East Asia Lubricants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

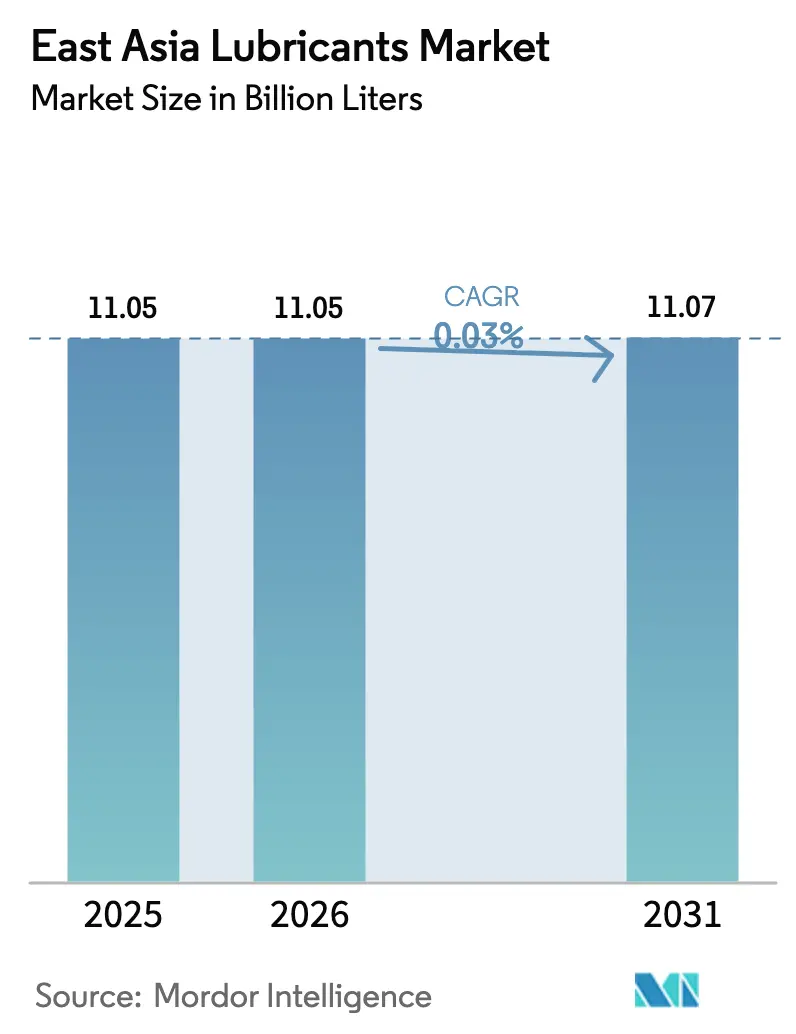

| Base Year Market Size (2025) | 11.05 Billion liters |

| Market Volume (2026) | 11.05 Billion liters |

| Market Volume (2031) | 11.07 Billion liters |

| Growth Rate (2026 - 2031) | 0.03% CAGR |

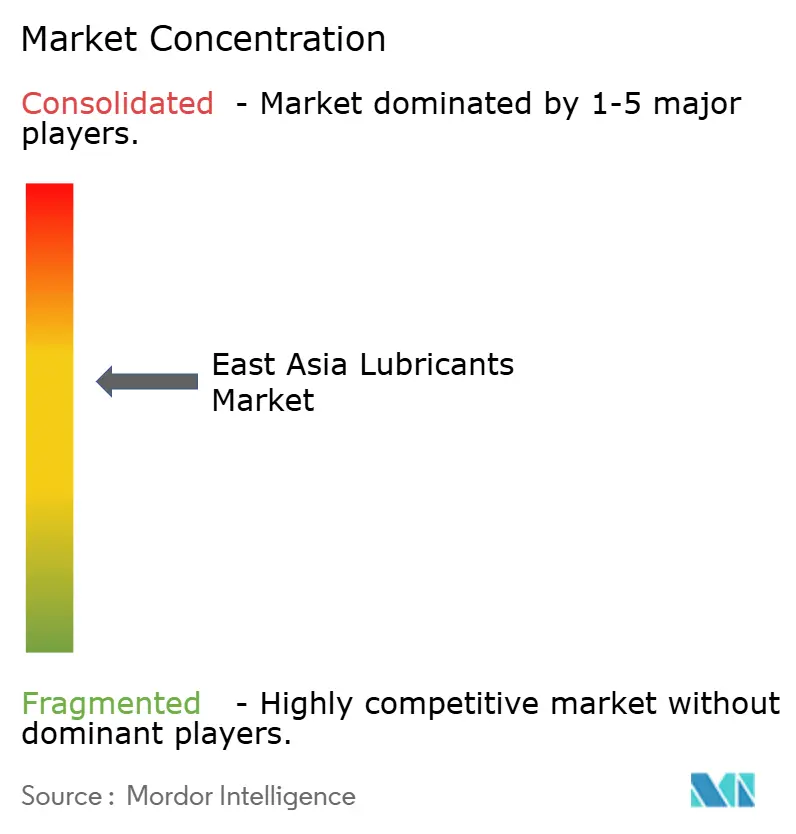

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

East Asia Lubricants Market Analysis by Mordor Intelligence

The East Asia Lubricants market size is expected to grow from 11.05 billion liters in 2025 to 11.05 billion liters in 2026 and is forecast to reach 11.07 billion liters by 2031 at 0.03% CAGR over 2026-2031. This mature demand curve conceals strong pockets of value, particularly where precision manufacturing, data center infrastructure, and advanced mobility platforms require premium formulations. China anchors regional consumption through its expansive industrial base and vehicle parc, while Taiwan’s fast-growing semiconductor ecosystem supplies incremental demand for ultra-high-purity fluids. Momentum also stems from corporate sustainability targets that favor low-viscosity synthetics and bio-based options, which meet the tight emission norms set by regulators in Singapore, Japan, and China. Competitive dynamics are intense because share gains depend on technical support, base-oil security, and rapid compliance with evolving chemical-safety directives.

Key Report Takeaways

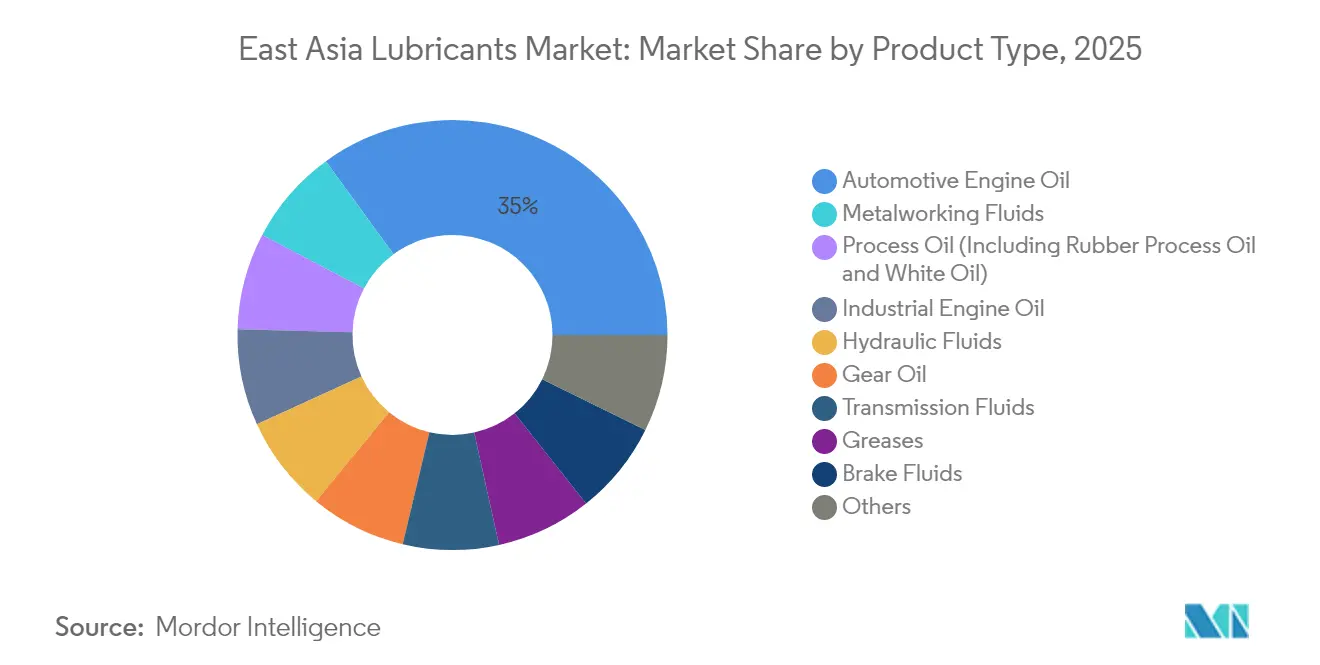

- By product type, automotive engine oils led with 35.02% of the East Asia lubricants market share in 2025; industrial engine oils are projected to expand at a 0.20% CAGR through 2031.

- By end-user industry, the automotive segment accounted for a 41.95% share of the East Asia lubricants market size in 2025, while industrial applications are expected to advance at a 0.14% CAGR to 2031.

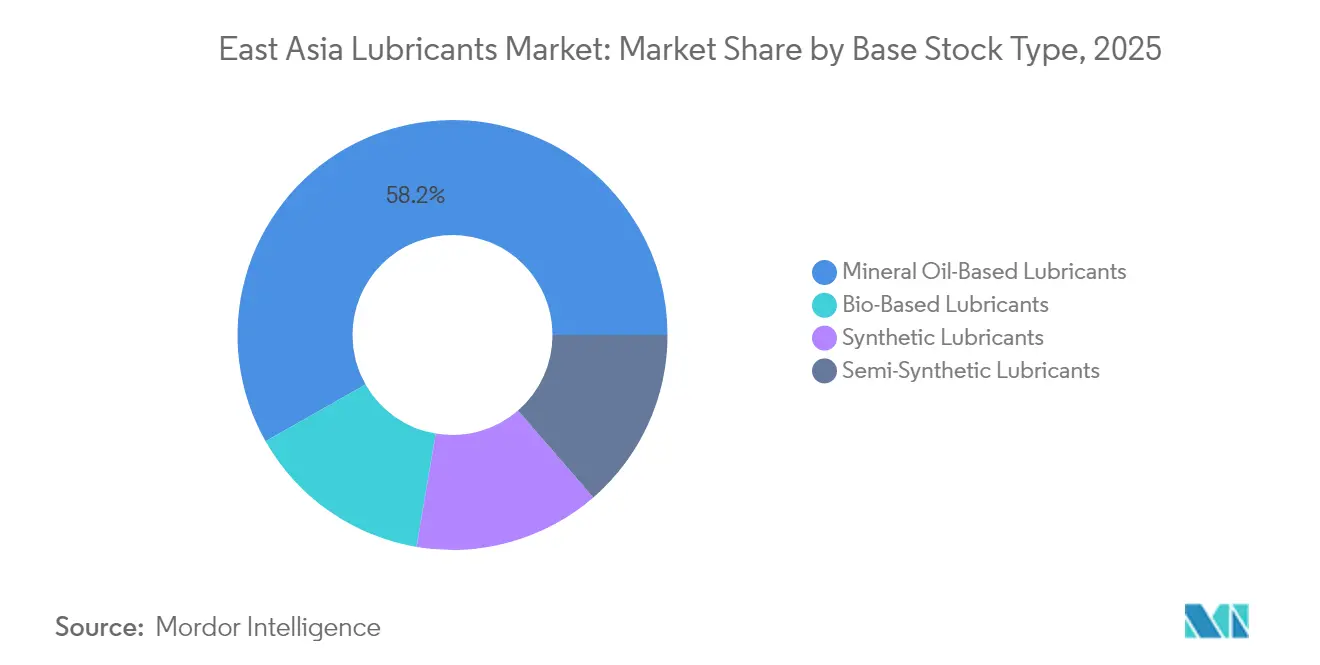

- By base stock, mineral-oil grades commanded a 58.22% share of the East Asia lubricants market size in 2025; bio-based lubricants posted the fastest growth rate of 0.43% CAGR through 2031.

- By geography, China held 69.05% of the East Asia lubricants market share in 2025, whereas Taiwan is projected to chart the fastest 0.85% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

East Asia Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resilient manufacturing activity in Japan, China, and South Korea | +0.8% | China, Japan, South Korea | Medium term (2-4 years) |

| OEM-linked demand for high-performance service-fill lubes | +0.6% | Regional automotive hubs | Long term (≥ 4 years) |

| Shift toward energy-efficient, low-viscosity formulations | +0.4% | Japan, South Korea, China | Medium term (2-4 years) |

| Specialty-grade niches from e-mobility and industrial automation | +0.5% | Taiwan, urban China, Japan | Long term (≥ 4 years) |

| Data-center immersion-cooling fluid uptake | +0.3% | Taiwan, Singapore, urban China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Resilient Manufacturing Activity in Japan, China, and South Korea

Factory utilization remains solid even as macro growth moderates. China experienced growth in industrial production in September 2024, underscoring demand for lubricants across robotics, CNC machining, and petrochemical plants. South Korea’s rebound in semiconductor shipments is lifting consumption of ultra-clean fluids for wafer fabrication tools. Manufacturers in all three economies are adopting ISO 14001 frameworks, which favor low-toxicity, biodegradable lubricants. The upshot is subdued volume but stronger value capture as users pay premiums for specialty blends that extend drain intervals and cut energy losses.

OEM-Linked Demand for High-Performance Service-Fill Lubes

Vehicle and equipment makers increasingly mandate proprietary oils to secure warranty performance. Passenger-car OEMs promote 0W-20 and 0W-16 grades to meet tougher fuel-economy rules under China’s CAFC program and Japan’s 2030 efficiency roadmap[1]“Technical Standards and Industry Guidelines,” Society of Automotive Engineers, sae.org. Industrial machinery builders follow suit by approving only products that clear exhaustive bench and field trials. These closed-list specifications protect incumbent suppliers capable of supplying Group III+, PAO, or ester synthetics, backed by robust technical service teams. Longer service intervals, often 20,000 km or 12,000 operating hours, reinforce demand for advanced additive chemistries that are resilient to shear and oxidation. As a result, premium synthetic lines outpace the overall growth of the East Asia lubricants market, despite flat underlying volumes.

Shift Toward Energy-Efficient, Low-Viscosity Formulations

Regulators and corporations pursue carbon-reduction targets, resulting in the rapid adoption of lower-viscosity oils. Japanese automakers were early movers, filling hybrids with 0W-16 formulations as standard fitment. Industrial users likewise switch to ISO VG 32 hydraulic fluids and low-friction gear oils to trim power bills. Base-oil suppliers, such as Shell and Chevron, have expanded Group III capacity in Singapore, ensuring a feedstock for these lighter blends. Smaller blenders lacking access to high-VI stocks struggle to keep pace, ceding share in the East Asia lubricants market to vertically integrated majors.

Specialty-Grade Niches from E-Mobility and Industrial Automation

Electric mobility presents new lubrication challenges not found in internal-combustion engines. EV reduction gears require fluids that combine dielectric strength and thin-film durability, driving the development of PAO-ester hybrids that cost multiples of conventional SAE 75W-90 gear oils. Battery thermal-management circuits rely on fluorinated or silicone-based coolants with zero electrical conductivity, a niche that yields margins far above legacy engine oils. Parallel growth in smart-factory deployments drives increased consumption of low-outgassing greases, which are critical to precision robots and cleanroom actuators. Taiwan’s fabs utilize fluids purified to parts-per-billion contamination thresholds, which enables qualified suppliers to secure long-term, high-value contracts.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ICE-vehicle production decline amid EV surge | −1.2% | China, regional spillover | Medium term (2-4 years) |

| Stricter bans on high-sulfur/non-biodegradable oils | −0.8% | Singapore, Japan, region-wide | Short term (≤ 2 years) |

| Geopolitical feed-stock volatility in East Asian seas | −0.6% | Import-reliant users | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ICE-Vehicle Production Decline Amid EV Surge

China is experiencing an increase in EV sales in 2024, which is eroding engine oil demand, as battery-electric models require only gear oils and small coolant volumes. Automakers such as BYD and Geely are pivoting their capital budgets away from ICE platforms, compressing aftermarket prospects over time. Each lost combustion vehicle reduces lubricant consumption, a headwind offset only partially by emerging EV fluid requirements. The effect dampens volume growth not just in China but across the East Asia lubricants market, given regional supply-chain integration.

Stricter Bans on High-Sulfur/Non-Biodegradable Oils

Environmental agencies tighten sulfur and toxicity thresholds, compelling expensive reformulations. Singapore’s 2025 Hazardous Chemical Controls upgrade stipulates new import permits and stricter warehouse standards[2]“Hazardous Chemical Controls Update,” Singapore Ministry of Manpower, mom.gov.sg. China’s gasoline-engine-oil rules, effective July 2024, cap sulfur and phosphorus while mandating biodegradability for marine uses. Japan and South Korea have advanced similar measures under their chemical substance laws. Compliance favors multinationals with dedicated research and development, while smaller domestic blenders risk market exit, amplifying competitive consolidation in the East Asia lubricants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Premium Grades Drive Incremental Growth

Automotive engine oils retained a 35.02% slice of the East Asia lubricants market in 2025, reflecting the still-large in-service vehicle parc. The sub-segment, however, is flat as EV substitution accelerates. Industrial engine oils, in contrast, record a 0.20% CAGR on the back of new gas-turbine peaker plants, distributed generation assets, and combined-cycle upgrades across China and South Korea. Metalworking fluids gain from aerospace component machining in China and high-precision tooling in Japan. Process oil demand is linked to polymer output, particularly ethylene-propylene rubber in South Korea and white oils for cosmetics in China. Grease formulations are transitioning from lithium-thickened types to polyurea and calcium-sulfonate grades, driven by lithium price volatility and the need for higher mechanical stability. Brake-fluid volumes contract modestly, but higher-dry-boiling-point DOT 4+ blends support value retention. The product mix tilts steadily toward synthetics and semi-synthetics, a pathway that allows suppliers to defend margins despite flat overall volumes in the East Asia lubricants market.

Synthetic grades are gaining wider customer acceptance as OEM drain intervals are extended. Group III+, PAO, and ester chemistries enable ultra-low-viscosity 0W-16 and 0W-8 engine oils tested under Japan’s JASO GLV-1 framework. Specialty turbine and compressor oils exploiting gas-to-liquid base stocks demonstrate superior varnish control, vital for LNG plants and PET bottle resin lines. Data-center immersion fluids and EV gear oils appear small but grow at double-digit rates. As technology filters through, even traditional segments such as gear and hydraulic oils increasingly specify advanced anti-wear and oxidation chemistries. Consequently, premium product lines outpace commodity ones, a shift that underpins revenue resilience in the East Asia lubricants market.

By End-User Industry: Industrial Applications Gain Momentum

Automotive users still account for 41.95% of 2025 volumes, spanning passenger cars, commercial trucks, and two-wheelers. Yet volume erosion is visible as EV adoption rises and public transport upgrades reduce private car miles in metropolitan China. Fleet operators shift to long-drain synthetics to reduce maintenance downtime, thereby elevating the per-liter value even as the number of liters decreases. Industrial consumers show sturdier prospects with a 0.14% CAGR, buoyed by semiconductor fabrication, petrochemicals, and renewable-energy assets. Power plants require turbo machinery oils that can withstand high-bearing loads. Marine lubricants adapt to IMO 2020 sulfur caps, spurring sales of low-BN cylinder oils for scrubber-equipped vessels departing Korean and Japanese yards.

Mining fleets in Mongolia and northern China require ISO 68 hydraulic oils that maintain viscosity at sub-zero temperatures, while agriculture in northeast China utilizes gearbox oils for autonomous tractors. Aerospace assembly lines, notably those of COMAC and Mitsubishi Heavy Industries, utilize AS9100-certified specialty fluids. Each industrial vertical values reliability and compliance over price, a dynamic that reallocates supplier focus away from shrinking automotive pools to higher-margin factory and infrastructure niches inside the East Asia lubricants market.

By Base Stock Type: Sustainability Drives Formulation Evolution

Mineral-oil grades capture 58.22% of 2025 demand, underpinned by cost-sensitive customers in trucking, small-engine, and general manufacturing segments. The share will likely trend lower as bio-based and synthetic alternatives continue to expand. Bio-based volumes rise at 0.43% CAGR as government procurement in Japan and Singapore favors renewable-content hydraulics for waterfront and forestry equipment. Users value rapid biodegradation and low ecotoxicity, which eases permitting near protected habitats. Synthetics preserve price premiums but win market share where extreme temperature stability and low volatility are key considerations. Semi-synthetics serve as transitional solutions, pairing mineral stocks with Group III fractions to strike a balance between cost and performance.

The East Asia lubricants market size for synthetics is expected to benefit from Asian refinery upgrades that increase Group III yields, such as Chevron’s Singapore improvement plan. Feedstock security also improves with the establishment of new import terminals in Taiwan and northern China. Bio-feedstock supply remains tight, constrained by limited rapeseed and palm-ester streams, but chemical recyclers and algae-oil prototypes could broaden the base beyond 2028. The sustainability lens, therefore, prompts formulators to optimize additive treatment rates for lower sulfur and phosphorus levels while maintaining performance amid longer drain times.

Geography Analysis

China supplied 69.05% of regional liters in 2025 owing to its vast industrial ecosystem and road-transport fleet. Updated GB engine oil standards, effective July 2024, escalate detergent and dispersant requirements, thereby increasing formulation complexity and cost. Domestic majors Sinopec and PetroChina respond with new CJ-4 and SP lines that directly compete with Shell and ExxonMobil. Taiwan, although holding a smaller base, leads with a 0.85% CAGR as TSMC and its peers expand 2 nm and 1.6 nm fabs, which require ultra-clean lubricants, and as hyperscale data centers deploy immersion cooling. Japan’s demand is concentrated in the robotics, renewable energy, and marine sectors, where lubricant uptime is critical for cost control. South Korea leverages its shipbuilding and petrochemical heft, buying trunk-piston cylinder oils, process oils, and PAO-based compressor fluids. Collectively, these market shapes ensure that the East Asia lubricants market remains volume-flat yet value-positive.

Competitive Landscape

The East Asia lubricants market is moderately consolidated. Chinese titans hold dominant domestic positions with state-backed retail networks, while Japan’s ENEOS and South Korea’s SK Lubricants excel in specialty synthetics tailored to their domestic OEM standards. Market rivalry centers on technical differentiation, rapid regulatory compliance, and the security of high-VI base stocks, rather than headline capacity additions. Strategic moves illustrate this emphasis. Integration into OEM service programs offers an extra moat. ExxonMobil renews decade-long links with Toyota for factory fills in Thailand and engine oil co-development in Japan. The ability to co-engineer fluids with equipment makers secures multi-year streams insulated from spot-pricing skirmishes, a critical buffer in the low-growth East Asian lubricants market.

East Asia Lubricants Industry Leaders

ENEOS Corporation

China Petrochemical Corporation

Shell plc

Idemitsu Kosan Co. Ltd

SK Enmove Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP p.l.c initiated a sale process for its Castrol lubricants division, valued at up to USD 10 billion, as part of a USD 20 billion divestment program scheduled through 2027.

- November 2024: PTT Lubricants launched EVOTEC Technology in Taiwan, a platform of advanced engine oil formulations focused on endurance and efficiency gains, bolstering its presence in the motorcycle and passenger car channels.

East Asia Lubricants Market Report Scope

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| China |

| South Korea |

| Japan |

| Taiwan |

| Others (Mongolia, Hong Kong) |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

| By Geography | China | |

| South Korea | ||

| Japan | ||

| Taiwan | ||

| Others (Mongolia, Hong Kong) | ||

Key Questions Answered in the Report

What volume does the East Asia lubricants market reach in 2026?

The region is projected to consume 11.05 billion liters in 2026.

Which product category commands the largest share in 2025?

Automotive engine oils lead with 35.02% of the total volume.

How quickly are industrial engine oils expanding?

They advance at a 0.20% CAGR through 2031, the fastest among product lines.

What is the main driver behind the shift to low-viscosity blends?

Stricter fuel-economy rules in China and Japan, combined with corporate carbon goals, push users toward 0W-20 and 0W-16 formulations.

How does rapid EV adoption influence lubricant demand?

Electric vehicles cut engine-oil volumes but open niche opportunities for specialty gear and thermal-management fluids.

Page last updated on: