Adhesive Tapes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

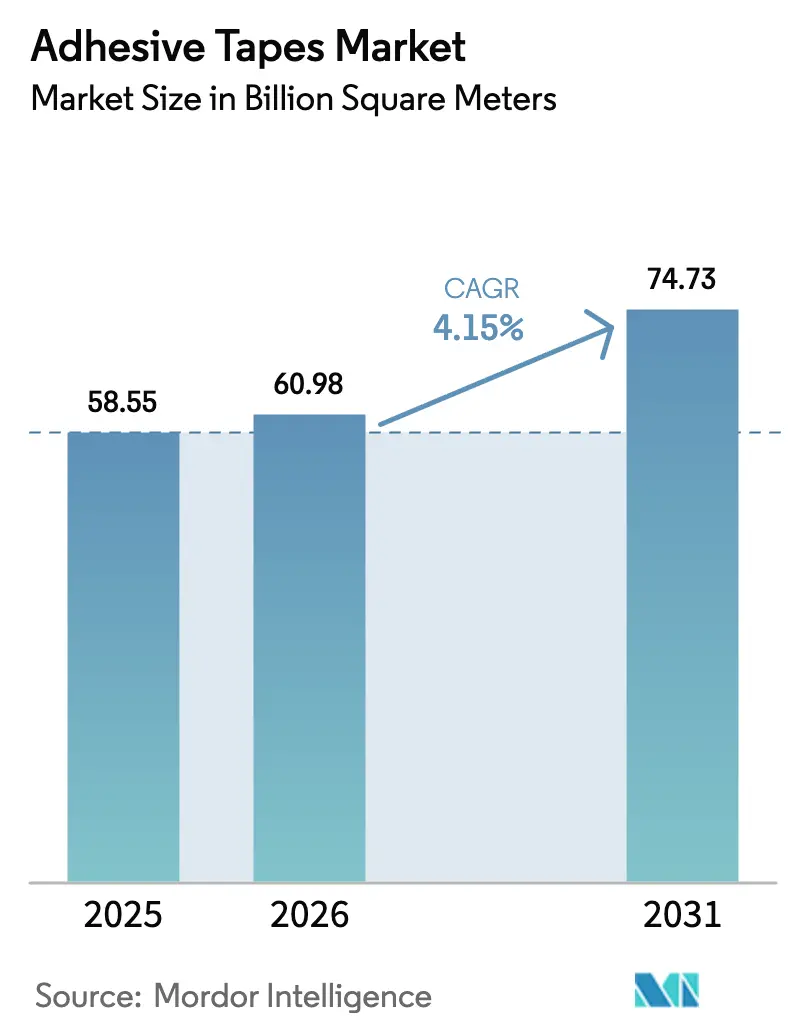

| Market Volume (2026) | 60.98 Billion square meters |

| Market Volume (2031) | 74.73 Billion square meters |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Adhesive Tapes Market Analysis by Mordor Intelligence

The Adhesive Tapes Market size is expected to grow from 58.55 Billion square meters in 2025 to 60.98 Billion square meters in 2026 and is forecast to reach 74.73 Billion square meters by 2031 at 4.15% CAGR over 2026-2031. This performance mirrors structural shifts—most notably e-commerce automation, vehicle electrification, and electronics miniaturization—that are redefining tape specifications and usage intensity. Fulfillment centers now run pressure-sensitive carton-sealing lines at more than 60 cartons per minute, which has multiplied demand for instant-tack, tamper-evident closures across North America, Europe, and Asia. OEMs are simultaneously replacing heavier PVC harness wraps with acrylic-backed cloth tapes that shave weight from each vehicle to meet fleet-average fuel-efficiency targets. On the formulation side, water-based and PFAS-free chemistries are gaining share as regulators tighten VOC and fluorochemical limits, while converters accelerate patent filings for conductive, stretchable, and bio-based systems that bring functional integration to commodity formats.

Key Report Takeaways

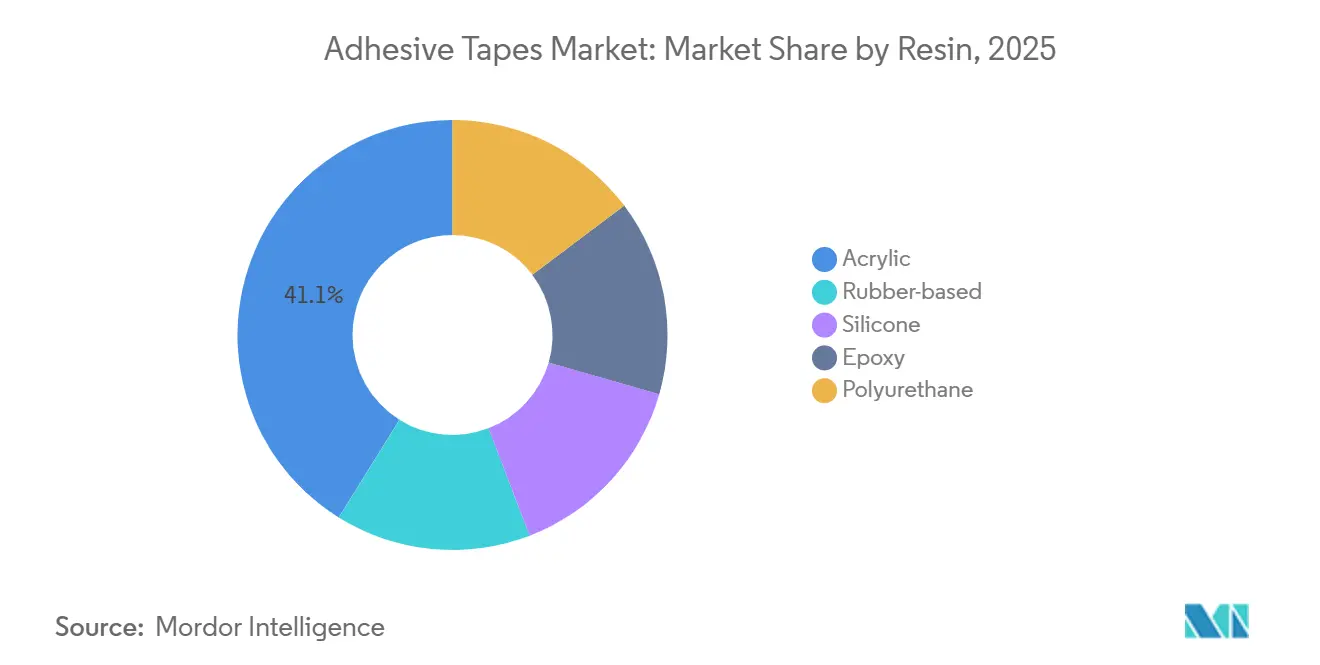

- By resin, acrylic led with 41.12% of 2025 volume, while rubber-based systems are advancing at a 4.29% CAGR through 2031.

- By technology, water-based chemistry captured a 45.19% share in 2025 and is forecast to post the fastest 4.51% CAGR.

- By product type, pressure-sensitive tapes held 61.12% share in 2025; heat-sensitive variants are pacing the category with a 4.58% CAGR.

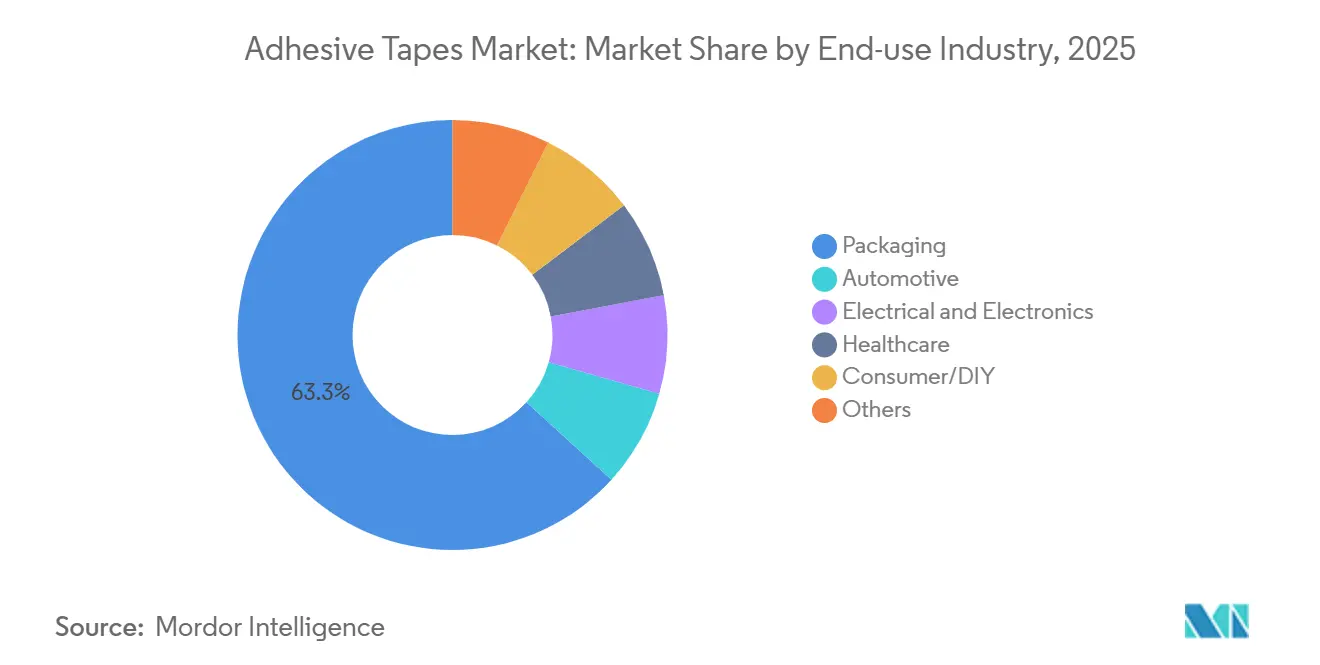

- By end use, packaging accounted for 63.26% of 2025 consumption, whereas healthcare is projected to grow at a 4.67% CAGR to 2031.

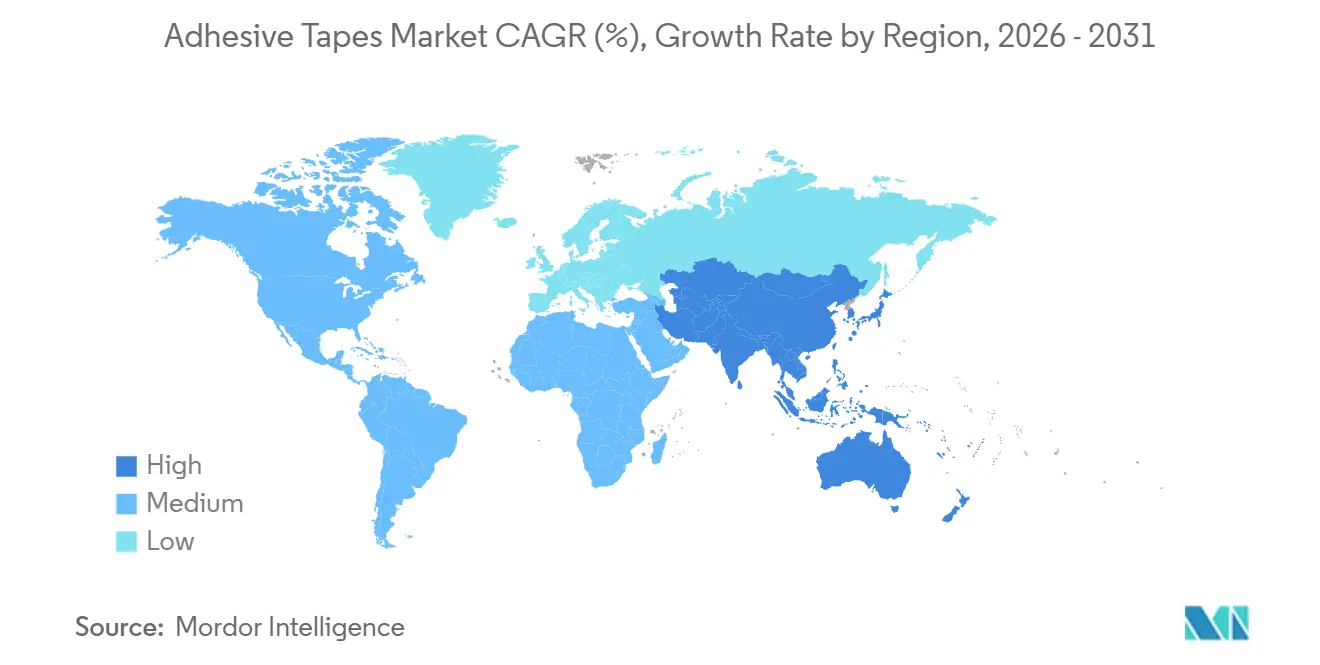

- By geography, Asia-Pacific dominated with a 58.91% share in 2025 and is set to expand at a 5.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Adhesive Tapes Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce packaging boom boosting adhesive tapes demand | +0.9% | Global, with concentration in North America, Europe, China, India | Medium term (2-4 years) |

| OEM shift to lightweight wire-harness tapes | +0.7% | APAC core (China, Japan, South Korea), spill-over to North America and Europe | Long term (≥ 4 years) |

| Wearable and flexible electronics adoption increasing tapes usage | +0.6% | Global, led by North America, Japan, South Korea | Medium term (2-4 years) |

| Construction boom in ASEAN and the Middle East boosting adhesive tape usage | +0.8% | ASEAN (Vietnam, Malaysia, Thailand), Middle East (Saudi Arabia, UAE, Qatar) | Short term (≤ 2 years) |

| EV battery-pack thermal/EMI tape integration | +0.5% | China, Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce Packaging Boom Boosting Adhesive Tapes Demand

Fulfillment giants like Amazon consumed significant volumes of pressure-sensitive packaging tape in 2025, a volume much higher than that of traditional retail distribution. Branded pre-printed rolls saw strong year-on-year growth, as converters reduced minimum order quantities to levels that empowered smaller sellers to utilize both tamper-evident and marketing features in a single closure. Legislative bodies are influencing material choices; for instance, the European Union's waste-packaging regulations favor water-activated kraft tapes, which are less likely to contaminate fiber recycling streams. Meanwhile, in humid logistics hubs across India and Southeast Asia, there is a shift towards synthetic-rubber hot-melt tapes. These tapes maintain tack at relative humidity above 80%, ensuring cartons are sealed without adhesive bleed. Collectively, these dynamics are not only increasing the penetration of carton-sealing tape in each shipped parcel but also bolstering the long-term growth of the adhesive tapes market.

OEM Shift to Lightweight Wire-Harness Tapes

Automakers are turning to acrylic cloth tapes, which are lighter than traditional PVC electrical wraps but offer the same dielectric strength. This switch results in a weight reduction per vehicle, translating to significant savings. These savings are crucial as they help automakers sidestep penalties for excess CO₂, in compliance with EU fleet regulations. Tesla’s Model Y, a testament to this trend, incorporates the new tape in its harness. In 2025, Japanese suppliers introduced flame-retardant polyester tapes that not only meet the stringent ISO 6722 Class D abrasion resistance standards but also do so without halogens, ensuring alignment with recyclability mandates. In 2025, China rolled out new-energy vehicles, each requiring harness tapes. This demand surge is attributed to battery platforms accommodating more cables than their combustion counterparts. The automotive industry's focus on lightweighting and safety propels the adhesive tapes market forward in automotive wiring.

Wearable and Flexible Electronics Adoption Increasing Tapes Usage

In 2025, Abbott shipped its FreeStyle Libre 3 glucose monitors. Each monitor utilized a medical-grade acrylic tape, designed to adhere for 14 days and successfully passed ISO 10993 tests. Foldable OLED displays required optically clear adhesive tape, boasting a haze level below 1% and proven durability for multiple fold cycles. In early 2025, the FDA granted clearance to Avery Dennison’s MED 5610 silicone tape, unlocking a lucrative opportunity in the wearable-pump market. Furthermore, patent filings for stretchable conductive adhesives saw a notable increase, highlighting a shift towards functional and skin-compatible bonding solutions. Such advancements firmly establish healthcare and consumer electronics as burgeoning leaders in the adhesive tapes market.

Construction Boom in ASEAN and Middle East Region Boosting Adhesive Tape Usage

In 2025, Saudi Arabia's ambitious NEOM project mandated the use of aluminum-foil acrylic tapes for its modular wall insulation, spurring additional demand. Meanwhile, Malaysia's East Coast Rail Link opted for halogen-free polyester harness tapes, ensuring compliance with the IEC 60332-3 fire safety standards. In Vietnam, a surge in manufacturing FDI heightened the demand for clean-room masking tapes, specifically those with particle counts under 100 per cubic foot. In Dubai, work on the Creek Tower resumed in 2025, utilizing high-bond acrylic foam tapes. These tapes not only replaced traditional mechanical fasteners but also slashed façade labor requirements. Such fast-tracked infrastructure projects are propelling a notable uptick in the regional adhesive tapes market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petro-derived raw-material price volatility | -0.6% | Global, acute in regions dependent on imported feedstocks | Short term (≤ 2 years) |

| VOC and hazardous-solvent regulations | -0.4% | North America, Europe, South Korea, Japan | Medium term (2-4 years) |

| PFAS-free reformulation disrupting fluoropolymer tapes | -0.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Petro-Derived Raw-Material Price Volatility

Between 2024 and 2025, acrylic acid spot prices fluctuated significantly, which in turn squeezed converter margins. Butadiene prices were influenced by supply constraints due to cracker maintenance. A 2025 report from Henkel highlighted that raw-material inflation contributed to increased costs. However, this was somewhat mitigated by a reduction in acrylic polymer loadings. The exit of smaller converters from commodity segments, due to feedstock volatility and without hedging, underscores the challenges in short-term expansion within the adhesive tapes market.

VOC and Hazardous-Solvent Regulations

California’s South Coast district lowered the VOC cap for pressure-sensitive adhesives, compelling a reformulation of toluene-based duct and masking tapes[1]South Coast Air Quality Management District, “Rule 1168 Amendments,” aqmd.gov. The EU added N-methyl-2-pyrrolidone to the REACH Candidate List, triggering a phase-out in coating lines. South Korea ordered VOC cuts at adhesive plants, prompting investments in thermal oxidizers or shifts to hot-melt lines. These mandates accelerate technology migration yet raise compliance costs, tightening near-term margins across the adhesive tapes market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin: Rubber-Based Formulations Secure Fastest Growth

Rubber-based chemistries are projected to compound at 4.29% between 2026 and 2031, the highest rate in the resin spectrum, even though acrylic maintained 41.12% adhesive tapes market share in 2025. For high-speed logistics, natural and styrene-butadiene rubbers are crucial, achieving instant tack even on dusty surfaces. On the other hand, silicone resins, though smaller in volume than acrylic and rubber-based systems, are favored in the medical field and for high-temperature applications, prioritizing clarity and biocompatibility over cost. There's also a rising interest in epoxy-based structural tapes, a niche known for providing high shear strength, making them ideal for aerospace applications and wind blades. While bio-based tall-oil and soy chemistries face a hurdle with cost premiums, pilot projects suggest a potential gradual market entry in the coming years.

Acrylic continues to own premium automotive and electronics slots thanks to UV stability and low outgassing, anchoring its large slice of the adhesive tapes market. Still, price-sensitive sectors lean toward rubber formulations that tolerate irregular cartons and dusty worksites. Silicone approvals for 30-day skin contact under ISO 10993-10 protocols widen medical use cases, while reactive polyurethane hot-melts bridge processing ease and structural strength in flexible packaging. Collectively, resin diversification supports steady value creation even as commodity pricing stays volatile.

By Technology: Water-Based Lines Accelerate Under Regulatory Tailwinds

Water-based technology held 45.19% of the 2025 volume and is forecast to clock the fastest 4.51% CAGR, reflecting tightening VOC norms and brand sustainability pledges. Modern acrylic emulsions now match solvent grades on peel and shear at lower coat weights, enabling converters to shut down solvent ovens and cut energy use. Ultra-fast packaging lines favor hot-melt systems due to their instant bonding capabilities. When factoring in energy costs, these systems prove to be more economical than their water-based counterparts. Meanwhile, solvent-based technology continues to dominate the automotive and aerospace sectors. Here, the emphasis on drying speed and low-surface-energy adhesion outweighs any regulatory challenges.

Reactive platforms—UV-curable acrylics and moisture-cure polyurethanes—collect a small share yet command premium prices in electronics and medical devices. Hybrids that co-package water-based carriers with UV crosslinkers are emerging, promising one-part processing with structural final properties. As these camps converge, the total adhesive tapes market size attached to water-based and hot-melt lines will expand most rapidly across the forecast window.

By Product Type: Heat-Sensitive Tapes Ride Electronics Miniaturization

Pressure-sensitive formats contributed 61.12% of the 2025 volume, yet heat-sensitive tapes are poised for a 4.58% CAGR, the best among product types. Thermally activated bonding eliminates liquid adhesives in flexible circuit assembly and wafer processing, reducing contamination risk. Water-activated kraft tapes enjoy renewed traction in e-commerce because they integrate with paper recycling loops. Specialty constructions—conductive, magnetic, and optically clear—are small in tonnage but vital for high-value electronics and 5G infrastructure.

Nitto’s Revalpha heat-release line underscores how debond-on-demand designs shorten semiconductor tool time. Rogers Corporation’s 6 W/m-K silicone tape underpins 5G power amplifiers, evidencing functional integration over classical bonding. The adhesive tapes market size for such specialty categories is still modest, yet it climbs faster than commodity segments as miniaturization intensifies.

By End-Use Industry: Healthcare Emerges as Fastest-Growing Consumer

Packaging consumed 63.26% of 2025 tonnage, driven by global parcel growth and automation intensity, but healthcare is set to outpace all categories at a 4.67% CAGR to 2031. Each continuous glucose monitor uses about 0.15 m² of medical-grade tape per 14-day sensor. Automotive uses pivot from emblem mounting to wire-harness bundling and battery-module bonding as electrification reshapes material bills. Electrical and electronics segments expand on 5G rollout and data-center construction, boosting demand for thermal-management and EMI-shielding tapes.

Consumer DIY and building-and-construction applications add steady, region-specific volume. In each vertical, commoditized carton-sealing tapes yield slim margins, while medical wearables and EV battery packs allow increased price realization, underscoring how end-use mix lifts average revenue in the adhesive tapes market.

Geography Analysis

Asia-Pacific held 58.91% of global volume in 2025 and is projected to expand at a 5.15% CAGR, the fastest of any region. China, a significant player, saw major demand driven by the provinces of Guangdong, Jiangsu, and Zhejiang—home to major electronics clusters and auto hubs. Meanwhile, India's market witnessed robust growth, fueled by a strong vehicle output and a booming e-commerce sector, leading to a surge in carton-sealing tape usage[2]Society of Indian Automobile Manufacturers, “Production Statistics 2025,” siam.in.

Japan continues to spearhead the market for optical and semiconductor tapes, exporting premium rolls throughout East Asia. South Korea's demand, closely tied to the display fabs of Samsung and LG, remained significant for specialty tapes. ASEAN countries, notably Vietnam, Thailand, and Malaysia, experienced strong annual growth as foreign direct investment shifted assembly lines from China, solidifying the region's dominance in the adhesive tapes market.

North America accounted for a notable share of global consumption in 2025, buoyed by the rise of electric vehicle production and a surge in parcel logistics, even as traditional packaging faced maturity. Europe adapted to recycling mandates, transitioning from PP-backed tapes to kraft paper alternatives in mono-material laminates. South America saw Brazil's robust automotive sector driving demand, albeit constrained by Argentina's currency challenges, limiting imports. The Middle East and Africa reaped benefits from mega projects in Saudi Arabia and the UAE, alongside South Africa's automotive output, maintaining a steady medium-term growth rate.

Competitive Landscape

The adhesive tapes market remains fragmented. Strategic focus has moved from square-meter capacity to formulation science. Incumbents funnel research and development toward PFAS-free fluoropolymers and low-VOC water-based emulsions, while smaller players gain packaging share with short-run, pre-printed rolls that bypass distributors. Digital printing speeds on-demand branding, and sensor-embedded tapes introduce track-and-trace without separate RFID tags. Emerging startups pursue reversible adhesives that debond via heat or light, aligning with circular-economy goals in electronics remanufacturing. Competitive intensity is highest in commodity cartons, where Chinese plants run at low margins. ISO 9001 and 14001 compliance is now standard; UL 94, FDA 21 CFR 175.105, and IEC 60454 approvals act as entry gates in regulated sectors, consolidating premium pockets within the adhesive tapes market.

Adhesive Tapes Industry Leaders

3M

tesa SE – A Beiersdorf Company

Nitto Denko Corporation

Avery Dennison Corporation

LINTEC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Avery Dennison Performance Tapes has introduced an innovative Solar Panel Bonding Portfolio featuring pressure-sensitive adhesive (PSA) tapes. This offering delivers significant advantages to solar panel manufacturers over traditional bonding methods.

- November 2024: tesa has established new offices in Mumbai and Bengaluru to strengthen its presence in India's manufacturing sector and advance its growth strategy in the Asia-Pacific region. This expansion is expected to positively influence the adhesive tapes market by enhancing accessibility and fostering regional innovation.

Global Adhesive Tapes Market Report Scope

Adhesive tapes are a combination of a base material and an adhesive film that bonds and fastens two objects together instead of bolts or welding.

The market is segmented based on resin, technology, product type, end-user industry, and geography. By resin, the market is segmented into acrylic, rubber-based, silicone, epoxy, and polyurethane. By technology, the market is segmented into water-based, solvent-based, hot-melt, and reactive. By product type, the market is segmented into pressure-sensitive tapes, water-activated tapes, heat-sensitive tapes, and specialty tapes. By end-use industry, the market is segmented into packaging, automotive, electrical and electronics, healthcare, consumer/DIY, and others (including building and construction). The report also covers the market size and forecasts for adhesive tapes in 16 countries across major regions. For each segment, the market sizing and forecasts have been done based on volume (square meters).

| Acrylic |

| Rubber-based |

| Silicone |

| Epoxy |

| Polyurethane |

| Water-based |

| Solvent-based |

| Hot-melt |

| Reactive |

| Pressure-Sensitive Tapes |

| Water-Activated Tapes |

| Heat-Sensitive Tapes |

| Specialty Tapes |

| Packaging |

| Automotive |

| Electrical and Electronics |

| Healthcare |

| Consumer/DIY |

| Others (Building and Construction, etc.) |

| Asia-Pacifc | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Resin | Acrylic | |

| Rubber-based | ||

| Silicone | ||

| Epoxy | ||

| Polyurethane | ||

| By Technology | Water-based | |

| Solvent-based | ||

| Hot-melt | ||

| Reactive | ||

| By Product Type | Pressure-Sensitive Tapes | |

| Water-Activated Tapes | ||

| Heat-Sensitive Tapes | ||

| Specialty Tapes | ||

| By End-use Industry | Packaging | |

| Automotive | ||

| Electrical and Electronics | ||

| Healthcare | ||

| Consumer/DIY | ||

| Others (Building and Construction, etc.) | ||

| By Geography | Asia-Pacifc | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected volume for the adhesive tapes market in 2031?

The adhesive tapes market is forecast to reach 74.73 billion square meters by 2031 from 60.98 billion square meters in 2026, registering a CAGR of 4.15%.

Which region leads demand growth?

Asia-Pacific tops both share and growth, holding 58.91% of 2025 volume and expanding at a 5.15% CAGR.

Which product category is growing fastest?

Heat-sensitive tapes are the fastest, advancing at a 4.58% CAGR through 2031.

How are VOC rules shaping technology choices?

Tightened VOC limits are steering converters from solvent-based lines toward water-based and hot-melt systems.

Why is healthcare an attractive end use?

Wearable glucose monitors and drug-delivery patches need skin-friendly tapes, driving healthcare demand at a 4.67% CAGR.

Page last updated on: