Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

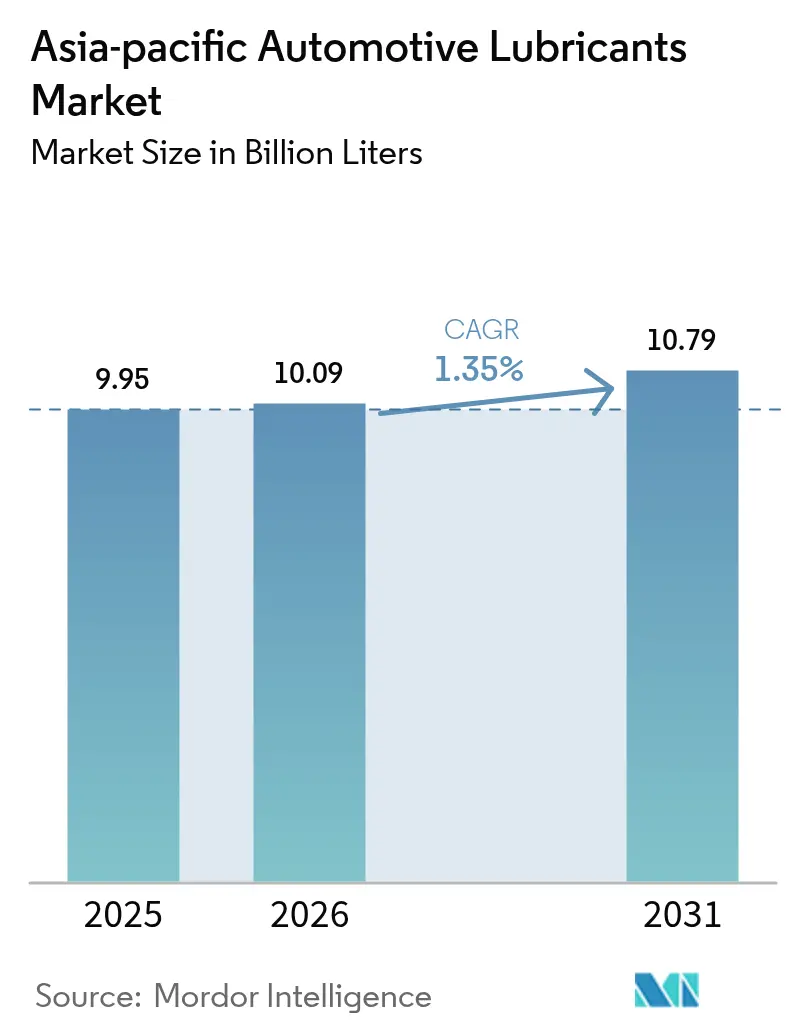

| Base Year Market Size (2025) | 9.95 Billion Liters |

| Market Volume (2026) | 10.09 Billion Liters |

| Market Volume (2031) | 10.79 Billion Liters |

| Growth Rate (2026 - 2031) | 1.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Automotive Lubricants Market Analysis by Mordor Intelligence

Asia-Pacific Automotive Lubricants Market size in 2026 is estimated at 10.09 Billion Liters, growing from 2025 value of 9.95 Billion Liters with 2031 projections showing 10.79 Billion Liters, growing at 1.35% CAGR over 2026-2031. Modest volume growth coexists with an aggressive shift toward premium, low-SAPs formulations that comply with China VI and Bharat VI emission rules while supporting rising factory-fill viscosity requirements. OEM “fill-for-life” mandates lengthen service intervals, prompting blenders to migrate from Group I toward Group II+ and Group III base oils that protect high-temperature turbocharged engines. Simultaneously, automatic transmissions and hybrid powertrains widen the product mix to include shear-stable ATF and e-axle greases, thereby cushioning volume loss from the adoption of electric vehicles. Competitive intensity remains elevated as global majors deploy predictive-maintenance platforms to defend their market share, while regional champions digitize fragmented Southeast Asian channels to maintain pricing power.

Key Report Takeaways

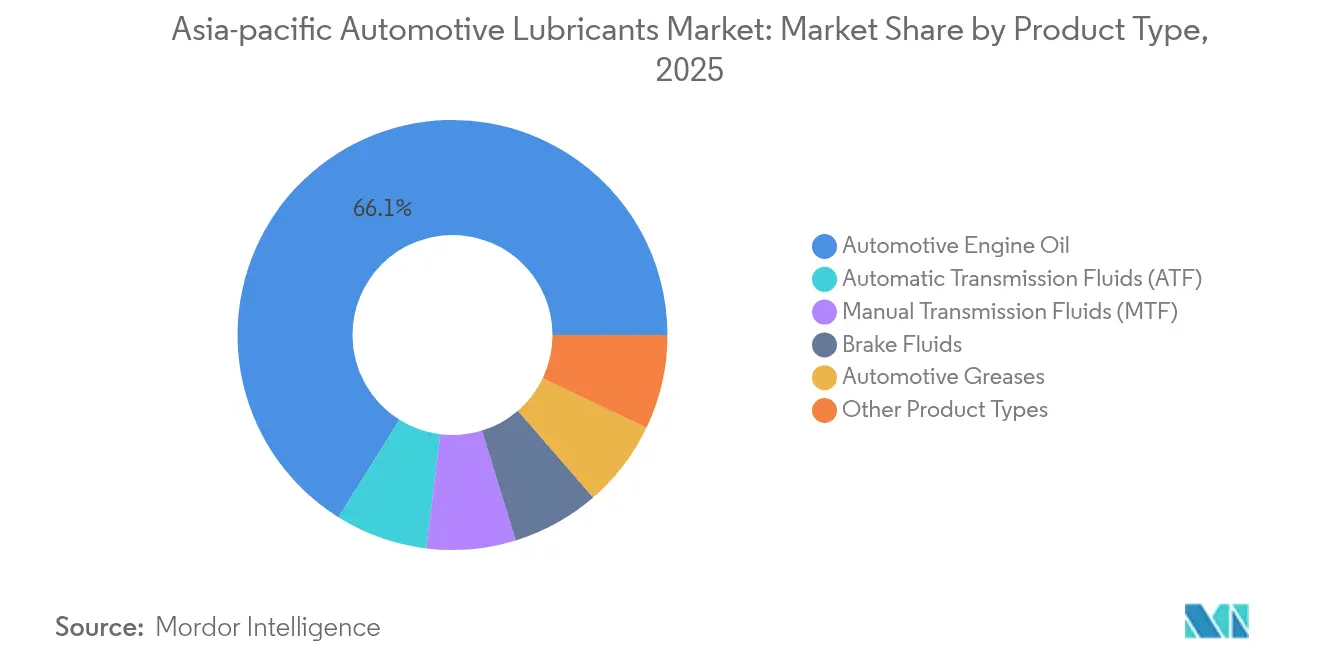

- By product type, automotive engine oil accounted for 66.10% of the market share in 2025. The share of automatic transmission fluids (ATF) is expected to increase with a CAGR of 1.56% during the forecast period (2026-2031).

- By vehicle type, passenger vehicles accounted for 58.30% of consumption in 2025, and the share of commercial vehicles is expected to increase at a CAGR of 1.65% during the forecast period (2026-2031).

- By geography, China held a 34.80% share in 2025, and India's market share is expected to increase at the fastest CAGR of 1.78% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of passenger-car parc | +0.8% | India, Indonesia, Vietnam with spillover to Thailand, Philippines | Medium term (2-4 years) |

| OEM "fill-for-life" mandates boosting lubricant quality | +0.6% | Global, with early adoption in Japan, South Korea, Australia | Long term (≥ 4 years) |

| Rising demand for high-performance synthetic lubes | +0.5% | China, Japan, South Korea, with gradual adoption across ASEAN | Medium term (2-4 years) |

| Explosive growth of e-scooter delivery fleets | +0.3% | Urban centers across China, India, Southeast Asia | Short term (≤ 2 years) |

| China VI & Bharat VI push low-SAPS formulations | +0.4% | China and India primarily, with regulatory spillover to ASEAN markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Passenger-Car Parc

Passenger-car ownership continues to rise in emerging economies, driving demand for lubricants even as the adoption of battery-electric vehicles (BEVs) accelerates. India sold 4.2 million passenger vehicles in fiscal 2024, representing an 8.4% year-over-year increase that pushed the national car parc to surpass 38 million units[1]Society of Indian Automobile Manufacturers, “Vehicle Sales FY 2024,” siam.in. Indonesia rebounded to 1.06 million light-vehicle sales in 2024, while motorcycle registrations surpassed 6.8 million units, underscoring the significant role of two-wheeler oil consumption. Vietnam’s parc expanded at a rate of 12.3% annually as disposable incomes rose and public-transport capacity lagged. With an average vehicle age of over nine years across these markets, aftermarket drain events remain frequent, sustaining the Asia-Pacific Automotive Lubricants Market despite the risk of EV substitution. ISO 14001 certifications adopted by regional workshops further steer buyers toward branded, low-emission lubes that meet environmental audits.

OEM “Fill-for-Life” Mandates Boosting Lubricant Quality

Automakers are increasingly specifying drain intervals of 15,000 km or more under warranty, forcing blenders to upgrade the base-stock quality and additive durability. Toyota’s Global Outstanding Assessment program demands 150,000-km fluid life under JASO GLV-2, effectively locking out Group I feedstocks from factory fill. Hyundai’s Smartstream engines in India require 0W-20 oils that can withstand sump temperatures exceeding 120°C without viscosity shear, resulting in the widespread use of poly-alpha-olefin boosters. Honda’s Earth Dreams powertrains require API SP Resource Conserving approval and low phosphorus to protect catalytic converters. These stringent OEM rules set a quality baseline that cascades through the aftermarket, elevating the Asia-Pacific Automotive Lubricants Market toward synthetics that command higher margins.

Rising Demand for High-Performance Synthetic Lubes

Consumer awareness of fuel-economy benefits, combined with stricter tailpipe emissions limits, drives the adoption of synthetic lubricants. Chinese motorists achieved a 36% synthetic fuel penetration in 2025, up from 29% in 2023, following the nationwide rollout of China VI standards. Japanese vehicle owners already exceed 70% synthetic usage as JASO standards entrench energy-conserving grades. South Korean OEMs promote 0W-20 and 0W-16 viscosity fluids for turbo-gasoline engines, boosting domestic synthetic demand by 7% in 2025. As ASEAN consumers upgrade from mineral to semi-synthetic blends, regional base-oil suppliers invest in Group III expansions that feed localized blending plants. This trajectory enlarges revenue per liter, mitigating flat volumes inside the Asia-Pacific Automotive Lubricants Market.

Explosive Growth of E-Scooter Delivery Fleets

Food-delivery platforms scale urban two-wheeler fleets that clock high mileage under severe, stop-start cycles. Chinese last-mile operators, such as Meituan, deployed more than 1.1 million e-scooters in 2025, each still requiring gearbox oil and fork greases, despite the use of battery powertrains. India licensed over 0.5 million electric scooters for gig-economy riders in 2025, encouraging niche lubricants for hub-motor bearings and hydraulic brakes. Rapid fleet turnover yields frequent workshop visits, even as specialty-fluid consumption increases, despite declining engine-oil liters. Municipal authorities mandate safety inspections every six months, further institutionalizing maintenance spending inside the Asia-Pacific Automotive Lubricants Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Battery-EV penetration lowering lube demand/vehicle | -0.9% | China leading, followed by Japan, South Korea, with gradual ASEAN adoption | Long term (≥ 4 years) |

| Volatile base-oil pricing squeezing margins | -0.4% | Global impact, particularly affecting price-sensitive markets in Southeast Asia | Short term (≤ 2 years) |

| AI-driven extended drain intervals cut volumes | -0.2% | Premium segments in developed markets (Japan, Australia, Singapore) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Battery-EV Penetration Lowering Lube Demand/Vehicle

Pure battery cars need up to 80% fewer lubricants by volume than internal combustion vehicles, eroding per-unit demand. China reached 35.7% BEV share in 2024, supported by BYD and Tesla output surpassing 8 million units. Japan’s purchase subsidy of JPY 850,000 boosted national BEV sales to 3.2% in 2024, despite hybrid vehicles' dominance. South Korea achieved an 8.8% BEV share in 2024, as Hyundai inaugurated the IONIQ 6 sedan. The shift siphons engine oil, though residual ICE fleets require higher-grade synthetics to compensate for extended service intervals, partially offsetting volume loss in the Asia-Pacific Automotive Lubricants Market.

Volatile Base-Oil Pricing Squeezing Margins

Group I spot prices fluctuated between USD 850 and USD 1,200 per metric ton in 2024, as crude volatility and refinery maintenance disruptions affected supply. Group II+ premiums widened beyond USD 300 per ton, putting pressure on independent blenders with limited working capital. India’s domestic production ran at 78% capacity, forcing imports priced at USD 1,045 per ton in late 2024. Thai producer PTT Global Chemical reported a 180-basis-point margin compression as feedstock costs increased. Hedging through forward contracts mitigates risk but raises overhead, challenging profitability across the Asia-Pacific Automotive Lubricants Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine-Oil Dominance Faces ATF Innovation Push

Automotive engine oil accounted for 66.10% of the Asia-Pacific Automotive Lubricants Market size in 2025; however, automatic transmission fluid is expected to register the fastest growth trajectory of 1.56% through 2031. Engine oil demand is concentrated in India, Indonesia, and rural China, where ICE vehicles remain prevalent. However, viscosity migration to 0W-20 and 0W-16 boosts the synthetic share and price realization. Rising adoption of turbo-gasoline particulate filters drives mid-SAPS chemistry, fostering demand for higher-margin Group III+ blends. Aftermarket workshops increasingly upsell semi-synthetic 5W-30 lines to small-car owners seeking warranty-compliant options.

ATF advances on the back of CVT and dual-clutch gearbox penetration, surpassing 60% in new Japanese and Korean passenger cars. Honda’s CVT-equipped City and HR-V models utilize proprietary HMMF fluids, which have anti-shudder durability exceeding 240 hours at 150°C. Nissan’s X-Tronic CVT platforms across ASEAN prescribe NS-3 spec oils that command a 40% premium over Dexron VI fluids. As ATF drain intervals extend to 100,000 km, total liter growth stays moderate, but revenue gains outstrip volume. Manual-transmission oil and brake-fluid segments plateau, while automotive greases see modest uptake for wheel-bearing relubrication in heavy-duty trucks. Product-mix evolution underpins value growth inside the Asia-Pacific Automotive Lubricants Market.

By Vehicle Type: Commercial Segment Accelerates Amid E-Commerce Boom

Passenger vehicles account for 58.30% of the Asia-Pacific Automotive Lubricants Market size, reflecting the dominant ownership of cars and two-wheelers across populous economies. However, commercial vehicles are expected to register the highest 1.65% CAGR to 2031, as e-commerce, infrastructure projects, and regional trade drive freight movement. India shipped 1.05 million commercial vehicles in fiscal 2024, with medium-heavy models capturing 42% of the segment volume, necessitating CJ-4 and CK-4 diesel oils with soot-handling additives.

China operates a 35 million-unit logistics fleet that logs intense stop-start cycles in urban hubs, compressing oil-change intervals to 15,000 km despite premium CK-4 products. Indonesia’s two- and three-wheeler courier bikes cover 60,000 km annually, driving demand for high-quality motorcycle oils with wet-clutch friction modifiers. The commercial surge spurs demand for driveline oils, coolants, and chassis greases, partly offsetting the decline in private-car kilometers in congested megacities. Environmental upgrades to Euro VI-equivalent standards are driving the adoption of low-ash diesel oils, reinforcing synthetic adoption and increasing average selling prices within the Asia-Pacific Automotive Lubricants Market.

Geography Analysis

China contributed 34.80% of the Asia-Pacific Automotive Lubricants Market in 2025, supported by domestic production exceeding 3.5 billion liters and a regulatory shift to China VI low-SAPS oils, which accelerated synthetic adoption. Multinationals compete with Sinopec and PetroChina by focusing on premium brands and digital service add-ons. India leads growth with a 1.78% CAGR through 2031; consumption reached 2.8 billion liters in fiscal 2024, as BS VI norms triggered an 18% uptrend in synthetic-oil share. Local refiners invest in hydrocracker upgrades to capture Group III margins, while global majors build blending plants near Mumbai and Chennai to localize supply.

Japan and South Korea represent mature, high-specification territories where JASO and K-AIS standards shape global formulation trends. Both rely on premium synthetics, achieving drain intervals of over 15,000 km and prioritizing value over volume. Southeast Asia exhibits heterogeneous dynamics; Thailand’s 1.9 million-unit vehicle output in 2024 generated significant factory-fill demand. Indonesia’s motorbike dominance, with 6.2 million annual sales, underpins the demand for two-stroke and four-stroke motorcycle oil volumes, despite a lower per-liter value. Vietnam and the Philippines deliver double-digit lubricant revenue growth as rising middle-class consumers upgrade to personal cars. Australia and New Zealand are small but lucrative, with synthetics exceeding 60% of retail shelves and mining fleets consuming high-viscosity monograde engine oils blended with friction modifiers to handle extreme loads. Pacific island markets import packaged lubes via Singapore hubs. Intra-ASEAN tariff reductions under the AEC facilitate cross-border shipments, letting producers optimize plant utilization. Diverse regulatory frameworks and consumer preferences compel multi-portfolio strategies, yet shared digital-commerce trends and regional trade agreements knit the Asia-Pacific Automotive Lubricants Market into an increasingly integrated arena.

Competitive Landscape

The Asia-Pacific Automotive Lubricants Market is moderately consolidated. Global majors Shell, ExxonMobil, and TotalEnergies maintain their leading positions by integrating base-oil production, advanced additive science, and predictive maintenance platforms. Market fragmentation persists in Southeast Asia, where independent dealers dominate workshop supply. Digital entrants pilot direct-to-mechanic platforms, yet scale advantages in feedstock sourcing and regulatory compliance keep entry barriers high. Competitive rivalry thus revolves around technology, brand equity, and omnichannel reach inside the Asia-Pacific Automotive Lubricants Market.

Asia-Pacific Automotive Lubricants Industry Leaders

China Petrochemical Corporation

BP p.l.c.

Shell plc

TotalEnergies

Exxon Mobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Shell India rolled out its revamped premium motor oil, Shell Helix Ultra, tailored to align with the cutting-edge 2025 API SQ Standard. The company also introduced a striking new packaging design for its Shell Helix lubricant lineup, emphasizing a contemporary aesthetic.

- June 2025: Mahindra awarded the Aftermarket Service Fill contract to PETRONAS Lubricants (PLIPL), a PETRONAS Lubricants International (PLI) subsidiary. This move bolsters PLIPL's presence in India's automotive lubricant sector. As part of the agreement, PLIPL becomes the exclusive distributor of the Maximile brand vehicle fluids, such as engine oils, transmission oils, axle oils, and steering fluids.

Asia-Pacific Automotive Lubricants Market Report Scope

By Resin Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

By Geography

| China |

| India |

| Pakistan |

| Bangladesh |

| Japan |

| South Korea |

| Taiwan |

| Australia |

| Malaysia |

| Indonesia |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| By Resin Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

| By Geography | China | |

| India | ||

| Pakistan | ||

| Bangladesh | ||

| Japan | ||

| South Korea | ||

| Taiwan | ||

| Australia | ||

| Malaysia | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large is the Asia-Pacific Automotive Lubricants Market in 2026?

The market totals 10.09 billion liters in 2026, with a projected rise to 10.79 billion liters by 2031 at a 1.35% CAGR.

Which product type dominates demand?

Engine oil leads with 66.10% share, although automatic transmission fluid grows fastest at a 1.56% CAGR through 2031.

What geography offers the highest growth?

India shows the strongest pace, expanding at a 1.78% CAGR as its vehicle parc and BS VI compliance requirements climb.

How do emission regulations affect lubricant formulation?

China VI and Bharat VI standards cap SAPs content, steering blenders toward Group II+ and Group III base oils and boosting synthetic penetration.

Which companies hold leading positions?

Shell, ExxonMobil, and TotalEnergies head the field, while ENEOS, Indian Oil Corporation, and Pertamina maintain strong regional power through localized assets.

Page last updated on: