Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | 3.78 Billion liters |

| Market Volume (2026) | 3.89 Billion liters |

| Market Volume (2031) | 4.48 Billion liters |

| Growth Rate (2026 - 2031) | 2.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Lubricants Market Analysis by Mordor Intelligence

The ASEAN Lubricants Market size is projected to be 3.78 Billion liters in 2025, 3.89 Billion liters in 2026, and reach 4.48 Billion liters by 2031, growing at a CAGR of 2.88% from 2026 to 2031. This steady trajectory reflects the intersection of longer drain intervals made possible by synthetic formulations, the first meaningful uptick in electrified power-trains, and input-cost swings that compress blender margins. Base-oil investments in Singapore, refinery constraints in Vietnam, and biodiesel mandates in Indonesia are reshaping trade flows and blurring the historical line between domestic and cross-border supply. Competitive strategies are coalescing around synthetic premiumization, service-layer digitization, and supply-chain hedging that links base-stock security with additive integration. These shifts give the ASEAN lubricants market new opportunities in industrial equipment, marine bunkering, and predictive-maintenance bundles while tempering growth in traditional passenger-car engine oils.

Key Report Takeaways

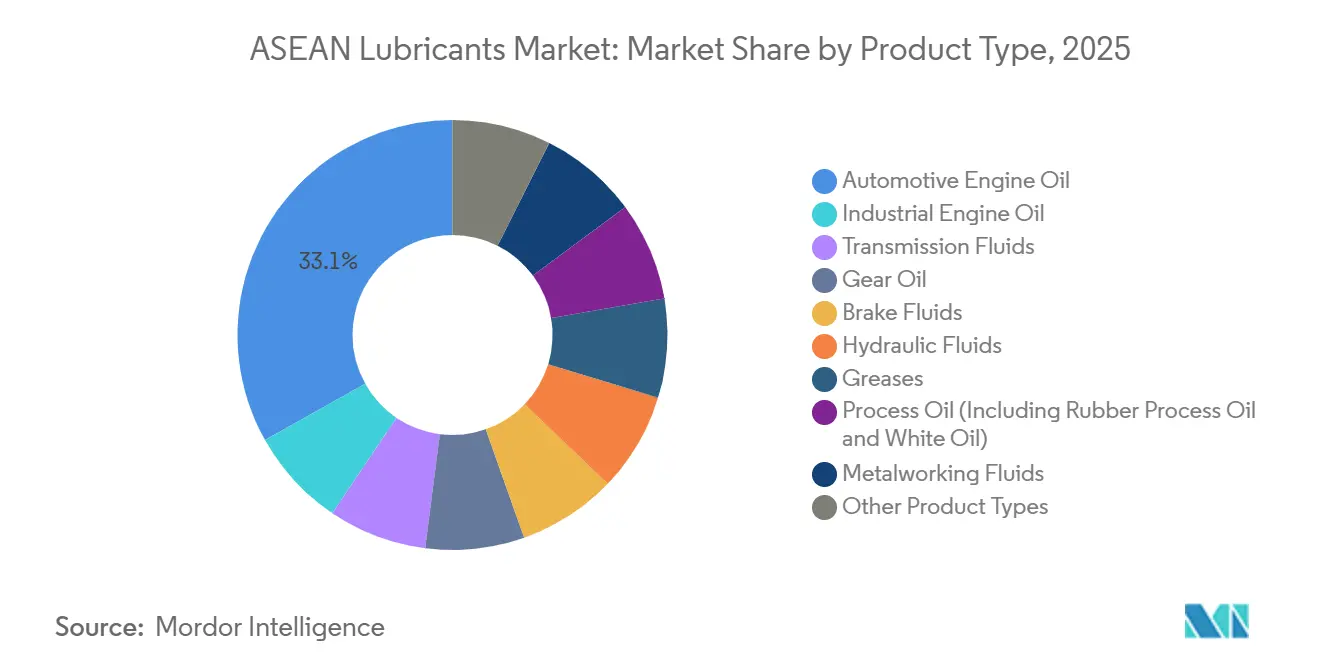

- By product type, automotive engine oil held 33.12% of the ASEAN lubricants market share in 2025 while industrial engine oil is forecast to grow at a 2.96% CAGR through 2031.

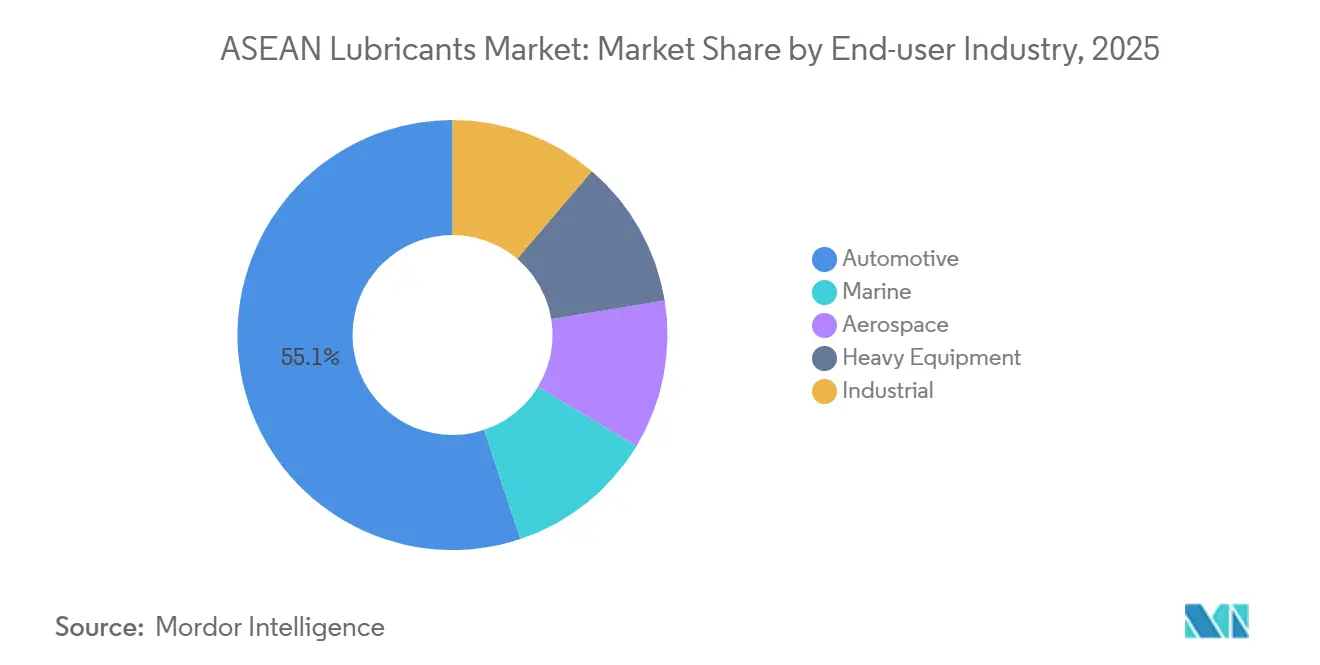

- By end-user industry, the automotive segment captured 55.12% volume in 2025 whereas the industrial segment is expected to post a 2.83% CAGR to 2031.

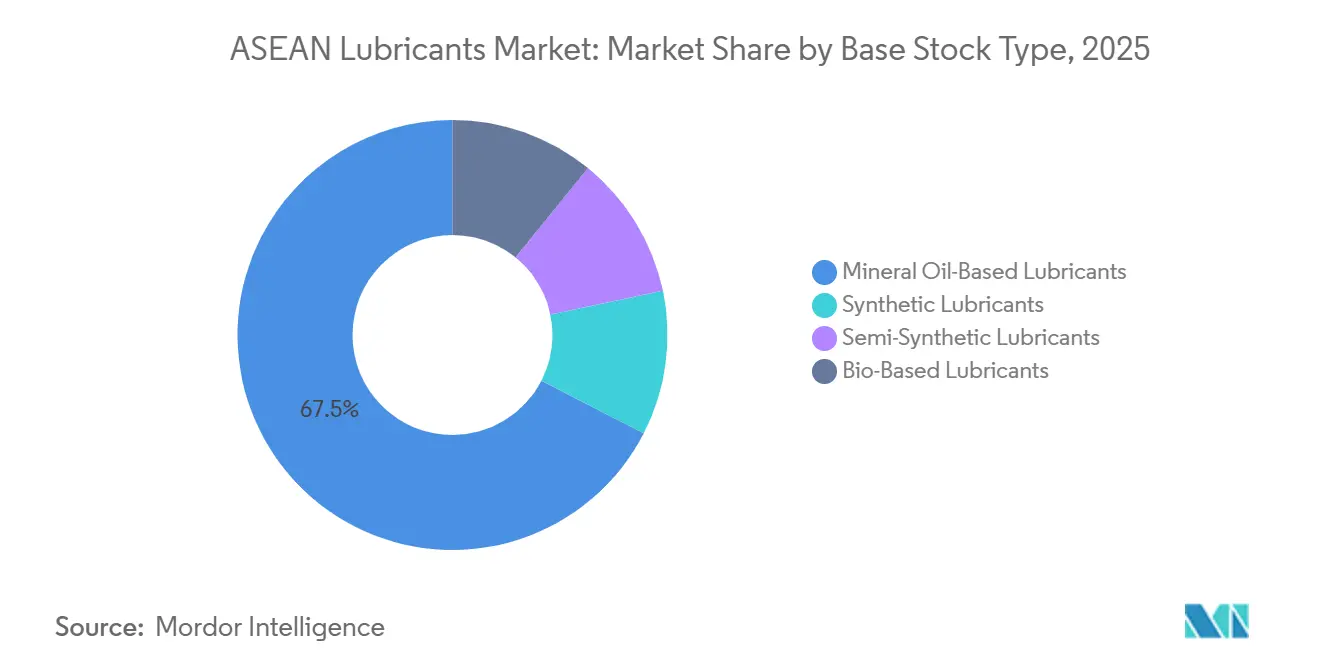

- By base-stock type, mineral oils controlled 67.45% of 2025 volumes and bio-based lubricants represent the fastest growth at a 3.36% CAGR to 2031.

- By geography, Indonesia accounted for 31.46% of 2025 volume yet Vietnam is projected to lead with a 3.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

ASEAN Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing vehicle parc and freight movement | +0.8% | Indonesia, Thailand, Vietnam, Philippines | Medium term (2-4 years) |

| Rapid industrialisation and manufacturing expansion | +0.7% | Vietnam, Indonesia, Thailand | Long term (≥4 years) |

| Shift towards high-performance synthetic lubricants | +0.5% | Singapore, Malaysia, Thailand | Medium term (2-4 years) |

| Digitalised distribution and predictive-lubrication services | +0.3% | Singapore, Malaysia, urban Indonesia and Thailand | Long term (≥4 years) |

| Rise of ASEAN marine-bunkering hubs | +0.4% | Singapore, Malaysia (Port Klang, Johor) | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Growing Vehicle Parc and Freight Movement

Commercial and passenger fleets continue to swell, yet two-wheeler dominance in Indonesia and Vietnam shifts demand toward small-sump volumes that turn over faster than car lubricants. Philippines automakers plan to assemble 480 000 units in 2025 while Malaysia produced 738 000 units in 2024 and targets 750 000 in 2025[1]Chamber of Automotive Manufacturers of the Philippines, “Industry Performance,” campi.com.ph. Freight growth tied to USD 222 billion in 2024 FDI inflows increases duty cycles for trucks and construction machinery. Suppliers that tailor two-wheeler and commercial-vehicle oils with enhanced shear stability and detergent chemistry benefit from higher replacement frequency. PETRONAS Sprinta and Mobil Super Moto lines already exploit this dynamic, reinforcing why the ASEAN lubricants market will keep an automotive volume edge even as per-unit consumption falls.

Rapid Industrialisation and Manufacturing Expansion

Relocation of electronics, semiconductor, and renewable component plants from China into Vietnam, Indonesia, and Thailand is lifting consumption of metalworking fluids, hydraulic oils, and turbine oils. The International Energy Agency sees regional oil use in industry rising to 6.4 million bpd by 2030 as new fabs and data centers go live[2]International Energy Agency, “Southeast Asia Energy Outlook 2024,” iea.org. Specialty additive demand is advancing faster than commodity grades, as shown by PETRONAS Chemicals which cited higher engineered-fluid sales in early 2024 despite weaker additive margins. This diversification makes the ASEAN lubricants market less tied to passenger-car cycles and more dependent on capital-equipment investments.

Shift Towards High-Performance Synthetic Lubricants

OEM factory-fill specifications for low-viscosity synthetics lock in aftermarket pull-through. PTT Lubricants’ EVOTEC platform, TotalEnergies’ expanded solar-powered Singapore blender, and ExxonMobil’s focus on PAO and ester base stocks illustrate the pivot toward higher margin fluids that extend drain intervals and boost fuel economy. Distributors face working-capital pressure because synthetic SKUs move slowly outside major metros, yet predictive analytics can refine stocking strategy and mitigate inventory risk.

Digitalised Distribution and Predictive-Lubrication Services

Condition-monitoring sensors that track viscosity, base number, and ferrous debris are embedding lubricants into broader maintenance contracts. Shell data show maintenance cost savings above 20% when predictive analytics guide oil changes. Castrol’s Fleet Health AI reports one-third fleet cost reduction and has convinced 74% of managers to invest in telematics despite patchy 5G coverage. In the ASEAN lubricants market, larger blenders pair fluids with dashboards and API integrations that raise switching costs and secure fleet loyalty.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Longer drain intervals in modern engines | -0.6% | Singapore, Malaysia, urban Thailand and Indonesia | Medium term (2-4 years) |

| Base-oil price volatility | -0.4% | All ASEAN, linked to Brent | Short term (≤2 years) |

| Accelerated EV adoption in key states | -0.5% | Thailand, Indonesia, Singapore | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Longer Drain Intervals in Modern Engines

Synthetic multigrades that meet ACEA C5 and API SP extend service intervals to 20 000 km, halving annual per-vehicle demand. Liqui Moly guidance and OEM validation of TotalEnergies Quartz EV-Drive show viscosity stability beyond 100,000 km. Blenders respond by upselling synthetics at a 30% price premium yet must invest in mechanic training and point-of-sale promotion in cost-sensitive markets.

Base-Oil Price Volatility

Average product prices fell in early 2024 even as silicone prices rose after an unplanned Chinese outage, underscoring how tight supply can detach from crude trends. ExxonMobil’s new Group II stream in Singapore alleviates some spot exposure, but Indonesia’s B40 mandate diverts feedstock toward biofuel and tightens base-stock pools. Regional players with limited hedging capacity endure the sharpest margin compression.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Industrial Oils Outpace Automotive in Growth

Automotive engine oil held 33.12% volume share in 2025, yet industrial engine oil is forecast to grow at 2.96% CAGR through 2031, the fastest rate among all product types, reflecting ASEAN's manufacturing buildout and power-generation investments that now rival passenger-vehicle parc expansion as the primary demand vector. Transmission fluids, gear oils, and brake fluids collectively serve the automotive drivetrain segment, where the shift to dual-clutch transmissions (DCT) in China and continuously variable transmissions (CVT) in Japan is spilling into ASEAN OEM specifications, requiring ATF formulations with enhanced shear stability and friction modifiers. Metalworking fluids benefit from clean-room manufacturing where bio-stable emulsions cut disposal costs. The ASEAN lubricants market size for turbine oils is poised to expand alongside gas-fired peaking plants that balance rising renewable penetration. Process oils remain a stable niche tied to tire and pharmaceutical output where food-grade white oils command premium pricing.

A dedicated grease wave is unfolding. Shell’s new Indonesian plant adds 12 million liters of capacity for lithium and calcium sulfonate greases that serve automotive bearings, industrial machinery, and marine deck equipment. Castrol’s electric-vehicle greases are engineered for electrical compatibility and reduced rolling resistance, a design that supports the 13,478 EV sales logged in Malaysia during 2024. Bio-based greases using ester base stocks already meet maritime biodegradability mandates and deliver the fastest gains within the broader lubricant basket.

By End-User Industry: Industrial Segment Closes Gap on Automotive Dominance

Automotive applications still deliver 55.12% of 2025 volume, yet industrial end users will add most incremental liters through 2031. Two-wheelers contribute outsize demand thanks to Indonesia and Vietnam each exceeding 100 million registered motorcycles, a figure that cements high-frequency oil changes despite small sump volumes. Commercial vehicles maintain demand as e-commerce drives last-mile logistics throughout the ASEAN lubricants market. Marine volumes climb in tandem with record bunker throughput at Singapore and Port Klang where B30 blends require high-alkaline cylinder oils.

The industrial segment is forecast to grow at 2.83% CAGR through 2031, narrowing the gap as manufacturing, power generation, and heavy equipment demand accelerates. Industrial users exhibit diversified needs. Metalworking shops in Vietnam, semiconductor clean rooms in Malaysia, and gas turbines across Thailand all rely on high-performance fluids with stringent cleanliness and oxidation profiles. PETRONAS reports aviation turbine oil sales rising alongside air travel recovery, while mining operations adopt predictive-maintenance platforms that bundle lubrication, edge sensors, and analytics. Industrial buyers value service reliability and technical support more than headline price, a contrast that helps premium suppliers grow mix even where volumes lag automotive totals.

By Base Stock Type: Bio-Based Gains Share Despite Mineral Dominance

Mineral oils retain a 67.45% volume stronghold although bio-based lubricants carry the top growth rate at 3.36% CAGR. Synthetic base stocks from ExxonMobil’s 20,000 bpd Singapore expansion and TotalEnergies’ 310,000 tpa blender cater to low-viscosity engine oils and EV driveline fluids that require high viscosity index and oxidative endurance. Semi-synthetics bridge cost gaps in rural channels where full synthetics face resistance.

Bio-based lubricants advance where environmental liability is high, including forestry machinery and harbor equipment subject to spill regulations. EU RED III and SAF quotas influence OEM purchasing across the supply chain, encouraging ester-based fluids even in ASEAN. PETRONAS’ Pengerang biorefinery and its silicone plant in Gebeng supply feedstocks for hybrid formulations that blend mineral, synthetic, and bio components for balanced cost and performance.

Geography Analysis

Indonesia leads with 31.46% of 2025 regional volume, supported by Pertamina Lubricants’ 36% domestic share and 612 430 kl sales in 2024. Vietnam, however, is set for the fastest 3.41% CAGR to 2031 as Idemitsu’s Nghi Son refinery lifts output to 11.4 million t at 120% capacity and manufacturing FDI floods into the north. Thailand balances a mature automotive base with BYD’s new EV plant, implying a pivot from engine oils to EV fluids. Malaysia combines semiconductor growth with Port Klang’s bunkering trade, while Singapore, despite modest consumption, anchors supply logistics thanks to world-scale blending and base-stock capacity.

Vietnam’s outsized growth invites supply chain arbitrage. Tight local base-stock availability raises spot prices for finished lubricants, advantaging importers who store cargo in bonded depots around Hai Phong and Ho Chi Minh City. Government interventions in fuel pricing can magnify spreads, rewarding agile distributors. Rural Vietnam maintains a vast two-wheeler parc, ensuring engine-oil demand remains relevant even as Hanoi and Ho Chi Minh City shift to electric scooters.

Competitive Landscape

The ASEAN Lubricants Market is moderately consolidated. Regional challengers assert home advantage. Pertamina dominates in Indonesia through retail station outreach and government contracts. PTT Lubricants owns strong local share and exports EVOTEC synthetics after winning the Prime Minister’s Export Award. Idemitsu backs its Vietnamese downstream ambitions with refinery supply security. These players grow by matching multinational portfolio breadth with localized distribution and faster regulatory approvals. Technology and service layers increasingly determine differentiation. Predictive maintenance, telematics, and API integration create sticky fleet relationships. Bio-based niche leadership in marine and forestry keeps pricing power for players who certify biodegradability early.

ASEAN Lubricants Industry Leaders

Castrol Limited

Caltex

Shell plc

PT Pertamina (Persero)

Petroliam Nasional Berhad (PETRONAS)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Kixx, a lubricant brand from South Korea, teamed up with GS25, a convenience store chain in Korea, to unveil the first Kixx Station in Vietnam. Kixx Station debuts a service model, merging the purchase of engine oil products with an oil change service. This partnership enables local motorcycle riders to buy authentic Kixx motorcycle engine oils.

- September 2025: Petron Malaysia secured the SIRIM Genuine Product License. This certification, granted under the 2024 Certification and Marking of Engine Oils Order, empowers Petron to seek SIRIM Genuine Product Labels for its engine oils in Malaysia.

ASEAN Lubricants Market Report Scope

Lubricant products are made from a combination of base oils and additives. The composition of base oil in the formulation of lubricants is primarily between 75-90%. Base oils possess lubricating properties and make up to 90% of the final lubricant product.

The market is segmented based on product type, end-user industry, base stock type, and geography. The market is segmented by product type into automotive engine oil, industrial engine oil, transmission fluids, gear oil, brake fluids, hydraulic fluids, greases, process oil, metalworking fluids, turbine oil, transformer oil, and other product types. By end-user industry, the market is segmented into automotive, marine, aerospace, heavy equipment, and industrial. By base stock type, the market is segmented into mineral oil-based lubricants, synthetic lubricants, semi-synthetic lubricants, and bio-based lubricants. The report also covers the size and forecasts for the lubricants market in 6 regional countries. The market sizing and forecasts for each segment are based on volume (liters).

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

By Geography

| Indonesia |

| Malaysia |

| Philippines |

| Singapore |

| Thailand |

| Vietnam |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

| By Geography | Indonesia | |

| Malaysia | ||

| Philippines | ||

| Singapore | ||

| Thailand | ||

| Vietnam | ||

Key Questions Answered in the Report

How large is the ASEAN lubricants market in 2026 and what growth is expected by 2031?

The market stands at 3.89 billion liters in 2026 and is forecast to reach 4.48 billion liters by 2031, reflecting a 2.88% CAGR.

Which product type will grow the fastest through 2031?

Industrial engine oil will grow the fastest at a 2.96% CAGR as manufacturing and power-generation investments rise.

Which country will see the highest growth in lubricant demand?

Vietnam is projected to post a 3.41% CAGR through 2031, the quickest in the region.

What base-stock segment shows the highest growth potential?

Bio-based lubricants carry the fastest growth at a 3.36% CAGR due to marine biodegradability mandates and sustainability goals.

How is electrification affecting lubricant suppliers?

EV adoption reduces engine oil volume but stimulates demand for EV transmission fluids, dielectric coolants, and specialty greases that command higher margins.

Page last updated on: