Taiwan Lubricants Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

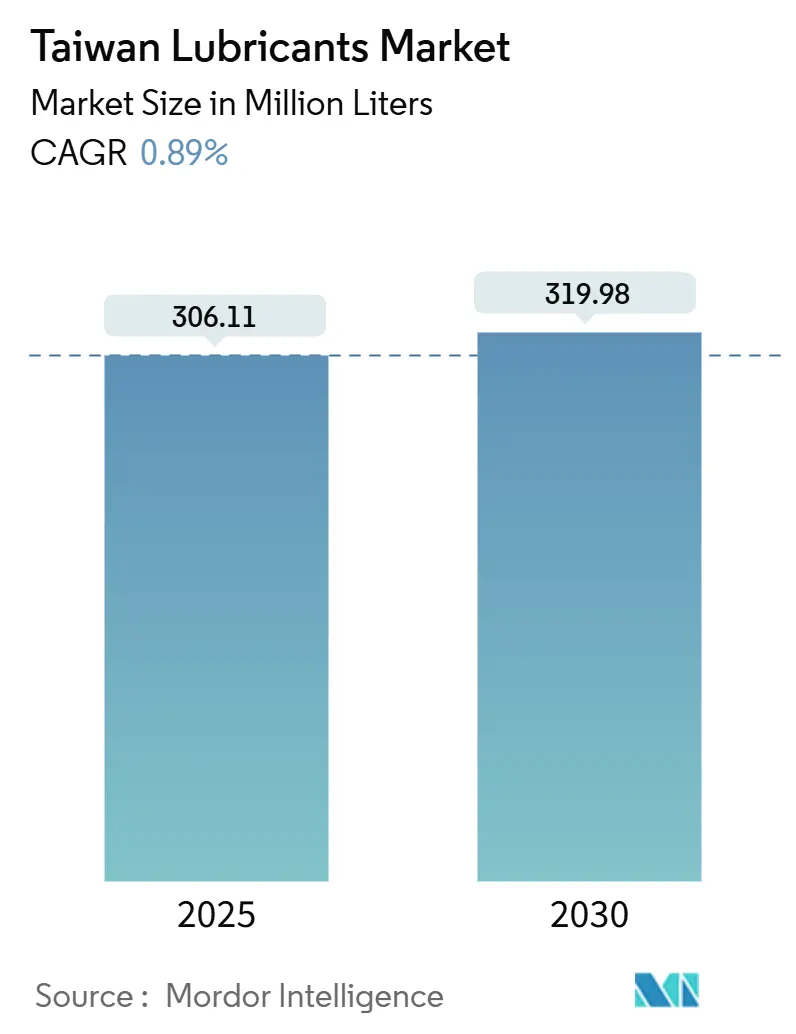

| Market Volume (2025) | 306.11 Million liters |

| Market Volume (2030) | 319.98 Million liters |

| Growth Rate (2025 - 2030) | 0.89% CAGR |

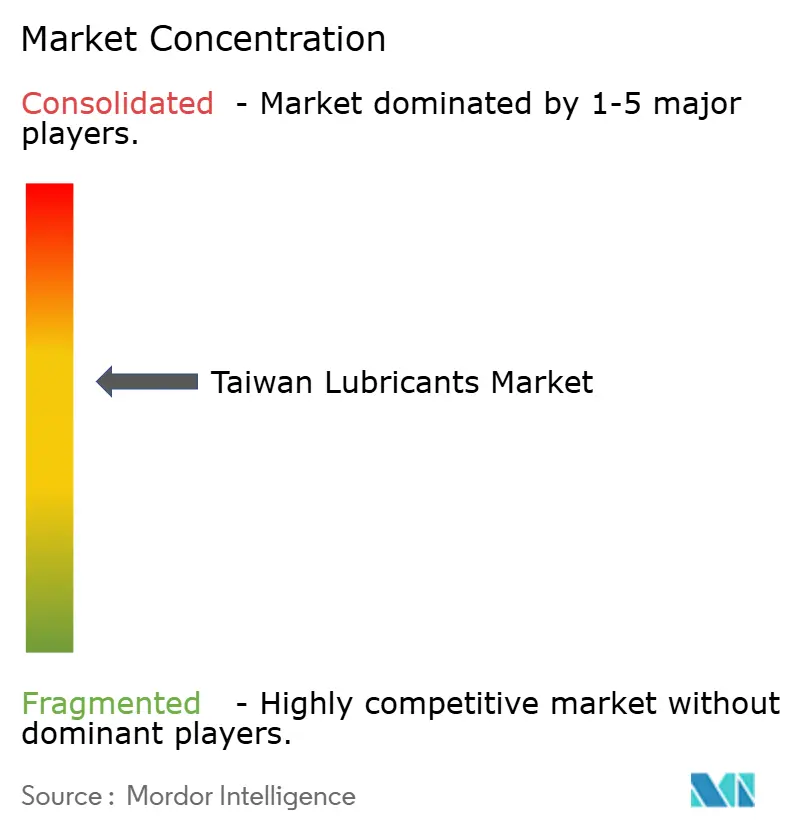

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taiwan Lubricants Market Analysis by Mordor Intelligence

The Taiwan lubricants market size is estimated at 306.11 million liters in 2025, and is expected to reach 319.98 million liters by 2030, at a CAGR of 0.89% during the forecast period (2025-2030). Precision manufacturing, offshore wind installation, and circular economy regulations are offsetting the slowdown in traditional engine oil demand linked to the government’s 2040 phase-out of internal combustion vehicles. Mineral-oil formulations still dominate, but fast adoption of synthetic and bio-based options is evident as manufacturers chase energy-efficiency gains, carbon-pricing compliance, and export-market sustainability audits. Competitive intensity remains moderate as domestic majors CPC Corporation Taiwan and Formosa Petrochemical defend their share against ENEOS, Shell, and specialty challengers that target semiconductor and renewable energy applications.

Key Report Takeaways

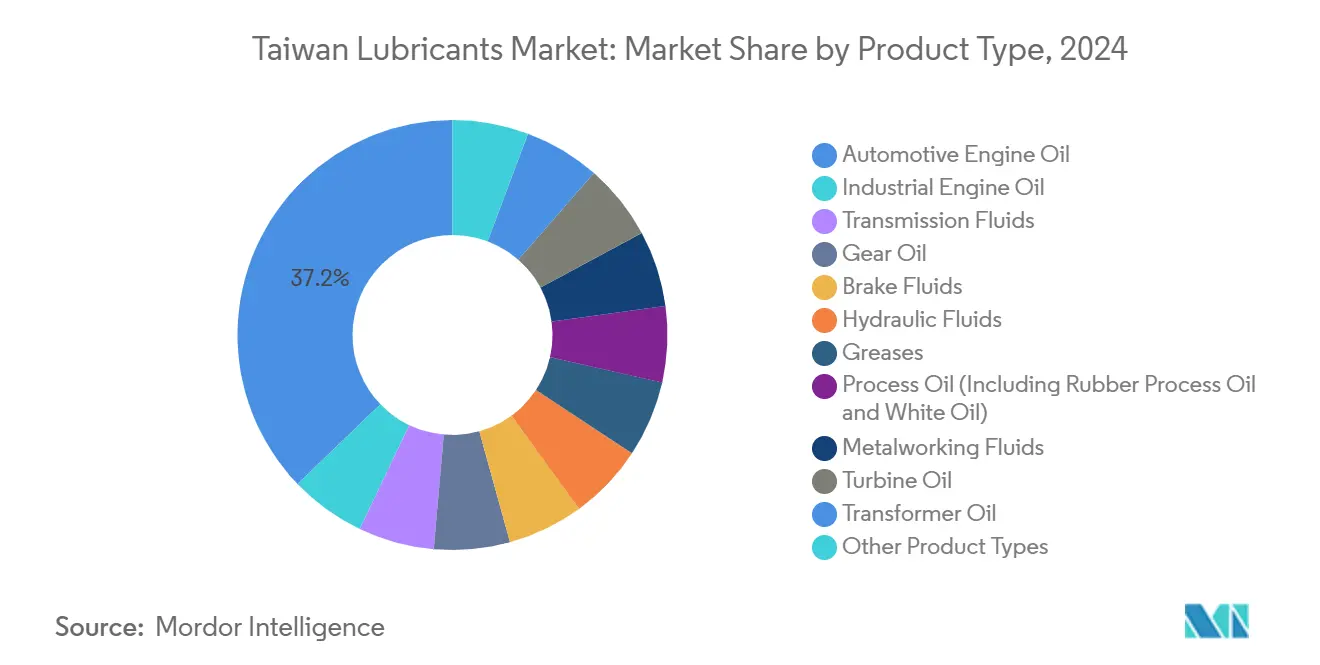

- By product type, automotive engine oil led with a 37.18% share of the Taiwan lubricants market in 2024, while industrial engine oil is projected to post the fastest growth of 1.12% CAGR through 2030.

- By end-user, the automotive segment held 46.31% of the Taiwan lubricants market share in 2024, with industrial users showing the strongest 1.03% CAGR momentum to 2030.

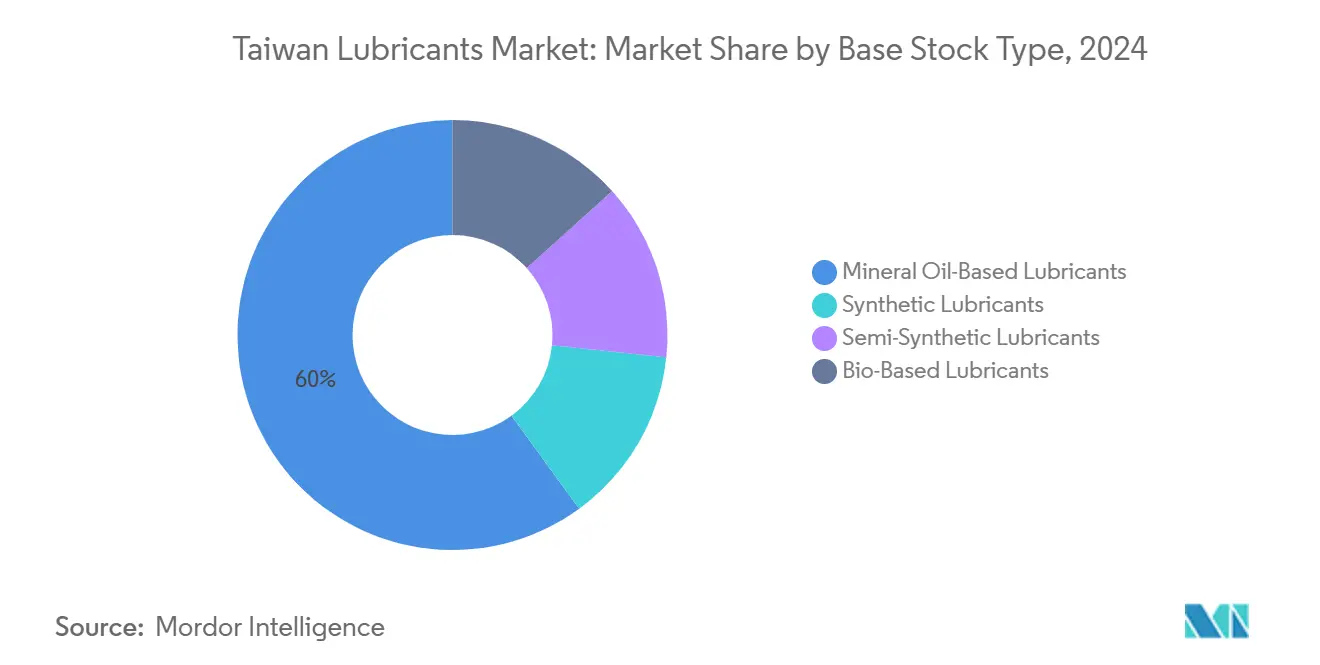

- By base stock, mineral oils commanded a 60.03% share of the Taiwan lubricants market size in 2024, whereas bio-based alternatives are advancing at a 1.78% CAGR, driven by waste-oil reuse mandates.

Taiwan Lubricants Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stable automotive aftermarket supporting engine-oil demand | +0.3% | National, urban centers | Medium term (2-4 years) |

| Advanced manufacturing and semiconductor sector demand | +0.2% | Hsinchu, Taoyuan, Taichung | Long term (≥ 4 years) |

| Rising adoption of synthetic lubricants for precision and energy efficiency | +0.2% | Taichung, Kaohsiung | Medium term (2-4 years) |

| Government focus on green manufacturing boosting bio-based uptake | +0.1% | National | Long term (≥ 4 years) |

| Offshore wind build-out requiring specialty oils | +0.1% | Changhua, Yunlin, Chiayi | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stable Automotive Aftermarket Supporting Engine-Oil Demand

Taiwan’s network of approximately 2,500 fuel stations maintains predictable routine oil-change volumes, even as new-car sales plateau[1]Shan-Loong Transportation Co. Ltd., “Fuel Station Network and Lubricant Services,” shanloong.com.tw. A mature passenger-car fleet, extended drain interval products, and persistent commercial vehicle mileage underpin baseline consumption. Two-wheeler electrification is eroding scooter oil volumes; however, commercial fleets are offsetting part of that decline by adopting premium formulations that lengthen service intervals. Suppliers rely on this cash-flow stability to finance research and development aimed at post-ICE opportunities. The aftermarket thus remains a near-term anchor while the sector pivots toward next-generation applications.

Advanced Manufacturing and Semiconductor Sector Driving Industrial Oil Usage

Taiwan’s semiconductor fabs require ultra-pure lubricants that tolerate narrow temperature spreads to avoid line shutdowns. Precision machinery plants in Taichung are deploying Industry 4.0 ball-screw assemblies with real-time lubrication monitoring from HIWIN, spurring demand for sensor-compatible oils. Diamond-wire wafer slicing reduces bulk cutting-fluid loads but raises the need for precise cooling oils. Growth in chip capacity through 2030, therefore, sustains a niche for high-specification industrial lubricants. Suppliers able to guarantee contamination-free performance gain pricing power in this environment.

Rising Adoption of Synthetic Lubricants for Machinery Precision and Energy Efficiency

Manufacturers are pursuing the island’s 2050 net-zero goal under an NTD 300 per-ton carbon price, effective from May 2026, favoring synthetic formulations that reduce frictional losses. Local blender HAI LU JYA HE markets nano-emulsion cutting oils that cut power draw and extend tool life, illustrating the shift toward value-adding chemistries. Export-facing plants must document carbon savings to satisfy European supply-chain audits, accelerating the switch from mineral to synthetic. Energy-cost sensitivity, combined with performance gains, is widening the synthetic premium segment despite higher upfront prices.

Government Focus on Green Manufacturing Promoting Bio-Based Lubricants

Industrial-waste regulations divert 87% of waste oil into recycling streams that feed bio-lubricant production, ensuring a stable feedstock supply and lowering disposal fees[2]Ministry of Environment Taiwan, “Waste Oil Recycling Regulations,” moenv.gov.tw . Food-service waste and cooking oil collection networks add another renewable source, converting a disposal problem into a circular-economy input. Bio-based oils struggle in high-temperature environments but excel in hydraulic and gear applications, where biodegradability earns environmental approvals. Firms integrating waste-oil processing with blending lines gain cost and compliance advantages over traders that rely solely on imports.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mature vehicle parc with slow new-car growth | –0.2% | National, urban | Medium term (2-4 years) |

| Import-driven base-oil and additive price volatility | –0.1% | National | Short term (≤ 2 years) |

| Strict waste-oil regulations elevating compliance costs | –0.1% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mature Vehicle Parc with Slow New-Car Growth

Stagnant household car purchases coupled with an accelerated 2040 EV roadmap reduce combustion-engine lubricant volumes. Older vehicles exit the fleet faster than replacements arrive, particularly in Taipei where public transit alternatives attract commuters. Suppliers must compete aggressively for a shrinking ICE pool, eroding margins unless they upsell premium synthetics. While motorbike electrification pressures two-stroke oils first, passenger-car switchovers are poised to weigh heavily on gasoline engine oils after 2030.

Import-Driven Base-Oil and Additive Price Volatility

Limited domestic refining capacity leaves blenders exposed to swings in Group III base-oil prices and additive packages sourced from Singapore and South Korea. A 4.13% import tariff does little to cushion spot-market surges, while fluctuations in the New Taiwan Dollar compound cost uncertainty for smaller firms that lack hedging lines. Multinationals spread procurement across regions, but local independents must pass spikes through to customers, risking share losses during down-cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oils Anchor Volume as High-Spec Industrial Fluids Accelerate

Automotive engine oil retained 37.18% of 2024 consumption, underscoring its status as the single largest contributor to the Taiwan lubricants market. Yet, industrial engine oils are projected to clock the highest 1.12% CAGR, fueled by semiconductor fabs and precision machinery upgrades. Transmission and gear oils benefit from fleet modernization, while hydraulic fluids capitalize on the offshore wind boom, which demands corrosion-resistant marine grades. Metalworking fluids grow steadily as cutting-tool technologies advance in Taichung’s machinery belt.

Volume growth tilts toward customized formulations rather than commodity grades. Contract wins with Ørsted turbine suppliers are securing multi-year off-take for hydraulic and gear oils. Meanwhile, dual-purpose process oils serve petrochemical plants in Kaohsiung. Turbine-oil demand from gas-fired peaker plants is stable but now supplemented by wind-turbine lubricants. Transformer oils see incremental gains from grid modernization grants. Brake fluids and greases hold niche but critical positions for commercial transport operators, who can leverage enhanced service packages and condition-monitoring add-ons.

By End-User Industry: Automotive Dominates for Now, but Industrial Momentum Builds

Automotive customers accounted for 46.31% of the Taiwan lubricants market volume in 2024, primarily driven by passenger-car maintenance routines. Yet the industrial cluster is set to outpace the market at a 1.03% CAGR, reflecting USD 40.3 billion in annual machinery exports and semiconductor fab expansions that require ultra-clean oils. Power-generation demand rises in response to the 15 GW offshore wind target, expanding turbine oil and hydraulic fluid opportunities. Metallurgy, marine logistics at Kaohsiung Port, and aerospace component machining add diversified anchors.

Heavy-equipment lubricants find traction in infrastructure projects such as the Suhua Highway safety improvement works, while agricultural modernization sustains demand for tractor hydraulic fluids in central counties. Niche aerospace grades earn premium margins by meeting Mil-spec oxidation stability requirements. Collectively, these trends signal an end-user pivot away from volume-centric automotive oils toward margin-rich industrial solutions tailored to Taiwan’s evolving production landscape.

By Base Stock Type: Mineral Dominance Persists Amid Carbon-Footprint Pressures

Mineral formulations held a 60.03% share in 2024, thanks to cost advantages and broad distribution coverage. Nevertheless, bio-based oils are the fastest-growing segment at a 1.78% CAGR, as waste-oil recycling mandates create low-cost feedstock pools and help manufacturers claim Scope 3 emission reductions. Synthetic grades are increasingly used in precision applications, where extended service intervals justify the higher sticker price, while semi-synthetics bridge the performance and price gap for mid-tier users.

The policy-driven shift toward circular feedstocks accelerates once the NTD 300 carbon levy takes effect. Firms with in-house re-refining gain a dual benefit of cost control and environmental credits. Synthetic importers, while exposed to currency swings, retain high-end niches in chip fabs. Semi-synthetics find favor in fleets that want longer oil-change intervals yet balk at full-synthetic premiums. Overall, suppliers that balance price, performance, and carbon intensity will capture a larger share as regulations tighten.

Geography Analysis

Northern Taiwan, anchored by Hsinchu Science Park, exhibits the highest lubricant demand density, driven by semiconductor fabs that require contamination-free oils for etching, CMP, and photolithography equipment. Taipei-Taoyuan’s logistics hub sustains a large commercial-vehicle maintenance market, further lifting engine-oil volumes.

Central Taiwan’s Taichung corridor is the heartland of precision machinery, hosting 1,500 firms that consume metalworking fluids and slideway oils for export-oriented CNC production. Consistent upgrading to Industry 4.0 machinery amplifies the demand for sensor-compatible lubricants that integrate with predictive maintenance systems. Transport routes through the central mountain range complicate bulk deliveries, prompting distributors to deploy regional stock points near industrial estates.

Southern Taiwan houses Kaohsiung’s integrated refinery-petrochemical complex, generating steady base-oil and process-oil flows, while heavy-industry clients drive grease and gear-oil needs. Proximity to deep-water ports spurs marine-lubricant bunkering, with global carriers relying on ISO-FMECA-certified supplies dockside. Offshore-wind staging areas in Changhua, Yunlin, and Chiayi introduce surges in specialty hydraulic-fluid imports ahead of each turbine-installation campaign. Eastern counties remain lightly industrialized but consume agricultural and tourism-fleet lubricants, providing a baseline that stabilizes regional demand.

Regulatory enforcement is consistent island-wide, yet compliance infrastructure is densest in the north and center, where multinational fabs adhere to strict audit protocols. Compact geography allows overnight deliveries between ports and industrial parks, lowering inventory costs for distributors but also intensifying competition, as customers can easily switch suppliers on short notice.

Competitive Landscape

The Taiwan lubricants market is moderately consolidated, with the top five suppliers accounting for a significant market share. CPC Corporation Taiwan leverages a vertically integrated base-oil supply and a 700-station retail network to secure a significant share of the engine oil market. Niche player HAI LU JYA HE focuses on nano-enhanced metalworking fluids, achieving ISO 9001:2015 certification and a monthly output of 150 tons to meet the precision-machinery tolerance demands. Specialized importers build portfolios around wind-turbine and marine lubricants, partnering with OEMs to secure approved-product listings that lock in aftermarket volumes. Regulatory compliance and the capital required for waste-oil recovery are nudging micro-blenders to exit or merge, accelerating gradual consolidation. Meanwhile, innovative entrants that integrate waste-oil re-refining into blending operations capture both cost savings and carbon credit revenues, making them increasingly attractive to corporate buyers bound by ESG scorecards.

Taiwan Lubricants Industry Leaders

CPC Corporation, Taiwan

Formosa Petrochemical Corporation

ENEOS Corporation

Shell plc

Exxon Mobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: SPARK-Lubricants inaugurated a Taiwan subsidiary to supply precision-manufacturing lubricants tailored for semiconductor cleanrooms.

- June 2024: Castrol invested USD 50 million in Gogoro, Taiwan's leading electric scooter manufacturer, signaling strategic positioning for the electrification transition and development of specialized lubricants for electric vehicle applications.

Taiwan Lubricants Market Report Scope

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Key Questions Answered in the Report

What is the current volume of the Taiwan lubricants market?

The market totals 306.11 million liters in 2025.

How fast is demand growing?

Consumption is projected to rise at a 0.89% CAGR through 2030.

Which segment is expanding the quickest?

Industrial engine oils, supported by semiconductor and wind-energy projects, show the highest 1.12% CAGR.

Why are bio-based lubricants gaining attention?

Waste-oil recycling mandates and carbon pricing raise demand for biodegradable formulations.

How will the 2040 EV ban affect lubricant suppliers?

It curbs long-term engine-oil volumes, pushing companies to pivot toward industrial and renewable-energy applications.

Who are the major players?

CPC Corporation Taiwan, Formosa Petrochemical, Shell, and ENEOS dominate sales.

Page last updated on: