to MEA and Asia-Pacific regulated sectors | Long term (≥ 4 years) |

| Task-Level Work Redesign For Human-AI Collaboration | +1.3% | Global, with early deployment in professional services and manufacturing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift To Skills-Based Workforce Planning

The talent intelligence platform market is gaining momentum because employers are moving away from job-title planning and toward skills-based workforce design. Betterworks found in April 2026 that 73% of HR leaders said skills data gaps had contributed directly to business failures in the prior 12 months, including missed internal placements and delayed strategic programs, and some mid-market firms linked those gaps to avoidable annual costs of USD 2 million or more. Betterworks also showed that only 16% of organizations had predictive, AI-driven workforce planning in place, which means most buyers in the talent intelligence platform market are still operating from reactive or early-stage models. This gap matters because firms can no longer treat skills infrastructure as a long-term HR project when workforce planning now affects execution speed across the business. The talent intelligence platform market, therefore, benefits when vendors combine skills ontologies, governance tools, and planning workflows in the same product rather than selling analytics as an isolated feature.

Expansion of Internal Talent Marketplace Adoption

The talent intelligence platform market is also supported by wider use of internal talent marketplaces, especially as companies try to redeploy workers before opening new external searches. Enterprise recruiting capacity is shifting toward internal mobility in 2026, and that increases demand for platforms that can match employees to projects, gigs, and lateral roles in near real time. The harder issue is not software installation but manager behavior, because team leaders are still often rewarded for holding talent rather than releasing it across the business. Adecco Group found that only 50% of companies had the internal mobility tools needed for workforce agility, and fewer than 45% of leaders believed their teams understood future skill requirements. That leaves room for the talent intelligence platform market to grow through products that include adoption analytics, manager prompts, and workflow rules that reduce resistance after deployment. Vendors that link marketplace usage to redeployment speed and talent retention are more likely to show durable value once the system goes live.

Enterprise Adoption of Generative AI And Agentic HR

The talent intelligence platform market has moved into a stronger adoption phase because HR teams are using AI for more than passive reporting. SHRM reported that AI adoption in HR rose from 26% of organizations in 2024 to 43% in 2025, with the strongest use cases in workforce planning, recruiting, and learning and development. This shift matters because agentic systems are starting to execute tasks instead of only producing recommendations, which changes what enterprises expect from the talent intelligence platform market. EMEA has already reached a higher AI adoption rate in HR than North America, which suggests that compliance pressure is not slowing adoption as much as forcing it into more structured deployments. As the talent intelligence platform market expands, vendors with explainable models, audit logs, and human override workflows are better placed to capture enterprise budgets tied to agentic HR programs.

Need For Unified Internal And External Talent Data

The talent intelligence platform market depends heavily on data quality, and many enterprises still operate with incomplete or stale views of workforce capability. Betterworks found in 2026 that 90% of HR leaders believed their organizations held complete skills data, yet 3 out of 4 estimated that fewer than 75% of actual employee skills were captured in those systems, and only 20.9% updated skills data in real time. That mismatch creates direct costs through unnecessary external hiring, slower restructuring, and weak succession choices, which makes unified data a core value driver for the talent intelligence platform market. TalentNeuron stated that its platform processes more than 3 billion professional profiles and 40 terabytes of normalized workforce data, which shows the scale of external data infrastructure now needed to complement internal HR records. The talent intelligence platform market is therefore favoring vendors that provide pre-built data pipelines, external labor benchmarks, and real-time skills inference instead of relying only on employee self-declared profiles. Those capabilities help buyers close the gap between what they think they know about workforce skills and what their systems can actually verify.

Restraints Impact Analysis*

| Integration Debt Across ATS, HRIS, LMS, And CRM Stacks | -2.5% | Global, most acute in large enterprises with legacy multi-vendor HR stacks | Short term (≤ 2 years) |

| Algorithmic Bias, Privacy, And Employment Law Exposure | -1.8% | EU and North America primary, Asia-Pacific core with spillover to MEA | Medium term (2-4 years) |

| Skills Taxonomy Drift And Weak Data Governance | -1.3% | Global, most acute in fast-moving technical sectors and Asia-Pacific markets | Medium term (2-4 years) |

| Low Utilization After Go-Live And Change-Management Failure | -1.1% | Global, concentrated in organizations with hierarchical management structures | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Integration Debt Across ATS, HRIS, LMS, And CRM Stacks

The main short-term drag on the talent intelligence platform market is the complexity built into legacy HR technology stacks. Truto reported that 88% of talent acquisition leaders used multiple point solutions, and 40% managed 4 or more platforms each day, which leaves core workforce data scattered across disconnected systems. That fragmentation limits how quickly a talent intelligence platform market deployment can produce reliable matching, planning, and mobility outputs. Truto also reported that building native integrations to even 5 large HRIS platforms can consume 70-80% more engineering time than a unified API approach, while vendor API changes keep adding maintenance work after launch. This means buyers often underestimate the full cost of deployment when they compare license fees without accounting for integration work and ongoing data mapping. In the talent intelligence platform market, vendors with certified connectors, stronger service-level commitments, and stable integration frameworks can reduce this hidden tax and shorten time to value.

Algorithmic Bias, Privacy, and Employment Law Exposure

The talent intelligence platform market also faces a growing compliance burden as AI-assisted talent decisions move under tighter legal scrutiny. The EU AI Act classifies many recruitment, promotion, task allocation, and performance monitoring systems as high-risk, and full Chapter III obligations were scheduled to apply in August 2026.[1]European Union, “Regulation (EU) 2024/1689,” Official Journal of the European Union, eur-lex.europa.eu Article 4 AI literacy requirements were already enforceable from February 2, 2025, which means deployers must ensure that staff using high-risk employment AI systems are properly trained before rollout. OECD reporting on AI in work has repeatedly highlighted the risk of bias and unequal outcomes in AI-enabled employment decisions, which raises exposure under anti-discrimination rules and hiring laws across major jurisdictions.[2]OECD, “AI in Work,” OECD, oecd.org The talent intelligence platform market is therefore under pressure to show bias testing, demographic performance tracking, human oversight, and override documentation as standard product features. Vendors that cannot provide those controls may still win pilots, but they face a harder path in enterprise procurement and regulated sectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform Software Leads The Talent Intelligence Platform Market While Services Deepen Adoption

Platform software accounted for 72.41% of the talent intelligence platform market size in 2025, which kept it as the largest revenue component in the talent intelligence platform market. Services are projected to expand at an 18.68% CAGR from 2026 to 2031, which makes them the faster-growing component even though software remains the larger base. This split shows that software contracts still anchor spending, but the real challenge in the talent intelligence platform market often begins after the license is signed. Adecco Group found that only 33% of companies invested adequately in data insights to understand workforce skills, which supports ongoing demand for implementation, integration, and analytics support. As a result, buyers increasingly view services as essential to reaching productive use rather than as optional post-sale add-ons.

That dynamic is pushing vendors to package consulting, integration management, and managed analytics more tightly around the core platform. Outcome-based services pricing is gaining relevance because clients want vendors to share accountability for hiring speed, internal mobility, and workforce planning accuracy. SAP's 1H 2026 SuccessFactors release added stronger skills governance, centralized skills management, and Joule AI support across hiring and career workflows, which shows how vendors are trying to embed services-grade governance directly into software.[3]SAP News Center, “SAP SuccessFactors 1H 2026 Release,” SAP News Center, news.sap.com In the talent intelligence platform industry, the providers that combine scalable software with disciplined onboarding and change support are more likely to protect renewals and expand account value. The same pattern suggests that services can remain strategically important even if software features become easier to copy.

By Deployment Model: Cloud Strength In The Talent Intelligence Platform Market Still Leaves Room For Hybrid

Cloud-based deployment captured 68.92% of the talent intelligence platform market size in 2025 and is projected to expand at a 22.73% CAGR through 2031, which reinforces its lead in the talent intelligence platform market. Cloud demand remains strong because multi-tenant architecture lowers delivery costs and allows vendors to push frequent model updates without long local upgrade cycles. The talent intelligence platform market also favors cloud when buyers want benchmarking across customers and faster access to new AI functions. Even so, hybrid deployment keeps a durable role in industries where data residency, classified workforce information, or audit needs limit full movement into public cloud environments. On-premises deployment remains the smallest and slowest-growing option, but it still matters in sovereign government and defense settings where infrastructure rules are strict.

Privacy rules are one reason hybrid models remain relevant even as cloud grows faster. Cornell eCommons noted that GDPR and Asia-Pacific localization frameworks such as China's PIPL and India's DPDP Act are shaping how companies manage AI in HR, especially when sensitive employee data must stay local while models are governed centrally. That gives the talent intelligence platform market a more complex deployment profile than many pure cloud software categories. Vendors that can support federated architectures without breaking the user experience can command better pricing in regulated accounts. In the talent intelligence platform industry, deployment flexibility is becoming a core buying factor rather than a technical detail.

By Organization Size: Large Enterprises Anchor The Talent Intelligence Platform Market While SMEs Accelerate Faster

Large enterprises held 74.13% of the talent intelligence platform market share in 2025, while SMEs are projected to grow at a 21.53% CAGR through 2031, which creates a two-speed demand structure in the talent intelligence platform market. Large employers still account for most spending because they manage large talent pipelines across many business units, countries, and compliance settings. Their need for cross-border skills visibility and workforce planning makes the platform decision more strategic and more expensive. At the same time, the talent intelligence platform market is opening to smaller buyers as subscription models become more flexible and pre-built skills ontologies reduce setup work. Cornerstone launched Cornerstone Workforce AI in May 2026 with open architecture, actionable skills insights, and governance-oriented auditability, which reflects a broader push to serve organizations at different maturity levels.

SMEs also benefit from flatter structures that can reduce internal resistance to redeployment and talent mobility. That matters because smaller firms can often show measurable results faster once a system is live, which helps justify follow-on spending. Skills-Base reported in 2026 that mature adopters achieved median workforce skills assessment coverage of 82%, showing that strong governance discipline can matter more than company size in actual execution. Vendors that simplify onboarding, data preparation, and governance setup are likely to keep this part of the talent intelligence platform market growing. The pattern suggests that SME expansion will come less from stripped-down tools and more from easier implementation of advanced capabilities.

By End-User Industry: IT And Telecom Lead The Talent Intelligence Platform Market And Healthcare Builds The Fastest Momentum

IT and telecommunications accounted for 24.82% of the talent intelligence platform market size in 2025, while healthcare and life sciences are projected to grow at a 24.12% CAGR through 2031, which highlights where the talent intelligence platform market is currently strongest and where it is moving fastest. IT and telecom led because persistent shortages in software engineering and cybersecurity have made skills visibility and internal mobility immediate business needs. The sector also had a higher comfort level with AI tools, which made adoption easier across recruiting and workforce planning workflows. Healthcare is expanding faster because staffing shortages, clinical credentialing, and competency-based planning create stronger operational pressure for more precise workforce intelligence. This part of the talent intelligence platform market is therefore moving toward deeper vertical specialization rather than only broad horizontal coverage.

Vertical depth is especially important in clinical settings where role matching depends on licensing data, shift constraints, and verified skill histories. Prolucent and SeekOut's nursing talent pool illustrate how specialist workflows can create stronger switching barriers than general recruiting or skills tools. BFSI adoption is shaped by regulated role fitness and formal competency expectations, while manufacturing and retail are gaining momentum as automation changes job tasks and forces employers to redesign roles instead of simply refilling old ones. Cross-sector requirements such as Joint Commission credentialing in healthcare, FCA competence rules in financial services, and ISO 9001 process discipline in manufacturing all raise the value of auditable workflows and validated skill records.[4]International Organization for Standardization, “ISO 9001 Quality Management Systems,” ISO, iso.org Vendors with domain-specific data models can therefore outperform broader platforms when buyers need compliance evidence alongside matching and planning.

Geography Analysis

North America held 41.61% of the talent intelligence platform market share in 2025, which kept it as the largest regional base in the talent intelligence platform market. The United States drives most of that demand because skills-based operating models and enterprise HR technology investment reached scale earlier there than in most other countries. Canada is also moving forward, especially in financial services and public-sector modernization programs, where workforce planning and skills visibility support broader digital transformation. Mexico remains earlier in adoption, but multinational manufacturers are starting to use skills-tracking tools to support cross-border workforce planning and role standardization. South America is still smaller, yet Brazil and Argentina are showing demand from professional services and BFSI firms, and ManpowerGroup's Q2 2026 outlook pointed to continued hiring intent in technology and services across the region.

Europe forms the second-largest regional block in the talent intelligence platform market, with Germany, the United Kingdom, and France leading adoption. Germany's recruitment consulting market fell 3.8% to EUR 2.82 billion (USD 3.07 billion) in 2024, and a further 1.2% decline to EUR 2.78 billion (USD 3.1 billion) was projected for 2025, which supports a shift toward in-house intelligence tooling. Europe also has a distinct compliance pull, because the EU AI Act is pushing employers toward vendors that can show high-risk employment AI controls before and after the August 2026 application point. France is also producing local scale players, and 365Talents reported more than 1 million users across Société Générale, SNCF, and Veolia in 45+ languages, while Russia remains constrained by sanctions and related limits on technology access.

Asia-Pacific is projected to grow at a 22.41% CAGR from 2026 to 2031, making it the fastest-growing region in the talent intelligence platform market. The region is expanding because workforce digitization is accelerating in India, Singapore, Japan, South Korea, and Australia, even though data localization rules are forcing more local deployment choices in some markets. Singapore has become a strong hub for pilots, where APAC-native vendors compete with global firms on multilingual assessment quality and local labor market depth. Japan faces sharp workforce pressure from demographic change and retirement-age extension, which makes redeployment and skills-based mobility tools more urgent for large employers. The Middle East is gaining traction through Saudi Vision 2030 and UAE digitization programs, while Africa remains at an earlier stage with South Africa and Nigeria acting as the main entry markets for enterprise-wide rollouts.

Competitive Landscape

The talent intelligence platform market is moderately fragmented at the enterprise tier, where LinkedIn Corporation, SAP SE, Workday, Oracle, and IBM benefit from large installed HCM relationships and deep enterprise access. Even so, the talent intelligence platform market remains highly competitive at the intelligence layer because specialists such as Eightfold AI, Phenom, Gloat, and TechWolf compete on skills graph depth, workflow automation, and speed of model development. This creates a split structure in the talent intelligence platform market, where distribution strength sits with suite vendors while product-level innovation often comes from specialists. That balance keeps pricing pressure active and encourages both partnerships and acquisitions. Buyers are therefore comparing vendors on ontology quality, integration reliability, compliance readiness, and adoption support rather than on recruiting workflow alone.

Consolidation was one of the clearest strategic themes in 2025 and 2026. SAP's September 2025 acquisition of SmartRecruiters produced its first native product integration in March 2026, connecting SmartRecruiters with SAP SuccessFactors Employee Central and Onboarding to create a more unified hire-to-retire architecture. Workday also made Sana generally available in March 2026, extending a conversational AI layer across HR, finance, and a wide set of third-party enterprise applications. Phenom completed three acquisitions in five months, including EDGE, Be Applied, and Plum, to assemble a broader stack spanning resource planning, cognitive assessment, situational judgment, and psychometric validation.[5]Phenom, “Phenom Acquires Plum,” Phenom, phenom.com These moves show how the talent intelligence platform market is shifting from point functionality toward broader decision support and agentic workflow coverage.

Talent Intelligence Platform Industry Leaders

SAP SE

Workday, Inc.

Oracle Corporation

Eightfold AI Inc.

Beamery Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Eightfold AI launched TalentForge at Cultivate 2026, a platform that allows enterprises to build custom HR applications on top of its Talent Intelligence Engine, accompanied by a 360 Interview capability and Workforce Readiness product, the launch repositioned Eightfold from a point-solution provider to an agentic HR development platform.

- May 2026: Cornerstone OnDemand launched Cornerstone Workforce AI, an open talent intelligence platform designed to provide leaders with actionable skills insights, AI-driven development paths, and governance-grade auditability across workforce decisions, the product competes directly with Workday and SAP SuccessFactors at the enterprise tier.

- April 2026: SAP released its 1H 2026 SAP SuccessFactors update, delivering over 400 innovations including a significant Talent Intelligence Hub upgrade with enhanced skills governance, centralized skills management, and Joule AI assistant integration across talent acquisition and career development workflows.

- April 2026: Phenom People acquired Plum, a psychometric-based talent assessment provider, completing its third acquisition in five months, the combined platform integrates cognitive (Be Applied), situational judgment, and psychometric validation into a single agentic HR infrastructure.

Global Talent Intelligence Platform Market Report Scope

A Talent Intelligence Platform (TIP) is an advanced HR technology solution that integrates artificial intelligence, data analytics, and workforce insights to enable organizations to make data-driven talent decisions. It surpasses traditional HR systems by consolidating data from various sources, delivering a comprehensive view of workforce skills, capabilities, and potential.

The Talent Intelligence Platform Market is Segmented by Component (Platform Software, and Services), Deployment Model (Cloud-based, Hybrid, and On-premises), Organization Size (Large Enterprises, and SMEs), End-User Industry (IT and Telecom, BFSI, Healthcare and Life Sciences, Retail and E-commerce, Manufacturing, Professional Services, Public Sector and Education, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Platform Software |

| Services |

| Cloud-based |

| Hybrid |

| On-premises |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Manufacturing |

| Professional Services |

| Public Sector and Education |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | Asia | China |

| India | ||

| Japan | ||

| South Korea | ||

| Singapore | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Israel | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Platform Software | ||

| Services | |||

| By Deployment Model | Cloud-based | ||

| Hybrid | |||

| On-premises | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-User Industry | IT and Telecom | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Retail and E-commerce | |||

| Manufacturing | |||

| Professional Services | |||

| Public Sector and Education | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | Asia | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Singapore | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East | Saudi Arabia | ||

| United Arab Emirates | |||

| Israel | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the talent intelligence platform market in 2026 and how fast is it growing?

The talent intelligence platform market is valued at USD 6.85 billion in 2026 and is forecast to reach USD 15.46 billion by 2031, growing at a 17.68% CAGR over 2026-2031.

Which component generates the most revenue in talent intelligence platforms?

Platform software leads the revenue mix with a 72.41% share in 2025, showing that enterprises still prefer a central intelligence layer over separate point tools.

Why is Asia-Pacific becoming so important for talent intelligence platforms?

Asia-Pacific is projected to grow at 22.41% CAGR through 2031 because workforce digitization is accelerating, while skills shortages and local deployment needs are creating strong regional demand.

Which customer group is growing the fastest in this space?

SMEs are the fastest-growing organization-size segment, with a projected 21.53% CAGR through 2031, helped by easier pricing models and lower implementation complexity.

Which end-user field is creating the strongest growth opportunity?

Healthcare and life sciences are projected to grow at 24.12% CAGR through 2031 because staffing shortages, credentialing needs, and competency-based planning are raising demand for better workforce intelligence.

What is holding adoption back for many enterprises?

The biggest barriers are integration debt across ATS, HRIS, LMS, and CRM systems, along with tighter rules on bias, privacy, and explainability in AI-assisted employment decisions.

Page last updated on: