North America Talent Acquisition Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

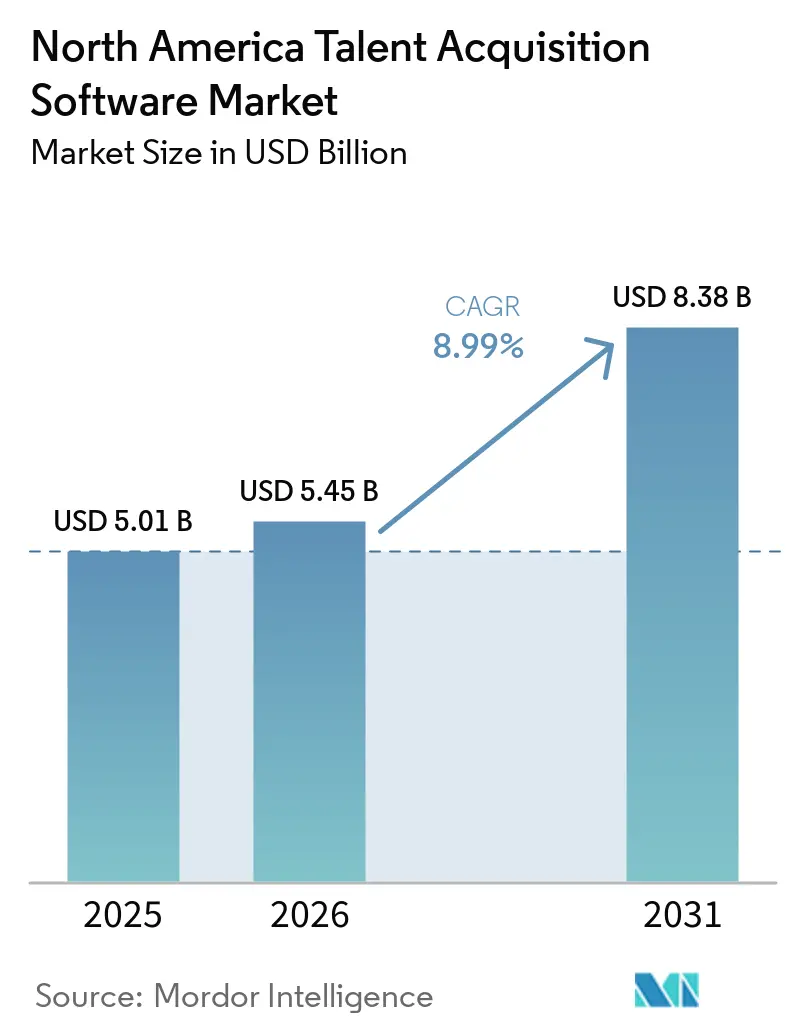

| Base Year Market Size (2025) | USD 5.01 Billion |

| Market Size (2026) | USD 5.45 Billion |

| Market Size (2031) | USD 8.38 Billion |

| Growth Rate (2026 - 2031) | 8.99% CAGR |

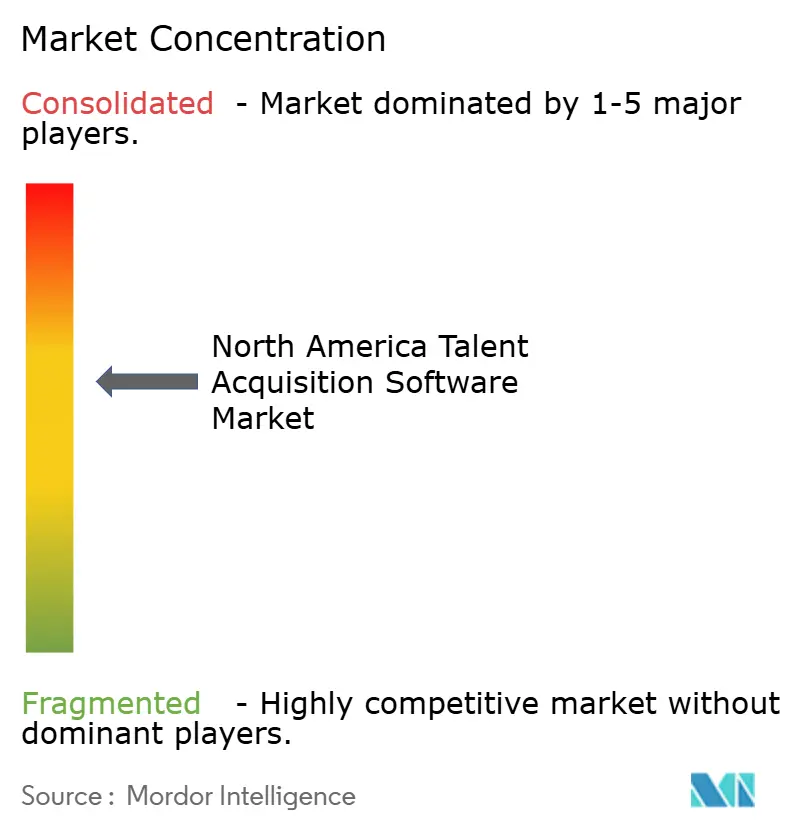

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Talent Acquisition Software Market Analysis by Mordor Intelligence

The North America talent acquisition software market size is projected to expand from USD 5.11 billion in 2025 and USD 5.45 billion in 2026 to USD 8.38 billion by 2031, registering a CAGR of 8.99% between 2026 and 2031. The North America talent acquisition software market is growing as employers replace manual and episodic hiring workflows with connected platforms that support continuous recruiting. AI adoption, tight labor conditions, and privacy rules across the United States, Canada, and Mexico are pushing buyers to treat recruiting software as a core part of business capability rather than a back-office tool. The market is also moving toward cloud delivery, stronger analytics, and employer brand tools as companies try to improve hiring speed and candidate quality. Vendor competition is narrowing around deeper platforms because buyers want fewer tools, cleaner integrations, and stronger audit controls. This keeps the North America talent acquisition software market on a path where growth comes from both new demand and stack consolidation.

Key Report Takeaways

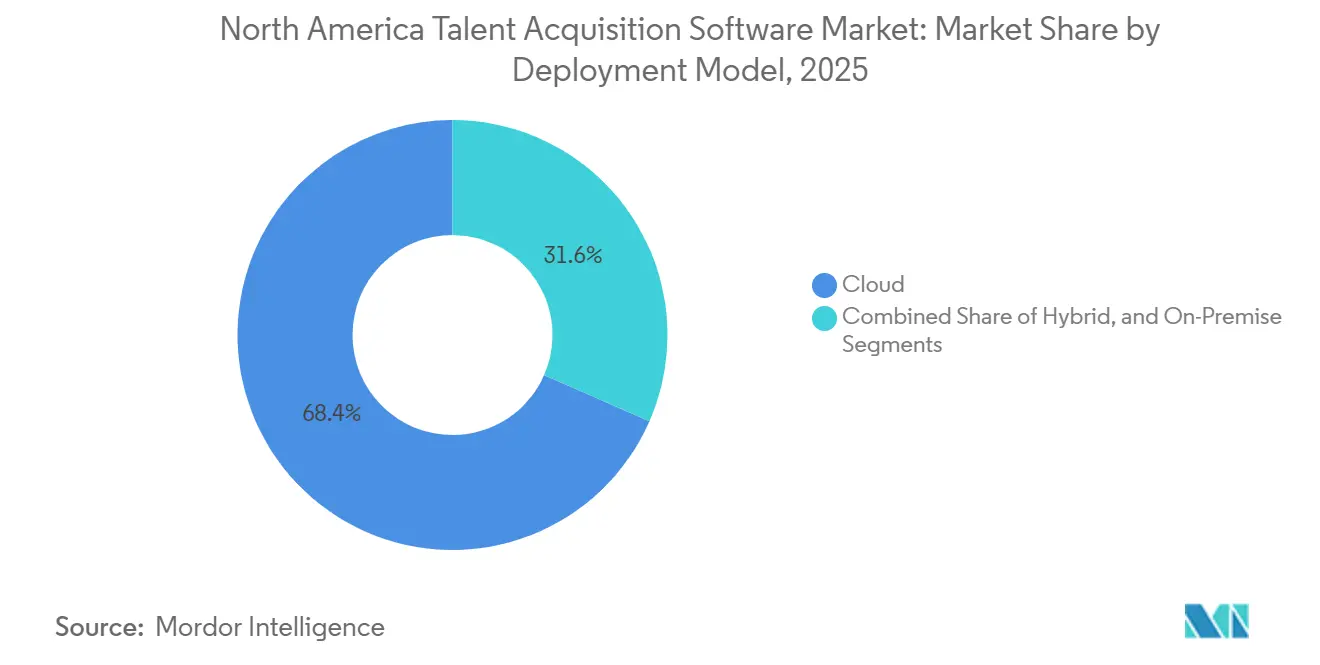

- By deployment model, cloud held 68.43% of the market value in 2025, while hybrid is projected to grow at 11.21% CAGR through 2031.

- By application, applicant tracking systems accounted for 31.61% of the market in 2025, while recruitment marketing is forecast to expand at a 12.42% CAGR through 2031.

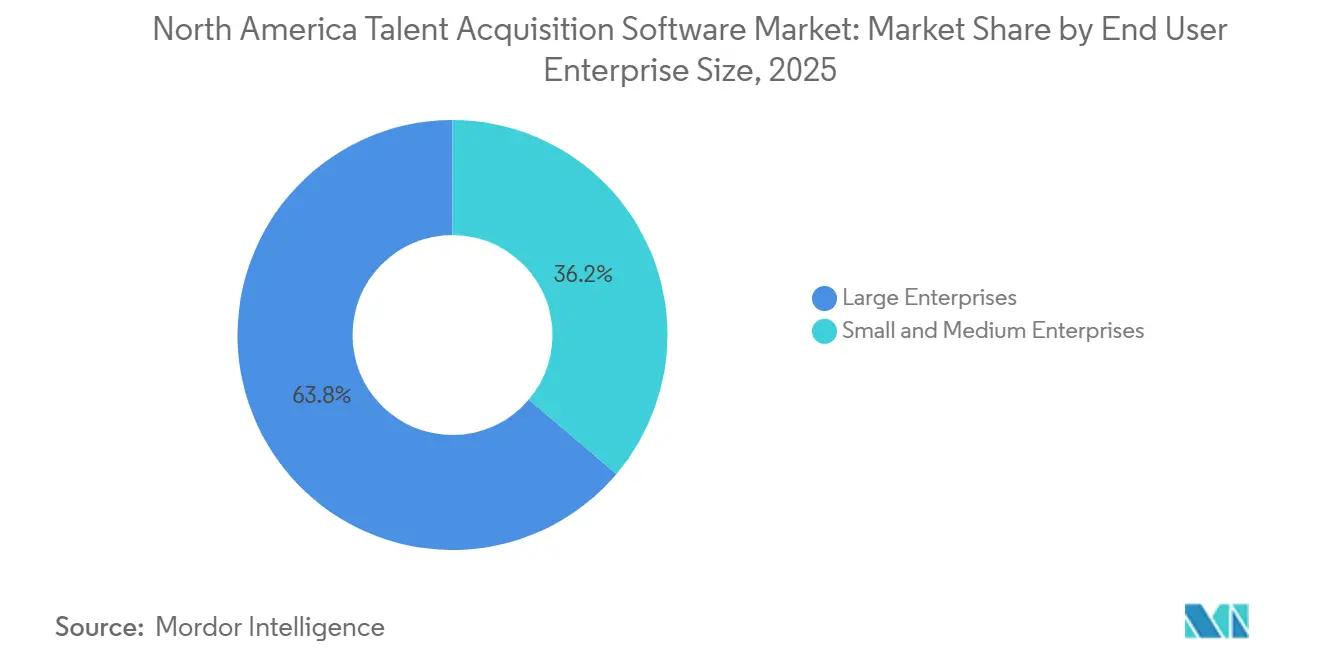

- By end-user enterprise size, large enterprises held 63.82% of market value in 2025, while small and medium enterprises are projected to grow at a 10.81% CAGR through 2031.

- By end-user enterprise industry vertical, information technology and telecommunications accounted for a 24.71% share in 2025, while healthcare and life sciences are forecast to expand at a 11.63% CAGR through 2031.

- By geography, the United States accounted for 84.11% of the regional market value in 2025, while Mexico is projected to grow at a 10.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Talent Acquisition Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption of AI-Based Recruiting Tools | +3.2% | Global | Short term (= 2 years) |

| Rising Demand for Data-Driven Hiring Decisions | +2.5% | North America and EU | Medium term (2-4 years) |

| Growing Gig Economy Requiring Agile Staffing Platforms | +1.8% | North America | Medium term (2-4 years) |

| Expansion of Remote and Hybrid Work Models | +1.4% | Global | Short term (= 2 years) |

| Upskilling Initiatives Driving Internal Mobility Solutions | +0.9% | North America | Long term (= 4 years) |

| VC Funding Surge for HR Tech Startups | +0.7% | North America and EU | Short term (= 2 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption Of AI-Based Recruiting Tools

AI screening, sourcing, and matching tools are now close to baseline expectations for buyers in the North America talent acquisition software market. Research showed that 78% of high-growth staffing firms had embedded AI in ATS workflows, and 46% said AI reduced candidate screening time by half or more.[1]Bullhorn, “GRID 2026 Staffing Industry Trends Report,” Bullhorn, bullhorn.com The same findings revealed that only 10% had implemented agentic AI across the full workflow, leaving a clear gap between basic adoption and full orchestration. In April 2026, Oracle introduced eight new AI agent applications within Oracle Fusion Cloud HCM to address that gap. Another survey found that 52% of talent leaders plan to deploy autonomous AI agents in 2026, while only 22% believe their organizations are ready to manage human-AI teams, supporting continued spending on governance and change support in the North America talent acquisition software market.

Rising Demand For Data-Driven Hiring Decisions

The North America talent acquisition software market is gaining board-level attention as employers measure the cost of slow hiring, weak sourcing, and poor early retention. Talent leaders using AI in hiring were more likely to report C-suite influence, at 85% versus 70% for non-AI users.[2]Oracle Corporation, “Oracle Introduces Oracle Fusion Agentic Applications for HR,” Oracle, oracle.com That shift is raising demand for platforms that combine workflow automation with predictive analytics and outcome tracking. Vendors that connect candidate attributes with post-hire performance are building proprietary datasets that are hard to replicate. This is making data depth a stronger competitive factor in the North America talent acquisition software market than feature breadth alone.

Growing Gig Economy Requiring Agile Staffing Platforms

The rise of independent work is changing how the North America talent acquisition software market is structured around permanent and contingent hiring needs. Full-time independent workers in the United States increased from 13.6 million in 2020 to 27.7 million in 2024, equal to 16.7% of the workforce.[3]Upwork, “Independent Work Trends Using MBO Partners Data,” Upwork, upwork.com Traditional ATS tools were built for permanent roles, so many employers now need systems that also support rapid sourcing, compliance checks, and project-based onboarding. That shift was acknowledged in September 2025 when iCIMS acquired Apli to extend coverage in frontline and gig hiring, including Mexico-linked labor flows. Governance and compliance tracking for contingent workers has also been identified as the biggest unmet need among enterprise HR buyers in 2026, supporting continued module expansion across the North America talent acquisition software market.

Expansion Of Remote And Hybrid Work Models

Hybrid work remains a major demand driver for the North America talent acquisition software market because employers now recruit across wider geographies than before. In 2025, 76% of organizations operated with hybrid structures. That operating model requires cross-time-zone scheduling, video assessment, and location-aware compliance support that older office-centered systems do not handle well. It also expands candidate pools, raising application volumes per role and increasing the value of AI-assisted screening. Workday’s January 2026 launch of Paradox ATS, with a 3.5-day average time-to-hire and 95% candidate satisfaction in early deployments, illustrates how vendors are building for fast distributed hiring in the North America talent acquisition software market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Compliance Complexities (CCPA, CPRA) | -1.2% | North America (United States and Canada focus) | Medium term (2-4 years) |

| Integration Challenges with Legacy HRIS Platforms | -0.9% | Global, with North America concentration | Long term (≥ 4 years) |

| Economic Slowdown Impacting Hiring Budgets | -0.7% | Global | Short term (≤ 2 years) |

| Talent Acquisition Software Vendor Saturation | -0.5% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy And Compliance Complexities

Privacy and automated decision-making rules are slowing parts of the buying cycle in the North America talent acquisition software market. California’s automated decision-making technology rules, effective January 1, 2026, apply directly to AI systems that make or substantially inform hiring decisions.[4]Littler Mendelson P.C., “California Automated Decision-Making Technology Rules and Hiring Impact,” Littler, littler.com Buyers now want clear audit trails, transparency disclosures, candidate notices, and consent controls before approving software purchases. Ontario added a second compliance layer when its Working for Workers Four Act took effect on January 1, 2026, requiring disclosure of AI use in hiring processes. The result is not weaker demand, but a clear preference in the North America talent acquisition software market for vendors that can prove compliance by design.

Integration Challenges With Legacy HRIS Platforms

Legacy HRIS environments continue to limit deployment speed in the North America talent acquisition software market because recruiting tools still need stable links with payroll, benefits, and workforce planning systems. Buyers are increasingly wary of adding point solutions that create more APIs, more version management work, and more data synchronization risk. Recurring API version changes underscore why third-party ATS connections require ongoing maintenance to maintain data fidelity. This ongoing maintenance burden pushes enterprise buyers toward end-to-end platforms rather than fragmented stacks. As a result, integration pressure is helping larger suite vendors strengthen their position in the North America talent acquisition software market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Adoption Keeps Platform Architecture Flexible

Cloud held 68.43% of the North America talent acquisition software market share in 2025, while hybrid is projected to grow at 11.21% CAGR through 2031. This shows the market still favors cloud delivery for scale, subscription pricing, and frequent feature updates. Cloud platforms also support faster AI rollouts because vendors can deploy new models and workflow tools without local infrastructure changes. UKG reinforced that direction in April 2026 by integrating Google Cloud’s Gemini Agent Gallery into UKG Pro.

Hybrid growth remains important because some employers still need local control over parts of their data environment. That is especially relevant in government-linked hiring, defense-related work, and selected BFSI use cases where public cloud adoption can remain limited. The North America talent acquisition software market for hybrid deployments is expanding as organizations operate across the United States, Canada, and Mexico and face varying data-handling obligations in each location. Once firms move core recruiting into cloud-native systems, they also accumulate historical hiring data, configured scoring logic, and skills taxonomies that are hard to migrate, which increases retention for early platform leaders in the North America talent acquisition software market.

By Application: ATS Remains Core While Recruitment Marketing Gains Speed

Applicant tracking systems accounted for 31.61% of the market value in 2025, while recruitment marketing is forecast to expand at a 12.42% CAGR through 2031 in the North America talent acquisition software market. ATS remains the system of record because it manages candidates, workflows, approvals, and compliance documentation in one place. CRM tools are gaining relevance as employers build pools of future candidates before roles formally open. Onboarding, interview management, assessment, and related tools are also moving closer to the recruiting stack instead of operating as separate HR functions.

Recruitment marketing is growing faster because employers now treat candidate attraction more like customer acquisition. As AI-generated applications increase overall volume, stronger brand signals are needed to attract qualified applicants who fit the role and culture. This shift was reinforced in March 2025 when Employ Inc. acquired Pillar and reported a 26% reduction in time-to-fill among pilot users. Over time, vendors that track the link from career site visit to accepted offer can build proprietary data advantages, giving recruitment marketing a more strategic role in the North America talent acquisition software market.

By End User Enterprise Size: SME Adoption Broadens The Buyer Base

Large enterprises accounted for 63.82% of the market value in 2025, while small and medium enterprises are projected to grow at 10.81% CAGR through 2031. Large employers continue to lead the North America talent acquisition software market due to long-standing HCM contracts, custom integrations, and larger compliance requirements, which favor established vendors with mature ATS, analytics, and support capabilities. However, SaaS pricing has lowered barriers, bringing advanced recruiting tools within reach of smaller organizations.

This shift is driven by hiring pressure as smaller technology firms compete with large employers for scarce talent, requiring stronger sourcing, screening, and candidate experience tools. Platforms such as Greenhouse, BambooHR, and Zoho Recruit are addressing these needs with cloud-based, easy-to-deploy offerings. SAP’s September 2025 acquisition of SmartRecruiters, which served around 4,000 organizations, highlighted how large vendors are seeking exposure to mid-market demand. As a result, the talent acquisition software industry is expanding beyond large enterprise budgets into broader operating needs across firms with 50 to 500 employees.

By End User Enterprise Industry Vertical: Healthcare Hiring Needs Lift Investment

Information technology and telecommunications accounted for 24.71% of market value in 2025, while healthcare and life sciences are projected to grow at 11.63% CAGR through 2031. Technology employers lead the North America talent acquisition software market due to sustained demand for specialized talent and early adoption of AI-enabled hiring tools. BFSI also remains important for auditable screening and stronger background verification. Retail and eCommerce require rapid, high-volume hiring, while government agencies continue modernizing slow civil service processes.

Healthcare and life sciences are growing faster because staffing gaps and credential complexity are difficult to manage manually. The average time-to-fill for registered nurse roles was 59 days in 2025. A 2026 review of healthcare staffing priorities found that hospital TA teams were planning investments in AI-powered credential matching and predictive demand forecasting. Nearshoring is also boosting demand for hiring software in industrial manufacturing, particularly where bilingual recruiting is needed across the United States, Canada, and Mexico in the North America talent acquisition software market.

Geography Analysis

The United States held 84.11% of the North America talent acquisition software market share in 2025, remaining the center of demand thanks to its concentration of enterprise software buyers, deep technology hiring activity, and strong HR technology funding base. California’s automated decision-making rules, effective January 1, 2026, have changed procurement criteria by making auditability, transparency, and consent management core product requirements. Surveys also showed that 84% of U.S.-based talent leaders planned to use AI in their next hiring cycle, indicating that compliance friction is not reducing AI intent in the North America talent acquisition software market.

Canada adds a different mix of regulatory and operating requirements. Ontario’s Working for Workers Four Act took effect on January 1, 2026, requiring employers to disclose the use of AI in recruitment and hiring. Employers in Canada are prioritizing AI-driven sourcing and onboarding automation to improve workforce agility. Bilingual deployment needs, provincial employment rules, and cross-province mobility also favor vendors that can localize products beyond U.S.-centered implementations.

Mexico is the fastest-growing country in the North America talent acquisition software market, with a projected CAGR of 10.91% through 2031. Growth is tied to nearshoring, as U.S. and Canadian companies expand production and technology operations across northern and central Mexico. This shift is creating demand for platforms that support bilingual communication, local labor compliance, and integration with local employment channels. The September 2025 acquisition of Apli demonstrated that vendors see Mexico as a direct growth market rather than an extension of U.S. hiring workflows. As a result, the North America talent acquisition software market in Mexico is being driven by a shift from informal or agency-led hiring to more structured ATS-led processes.

Competitive Landscape

The North America talent acquisition software market has a two-layer competitive structure. A concentrated upper tier, led by Workday, SAP SuccessFactors, and Oracle Fusion Cloud, competes for large enterprise contracts through broader platform coverage and deeper contract relationships. A wider field of specialist providers still competes on workflow depth, speed, and narrower use cases. SAP’s completed SmartRecruiters acquisition in September 2025 and Oracle’s launch of eight new AI agent applications in April 2026 show how larger vendors are closing capability gaps with both product expansion and acquisition activity.

The market is also seeing pressure from AI-native challengers. Juicebox raised USD 80 million in March 2026 at a USD 850 million valuation, showing that growth capital continues to support focused hiring platforms built around AI-first design. Elly entered the market in February 2026 with USD 8 million in seed funding, highlighting investor interest in lighter alternatives to legacy ATS deployments. This puts incumbents under pressure to improve AI orchestration while keeping costs and user complexity under control.

Commercial white space remains strongest in cross-border contingent workforce management, audit-ready AI screening, and internal mobility tools that connect hiring with workforce redeployment. These openings are particularly relevant where employers need stronger governance for AI use, better skills visibility, and smoother hiring across the United States-Mexico corridor. The market is therefore moving toward vendors that combine compliance, analytics, and broad workflow support within a single architecture. Standards-based reporting and growing algorithm accountability expectations are adding a qualification layer that goes beyond product features alone. Vendors that package AI tools with governance support are likely to capture a larger share of the enterprise upgrade cycle as buyer scrutiny increases.

North America Talent Acquisition Software Industry Leaders

Workday Inc.

SAP SE

Oracle Corporation

iCIMS Inc.

Automatic Data Processing Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: iCIMS, in partnership with Aptitude Research, released findings indicating that 69% of organizations report using AI in talent acquisition while only 18% have achieved broad workflow integration, identifying an adoption gap with significant implications for full-cycle TA software platform investment.

- April 2026: Oracle introduced Oracle Fusion Agentic Applications for HR, launching 8 new AI agent applications within Oracle Fusion Cloud HCM that automate complex, multi-step talent management and recruiting workflows, including job requisition drafting, candidate matching, and offer generation, at scale.

- April 2026: UKG and Google Cloud launched the Gemini Agent Gallery within UKG Pro, featuring the People Assist agent for HR workflow automation, with general availability scheduled for July 2026. The partnership embeds Google’s Gemini large-language model capabilities directly into UKG’s cloud-native TA and HR platform.

- March 2026: SAP deepened the integration between SmartRecruiters and SAP SuccessFactors, deploying Joule and Winston AI agents to create a continuous AI-orchestrated hiring workflow, the first fully connected HCM and TA platform offering from SAP following the September 2025 acquisition.

North America Talent Acquisition Software Market Report Scope

The North America talent acquisition software market comprises digital platforms and tools that streamline recruiting, sourcing, screening, and onboarding for both permanent and contingent roles. It emphasizes AI-driven workflows, compliance-ready documentation, and integration with broader HR systems. Demand is shaped by hybrid work, regulatory requirements, and enterprise-scale hiring needs, making cloud delivery and workflow automation central to growth.

The North America Talent Acquisition Software Report is segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Application (Applicant Tracking System, Candidate Relationship Management, Recruitment Marketing, Onboarding, Interview Management and Assessment, and Other Talent Acquisition Applications), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Information Technology and Telecom, Banking Financial Services and Insurance, Healthcare and Life Sciences, Industrial Manufacturing, Retail and eCommerce, and Government and Public Sector), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-Premise |

| Hybrid |

| Applicant Tracking System (ATS) |

| Candidate Relationship Management (CRM) |

| Recruitment Marketing |

| Onboarding |

| Interview Management and Assessment |

| Other Talent Acquisition Applications |

| Large Enterprises |

| Small and Medium Enterprises |

| Information Technology (IT) and Telecom |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Industrial Manufacturing |

| Retail and eCommerce |

| Government and Public Sector |

| United States |

| Canada |

| Mexico |

| By Deployment Model | Cloud |

| On-Premise | |

| Hybrid | |

| By Application | Applicant Tracking System (ATS) |

| Candidate Relationship Management (CRM) | |

| Recruitment Marketing | |

| Onboarding | |

| Interview Management and Assessment | |

| Other Talent Acquisition Applications | |

| By End User Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By End User Enterprise Industry Vertical | Information Technology (IT) and Telecom |

| Banking, Financial Services and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| Industrial Manufacturing | |

| Retail and eCommerce | |

| Government and Public Sector | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current size of the North America talent acquisition software market?

The North America talent acquisition software market was valued at USD 5.11 billion in 2025, reached USD 5.45 billion in 2026, and is forecast to reach USD 8.38 billion by 2031 at an 8.99% CAGR.

What is driving growth in talent acquisition software across North America?

Growth is being supported by wider AI use in recruiting, stronger demand for analytics in hiring, hybrid work, and a shift toward more connected and auditable recruiting platforms.

Which deployment model leads adoption in this space?

Cloud led with 68.43% of market value in 2025, while hybrid is the fastest-growing model with an 11.21% CAGR through 2031.

Which application area is growing the fastest?

Recruitment marketing is the fastest-growing application segment, with a projected 12.42% CAGR through 2031, while applicant tracking system remained the largest segment in 2025 with 31.61% share.

Why is Mexico the fastest-growing country in this regional landscape?

Mexico is forecast to grow at 10.91% CAGR through 2031 because nearshoring is increasing demand for bilingual, compliance-capable hiring platforms across manufacturing and technology operations.

How are privacy regulations changing software buying decisions?

Employers are placing more weight on audit trails, candidate notices, transparency controls, and AI governance because California and Ontario rules now affect how AI can be used in hiring.

Page last updated on: