Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

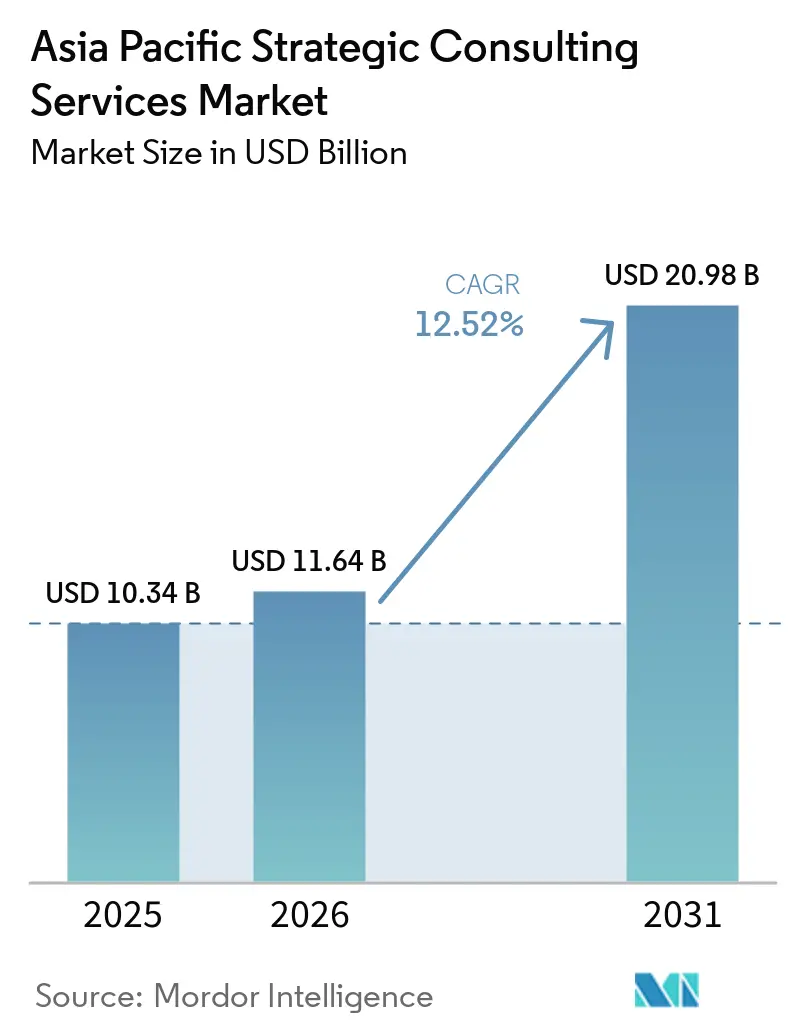

| Base Year Market Size (2025) | USD 10.34 Billion |

| Market Size (2026) | USD 11.64 Billion |

| Market Size (2031) | USD 20.98 Billion |

| Growth Rate (2026 - 2031) | 12.52% CAGR |

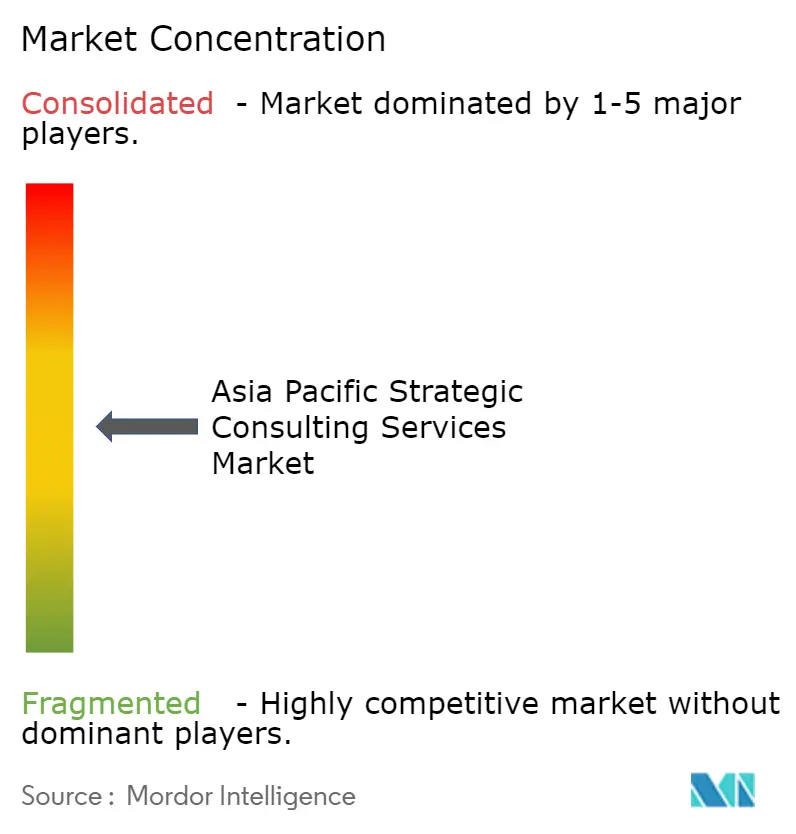

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Strategic Consulting Services Market Analysis by Mordor Intelligence

Asia Pacific strategic consulting services market size in 2026 is estimated at USD 11.64 billion, growing from 2025 value of USD 10.34 billion with 2031 projections showing USD 20.98 billion, growing at 12.52% CAGR over 2026-2031. Growth is propelled by enterprise-wide digital transformation programs, brisk cross-border merger and acquisition pipelines, and tightening environmental, social, and governance disclosure mandates across the region’s diversified economies. Digital strategy engagements dominate spending, underpinned by rapid artificial intelligence adoption, data-driven decision making, and platform business model shifts. At the same time, heightened regulatory scrutiny in financial services, life sciences, and technology sectors sustains demand for risk, compliance, and restructuring advisory work. Competitive intensity is rising as technology vendors and freelance platforms encroach on traditional consultancies, prompting incumbents to invest heavily in proprietary AI toolkits, specialized ESG offerings, and hybrid delivery models. Meanwhile, government incentives aimed at SME digitalization and supply-chain decarbonization are broadening the client base, reshaping staffing models, and influencing pricing structures across the Asia Pacific strategic consulting services market.

Key Report Takeaways

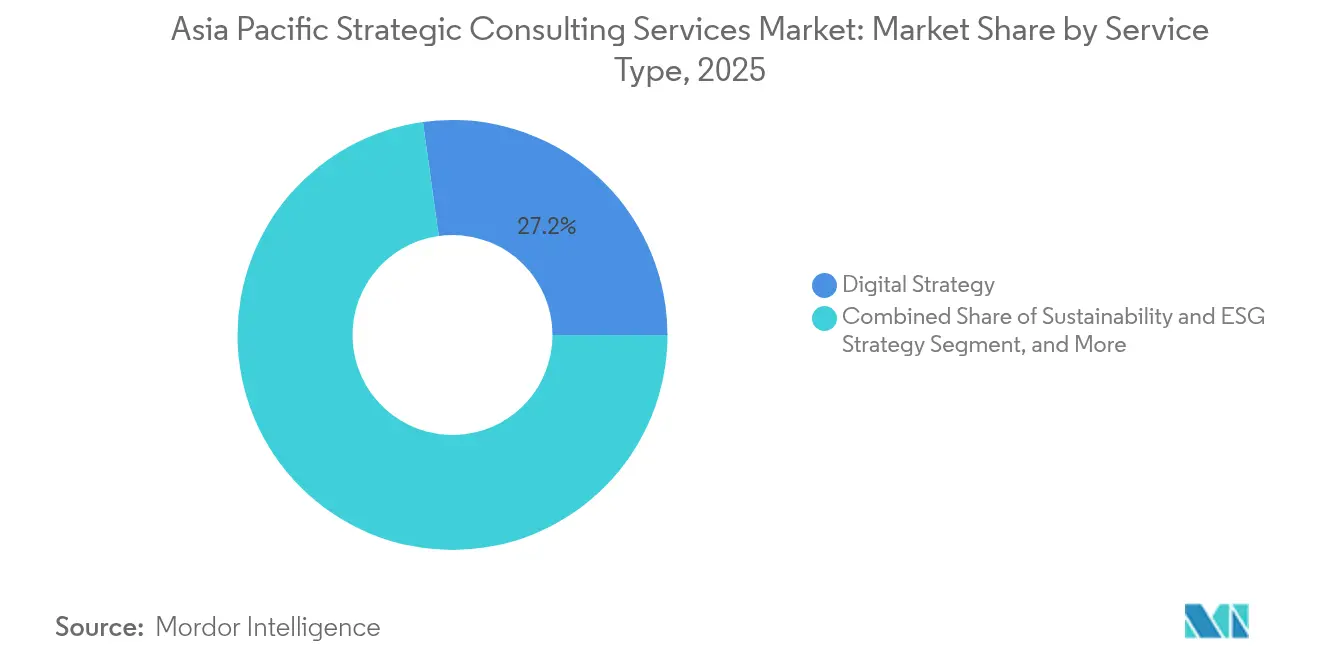

- By service type, digital strategy captured 27.20% revenue share in 2025; sustainability and ESG strategy is projected to post a 13.05% CAGR to 2031.

- By end-user industry, financial services accounted for 24.12% share of the Asia Pacific strategic consulting services market size in 2025; life sciences and healthcare is advancing at a 13.70% CAGR through 2031.

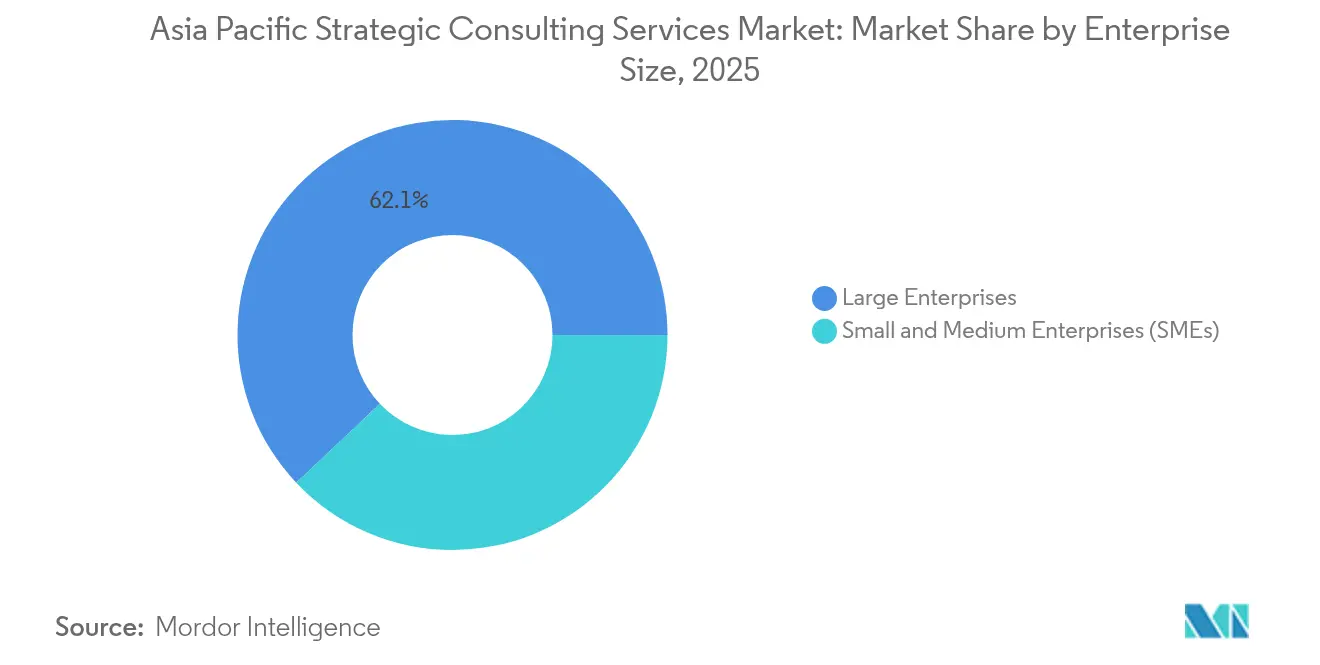

- By enterprise size, large enterprises held 62.05% share in 2025, whereas the SME segment is poised for a 13.02% CAGR during 2026-2031.

- By delivery model, on-site consulting represented 55.15% of the Asia Pacific strategic consulting services market size in 2025; remote and virtual engagements are expanding at a 12.95% CAGR to 2031.

- By country, China led with 30.05% of Asia Pacific strategic consulting services market share in 2025, while India is on track for a 13.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Strategic Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-transformation wave across Asia Pacific | +3.2% | Global, early gains in Singapore, China, India | Medium term (2-4 years) |

| Surge in cross-border M and A and restructuring mandates | +2.8% | Asia Pacific core, spill-over to Middle East and Africa | Short term (≤ 2 years) |

| Escalating demand for ESG / sustainability road-maps | +2.5% | Global | Long term (≥ 4 years) |

| Embedded-finance disruption driving payments strategy work | +1.9% | Southeast Asia, India, China | Medium term (2-4 years) |

| Freelance-consultant supply mismatch enabling new delivery models | +1.4% | Japan, Australia, Singapore | Short term (≤ 2 years) |

| Heavy-industry supply-chain decarbonization (CBAM spill-overs) | +0.9% | China, South Korea, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital-transformation wave across Asia Pacific

Enterprises in the region accelerated digital spending following pandemic disruptions, with 44% of previously offline organizations planning to automate over half their non-automated processes by 2025.[1]Fujitsu Ltd., “Fujitsu Global Survey Demonstrates Priorities in the Post-pandemic World,” acnnewswire.com Consulting firms are seizing the opportunity by embedding AI throughout project lifecycles, raising utilization rates by up to 50% and enabling data-rich strategy sprints that shorten engagement timelines. Regulators are also shaping demand: Singapore’s Monetary Authority issued transition planning guidelines, and Japan’s Financial Services Agency published AI use frameworks that encourage structured advisory support. As clients favor expert-heavy teams, firms are migrating from pyramid to diamond staffing, pushing mid-level and specialist hiring higher and redefining talent economics across the Asia Pacific strategic consulting services market.

Surge in cross-border M and A and restructuring mandates

Supply-chain diversification and geopolitical realignment lifted regional deal volumes to multi-year highs in 2024, energizing transaction strategy practices. The complexity of navigating disparate regulatory codes and national security reviews gives a distinct edge to advisory teams with deep local credentials and collaborative toolsets. Technology-driven acquisitions such as IBM’s USD 6.4 billion HashiCorp purchase underscore how software capabilities influence valuation thresholds, while spin-offs and carve-outs linked to de-risking strategies further expand restructuring pipelines. As a result, consultancies are formalizing geostrategy cells that translate macro risk signals into board-level action plans across ASEAN, Japan, and Australia.

Escalating demand for ESG / sustainability road-maps

The European Union’s Carbon Border Adjustment Mechanism, covering 41% of EU imports from Asia, and the International Sustainability Standards Board’s inaugural disclosure standards have amplified compliance urgency. Consulting firms are now building end-to-end decarbonization offerings that integrate greenhouse-gas baselining, supply-chain tracing, and climate-aligned finance. Early adopters such as KPMG China’s shipping practice illustrate how sector-focused ESG services can secure long-term transformation programs. Meanwhile, Singapore’s Asia Taxonomy and Malaysia’s Greening Value Chain Program signal that government-driven frameworks will continue to broaden addressable ESG advisory demand across the Asia Pacific strategic consulting services market.

Embedded-finance disruption driving payments strategy work

Open-banking standards and digital wallets are redrawing Asia Pacific’s financial infrastructure, generating advisory demand for embedded-finance roadmaps, digital-identity tooling, and cross-border payments compliance.[2]TrustDecision, “APAC’s Fintech Regulation (Part 3),” trustdecision.com India’s Unified Payments Interface has unlocked massive inclusion opportunities, while Japan’s push toward 40% cashless transactions by 2025 is reshaping merchant strategies. Consulting teams with combined fintech and regulatory credentials are winning multi-year mandates to design trusted data architectures, secure cloud frameworks, and ESG-oriented fintech propositions that align with both consumer protection and sustainability criteria.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising price sensitivity among large enterprise clients | -1.8% | Global | Short term (≤ 2 years) |

| Intensifying competition from Big Tech and IT-services firms | -1.2% | China, India, Southeast Asia | Medium term (2-4 years) |

| Client skepticism on Gen-AI consulting ROI | -0.9% | Japan, Australia, Singapore | Short term (≤ 2 years) |

| Regional talent drain to freelance and in-house strategy teams | -0.7% | Asia Pacific core, especially Singapore and Hong Kong | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising price sensitivity among large enterprise clients

C-suite buyers are renegotiating fee structures in response to macro uncertainty, shifting toward outcome-based pricing and shorter project cycles. Firms are countering with fixed-fee models underpinned by detailed ROI baselines and AI-enabled delivery accelerators that sustain margins even at lower blended rates.[3]Napta, “Consulting in 2025: Challenges, AI, Talent and Growth Strategies,” napta.io The emphasis on specialist staffing further compresses junior demand, intensifying the search for mid-level talent and fostering alumni networks that feed freelance marketplaces.

Intensifying competition from Big Tech and IT-services firms

Technology vendors are bundling strategic advice with implementation, leveraging proprietary platforms to position themselves as end-to-end partners, particularly in the Asia Pacific Digital Transformation and data strategy arenas. Western consultancies face heightened rivalry in China and India, where local tech champions possess deep regulatory relationships and cost advantages. Strategic alliances, co-development labs, and equity investments in niche SaaS providers are emerging counter-moves as incumbents defend share across the Asia Pacific strategic consulting services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital Strategy Commands the Largest Wallet Share

The digital strategy segment contributed 27.20% to Asia Pacific strategic consulting services market size in 2025 and remains the reference point for enterprise reinvention programs. Its dominance is rooted in AI integration, data modernization, and platform business model expansion that deliver quantifiable revenue lifts and cost efficiencies. ESG and sustainability consulting, though smaller today, is posting a 13.05% CAGR and is expected to chip away at traditional corporate strategy budgets, as disclosure mandates embed environmental metrics into boardroom agendas. M and A strategy rides the wave of supply-chain and geopolitical realignments, reinforcing demand for integrative transaction playbooks. Risk and compliance work remains resilient, fueled by tightening anti-money-laundering standards, cyber regulations, and digital sovereignty laws proliferating across Asia Pacific jurisdictions.

Service providers are differentiating by sector-specific accelerators and proprietary data assets that compress time to insight. For example, carbon-accounting platforms are embedded into ESG engagements, while digital twins accelerate manufacturing strategy design. These tools create recurring revenue streams via subscription or managed-service models, subtly shifting revenue mixes away from pure time-and-materials billing. In parallel, the Asia Pacific strategic consulting services market is witnessing consultancies spinning off specialist boutiques to maintain premium pricing and brand clarity in digital strategy and sustainability niches.

By End-User Industry: Financial Services Retains the Crown

Financial institutions captured 24.12% of Asia Pacific strategic consulting services market share in 2025 as banks, insurers, and capital-market operators navigated digital disruption and regulatory tightrope walks. Fintech collaborations, open-banking interfaces, and embedded finance ecosystems require intricate transition blueprints that integrate technology, operations, and compliance layers. Life sciences and healthcare, meanwhile, is accelerating at a 13.70% CAGR, underpinned by demographic shifts, telehealth diffusion, and rising biotech investment. TMT players continue to seek guidance on 5G-enabled platforms, AI content generation, and data-privacy imperatives, while manufacturing clients demand Industry 4.0 roadmaps with decarbonization milestones.

Sector specialization is redefining delivery teams: consultants with dual backgrounds in, for instance, clinical research and data science, or payments operations and cybersecurity, now command premium billing rates. Government clients are selectively commissioning smart-city and public-finance transformation projects, although budget constraints temper overall growth. Across sectors, outcome metrics such as loan origination speed, patient adherence, or emissions reduction are baked into contracting terms, reinforcing result-based engagement models in the Asia Pacific strategic consulting services market.

By Enterprise Size: SME Digital Adoption Unlocks New Pools of Demand

Large corporations represented 62.05% of 2025 contract value, but SME engagements are projected to expand at a 13.02% CAGR through 2031 as cloud platforms, government grants, and freelance ecosystems lower entry barriers to strategic advice. Malaysia’s Greening Value Chain Program, which engaged 650 SMEs and prompted 200 to report emissions, illustrates how policy-led incentives create advisory opportunities at scale. Consultancies are responding with modular playbooks, digital workshops, and subscription portals that bundle best practices, benchmarks, and virtual coaching.

The Asia Pacific strategic consulting services market therefore bifurcates into high-touch, bespoke work for conglomerates and scalable, template-driven offerings for SMEs. Freelance consultant platforms report average monthly fees of JPY 1.2 million (USD 8,500) for hybrid digital-transformation projects, signaling a shift toward variable-cost talent models that enable price points palatable to smaller enterprises.

By Delivery Model: Hybrid Approaches Gain Ground

On-site engagements still account for 55.15% of Asia Pacific strategic consulting services market size, a testament to relationship-heavy strategy development and stakeholder alignment needs. Yet remote and virtual models are clocking a 12.95% CAGR, supported by secure collaboration suites, virtual whiteboarding, and asynchronous work rhythms. Hybrid delivery, combining initial on-site workshops with remote analytics sprints, is emerging as the default, particularly in Singapore, Japan, and Australia where digital infrastructure and regulatory frameworks support secure data exchange.

Advisories are investing in VR-based client war rooms, AI transcription services, and digital playbook libraries to sustain engagement intensity in virtual settings. This capability set also enables cross-border team composition, unlocking expertise pools previously constrained by travel budgets and visa timelines. Hybrid delivery’s cost-to-serve advantage strengthens competitiveness, especially in SME and sustainability project categories within the Asia Pacific strategic consulting services market.

Geography Analysis

China anchored 30.05% of Asia Pacific strategic consulting services market share in 2025, driven by the breadth of its enterprise landscape, state-owned reform agendas, and relentless demand for digital and ESG transformation playbooks . Regulatory complexity across cybersecurity, data privacy, and capital controls necessitates localized advice, granting consultancies with deep provincial networks a durable edge. India is the fastest-growing node, expanding at a 13.90% CAGR as digital public-infrastructure rollouts, production-linked incentive schemes, and swelling foreign direct investment catalyze strategic advisory uptake.

Japan remains a high-value market where corporate governance overhaul, aging infrastructure renewal, and sustainability mandates sustain premium consulting spend. Australia’s resource-sector modernization and stringent prudential frameworks create steady demand for risk, compliance, and transition strategy services. Singapore punches above its economic weight; its Finance for Net Zero Action Plan and Asia Taxonomy anchor ESG engagements, while its role as a regional headquarters hub concentrates multi-country transformation programs.

South Korea’s conglomerates pursue digital platform pivots and governance reforms, while Indonesia, Malaysia, and Thailand are emerging battlegrounds where infrastructure modernization, manufacturing relocation, and regulatory uplift open advisory inroads albeit amid fragmented client bases and local partner obligations. Cross-border M and A flows and supply-chain realignments knit these markets together, prompting clients to seek integrated, multi-jurisdictional consulting frameworks to manage geopolitical risk exposure across the Asia Pacific strategic consulting services market.

Competitive Landscape

Market concentration is moderate as global strategy houses, Big Four advisories, technology consultancies, and specialist boutiques vie for share. McKinsey and Company, Boston Consulting Group, and Bain and Company leverage entrenched C-suite relationships, global benchmarks, and proprietary analytics to anchor large transformation mandates, yet face encroachment from Big Tech and IT services players offering bundled strategy-to-execution propositions. To protect margin, incumbents are accelerating AI investments, evidenced by in-house generative-AI copilots that automate research synthesis and scenario modeling, cutting proposal turnaround by up to 30%.

Staffing architectures are in flux: diamond-shaped models prioritize mid-career experts and data engineers over entry-level generalists, curbing leverage but boosting value perception. Freelance platforms unlock flexible, high-caliber talent, enabling clients to bypass traditional firm overheads. Sustainability consulting forms the newest white space, with boutique players attaining premium billing through niche carbon-accounting and supply-chain traceability offerings. Compliance-heavy sectors such as finance and healthcare still reward incumbents with decades of regulatory liaison experience; however, specialized law firms and risk advisories are also extending into strategic territory, blurring competitive lines in the Asia Pacific strategic consulting services market.

Asia Pacific Strategic Consulting Services Industry Leaders

Deloitte Touche Tohmatsu Limited

McKinsey & Company

KPMG International Limited

Ernst and Young Global Limited

Accenture plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Koike Consulting Co., Ltd. garnered a nomination for HRM Asia Leaders' Choice Awards 2025 in the Best Corporate - Leadership Development Provider category, reflecting its expanding executive assessment portfolio.

- May 2025: Overcyber Partners’ April 2025 Freelance Consultant Project Trend Report analyzed 417 listings, revealing that IT and digital-transformation projects form 60% of demand, with hybrid work structures adopted in 70% of cases.

- April 2025: Asian Development Bank and United Nations Development Programme released a supply-chain resilience playbook citing 650 SMEs engaged in Malaysia’s Greening Value Chain Program.

- April 2025: Deloitte Asia Pacific Centre for Regulatory Strategy issued quarterly updates on supervisory focus areas, informing compliance strategy roadmaps.

Asia Pacific Strategic Consulting Services Market Report Scope

Strategy consulting is advising the organizations on high-level decisions in an unbiased fashion, using deep industry knowledge and understanding to deliver the best results. It is a type of management consulting that generally implies advising on the disciplines such as business model transformation, corporate strategy, mergers & acquisitions, economic policy, functional strategy, organizational strategy, digital strategy, and strategy & operations.

Asia Pacific Strategic Consulting Services Market By End-User Industry (Financial Services, Life Sciences, and Healthcare, Retail, Government, Energy, Others) and Countries.

By Service Type

| Corporate Strategy |

| Digital Strategy |

| Operations Strategy |

| M&A and Restructuring |

| Sustainability and ESG Strategy |

| Risk and Compliance Strategy |

By End-User Industry

| Financial Services |

| Life Sciences and Healthcare |

| Retail and Consumer |

| Government and Public Sector |

| Energy and Utilities |

| Manufacturing |

| Technology Media and Telecommunications |

| Other End-User Industries |

By Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

By Delivery Model

| On-site Consulting |

| Remote / Virtual Consulting |

| Hybrid Consulting |

By Country

| China |

| Japan |

| India |

| Australia |

| South Korea |

| Singapore |

| Indonesia |

| Malaysia |

| Thailand |

| Rest of Asia Pacific |

| By Service Type | Corporate Strategy |

| Digital Strategy | |

| Operations Strategy | |

| M&A and Restructuring | |

| Sustainability and ESG Strategy | |

| Risk and Compliance Strategy | |

| By End-User Industry | Financial Services |

| Life Sciences and Healthcare | |

| Retail and Consumer | |

| Government and Public Sector | |

| Energy and Utilities | |

| Manufacturing | |

| Technology Media and Telecommunications | |

| Other End-User Industries | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Delivery Model | On-site Consulting |

| Remote / Virtual Consulting | |

| Hybrid Consulting | |

| By Country | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Singapore | |

| Indonesia | |

| Malaysia | |

| Thailand | |

| Rest of Asia Pacific |

Key Questions Answered in the Report

What is the projected value of the Asia Pacific strategic consulting services market in 2031?

Forecasts indicate the market will reach USD 20.98 billion by 2031, reflecting a 12.52% CAGR.

Which service category is expanding the fastest?

Sustainability and ESG strategy consulting is registering a 13.05% CAGR through 2031 as disclosure mandates intensify.

Which country currently generates the highest consulting spend?

China accounts for 30.05% of regional spend due to its large enterprise base and complex regulatory environment.

Why are SMEs becoming important clients for consultants in Asia Pacific?

Government digitalization incentives and flexible delivery models are making strategic advice affordable, driving a 13.02% CAGR in SME engagements.

How are delivery models evolving post-pandemic?

Hybrid structures that blend on-site workshops with remote analytics sprints are gaining traction, growing at a 12.95% CAGR.

Which industry contributes the largest share of consulting revenue?

Financial services holds 24.12% of revenue owing to fintech disruption, regulatory reforms, and digital transformation imperatives.

Page last updated on: