South-East Asia And Oceania Lubricants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

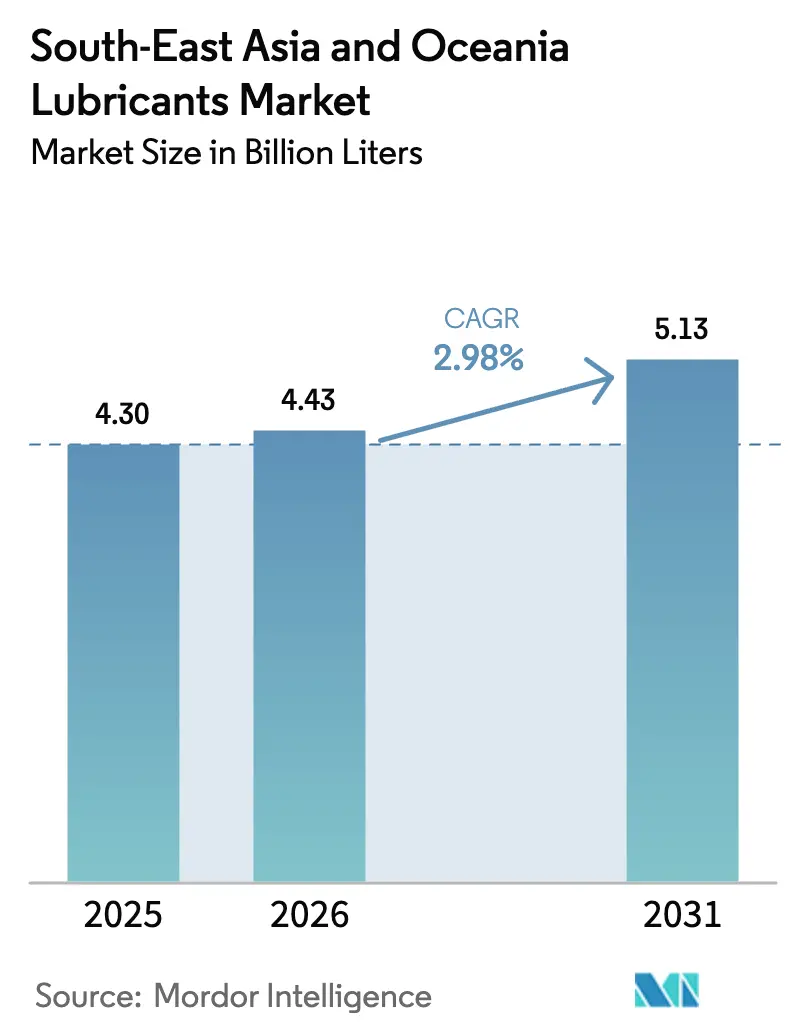

| Base Year Market Size (2025) | 4.30 Billion liters |

| Market Volume (2026) | 4.43 Billion liters |

| Market Volume (2031) | 5.13 Billion liters |

| Growth Rate (2026 - 2031) | 2.98% CAGR |

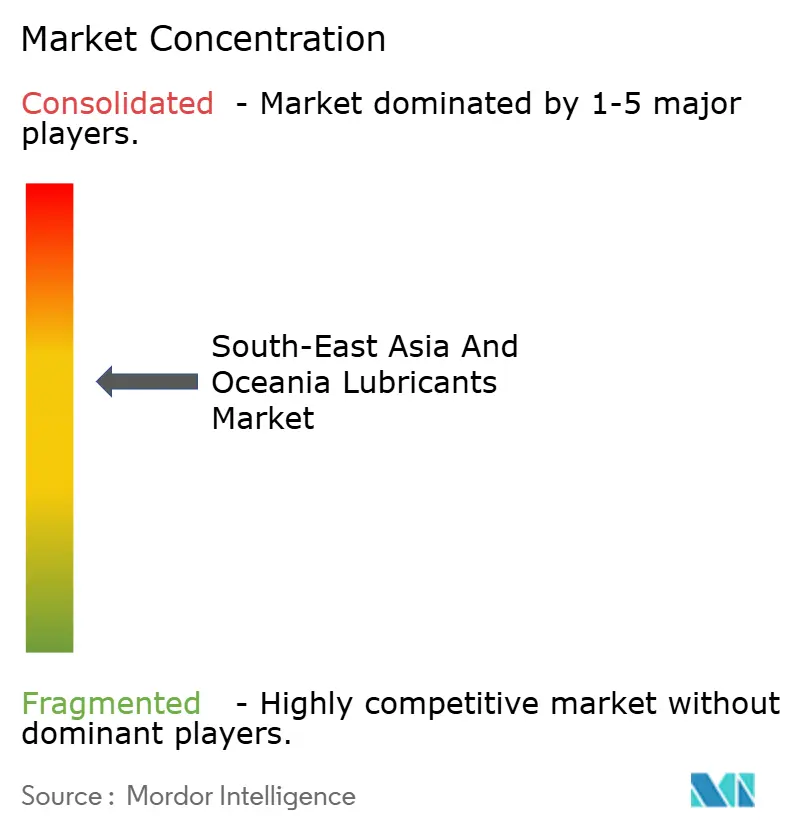

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South-East Asia And Oceania Lubricants Market Analysis by Mordor Intelligence

The South-East Asia and Oceania Lubricants Market size is expected to grow from 4.30 billion liters in 2025 to 4.43 billion liters in 2026 and is forecast to reach 5.13 billion liters by 2031 at 2.98% CAGR over 2026-2031. Manufacturing resurgence across Indonesia, Vietnam, and Thailand, coupled with large-scale infrastructure programs, anchors this expansion as global supply chains diversify toward the region. Rising automotive production, mining capital expenditures, and demand for construction equipment reinforce lubricant consumption, while regulatory shifts favoring synthetic and bio-based formulations open up premium-pricing opportunities. Competitive behavior remains fragmented yet poised for mid-tier consolidation in the wake of Saudi Aramco’s downstream push and BP’s potential exit from Castrol. Counterfeit clamp-downs in Malaysia and Indonesia further tilt share toward established brands with certified supply chains.

Key Report Takeaways

- By product type, automotive engine oil commanded 28.62% revenue share in 2025, while industrial engine oil is forecast to expand at 2.22% CAGR to 2031.

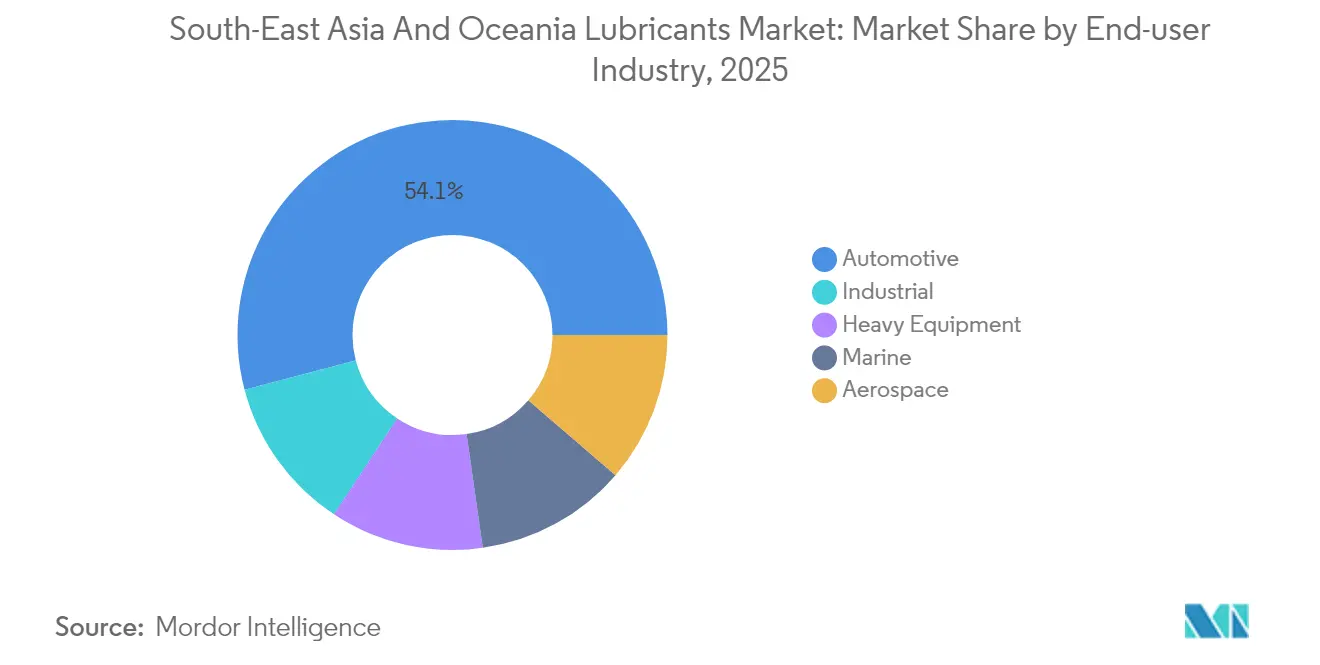

- By end-user, automotive applications accounted for 54.10% of demand in 2025; industrial users are expected to record the highest CAGR of 2.12% through 2031.

- By base stock, mineral formulations retained a 58.31% share in 2025, yet bio-based lubricants are poised for a 3.05% CAGR on sustainability mandates.

- By geography, Indonesia led the South-east Asia and Oceania lubricants market with 28.10% of the market share in 2025; Australia is projected to post the fastest growth at a 3.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South-East Asia And Oceania Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic rebound in transport and logistics | +0.8% | Indonesia, Thailand, Vietnam | Short term (≤ 2 years) |

| Manufacturing boom in Indonesia, Vietnam and Thailand | +1.1% | Indonesia, Vietnam, Thailand | Medium term (2-4 years) |

| Mining and construction upcycle lifting heavy-duty demand | +0.6% | Australia, Indonesia, Philippines | Long term (≥ 4 years) |

| Rapid switch to synthetics across ASEAN and Oceania | +0.4% | Singapore, Malaysia | Medium term (2-4 years) |

| Bio-based lubricant uptake on sustainability mandates | +0.3% | Malaysia, Indonesia, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-Pandemic Rebound in Transport and Logistics

Automotive sales in ASEAN increased by 12% in 2024 as supply chain normalization revived fleet purchases, leading to higher lubricant demand. Thailand produced 1.9 million vehicles, stimulating commercial-vehicle lubricant consumption as e-commerce logistics scaled. Fleets shifted to higher-viscosity API CK-4 and JASO DH-2 oils, which carry premium price points, thereby improving distributor margins. The expansion of last-mile delivery in Vietnam and Indonesia accelerated the drain-interval optimization programs, increasing synthetic penetration. Regional trucking firms mandated telematics-enabled maintenance regimes, indirectly boosting consumption through shorter oil-change intervals in heavy urban cycles.

Manufacturing Boom in Indonesia, Vietnam, and Thailand

Foreign direct investment in electronics, textiles, and automotive assembly reached USD 15.8 billion in Vietnam in 2024, underpinning sustained demand for metalworking fluids and spindle oils[1]Tran Nguyen, “FDI Manufacturing Inflows Reach USD 15.8 Billion,” Vietnam Investment Review, vir.com.vn. Indonesia’s plan for 50 new industrial estates by 2030 standardizes lubricant supply tenders, offering multi-year volume visibility. Thailand’s Eastern Economic Corridor continues to attract petrochemical expansions requiring turbine and compressor fluids compliant with ISO 21469 hygiene standards. OEMs favor suppliers with in-country blending plants, prompting capacity additions by Shell and PETRONAS. Automation upticks elevate hydraulic-fluid specifications for fire-resistance and narrower viscosity indices.

Mining and Construction Upcycle Lifting Heavy-Duty Demand

Australia’s mining sector logged an 8% rise in lubricant consumption during 2024 as iron ore and lithium projects revamped fleets. Indonesia’s nickel output ambitions necessitate high-temperature greases and EP gear oils that can withstand corrosive ore-handling environments. ASEAN construction equipment imports climbed 15%, amplifying demand for hydraulic fluids with anti-wear zinc-free chemistries suitable for tropical humidity. The Philippines' expressway projects lengthen operating hours, accentuating the need for extended-drain formulations. Wear-metals monitoring services bundled with lubricant supply contracts gained popularity, locking in recurring revenue.

Rapid Switch to Synthetics Across ASEAN and Oceania

OEM warranty requirements for Group III and PAO oils accelerated the uptake of synthetic oils, with Singaporean ship operators reporting 3-5% fuel efficiency gains from low-friction marine lubricants. Heat-stress conditions above 40°C in Jakarta and Manila accelerated the migration from mineral to synthetic engine oils, resulting in superior oxidative stability. Logistic fleet trials in Malaysia validated 20,000-km drain intervals, resulting in reduced downtime and total cost of ownership. Electric forklifts in Vietnamese factories continue to use synthetic gearbox oils for load handling. Cross-indemnification clauses in OEM service contracts increasingly specify ACEA E8/E11 compliant synthetics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and grey-market products | -0.5% | Malaysia, Indonesia, Philippines | Short term (≤ 2 years) |

| Base-oil price volatility | -0.3% | Import-dependent markets | Medium term (2-4 years) |

| EV penetration trimming ICE demand | -0.4% | Thailand, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Grey-Market Products Eroding Margins

Malaysian police seized RM 1.15 million worth of fake lubricants in 2024, reflecting a persistent illicit trade that undercuts branded pricing and erodes consumer trust. Advanced holographic seals and QR-verified packaging raise operating costs for legitimate suppliers. Indonesia’s 2025 SNI upgrade tightens quality thresholds; however, enforcement gaps persist in rural outlets, where price sensitivity often dominates purchasing decisions. Branded distributors invest in route-to-market audits and GPS-tracked delivery to assure provenance. Training programs with automotive repair chains promote genuine product differentiation, but gray imports still dampen revenue growth forecasts by 0.5 percentage points.

EV Penetration Curbing Long-Term ICE Lubricant Growth

Thailand’s EV sales skyrocketed 700% in 2024 to 89,000 units, supported by tax incentives and domestic battery production, signaling a structural shift away from ICE oils[2]Thailand Board of Investment, “Thailand EV Sales Surge,” boi.go.th. Singapore’s 2030 ICE phase-out timeline likewise compresses long-run engine oil volumes. However, specialized dielectric and thermal-management fluids for electric drivetrains open nascent revenue streams. Lubricant producers retool their R&D to develop greases compatible with high-speed electric motor bearings. Battery-coolant adoption still lags due to limited OEM standardization, muting near-term volume offsets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oils Retain Primacy amid Rising Industrial Demand

Automotive engine oils accounted for a 28.62% share of the South-East Asia and Oceania lubricants market in 2025, supported by the region’s sizable passenger-car and motorcycle parc. Industrial engine oils are expected to surpass other categories with a 2.22% CAGR to 2031 as power-generation and backup-generator installations scale across data center clusters. Higher-spec JASO M364:2024 formulations fetch premium margins, benefiting suppliers with additive-technology leadership. Process oils ride tire-manufacturing growth in Thailand and Malaysia, while metalworking fluids serve electronics hubs in Vietnam and Singapore. Transmission and gear oils track commercial-vehicle sales, while brake-fluid demand aligns with increased vehicle exports from Thailand’s assembly lines.

Automotive engine oils will continue to dominate absolute volumes; however, their share will gradually dilute as industrial diversification outpaces vehicle fleet growth. Suppliers invest in condition-monitoring services to secure repeat sales and differentiate commoditized products. Environmental legislation nudges OEMs toward low-SAP oils, shifting formulation complexity upward. Regional refineries are expanding their Group II/III output to support a premium product mix and reduce import dependence for high-viscosity index stocks.

By End-User Industry: Automotive Still Leads but Industry Gains Momentum

Automotive applications accounted for 54.10% of 2025 demand, driven primarily by the dominance of two-wheelers in Indonesia and Thailand. Industrial users, however, are expected to post the strongest 2.12% CAGR, reflecting broad-based growth in manufacturing, power, and resource extraction. Marine demand, centered on Singapore’s bunkering operations, benefits from IMO 2020 low-sulfur fuel mandates that require compatible cylinder oils. Heavy-equipment segments draw increased volumes from mining in Australia and nickel processing in Indonesia. Aerospace remains a niche yet strategic sector, with Singapore’s MRO cluster dictating premium turbine oil specifications.

Power-generation operators prioritize high-TBN oils to cope with the combustion of low-sulfur fuels, thereby extending drain intervals in remote grids. Metallurgy and metal-fabrication activities align lubricant consumption with the growth of electronics exports in Vietnam. OEM service contracts are increasingly bundling lubricant supply, favoring brands with extensive technical-service footprints. Supply-chain digitalization enables predictive replenishment, reduces stockouts, and stabilizes industrial consumption patterns.

By Base Stock Type: Mineral Dominance Gives Way to Synthetic and Bio Growth

Mineral oils held a 58.31% share in 2025, but synthetics and bio-based variants collectively outpaced them through 2031 as regulations tightened on performance and environmental metrics. Semi-synthetic blends offer cost-effective upgrades for fleets seeking longer drain intervals without full synthetic premiums. Group III and PAO stocks underpin marine and high-temperature industrial oils, while esters gain attention in aviation and high-speed spindle applications. Bio-based lubricants, derived largely from palm oil, meet biodegradability standards for marine and forestry equipment.

The South-east Asia and Oceania lubricants market size for bio-based formulations is forecast to register a 3.05% CAGR, supported by green-procurement policies and OEM endorsement. Indonesia’s SNI revisions and Malaysia’s SIRIM certification elevate entry barriers for low-quality mineral imports, nudging users toward higher-performance alternatives. Blenders in Singapore leverage tariff-free re-export status to supply premium synthetics across the region. Additive-supply security becomes critical as global manufacturers rationalize their footprint, positioning local toll-blenders with diverse sourcing at an advantage. Cost parity between synthetic blends and higher-quality mineral oils narrows, encouraging migration up the value curve.

Geography Analysis

Indonesia commanded a 28.10% share of the South-East Asia and Oceania lubricants market in 2025, thanks to its 280 million population and motorcycle-centric mobility patterns. Rapid growth in nickel mining and the establishment of new textile parks drive industrial fluid demand. Shell’s USD 300 million blending plant expansion to 300 million liters annually underscores its confidence in sustained volume growth.

Australia is the fastest-growing market, on track for a 3.56% CAGR, driven by mining fleet modernization and environmental mandates favoring biodegradable hydraulics in sensitive regions. Stringent work-site regulations reward suppliers with low-toxicity, fire-resistant formulations. The uptake of construction equipment linked to resource corridors boosts demand for high-performance gear oils designed for extreme loads.

Thailand and Malaysia sustain meaningful volumes through automotive manufacturing clusters, petrochemical complexes, and palm-oil processing plants that absorb specialty process oils. Singapore, although small in absolute terms, wields outsized influence through marine bunkering, accounting for 25% of global ship refueling and dictating cylinder-oil specification trends. Vietnam’s 2024 FDI inflow of USD 15.8 billion catalyzes metalworking and industrial-lube consumption, while the Philippines rides construction and mining capex cycles despite counterfeit challenges in rural distribution.

Competitive Landscape

The South-East Asia and Oceania Lubricants Market is moderately concentrated, with the top five players accounting for the majority of the 2024 volumes. Saudi Aramco’s USD 1 billion purchase of Shell’s Malaysian retail network widens downstream reach and signals further consolidation potential. BP’s strategic review of Castrol highlights portfolio repositioning as oil majors shift their focus to renewables. Intellectual property protection and OEM approvals differentiate incumbents from fringe players. Adherence to API 1560 and JASO standards adds testing cost layers that smaller players struggle to absorb. Counterfeit crackdowns and evolving SIRIM/SNI protocols further squeeze informal operators, nudging the competitive mix toward scale players with traceable supply chains and in-house expertise in additives.

South-East Asia And Oceania Lubricants Industry Leaders

BP p.l.c.

Shell plc

Exxon Mobil Corporation

PETRONAS Lubricants International

Chevron Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP p.l.c. announced plans to divest its global Castrol lubricants division, valued at up to USD 10 billion, as part of a broader USD 20 billion asset-rotation strategy aimed at funding upstream projects.

- May 2025: Lubrizol appointed IMCD Group as its channel partner for lubricant and fuel additive distribution in Vietnam, enabling broader access to specialty technology for domestic blenders.

South-East Asia And Oceania Lubricants Market Report Scope

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| Malaysia |

| Singapore |

| Thailand |

| Vietnam |

| Indonesia |

| Philippines |

| Australia |

| Others (New Zealand, Cambodia and Myanmar) |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

| By Geography | Malaysia | |

| Singapore | ||

| Thailand | ||

| Vietnam | ||

| Indonesia | ||

| Philippines | ||

| Australia | ||

| Others (New Zealand, Cambodia and Myanmar) | ||

Key Questions Answered in the Report

What is the current size of the South-East Asia and Oceania lubricants market?

The market stands at 4.43 billion liters in 2026 and is projected to hit 5.13 billion liters by 2031.

Which country is the largest consumer of lubricants in the region?

Indonesia leads with 28.10% share thanks to its large population and extensive two-wheeler fleet.

Which segment is growing the fastest?

Industrial engine oils are expected to post a 2.22% CAGR to 2031 on the back of manufacturing and power-generation growth.

How will electric vehicles affect lubricant demand?

EV adoption curbs long-term engine-oil volumes but opens new demand for specialized thermal-management and gearbox fluids.

Why are synthetic lubricants gaining traction?

OEM warranty requirements and high ambient temperatures push users toward Group III and PAO formulations that offer longer drain intervals and better oxidative stability.

Page last updated on: