Competitive Intelligence Tools Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 0.59 Billion |

| Market Size (2030) | USD 1.46 Billion |

| Growth Rate (2025 - 2030) | 19.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

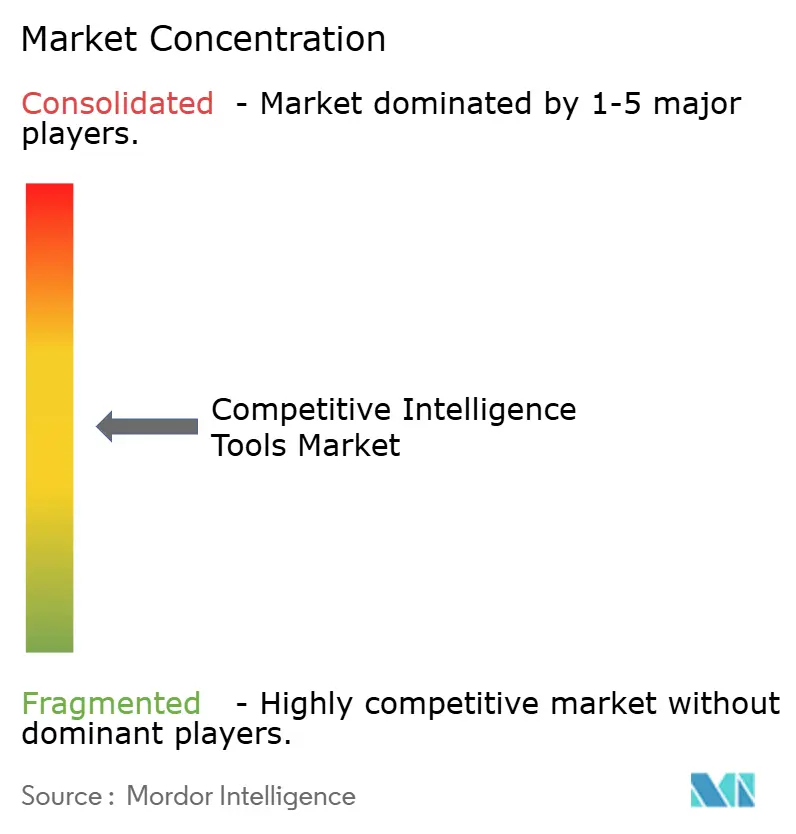

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Competitive Intelligence Tools Market Analysis by Mordor Intelligence

The competitive intelligence tools market size stood at USD 0.59 billion in 2025 and, supported by a 19.96% CAGR, is forecast to reach USD 1.46 billion by 2030. Powerful AI-driven data-fusion capabilities, cloud scalability, freemium pricing, and tighter regulatory oversight are collectively accelerating enterprise adoption. Organizations that embed real-time competitor monitoring into revenue operations report materially shorter sales cycles, while cloud deployment lowers total cost of ownership and speeds implementation. Large enterprises still account for over 60% of spending, yet SMEs are catching up quickly because freemium and usage-based plans remove historical licensing barriers. Vendors are increasingly positioning platforms as embedded decision-intelligence layers rather than standalone dashboards, which is catalyzing both ecosystem partnerships and M&A.

Key Report Takeaways

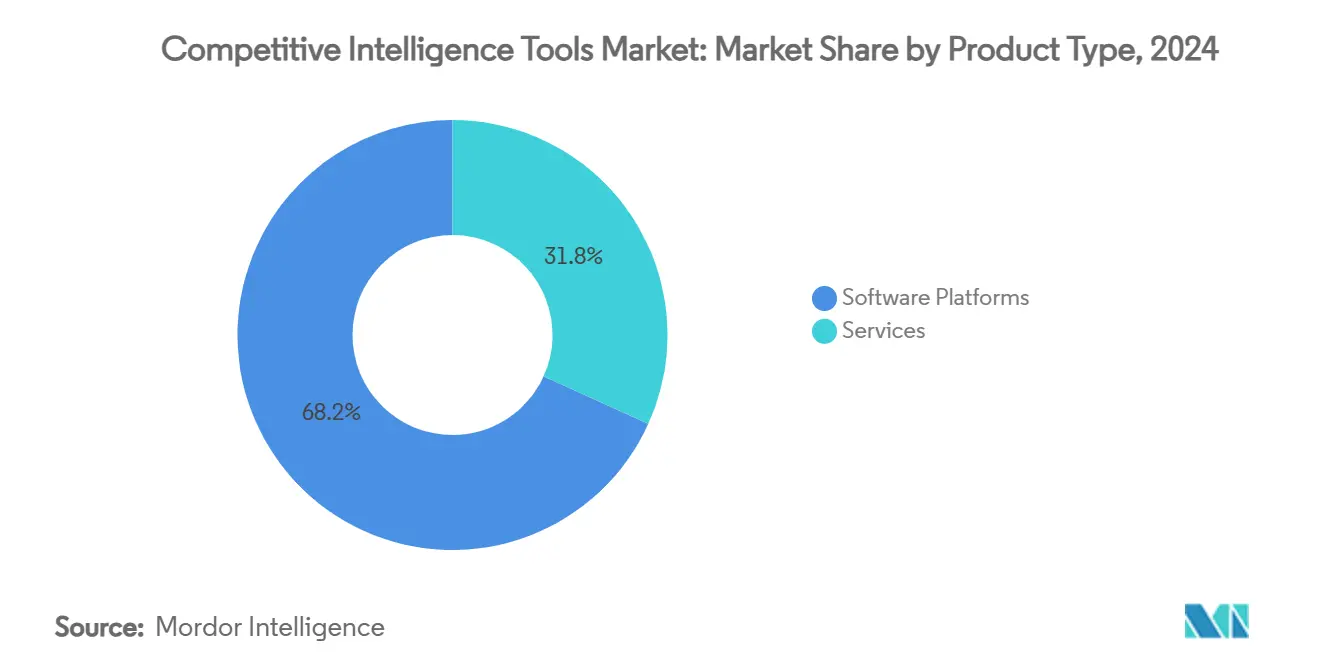

- By product type, software platforms led with 68.23% of competitive intelligence tools market share in 2024, whereas services are projected to grow fastest at a 20.64% CAGR through 2030.

- By deployment mode, cloud captured 78.04% share of the competitive intelligence tools market size in 2024 and is forecast to expand at a 22.64% CAGR to 2030.

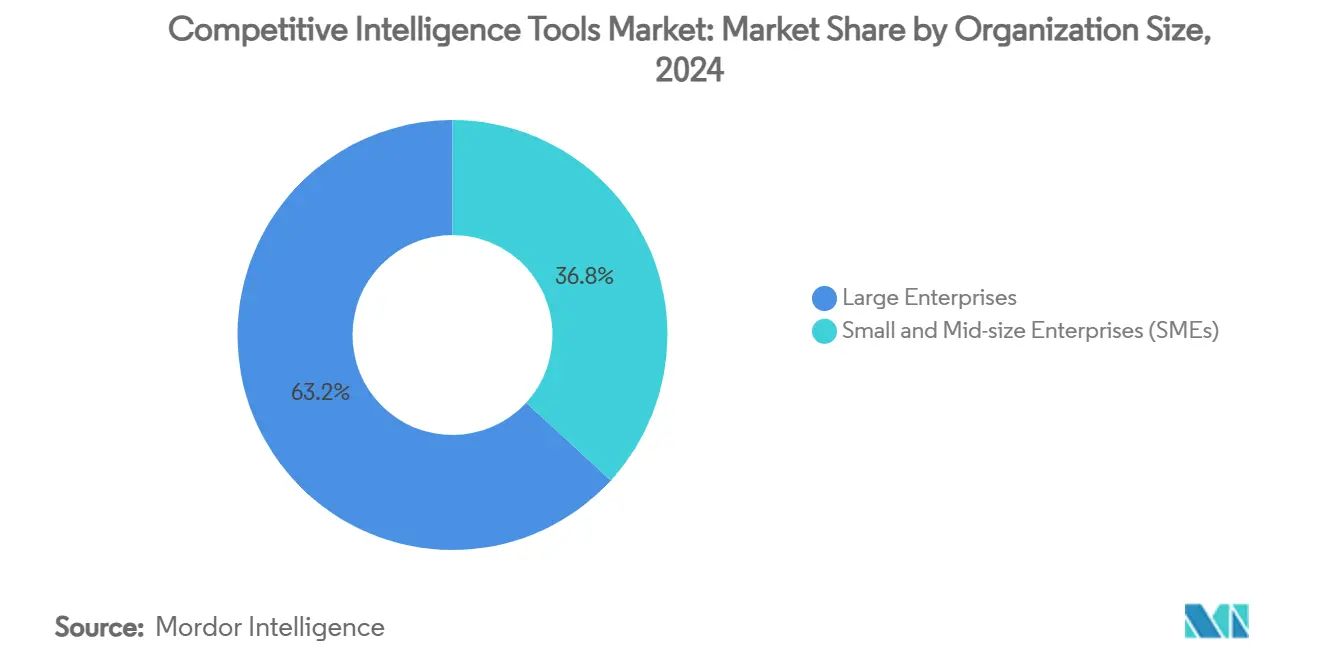

- By organization size, large enterprises held 63.18% of the competitive intelligence tools market size in 2024, while SMEs will advance at a 21.53% CAGR between 2025–2030.

- By end-user industry, technology and telecom commanded 25.74% of competitive intelligence tools market share in 2024 and healthcare is set to record the highest 21.89% CAGR through 2030.

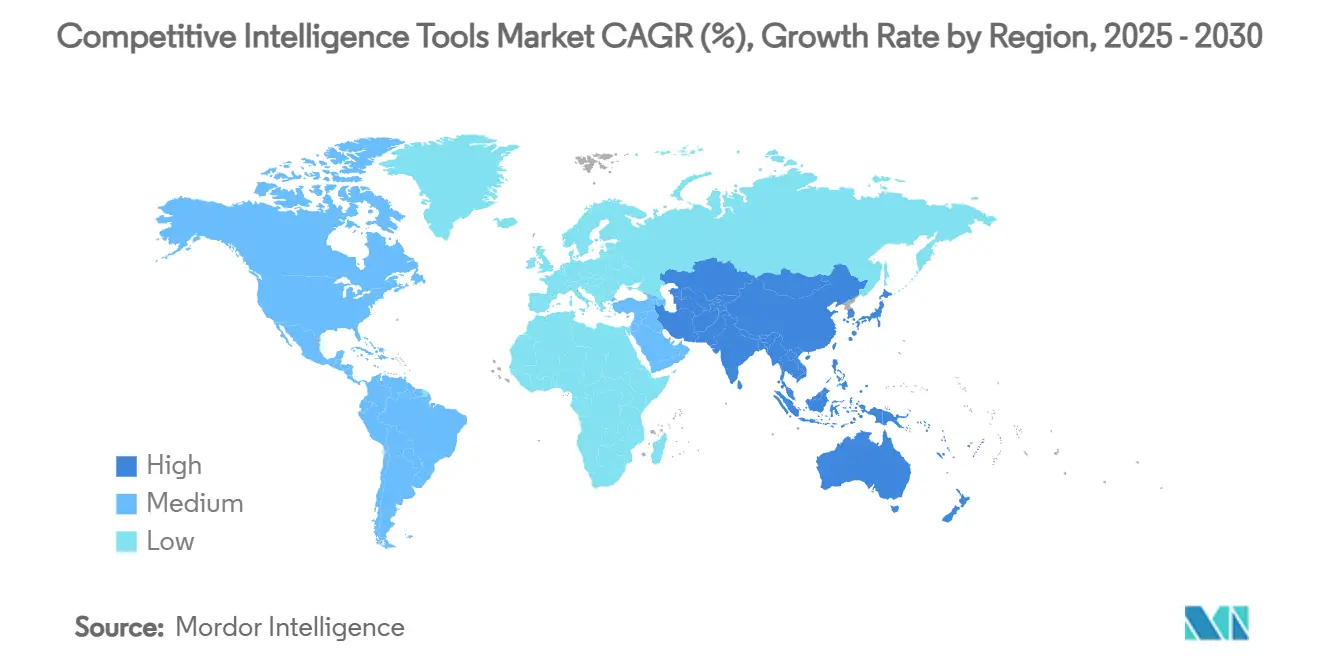

- By geography, North America maintained 39.41% share in 2024, whereas Asia-Pacific is expected to post a 23.67% CAGR during 2025-2030.

Global Competitive Intelligence Tools Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven data fusion boosts actionable insights | +4.2% | Global, with concentration in North America & APAC | Medium term (2-4 years) |

| Enterprise shift toward "continuous intelligence" workflows | +3.8% | North America & EU primary, expanding to APAC | Long term (≥ 4 years) |

| Democratization of alt-data (mobile, web, geolocation) APIs | +3.1% | Global, with early adoption in tech hubs | Short term (≤ 2 years) |

| Freemium pricing disrupting incumbent license models | +2.9% | Global, particularly impacting SME adoption | Medium term (2-4 years) |

| Privacy-preserving analytics compliance (GDPR 2.0, CPRA) | +2.4% | EU & California leading, global spillover | Long term (≥ 4 years) |

| Adoption inside revenue-ops to shorten competitive deal cycles | +2.1% | North America & EU, expanding to enterprise APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI-driven Data Fusion Boosts Actionable Insights

Generative AI allows platforms to unify structured and unstructured feeds, raising prediction accuracy by 33% and cutting data-processing time 45%.[1]Strategic & Competitive Intelligence Professionals, “Leveraging GenAI for Competitive Intelligence,” scip.org Manufacturing firms adopting these engines have deployed them across supply-chain nodes, enabling earlier detection of vendor risk and competitive moves. Patent activity around multimodal document ingestion underscores the technical moat being built by leading vendors. The widening gap between AI-powered leaders and manual analysts is reshaping procurement criteria, pushing buyers to prioritize model explainability and domain-specific training data. Consequently, vendors with proprietary language models secure higher renewal rates.

Enterprise Shift toward Continuous-Intelligence Workflows

Weekly distribution of competitor signals correlates with 31% stronger revenue impact compared with monthly cycles.[2]LexisNexis, “Total Economic Impact Study,” lexisnexis.com Integrations with CRM and revenue-ops stacks ensure real-time alerts surface inside opportunity records, compressing deal-response time. Large technology firms quantify a USD 1.20 million net present value over three years from these deployments. Patent filings around automated playbook triggers indicate that future roadmaps will lean on robotic process automation fused with competitive feeds. Early adopters in BFSI and telecom now position continuous intelligence as a board-level KPI.

Democratization of Alt-data APIs

Low-cost access to mobile, web, and geolocation streams equips SMEs with insight once reserved for Fortune 500 strategists. Studies show SMEs using BI suites trimmed process time 12% and increased revenue 15%. Asia-Pacific momentum is accelerating as regionally trained language models proliferate, easing multilingual ingestion challenges. Vendors are commercializing vertical datasets-such as decentralized-finance ledgers-to widen use cases. The opportunity forces buyers to refine data-quality governance to avoid noisy signals that distort strategy.

Freemium Pricing Disrupts Incumbent License Models

Usage-based metering lowers entry barriers, allowing SMEs to pilot AI modules without six-figure contracts. Analysts record a surge of pricing overhauls as vendors shift from seat-based fees to event-based or outcome-based structures. While gross margins tighten compared with classic SaaS, vendors gain broader funnel reach that converts to higher lifetime value once advanced features are unlocked. Investors reward platforms that demonstrate rapid user-base expansion even at lower ARPU, driving further capital into go-to-market experimentation. Incumbents retaliate by bundling premium datasets and advanced visualization into enterprise tiers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising legal exposure from web-scraping litigations | -2.8% | Global, with highest impact in US & EU | Short term (≤ 2 years) |

| High internal change-management costs for CI programme roll-out | -2.1% | North America & EU primary, emerging in APAC | Medium term (2-4 years) |

| Data silos and poor CRM/BI integration | -1.9% | Global, particularly affecting large enterprises | Medium term (2-4 years) |

| Volatility of third-party data sources (API deprecation, paywalls) | -1.6% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Legal Exposure from Web-scraping Litigations

GDPR, CPRA, and the forthcoming EU AI Act impose strict consent and transparency mandates that complicate large-scale data harvesting.[3]Secure Privacy, “AI & GDPR Compliance Challenges,” secureprivacy.ai Enforcement is tightening, with 144 jurisdictions now imposing privacy statutes covering 82% of the global population. Vendors respond by adopting privacy-preserving analytics, audit trails, and source-attribution tags. Legal teams negotiate indemnification clauses into master agreements, raising total cost of ownership and lengthening procurement cycles. Some buyers ring-fence high-risk scraping to third-party partners to limit exposure.

High Internal Change-Management Costs for CI Programme Roll-out

Enterprises embracing competitive intelligence platforms must fund training, workflow redesign, and cultural shifts toward data-driven decisions. Organizations with performance KPIs tied to competitive-insight utilization are four times likelier to report positive revenue impact, yet achieving this maturity requires significant upfront investment. Legacy process owners often resist new cadences, slowing ROI realization. Manufacturing case studies illustrate that success hinges on cross-functional collaboration and governance boards that standardize taxonomy. Vendors counter the hurdle by packaging onboarding accelerators and managed-service bundles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Platforms Retain Control While Services Scale Expertise

Software platforms commanded 68.23% of competitive intelligence tools market share in 2024, generating the majority of subscription revenue through integrated data ingestion, analytics, and visualization modules. Services, however, will register a 20.64% CAGR across 2025-2030 as enterprises seek implementation support, custom connector builds, and managed monitoring to maximize value extraction.

Services growth rests on client recognition that technology alone does not guarantee insight. Specialist consultancies deliver taxonomy alignment, data-quality audits, and change-management roadmaps. Pure-play platform vendors respond by building in-house professional-services teams, aiming to capture downstream revenue and defend account control. The interplay of core platform revenue with higher-margin advisory creates cross-sell momentum, particularly among large enterprises rolling out multi-geography deployments.

By Deployment Mode: Cloud Model Accelerates

Cloud solutions held 78.04% of competitive intelligence tools market size in 2024, and the segment will expand at 22.64% CAGR to 2030 driven by elastic compute requirements for AI-heavy workloads. Cloud vendors leverage geographic availability zones to meet data-residency mandates while offering continuous model updates that on-premises stacks cannot match.

High-compliance verticals still preserve certain use-cases on-premises. Yet even heavily regulated institutions increasingly adopt virtual-private-cloud architectures combined with customer-managed keys. Platform providers employ reference architectures certified under SOC 2, ISO 27001, and GDPR to mitigate security concerns, driving cloud preference across procurement scorecards. Freemium pricing aligns naturally with cloud delivery, enabling event-based billing that tracks API calls and model inferences.

By Organization Size: SME Momentum Builds

Large enterprises generated 63.18% of competitive intelligence tools market size in 2024 owing to multi-department deployments and complex analytical requirements. SMEs, however, will scale fastest at 21.53% CAGR through 2030 as usage-metered tiers democratize access.

SMEs prioritize out-of-the-box connectors and templated dashboards that shorten time-to-insight. Vendors courting the segment focus on simplified UI, guided onboarding, and marketplace integrations with popular CRM suites. Meanwhile, large enterprises act as innovation incubators for predictive engines and deep-learning summarizers, which eventually cascade into lighter SME editions. The two segments therefore create a virtuous cycle of feature refinement and distribution expansion.

By End-User Industry: Tech Leads, Healthcare Accelerates

Technology and telecom companies held 25.74% competitive intelligence tools market share in 2024, driven by rapid product cycles and aggressive go-to-market plays. Healthcare and life sciences will register a 21.89% CAGR to 2030 as precision medicine, regulatory submissions, and drug-pricing wars necessitate near-real-time competitor tracking.

In BFSI, regulatory monitoring fuels demand for alerts on policy changes, while manufacturing uses supplier intelligence to foresee margin pressures. Retailers adopt price-scraping utilities for dynamic repricing engines. The breadth of use cases pushes vendors toward modular architectures that let clients add vertical-specific data packs without re-platforming.

Geography Analysis

North America retained 39.41% competitive intelligence tools market share in 2024 on the back of mature SaaS penetration, venture capital funding, and landmark deals such as AlphaSense acquiring Tegus for USD 930 million. Early adoption of continuous-intelligence workflows yields tangible ROI, evidenced by a 110% return reported by enterprises leveraging integrated research suites. Sub-regional demand extends into Canada and Mexico as cross-border trade drives intelligence needs around supply-chain resilience.

Asia-Pacific is the fastest-growing theatre, forecast at 23.67% CAGR through 2030. Governments in China, Japan, and India place AI at the center of digital-economy roadmaps, while Forrester expects 60% of enterprises to deploy regionally trained LLMs by 2025. Although only 41% of firms currently leverage AI tools, skill-development programs and cloud-infrastructure expansion are closing this gap. Local language support and sovereign-cloud options are decisive factors in vendor selection.

Europe maintains consistent momentum as GDPR and the impending EU AI Act heighten requirements for auditable data pipelines. Vendors with privacy-by-design credentials win procurement cycles, illustrated by ChapsVision acquiring Sinequa for EUR 85 million (USD 92 million) to expand compliant enterprise search. Strong adoption in Germany’s manufacturing cluster and London’s financial hub continues to anchor regional revenue, while Southern Europe gains traction through digital-fund stimulus packages.

Competitive Landscape

The competitive intelligence tools market is moderately fragmented yet tilting toward consolidation. AlphaSense, Similarweb, and Crayon defend share through proprietary data networks, domain-specific language models, and collaboration features. Mastercard’s USD 2.65 billion takeover of Recorded Future underscores non-traditional entrants embedding intelligence into core workflows.

Start-ups counter by focusing on vertical precision or disruptive pricing. Klue’s Compete Agent applies generative AI to automate battlecard creation, appealing to B2B sellers that need real-time objection handling. Patent filings show a surge in automated document-classification and multimodal intent discovery, indicating a race for intellectual property defensibility.

Strategic partnerships are equally active. Cloud hyperscalers integrate competitive-intelligence connectors into data-fabric offerings, positioning themselves as neutral orchestration layers. System integrators package competitive-intelligence modules within broader digital-transformation programs, accelerating enterprise-wide adoption. Vendors differentiate by offering governance toolkits, sector-specific taxonomies, and API marketplaces that embed intelligence into existing BI or CRM investments.

Competitive Intelligence Tools Industry Leaders

AlphaSense Inc.

Similarweb Ltd.

Crayon AS

Klue Labs Inc.

CI Radar LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Datasite acquired Grata, a New York private-market intelligence company, backed by CapVest Partners’ USD 500 million investment, enhancing market-intelligence solutions for M&A professionals.

- May 2025: IgniteTech acquired Khoros, a digital-first customer-engagement platform serving 2,000 companies, to infuse AI features into community and service offerings.

- April 2025: Dataminr secured a USD 100 million investment from Fortress Investment Group to accelerate corporate-enterprise growth and global expansion.

- April 2025: AlertMedia bought Pyrra Technologies, an AI-enabled social-media monitoring firm tracking 3 billion conversations annually.

Global Competitive Intelligence Tools Market Report Scope

| Software Platforms |

| Services |

| Cloud-based |

| On-premises |

| Large Enterprises |

| Small and Mid-size Enterprises (SMEs) |

| Technology and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Manufacturing and Industrial |

| Retail and eCommerce |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Software Platforms | ||

| Services | |||

| By Deployment Mode | Cloud-based | ||

| On-premises | |||

| By Organisation Size | Large Enterprises | ||

| Small and Mid-size Enterprises (SMEs) | |||

| By End-User Industry | Technology and Telecom | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Manufacturing and Industrial | |||

| Retail and eCommerce | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the competitive intelligence tools market growing until 2030?

Revenue is projected to expand from USD 0.59 billion in 2025 to USD 1.46 billion in 2030, reflecting a 19.96% CAGR.

Which deployment mode dominates client spending?

Cloud accounts for 78.04% of 2024 revenue and is forecast to grow at a 22.64% CAGR as enterprises favor elastic compute for AI workloads.

What segment registers the quickest future growth?

Services are set to rise at 20.64% CAGR through 2030 because firms need implementation, training, and managed-intelligence support.

Why are SMEs increasing their adoption rate?

Freemium and usage-based tariffs remove traditional licensing barriers, enabling SMEs to trial advanced functions at lower entry costs.

Which region shows the highest future potential?

Asia-Pacific is predicted to achieve a 23.67% CAGR as local language models and government digital-economy programs drive demand.

How are acquisitions reshaping the vendor landscape?

High-value deals such as Mastercard-Recorded Future and AlphaSense-Tegus signal integration of intelligence layers into broader enterprise platforms, accelerating consolidation.

Page last updated on: