Talent Acquisition In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

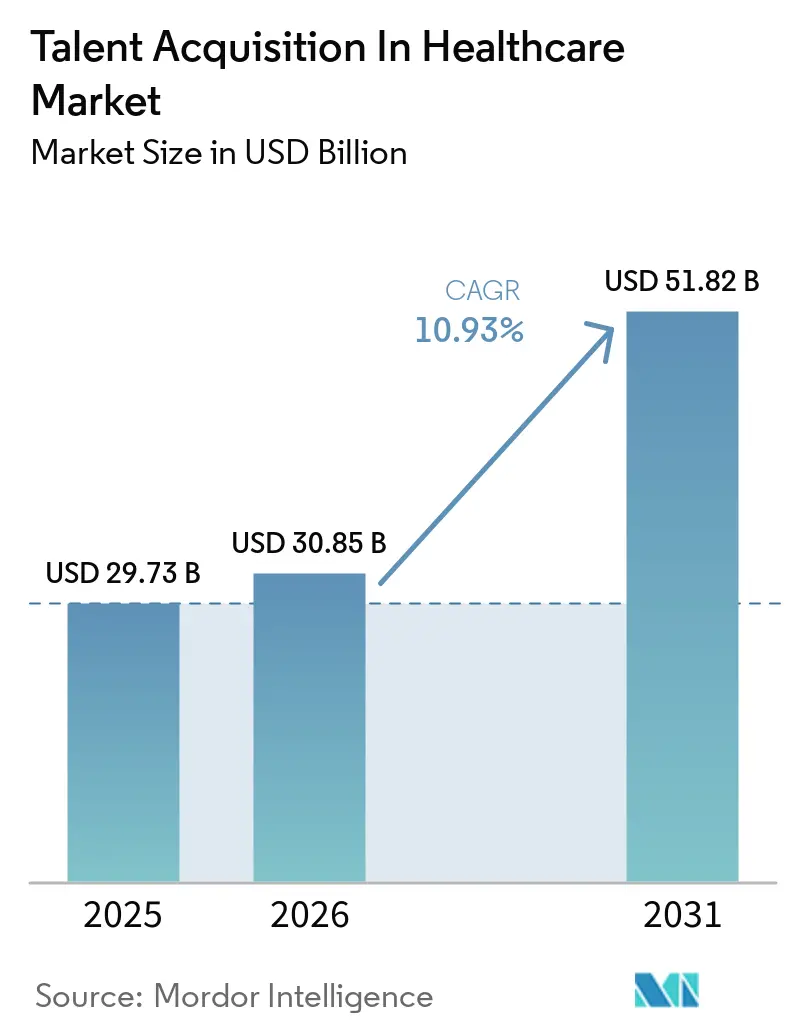

| Market Size (2026) | USD 30.85 Billion |

| Market Size (2031) | USD 51.82 Billion |

| Growth Rate (2026 - 2031) | 10.93% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Talent Acquisition In Healthcare Market Analysis by Mordor Intelligence

The talent acquisition in the healthcare market was valued at USD 29.73 billion in 2025 and is estimated to grow from USD 30.85 billion in 2026 to USD 51.82 billion by 2031, at a CAGR of 10.93% during the forecast period (2026-2031). Structural workforce shortages, coupled with aggressive hospital capacity expansion, are pushing providers to adopt automated credentialing and multistate licensing workflows that streamline hiring cycles. Permanent shifts in care delivery, telehealth normalization, ambulatory surgery center growth, and the rise of home-based acute care fragment demand across settings, forcing recruiters to source clinicians for diverse practice environments. At the same time, the Equal Employment Opportunity Commission’s 2024 guidance on auditing artificial intelligence (AI) tools is encouraging a blended approach that marries predictive analytics with human oversight. The result is an ecosystem in which the talent acquisition in the healthcare market is moving beyond digitizing forms to orchestrating end-to-end workforce intelligence.

Key Report Takeaways

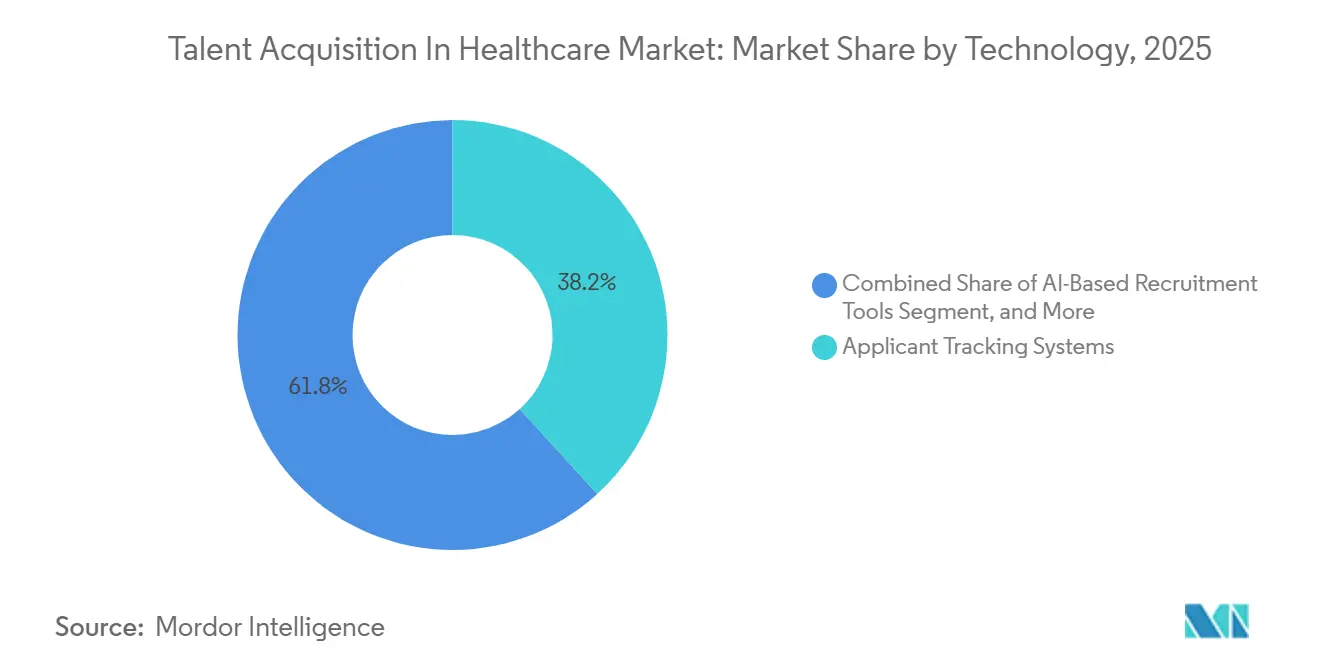

- By technology, applicant tracking systems held 38.28% of 2025 expenditure, while AI-based recruitment tools are expanding at 12.19% through 2031, underscoring a pivot toward predictive candidate matching that is reshaping the talent acquisition in healthcare market.

- By service type, permanent staffing commanded 41.43% revenue share in 2025, yet locum tenens staffing is advancing at 11.43%, reflecting physician burnout and a preference for episodic engagements that is redefining the talent acquisition in healthcare market landscape.

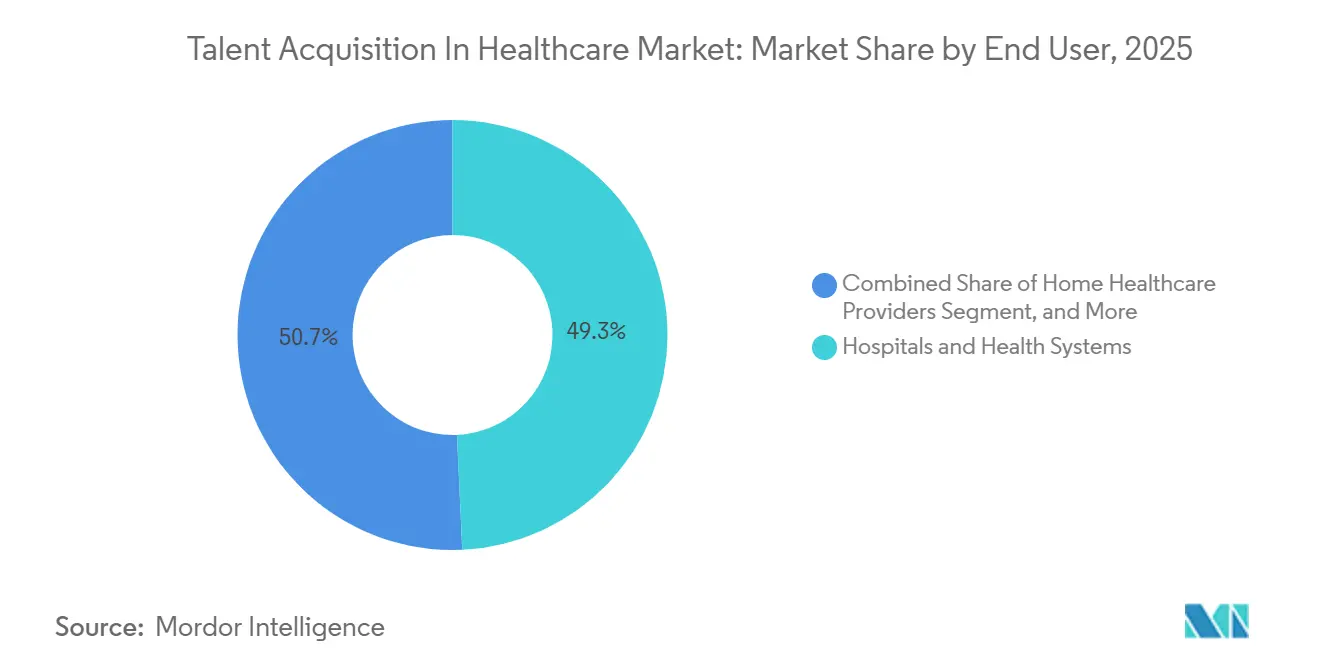

- By end user, hospitals and health systems accounted for 49.28% spending in 2025, whereas home healthcare providers are scaling at 12.71% as Medicare Advantage reforms reward post-acute services delivered at home, accelerating demand within the talent acquisition in healthcare market.

- By mode, outsourced talent acquisition captured 54.23% of 2025 deployment value, but hybrid models are growing at 11.82%, enabling health systems to keep strategic roles in-house while leveraging third-party scale for routine hiring across the talent acquisition in healthcare market.

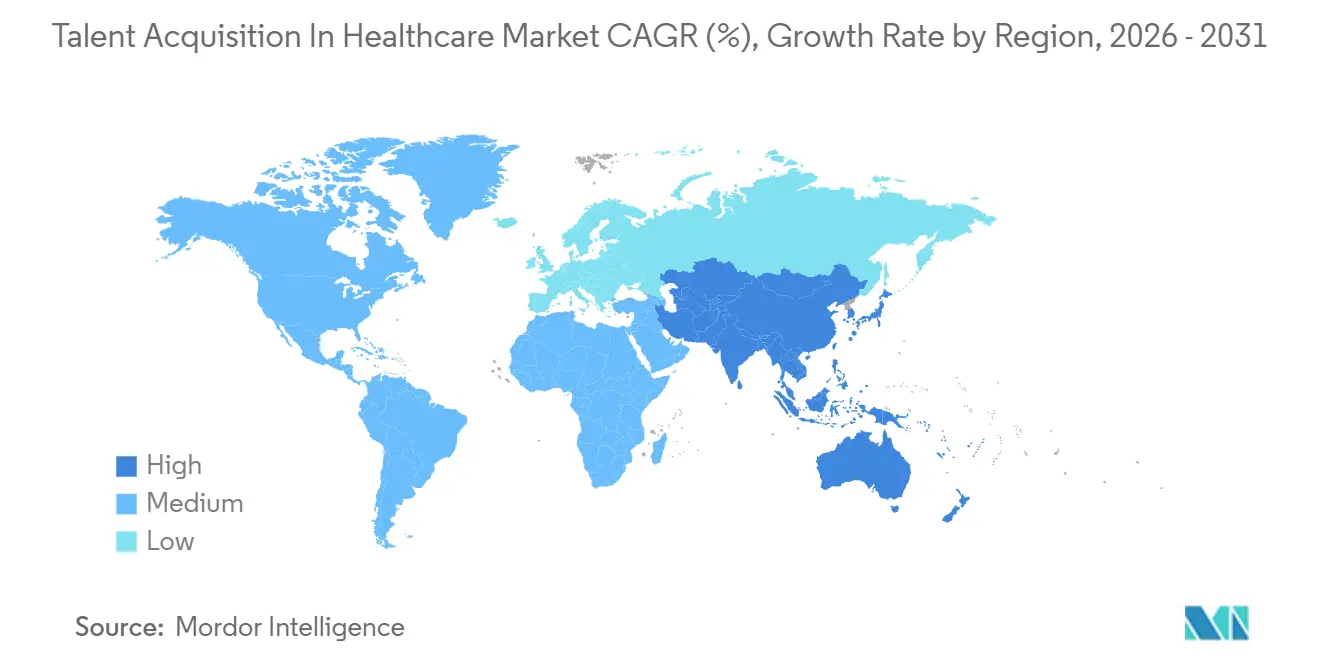

- By geography, North America secured 37.21% revenue share in 2025, yet Asia-Pacific is registering a 10.94% CAGR through 2031 as hospital construction in India, Saudi Arabia, and the United Arab Emirates fuels regional momentum in the talent acquisition in healthcare market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Talent Acquisition In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Workforce Shortages in Allied Health Roles | +2.8% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Accelerating Digital Transformation of Hospital HR Functions | +2.1% | North America and Europe lead, Asia-Pacific catching up | Medium term (2-4 years) |

| Shift Toward Flexible Gig-Based Clinical Staffing Models | +1.7% | North America, expanding to Asia-Pacific urban centers | Medium term (2-4 years) |

| Adoption of AI-Powered Sourcing to Reduce Time-to-Hire | +1.5% | North America, Europe, select Asia-Pacific markets | Short term (≤ 2 years) |

| Growing Regulatory Pressures for Credential Verification Automation | +1.3% | United States, European Union | Medium term (2-4 years) |

| Expansion of Cross-Border Telehealth Driving Global Talent Pools | +0.9% | Global, early gains in the Middle East and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Workforce Shortages in Allied Health Roles

Allied health vacancies are compelling hospitals to pay premium rates for temporary staff, straining operating margins and fueling aggressive recruitment investments. The American Hospital Association reported in 2025 that 94% of executives ranked staffing as their top operational issue, with annual turnover for respiratory therapists and radiology technicians exceeding 30%. Enrollment in allied health programs fell 8% between 2020 and 2024, while outpatient diagnostics demand jumped 17% over the same span. Health systems are launching apprenticeship pipelines, but those programs take three to five years to produce certified workers, leaving an acute gap that staffing agencies exploit through per-diem placements. Rural providers are hit hardest because clinicians cluster in cities for higher wages, forcing small hospitals to rely on travelers whose costs are 40-60% higher than those of permanent staff. Consequently, talent acquisition in the healthcare market must balance immediate stopgaps with long-term workforce development.[1]American Hospital Association, “2025 Workforce Scan,” AHA.ORG

Accelerating Digital Transformation of Hospital HR Functions

Hospital HR digitization is evolving from back-office automation to strategic workforce forecasting. Children’s Hospital of Philadelphia cut nursing time-to-hire from 62 to 38 days after rolling out an AI-enabled applicant tracking system in 2024, saving an estimated USD 4.2 million annually. Modern platforms now integrate with electronic health records to flag high-performing clinicians before they enter the job market, lowering cost-per-hire by 30-40%. Credentialing vendors such as Propelus compress onboarding from 45 to 15 days, allowing hospitals to ramp capacity faster during seasonal spikes. The National Committee for Quality Assurance mandated monthly sanction monitoring in 2025, pushing facilities toward automated compliance. These breakthroughs reinforce a data-driven culture that is redefining how talent acquisition in the healthcare market operates.[2]Children’s Hospital of Philadelphia, “Annual Report 2024,” CHOP.EDU

Shift Toward Flexible Gig-Based Clinical Staffing Models

Gig staffing platforms mimic ride-hailing dynamics, letting clinicians bid on shifts in real time and choose assignments that fit lifestyle needs. A 2025 American Nurses Association survey found 62% of nurses under 35 favored contract, or per-diem work over full-time employment. Facilities respond by creating internal float pools, yet external platforms aggregate demand across employers and pay premiums that hospitals struggle to match. While rotation heightens continuity-of-care risks, gig staffing supplies rapid relief during flu surges and natural disasters. The talent acquisition in the healthcare market is therefore recalibrating around flexibility, balancing clinical quality with workforce preferences.[3]National Committee for Quality Assurance, “Credentialing Standards Update,” NCQA.ORG

Adoption of AI-Powered Sourcing to Reduce Time-to-Hire

AI tools scrape millions of professional profiles to uncover passive candidates, cutting recruiter workloads by up to 60%. Video interviews scored by natural language processing further accelerate selection decisions. However, labor unions in 17 U.S. states contended in 2025 that algorithms sideline mid-career nurses, compelling hospitals to incorporate manual review layers. In 2024, the Equal Employment Opportunity Commission mandated annual bias audits of AI systems, driving “human-in-the-loop” operating models. These safeguards are shaping adoption curves across the healthcare talent acquisition market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Sensitivity of Candidate Data to Cyber-Security Breaches | -1.2% | Global; acute in North America | Short term ≤ 2 years |

| Fragmented Licensing Rules Across US States and EU Nations | -0.9% | United States; European Union | Medium term 2-4 years |

| Union-Led Resistance to Algorithmic Screening Tools | -0.6% | North America; select European markets | Short term ≤ 2 years |

| Budget Constraints in Rural and Safety-Net Facilities | -0.8% | Rural United States; parts of Africa and South America | Long term ≥ 4 years |

| Source: Mordor Intelligence | |||

High Sensitivity of Candidate Data to Cyber-Security Breaches

Recruitment platforms store Social Security numbers, license records, and malpractice histories, making them prime targets for ransomware. The February 2024 attack on Change Healthcare exposed data on over 100 million individuals and cost USD 2.3 billion in remediation.[4]Reuters Staff, “UnitedHealth Faces USD 2.3 Billion in Costs After Cyberattack,” REUTERS.COM Under the Health Insurance Portability and Accountability Act, inadequate safeguards can result in fines of up to USD 1.5 million per violation. Hospitals now require vendors to obtain SOC 2 Type II certification and undergo annual penetration tests, which are inflating compliance costs, especially for small agencies. These cyber risks temper investment appetite in talent acquisition in the healthcare market.

Fragmented Licensing Rules Across US States and EU Nations

Licensing fragmentation slows multi-state and cross-border hiring. As of 2025, 41 states have adopted the enhanced Nurse Licensure Compact, yet California and New York still require standalone credentials that add 60-90 days to onboarding. Only 40 states participate in the Interstate Medical Licensure Compact, and each new license can cost up to USD 1,500. In Europe, member states impose language exams beyond the requirements of Directive 2005/36/EC, delaying foreign nurse entry by 6-12 months. These hurdles curb clinician mobility and add administrative overhead across the healthcare talent acquisition market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: AI Tools Reshape Candidate Discovery

Applicant tracking systems accounted for 38.28% spending in 2025 and remain the system of record for most hospitals. Yet the segment’s growth is moderating as buyers prioritize platforms that mesh with payroll, scheduling, and electronic health records. AI-enabled sourcing and candidate relationship management solutions, growing 12.19% annually, are redefining how talent acquisition in the healthcare market evolves at the technology layer. Hospitals deploying these tools report time-to-hire reductions of 20-30% and lower “ghosting” rates, because machine-learning engines nudge candidates with automated reminders.

The talent acquisition market share for traditional background screening software is shrinking as hospitals seek unified stacks that conduct criminal checks, license verification, and reference checks in a single workflow. Video interviewing remains commonplace for telehealth roles, but pricing compression is driving consolidation. Vendors differentiating on predictive analytics, such as recommending competitive pay bands based on regional benchmark data, are gaining traction, especially among large systems that hire thousands of clinicians yearly.

By Service Type: Locum Tenens Gains as Burnout Persists

Permanent staffing delivered 41.43% of 2025 revenue, reflecting ongoing demand for full-time clinicians. Yet rising physician burnout propels an 11.43% CAGR for locum tenens services, which now represent a critical pressure valve for facilities in remote geographies. This growth influences the talent acquisition in the healthcare market, as episodic contracts fetch premium bill rates that outpace inflation.

Managed service providers (MSPs) and recruitment process outsourcing (RPO) continue to gain share by offering bundled contingent labor, compliance monitoring, and vendor consolidation. Hospitals using MSPs report administrative savings of 15-20% because a single dashboard unifies invoicing and credential tracking. Meanwhile, temporary allied health staffing is broadening beyond respiratory therapy into imaging and laboratory specialties, widening the scope of talent acquisition in the healthcare industry.

By End User: Home Healthcare Surges on Payment Reforms

Hospitals and health systems remain the largest buyers, accounting for 49.28% of 2025 spending, but home healthcare providers are experiencing 12.71% annual growth. Reimbursement changes under Medicare Advantage spur hospital-at-home models, thereby altering demand patterns within the healthcare talent acquisition market. Agencies must vet caregivers for competence with remote monitoring technology alongside traditional bedside skills.

Ambulatory surgical centers seek perioperative nurses who can manage same-day discharge pathways, while diagnostic laboratories staff for chronic disease panels that proliferated after COVID-19 normalized routine testing. Long-term care facilities confront turnover exceeding 40%, forcing greater reliance on agencies. Collectively, these shifts diversify the talent acquisition in the healthcare market across end users.

By Mode: Hybrid Models Balance Control and Efficiency

Outsourced models accounted for 54.23% of the value in 2025, but a projected 11.82% CAGR for hybrid approaches signals a nuanced sourcing landscape. Large integrated delivery networks keep strategic hires in-house to safeguard cultural alignment, yet outsource high-volume ancillary roles to RPO vendors, creating a blended structure within the broader healthcare talent acquisition market.

Unified technology stacks make hybrid oversight feasible by consolidating pipelines, whether leads flow from an internal recruiter or an agency partner. Hospitals that adopt hybrid MSP agreements report 360-degree visibility into cost-per-hire, fill rates, and credential lag times. As reimbursement models sharpen the focus on quality outcomes, retaining strategic oversight of physician recruitment while leveraging third-party speed for support roles becomes the dominant operating model.

Geography Analysis

North America generated 37.21% revenue in 2025, anchored by the United States’ multistate licensing complexity, elevated clinician wages, and a payer mix that sustains premium bill rates. Enhanced Nurse Licensure Compact adoption across 41 states eases nurse mobility, but California and New York maintain independent processes that prolong onboarding. Canada bolsters rural coverage by importing 4,200 international medical graduates in 2025, an 18% jump from 2023. Mexico’s private hospital boom along the border attracts bilingual care teams, funneling cross-border recruitment dollars into the healthcare talent acquisition market.

Asia-Pacific posts the fastest regional trajectory with a 10.94% CAGR to 2031. India’s surplus of 140,000 nurses in 2025 feeds outbound staffing pipelines to Gulf Cooperation Council nations and Australia. Saudi Arabia’s Vision 2030 hospital build-out and the United Arab Emirates’ specialty clinic growth amplify regional demand. Japan faces an aging population, with 28.7% of the population over 65 in 2025, prompting investments in robotics and task-shifting to offset nursing shortages. China’s private hospital segment grows 12% annually, but provincial licensing and Hukou restrictions impede national staffing platforms, limiting scale advantages in regional healthcare talent acquisition.

Europe’s free-movement directive, in theory, simplifies credential portability, yet language and competency tests in Germany, France, and Italy create bottlenecks. Germany hired 12,400 foreign nurses in 2025, largely from the Philippines and India, to mitigate demographic pressures. The United Kingdom’s National Health Service filled 35% of nursing vacancies with international recruits in 2025, but competition from Gulf countries offering higher wages is eroding its pull factor. South America remains under-penetrated, though private hospital chains in Brazil and Argentina are beginning to adopt structured vendor management, hinting at future growth opportunities for talent acquisition in the healthcare market.

Competitive Landscape

The top five global firms held only a modest share in 2025, indicating that the healthcare talent acquisition market is moderately fragmented. AMN Healthcare Services and CHG Healthcare Services use MSP contracts to embed multi-year relationships, bundling contingent and permanent hiring under single agreements that streamline hospital procurement. Aya Healthcare leverages a mobile-first platform that cuts placement time from 45 to 20 days, resonating with younger clinicians seeking real-time shift bidding.

Cross Country Healthcare and Ingenovis Health differentiate through breadth, spanning nursing, allied health, and physician specialties, enabling hospitals to compress vendor rosters. Technology investment is the chief battleground. Vendors that integrate applicant tracking, candidate relationship management, and predictive analytics into a single interface outperform peers still reliant on manual spreadsheets.

Niche specialists flourish in high-complexity domains such as interventional radiology and neonatal intensive care, where deep practitioner networks command premium fees. Compliance capabilities, including 50-state licensure tracking and real-time sanction monitoring, act as barriers to entry and create operating leverage for incumbents. Consequently, the competitive dynamic centers on technology maturity, data security posture, and vertical specialization within the wider healthcare talent acquisition market.

Talent Acquisition In Healthcare Industry Leaders

AMN Healthcare Services Inc.

CHG Healthcare Services Inc.

Cross Country Healthcare Inc.

Jackson Healthcare LLC

Aya Healthcare Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: CHG Healthcare Services rolled out an AI credentialing platform that trims onboarding from 45 to 15 days by integrating state boards and the National Practitioner Data Bank.

- January 2026: Aya Healthcare secured USD 150 million in Series D funding led by Fidelity Investments to expand into allied health and enhance 90-day staffing demand forecasts.

- December 2025: Cross Country Healthcare bought a home healthcare staffing agency for USD 62 million, adding 3,500 caregivers to capitalize on post-acute reimbursement reforms.

- November 2025: Ingenovis Health partnered with HireVue to deploy video interviewing across nursing and allied health divisions, reducing time-to-hire by 35%.

Global Talent Acquisition In Healthcare Market Report Scope

The talent acquisition in the healthcare market refers to the ecosystem of technologies, staffing models, and service providers that enable hospitals, clinics, and care facilities to recruit, credential, and retain clinicians. It encompasses permanent, temporary, and gig staffing solutions, leveraging AI, compliance automation, and workforce analytics to balance quality care with evolving workforce preferences.

The Talent Acquisition in Healthcare Market Report is Segmented by Technology (Applicant Tracking Systems, Candidate Relationship Management Platforms, AI-Based Recruitment Tools, Video Interviewing Platforms, Background Screening Software, and Other Technologies), Service Type (Permanent Staffing Services, Temporary Staffing Services, Recruitment Process Outsourcing, Managed Service Providers, Locum Tenens Staffing, and Other Service Types), End User (Hospitals and Health Systems, Ambulatory Surgical Centers, Nursing Homes and Long-Term Care Facilities, Home Healthcare Providers, Diagnostic Laboratories, and Other Healthcare Providers), Mode (In-House Talent Acquisition, Outsourced Talent Acquisition, and Hybrid Model), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Applicant Tracking Systems (ATS) |

| Candidate Relationship Management Platforms |

| AI-Based Recruitment Tools |

| Video Interviewing Platforms |

| Background Screening Software |

| Other Technologies |

| Permanent Staffing Services |

| Temporary Staffing Services |

| Recruitment Process Outsourcing (RPO) |

| Managed Service Providers (MSP) |

| Locum Tenens Staffing |

| Other Service Types |

| Hospitals and Health Systems |

| Ambulatory Surgical Centers |

| Nursing Homes and Long-Term Care Facilities |

| Home Healthcare Providers |

| Diagnostic Laboratories |

| Other Healthcare Providers |

| In-House Talent Acquisition |

| Outsourced Talent Acquisition |

| Hybrid Model |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Technology | Applicant Tracking Systems (ATS) | |

| Candidate Relationship Management Platforms | ||

| AI-Based Recruitment Tools | ||

| Video Interviewing Platforms | ||

| Background Screening Software | ||

| Other Technologies | ||

| By Service Type | Permanent Staffing Services | |

| Temporary Staffing Services | ||

| Recruitment Process Outsourcing (RPO) | ||

| Managed Service Providers (MSP) | ||

| Locum Tenens Staffing | ||

| Other Service Types | ||

| By End User | Hospitals and Health Systems | |

| Ambulatory Surgical Centers | ||

| Nursing Homes and Long-Term Care Facilities | ||

| Home Healthcare Providers | ||

| Diagnostic Laboratories | ||

| Other Healthcare Providers | ||

| By Mode | In-House Talent Acquisition | |

| Outsourced Talent Acquisition | ||

| Hybrid Model | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current talent acquisition in healthcare market size?

The talent acquisition in healthcare market size stood at USD 29.73 billion in 2025 and is forecast to reach USD 51.82 billion by 2031, according to Mordor Intelligence.

Which technology segment is growing the fastest?

AI-based recruitment tools are expanding at a 12.19% CAGR through 2031 as hospitals shift from simple workflow digitization to predictive candidate matching.

Why is locum tenens staffing gaining traction?

Physician burnout and a desire for schedule flexibility are driving an 11.43% CAGR for locum tenens services, enabling hospitals to cover gaps without long-term commitments.

How are payment reforms influencing hiring patterns?

Medicare Advantage incentives for at-home post-acute care are pushing home healthcare providers to accelerate hiring, producing a 12.71% growth rate for the segment.

What limits cross-border telehealth recruitment?

Fragmented licensing, such as state-by-state rules in the United States and varied language exams in Europe, adds months to onboarding and stifles clinician mobility.

Which regions offer the highest growth opportunities?

Asia-Pacific leads with a 10.94% CAGR to 2031, driven by hospital construction in India and the Gulf states as well as relaxed foreign-worker policies.

Page last updated on: