Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.09 Billion |

| Market Size (2026) | USD 1.16 Billion |

| Market Size (2031) | USD 1.56 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

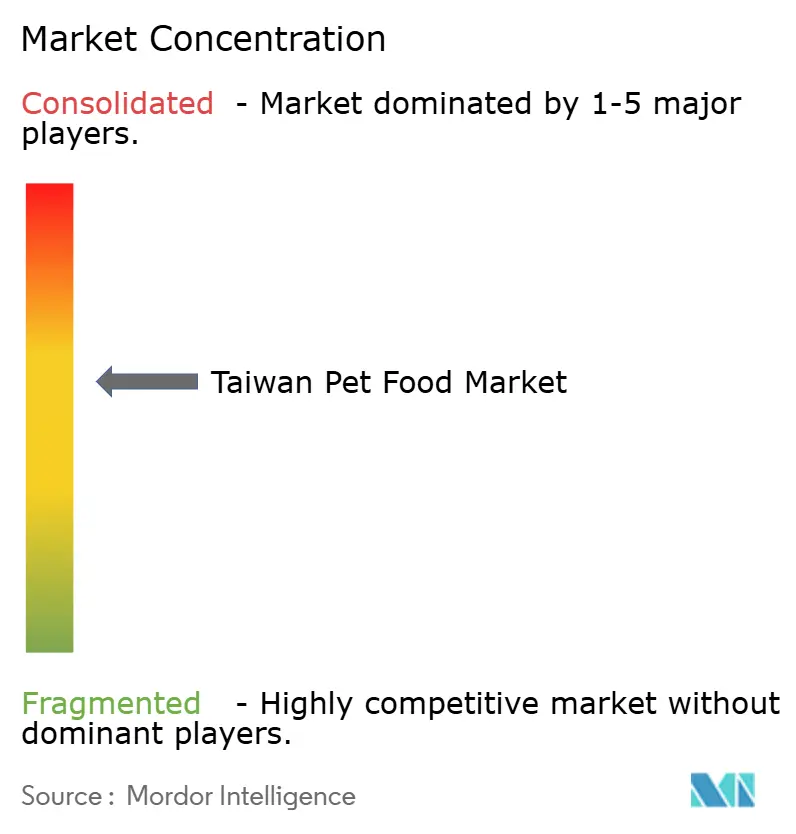

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taiwan Pet Food Market Analysis by Mordor Intelligence

The Taiwan pet food market size was valued at USD 1.09 billion in 2025 and estimated to grow from USD 1.16 billion in 2026 to reach USD 1.56 billion by 2031, at a CAGR of 6.12% during the forecast period (2026-2031). Rising pet ownership in metropolitan apartments, premiumization toward human-grade nutrition, and a rapid migration to digital shopping channels have accelerated demand and reinforced the dominant role of imports in meeting local needs. Thailand and the United States, together accounting for more than half of imports, continue to shape price tiers and brand positioning while domestic manufacturers focus on niche raw and freeze-dried formats that fit premium consumer segments. Regulatory tightening on heavy metals and mycotoxins, implemented in April 2025, is elevating quality expectations and reinforcing the value of strong traceability systems. Competitive intensity remains moderate; the top five brands control a major share of retail sales, yet specialty suppliers still capture growth in function-specific formulations and novel protein diets.[1]Source: Ministry of Agriculture, “2025 Feed Safety Standards Update,” moa.gov.tw

Key Report Takeaways

- By product type, dry pet food held 47.60% of the Taiwan pet food market share in 2025; raw and freeze-dried formats are projected to record the fastest 10.94% CAGR to 2031.

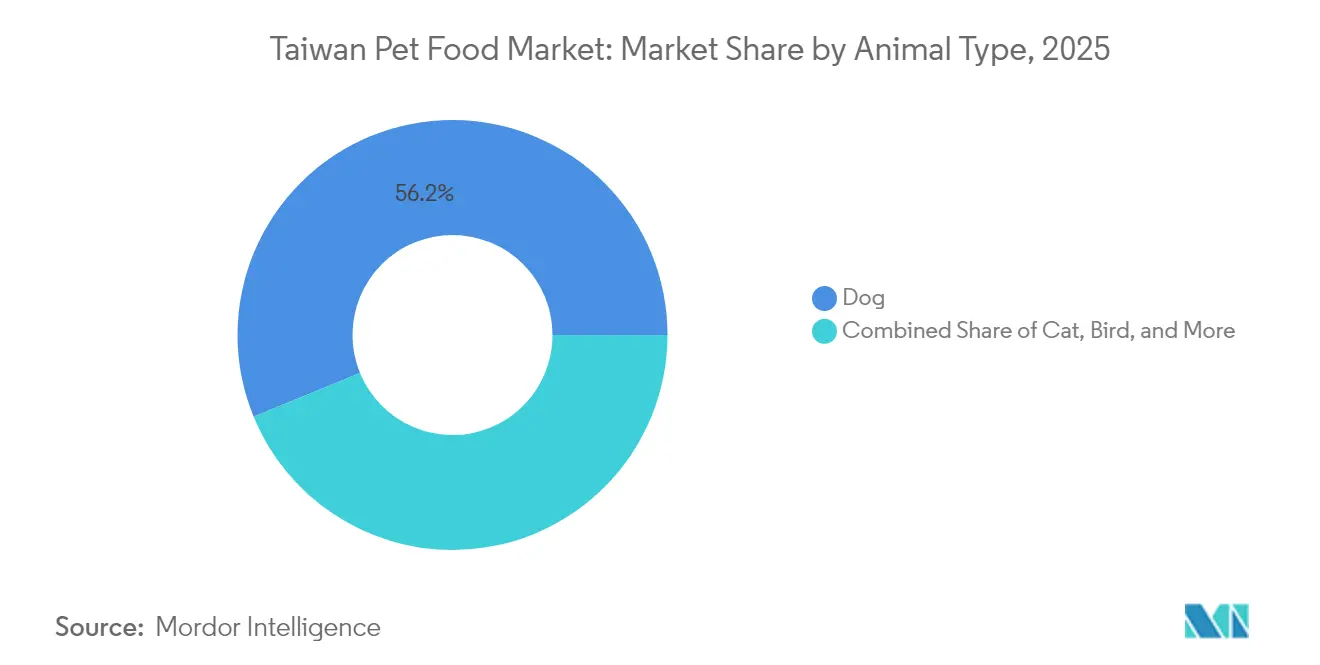

- By animal type, dog captured 56.20% of the Taiwan pet food market size in 2025, while cat nutrition is poised to expand at an 8.67% CAGR through 2031.

- By ingredient type, animal-derived proteins retained a 53.40% share in 2025; novel and insect proteins are forecast to rise at a 13.28% CAGR by 2031.

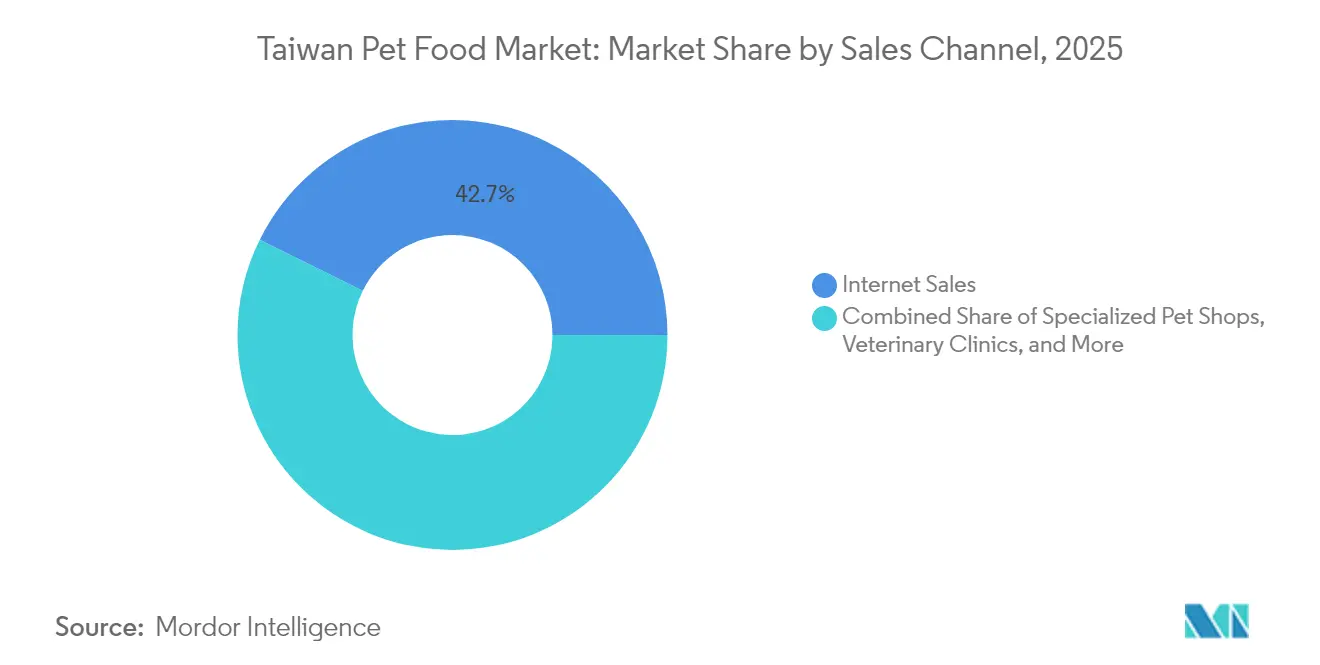

- By sales channel, internet platforms accounted for a 42.70% share in 2025, and veterinary clinics are advancing at a 10.37% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Taiwan Pet Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet ownership density in urban apartments | +1.2% | Taiwan metropolitan areas, with concentration in Taipei, New Taipei, Taichung | Medium term (2-4 years) |

| Premiumization: human-grade, functional and limited-ingredient formulas | +1.8% | Taiwan-wide, with higher adoption in urban centers | Long term (≥ 4 years) |

| Rapid shift to online and omnichannel fulfillment | +1.4% | Taiwan national, with early gains in Taipei, Kaohsiung, Taichung | Short term (≤ 2 years) |

| Expansion of pet insurance boosting spend per pet | +0.6% | Taiwan urban markets, limited rural penetration | Long term (≥ 4 years) |

| Growth of niche exotic-pet segment | +0.4% | Taiwan specialty retail channels, concentrated in major cities | Medium term (2-4 years) |

| Corporate ESG mandates favoring sustainable packaging | +0.3% | Taiwan retail chains and multinational suppliers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Ownership Density in Urban Apartments

Single-person households and aging residents increasingly acquire companion animals, lifting demand for smaller-breed dog and indoor-cat nutrition. Taiwan’s Ministry of the Interior counted 9.3 million households in May 2024, with seniors comprising 18.71% of the population.[2]Source: Ministry of the Interior, “Household Registration Statistics May 2024,” moi.gov.tw A government-run digital registration system logged 94,544 dogs and 137,652 cats in 2024, yet market estimates show more than 1.48 million dogs and 1.31 million cats, underscoring expansion headroom as registration compliance improves. Urban apartment living translates to portion-controlled, odor-moderate diets that favor premium kibble and high-protein wet formulas. Pets increasingly receive “family member” status, reinforcing sustained willingness to pay for veterinary-endorsed and function-specific products.

Premiumization: Human-Grade, Functional and Limited-Ingredient Formulas

Human-grade ingredient sourcing, probiotic inclusion, and limited-ingredient claims are reshaping the premium landscape. The Taiwan Food and Drug Administration’s July 2024 guidance requires scientific substantiation for any physiological or medical claims, rewarding brands that invest in clinical validation.[3]Source: Taiwan Food and Drug Administration, “Guidance on Functional Claims,” fda.gov.tw Average annual spending per pet owner reached TWD 28,081 (USD 891) in 2024, supported by an accessible network of nearly 4,000 small-animal veterinarians. Products addressing digestive health, skin sensitivities, urinary care, and joint mobility continue to earn shelf space, especially within veterinary and specialty e-commerce platforms.

Rapid Shift to Online and Omnichannel Fulfillment

E-commerce generated around 40% of 2024 pet food receipts, propelled by free delivery and bulk discounts that offset the weight of kibble shipments. Uni-President Enterprises’ acquisition of Yahoo Taiwan bonds and a stake in PChome created an integrated omnichannel ecosystem that leverages 7-Eleven’s 45 logistics hubs for convenient pickup and returns. Social-commerce and livestream-based selling are already growing, allowing brands to demonstrate texture, palatability, and feeding outcomes in real time. Rising complaint volumes on leading marketplaces highlight service gaps and opportunities for differentiation through reliable delivery and transparent after-sales support.

Expansion of Pet Insurance Boosting Spend Per Pet

Regulators and insurers are collaborating on broader pet insurance coverage beyond the 252 working dogs presently insured. The Ministry of Agriculture and the Financial Supervisory Commission have invited private insurers to launch consumer products, with Nan Shan General Insurance among the first expressing interest. Taiwan’s veterinarian-to-animal ratio of about 1:575 supports insurance-driven growth in therapeutic diets, particularly renal, weight-management, and hypoallergenic formulations supplied by Hill’s, Royal Canin, and Purina Pro Plan.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price elasticity amid slowing real wage growth | -1.1% | Rural communities and lower-income urban districts | Short term (≤ 2 years) |

| Stringent TFDA additive and labeling enforcement | -0.8% | Importers and domestic processors nationwide | Medium term (2-4 years) |

| Over-reliance on imported ingredients with currency risk | -0.6% | Entire supply chain, especially protein imports | Short term (≤ 2 years) |

| Capacity bottlenecks in domestic freeze-drying lines | -0.4% | Premium raw segment manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Price Elasticity Amid Slowing Real Wage Growth

Premium diets can cost more than ten times the price of entry-level kibble, exposing the Taiwan pet food market to down-trading when real wage growth slows. Heavy reliance on imported inputs also transmits currency fluctuations and commodity cost spikes. Hypermarkets respond with frequent promotions on Thai brands, while specialty retailers report basket-mix shifts toward mid-tier offerings during economic stress.

Stringent TFDA Additive And Labeling Enforcement

Taiwan's regulatory environment has intensified significantly with the Ministry of Agriculture's implementation of expanded mycotoxin controls and reduced heavy metal limits, creating compliance challenges for importers and domestic manufacturers. The new standards, effective 2025, establish tolerance levels for five additional mycotoxins, including vomitoxin at 2 ppm for dog food and 5 ppm for cat food, fumonisin at 5 ppm, zearalenone at 0.2 ppm, ochratoxin at 0.01 ppm, and T-2 mycotoxin at 0.05 ppm for cat food. Simultaneously, mercury limits were reduced from 0.4 ppm to 0.3 ppm, requiring supply chain adjustments and enhanced testing protocols. The Animal and Plant Health Inspection Agency's enforcement against illegal pet food imports, with fines up to NT$1 million (USD 31,000), particularly targets freeze-dried products containing meat that risk introducing African swine fever. Enhanced testing adds cost and prolongs customs clearance, challenging smaller importers and incentivizing investment in accredited laboratories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dry Kibble Dominates but Raw Formats Accelerate

Dry pet food retained 47.60% of the Taiwan pet food market share in 2025, supported by price competitiveness and shelf stability that appeal to apartment dwellers. The raw and freeze-dried category, though still niche, is forecast to record a 10.94% CAGR, outpacing all other segments due to premium positioning and human-grade ingredient claims. Veterinary diets, expanding at an impressive growth rate, benefit from proposed insurance reimbursements and clinic-based recommendations. Import regulations under the Feed Control Act mandate separate facilities for pet and human food processing, guiding manufacturers toward dedicated production lines and bolstering consumer trust.

Retailers note that the Taiwan pet food market size for raw formats remains constrained by domestic freeze-drying capacity and strict quarantine protocols on foreign meat inputs. Nevertheless, omnichannel players leverage livestream demonstrations to highlight the “whole-food” texture and convenience of rehydration, winning trials among premium customers. Kibble suppliers continue to innovate with coated probiotics and “soft-center” dual-texture pieces to defend share.

By Animal Type: Cat Nutrition Gains Momentum

Dog contributed 56.20% of 2025 sales, but growth is moderating as ownership reaches a mature plateau. Cat is advancing at an 8.67% CAGR, supported by their suitability for compact living spaces and lower exercise demands. The Taiwan pet food market size for feline diets is further lifted by higher protein requirements and specialized taurine supplementation that command premium price points.

Veterinary registration data reveal regional differences: New Taipei City leads clinical density, improving access to therapeutic feline diets. Government deliberations on mandatory cat registration would enhance population visibility and support demand forecasting. Exotic pet diets remain minor but diversify assortments, introducing insect protein snacks and botanical blends shaped for reptiles and birds.

By Ingredient Type: Novel Proteins Expand

Animal-derived proteins furnished 53.40% of 2025 formulations, anchored by chicken and fish meals imported largely from Thailand and the United States. Novel and insect proteins, at 13.28% forecast CAGR, respond to sustainability priorities and allergen-free positioning. Brands market black soldier fly and cricket meals as hypoallergenic, low-carbon options, aligning with corporate ESG mandates. The Taiwan pet food market share of such proteins remains small but visible in specialty e-commerce and premium wet pouches.

Regulators have broadened mycotoxin surveillance, placing extra scrutiny on cereal-based inputs. Suppliers with robust testing protocols and full ingredient disclosure gain procurement preference among leading packers. Fermentation-derived probiotics and postbiotics manufactured domestically add functional depth, reinforcing Taiwan’s biotechnology strengths and reducing import reliance for advanced nutraceuticals.

By Sales Channel: Digital Leads Omnichannel Convergence

Internet platforms generated 42.70% of the 2025 value, aided by free shipping thresholds and subscription discounts. The livestream and social-commerce avenues are anticipated to climb rapidly as pet influencers showcase feeding routines and live Q&A sessions. Specialized pet shops maintain a significant share, essential for premium education and grooming services. Hypermarkets and supermarkets are driving volume through promotions on value brands, while convenience stores are extending 24-hour pickup flexibility for online orders.

Veterinary clinics, representing the fastest growing CAGR at 10.37% but a strategic channel, grow in tandem with therapeutic diet adoption. Complaint statistics from Taipei City underscore the need for service upgrades on major platforms; reliability gaps present an opening for niche sellers emphasizing customer support and traceability. Uni-President’s integrated model illustrates how brick-and-mortar reach combined with strong logistics can defend share against pure-play e-commerce competitors.

Geography Analysis

Northern Taiwan, led by Taipei and New Taipei City, captures the largest share of spending due to higher incomes, dense apartment living, and rapid adoption of premium nutrition. The Taiwan pet food market size in the north benefits from proximity to major ports and import inspection facilities that streamline product flow. Central Taiwan, anchored by Taichung, balances urban demand and suburban affordability, supporting a mixed product portfolio spanning value kibble and functional wet pouches. Southern hubs like Kaohsiung and Tainan display fast growth yet remain price-sensitive, relying on promotions and smaller pack sizes to boost trial.

Veterinary clinic density correlates with market penetration: New Taipei’s 84.3% coverage facilitates access to science-based diets, whereas more rural districts depend on e-commerce for specialty products. Government investment in digital pet registration and potential expansion to cats will furnish granular geographic data, improving supply-chain planning. Island-wide logistics networks operated by convenience chains ensure that even remote communities can receive refrigerated or freeze-dried diets within 24 hours, leveling access disparities.

Rural and smaller urban areas face distinct challenges, including limited specialty retail presence, reduced veterinary access, and higher price sensitivity that favors basic nutrition over premium formulations. These regions benefit from Taiwan's advanced logistics infrastructure and e-commerce penetration that enables access to specialized products previously unavailable through traditional retail channels. The government's digital pet registration system expansion, potentially including mandatory cat registration, could provide enhanced market visibility and regulatory compliance in underserved geographic segments. Island-wide regulatory harmonization under the Taiwan Food and Drug Administration ensures consistent quality standards and import protocols, supporting market integration and brand expansion across geographic boundaries.

Regulatory Landscape

Taiwan regulates pet food mainly through the Ministry of Agriculture (MOA) under the Animal Protection Act framework. Manufacturers, processors, and importers are required to file web-based product records via the MOA Pet Food Reporting System and to report quantities on a quarterly basis. Importers handling animal-origin ingredients also follow Animal and Plant Health Inspection Agency (APHIA) quarantine and inspection requirements, using ingredient- and risk-specific health certification pathways that can extend clearance time and increase documentation needs.

Food safety oversight tightened with the MOA revision of standards for pathogenic microorganisms and health-hazard materials in pet food, which entered into force on April 26, 2025. The update expanded mycotoxin controls (including deoxynivalenol, fumonisins, zearalenone, ochratoxin A, and T-2 toxin) and reduced the mercury limit to 0.3 ppm, raising the bar for supplier qualification, inbound testing, and traceability. The MOA also published testing methods on September 30, 2025 for pathogens, heavy metals, preservatives, antioxidants, harmful chemicals, and nutritional content, supporting more consistent inspection and recall execution across both imported and domestically produced products.

Competitive Landscape

Taiwan's pet food market exhibits moderate consolidation, with the top 5 companies controlling maximum market share, creating a competitive environment that balances multinational scale advantages with opportunities for specialized players. Mars Inc. leads with a significant share through its Royal Canin, Pedigree, and Whiskas brands, leveraging global supply chain efficiencies and veterinary channel relationships, while Nestlé Purina PetCare captures a prominent share across multiple price tiers from Purina ONE to Fancy Feast and Friskies. The competitive intensity reflects Taiwan's import-dependent market structure, where international suppliers compete on brand positioning, distribution channel access, and regulatory compliance capabilities rather than manufacturing cost advantages.

Strategic patterns reveal distinct channel specialization, with premium brands like Hill's Science Diet dominating veterinary clinics through science-based positioning and professional endorsement, while Thai suppliers focus on hypermarket distribution with competitive pricing strategies. Colgate-Palmolive Company (Hill’s Pet Nutrition) recent strategic moves, including the USD 700 million acquisition of three Red Collar Pet Foods plants and the expansion of canned food production capacity in Kansas, demonstrate a commitment to vertical integration and supply chain control. White-space opportunities exist in the rapidly growing raw and freeze-dried segment, where capacity constraints limit domestic production and create openings for international suppliers with established processing capabilities.

Technology adoption for market share gains includes Hill's digital-first packaging redesign and e-commerce optimization strategies that serve as models for parent company Colgate-Palmolive Company (Hill’s Pet Nutrition) broader portfolio applications. The regulatory environment under Taiwan's Feed Control Act requires comprehensive traceability systems and manufacturing facility separation from human food production, creating barriers to entry that favor established players with compliance infrastructure while potentially limiting new market entrants.

Taiwan Pet Food Industry Leaders

Mars Inc.

Nestlé Purina PetCare

Colgate-Palmolive Company (Hill’s Pet Nutrition)

General Mills Inc. (Blue Buffalo)

Yoda Pet Food Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Stricter safety thresholds and more formalized test methods are increasing the value of verifiable quality systems. This creates whitespace for brands and suppliers that can demonstrate compliance across mycotoxins and heavy metals, including the 0.3 ppm mercury limit effective from April 2025, and can sustain documentation through the MOA product-record and quarterly reporting processes. The environment supports differentiated propositions in premium, limited-ingredient, and function-led diets where labeling discipline and substantiation matter, and it also encourages growth in accredited laboratory services and import compliance expertise for smaller players managing APHIA quarantine documentation and inspection readiness.

Import reliance is still a structural feature, but domestic capacity additions are increasingly relevant for shortening lead times and improving control over ingredient sourcing and batch traceability. One example is the new pet food manufacturing facility inaugurated by Cat in Love in April 2026 at the Pingtung Agricultural Biotechnology Park, equipped with automated mixing, drying, grinding, and coating systems. In parallel, Taiwan's heavy use of digital commerce continues to provide a clear route to market for specialty and therapeutic portfolios, particularly where brands can pair online scale with compliant labeling, stable supply, and consistent after-sales handling for repeat purchases.

Recent Industry Developments

- April 2026: Cat in Love inaugurated a new pet food manufacturing facility in the Pingtung Agricultural Biotechnology Park, adding automated mixing, drying, grinding, and coating capabilities. The investment strengthens domestic supply options in a market where imports play a dominant role, and it supports faster replenishment cycles and tighter batch-level traceability for premium formulations.

- February 2025: Colgate-Palmolive announced the acquisition of Care TopCo Pty Ltd (Prime100), expanding Hill's Pet Nutrition into fresh pet food with refrigerated and shelf-stable, veterinarian-endorsed dog food offerings. The acquisition broadens the premium portfolio that can be marketed through Taiwan's veterinary and specialty channels, where therapeutic and function-led claims face closer scrutiny.

- August 2024: Taiwan's Ministry of Agriculture recalled four types of cat and dog snacks due to salmonella contamination and mercury exceedances, affecting Simple Sense, Fuzzywuzzycare, Mao Siao San, and Cat Pool products. The action reinforced enforcement momentum around contaminant controls and raised the operational importance of supplier qualification, inbound testing, and rapid recall execution for brands selling through both e-commerce and physical retail.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is sized as the value of commercially prepared pet food sold in Taiwan across retail and veterinary-led channels, covering everyday feeding and specialized nutrition products that are packaged and marketed as pet food.

Scope exclusions: It does not count pet medicines, veterinary services, grooming, accessories, and other non-food pet care items.

Segmentation Overview

- By Product Type

- Dry Pet Food (Kibble)

- Wet Pet Food

- Veterinary Diets

- Treats and Snacks

- Raw and Freeze-Dried

- Other Product Types

- By Animal Type

- Dog

- Cat

- Bird

- Fish and Reptile

- Small Mammal

- By Ingredient Type

- Animal-Derived Proteins

- Plant-Derived Proteins

- Cereals and Derivatives

- Novel and Insect Proteins

- Other Ingredient Types

- By Sales Channel

- Specialized Pet Shops

- Veterinary Clinics

- Internet Sales

- Hypermarkets and Supermarkets

- Convenience Stores

- Other Channels (Department Stores, Home-delivery, etc.)

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the demand pool and to make sure inputs like Taiwan pet ownership and trade flows are directionally correct before modeling starts. We typically refer to public statistics and official publications such as Taiwan government agriculture and statistics releases, customs and trade statistics, UN Comtrade, and FAOSTAT, which help validate import dependence and category movement over time.

To tighten assumptions around format mix and channel shifts, we also review sources such as association and event pages for the Taiwan pet industry, peer-reviewed nutrition and veterinary journals for diet adoption cues, and company filings and investor presentations for category commentary. Where needed, paid subscriptions that cover company financials, news, patents, and shipment-level import and export records are used to cross-check totals and remove obvious gaps. These sources are illustrative, and many other public and subscription sources were also used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work was used to confirm what is really sold as pet food in Taiwan and how pricing and volumes move across channels, especially for veterinary diets and treats. We spoke with a mix of manufacturers, importers, distributors, specialty retail and online participants, and industry experts, then checked the inputs against the main consumer demand centers within Taiwan.

Distribution of primary research fieldwork respondents

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 15% | APAC: 41% |

| Mid tier: 48% | Functional/Unit leaders: 27% | EMEA: 37% |

| Smaller Players: 15% | Managers: 58% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where household pet counts and feeding incidence are translated into an addressable consumption pool, which is then valued using observed price bands by format and channel. The results are then corroborated with selective bottom-up approximations, including sampled brand and channel price checks, distributor feedback on throughput, and imported-product share signals to adjust totals where the first pass looks overstated or understated.

Key inputs that shape the model include dog and cat population trends, the share of pets on commercial diets versus home feeding, mix shifts between dry food, wet food, treats and snacks, and veterinary diet adoption for common health needs. We also track import values and category movement as a reality check, since a meaningful part of Taiwan supply is imported, which helps reconcile value growth with volume and pricing. For forecasting, scenario analysis is used, where baseline demand growth is linked to pet population, premiumization, and channel shift assumptions, and the price path is reviewed with interview feedback before the final curve is locked.

Data Validation & Update Cycle

Outputs are checked through triangulation across independent signals such as trade trends, pet population indicators, and observed shelf pricing, and then variances are investigated before sign-off. When a jump is seen in a category like veterinary diets or treats, the assumptions are reopened and the team re-contacts relevant interviewees to confirm what changed and whether it is temporary.

Each report is refreshed annually, and interim updates are made when material events affect pricing, supply, or regulation. Before delivery, a final analyst pass is completed so clients receive an updated view that matches the latest available public releases and market feedback.

Mordor Intelligence's Taiwan Pet Food Market Sizing Compared With Other Published Estimates

Published estimates for Taiwan pet food can look different because the counted product basket and the pricing logic are not always the same across sources. Gaps usually come from whether treats, veterinary diets, and newer formats are included, how online pricing is blended with offline pricing, and which year is treated as the reference point.

The main gap comes from whether veterinary diets and treats are counted as part of pet food and then priced using Taiwan channel-weighted averages, where Mordor Intelligence includes these formats only when they are sold as packaged pet food through defined retail and veterinary sales channels.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.09 B (2025) | |

| Global Consultancy A | USD 0.94 B (2025) | Often narrows the basket to core dry and wet food, and it may treat veterinary diets as pharmaceuticals, which reduces the counted value in premium-heavy categories. |

| Trade Journal B | USD 1.28 B (2024) | Can blend broader pet product retail value with pet food, or apply aggressive average selling price uplift from premiumization without aligning it to channel mix and import-value checks. |

Across the three figures, the spread is mostly explained by what gets classified as pet food and how price is translated from shelf signals into an all-market average. By keeping the scope tied to clearly defined pet food formats and then validating value movement with trade and channel cues, the final number stays traceable to inputs that can be rechecked and updated each year.

Key Questions Answered in the Report

How large is the Taiwan pet food market in 2026?

It reached USD 1.16 billion in 2026 and is forecast to grow at a 6.12% CAGR to 2031.

Which product type leads sales?

Dry pet food holds 47.60% of 2025 value, supported by convenience and competitive pricing.

What segment is growing fastest?

Raw and freeze-dried diets are projected to expand at a 10.94% CAGR through 2031.

How important is e-commerce?

Internet sales already contribute 42.70% of spending and continue to gain share via social-commerce and omnichannel models.

Page last updated on: