South Asia Lubricants Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

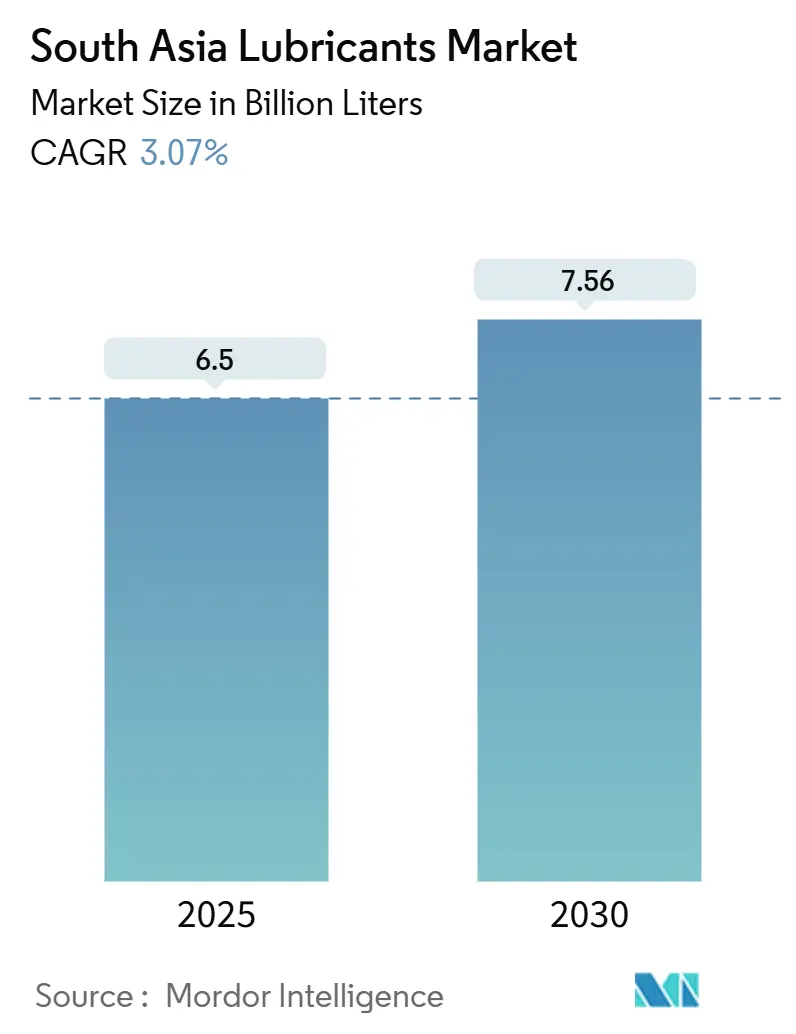

| Market Volume (2025) | 6.5 Billion liters |

| Market Volume (2030) | 7.56 Billion liters |

| Growth Rate (2025 - 2030) | 3.07% CAGR |

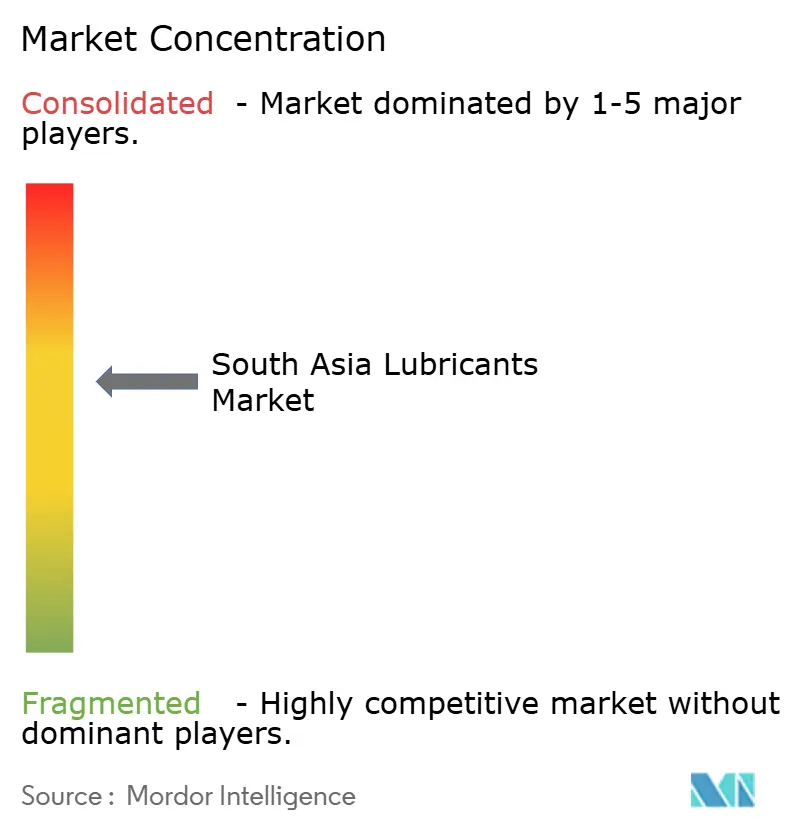

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Asia Lubricants Market Analysis by Mordor Intelligence

The South Asia Lubricants Market size is estimated at 6.5 billion liters in 2025, and is expected to reach 7.56 billion liters by 2030, at a CAGR of 3.07% during the forecast period (2025-2030). Momentum stems from industrial production recovery, higher freight intensity, and steady infrastructure spending, while ongoing electrification headwinds temper automotive lubricant volumes. India anchors regional demand, while Bangladesh and Pakistan contribute incremental growth. The dominance of mineral oil is facing gradual displacement by bio-based and synthetic alternatives. Key trends shaping expansion include Make in India–led diversification of manufacturing, logistics corridor upgrades, and OEM‐driven preference for performance-enhancing synthetics. Competitive strategies center on base-oil integration, the depth of the distribution network, and innovation in biodegradable formulations. The South Asia lubricants market continues to benefit from heavy-duty commercial transport, power-generation maintenance, and construction equipment utilization; however, escalating EV penetration, base-oil price volatility, and grey-market recycling weigh on margins.

Key Report Takeaways

- Automotive engine oil accounted for 29.84% of the South Asian lubricants market share in 2024. Industrial engine oil is forecast to grow at a 3.36% CAGR through 2030.

- By end-user, the automotive sector captured 45.75% of the South Asia lubricants market size in 2024, while industrial applications are projected to advance at a 3.25% CAGR to 2030.

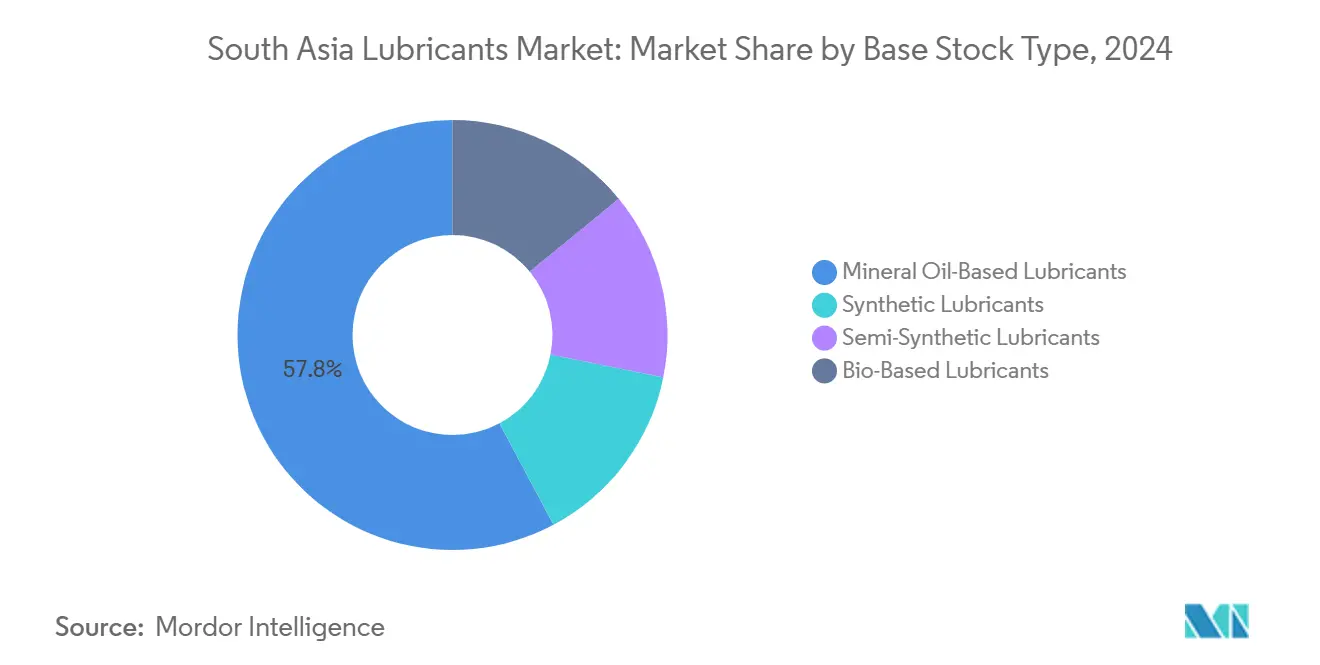

- Mineral oil-based products dominated the market with a 57.78% share in 2024; bio-based lubricants are expected to register a 3.12% CAGR from 2024 to 2030.

- India held an 86.07% geographic share in 2024 and is expected to expand at a 3.69% CAGR through 2030.

South Asia Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industrial output recovery | +0.8% | India, Bangladesh industrial zones | Medium term (2-4 years) |

| Freight and logistics expansion | +0.6% | Key trade corridors | Short term (≤ 2 years) |

| Manufacturing sector diversification | +0.5% | India, spill-over to Bangladesh and Pakistan | Long term (≥ 4 years) |

| Penetration of synthetic lubricants | +0.4% | India, urban Pakistan, Bangladesh | Medium term (2-4 years) |

| Power-generation and construction demand | +0.3% | Infrastructure-dense regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Industrial Output Recovery Drives Regional Lubricant Consumption

Regional manufacturing indices surpassed pre-2020 levels by late 2024, driving demand for metalworking fluids, turbine oils, and hydraulic oils. India’s PMI remained above 55 for 12 consecutive months in 2024; Production-linked incentive schemes worth USD 8.2 billion in 2024 further stimulated the uptake of lubricants in automotive, electronics, and pharmaceutical clusters. Accelerated factory utilization led to more frequent machinery maintenance cycles, directly underpinning the growth of South Asia's lubricants market.

Freight Logistics Expansion Accelerates Commercial Lubricant Demand

Goods traffic on the Delhi–Mumbai Industrial Corridor rose in 2024. Heavier truck platforms and higher vehicle-kilometer run rates boosted consumption of heavy-duty engine oils, transmission fluids, and gear oils. Dedicated freight corridors elevated lubricant drain intervals, catalyzing uptake of premium synthetics capable of sustaining severe operating temperatures. Elevated axle loads and longer hauls fortified demand projections for the South Asia lubricants market through 2027.

Manufacturing Sector Diversification Under Regional Industrial Policies

Electronics output in India expanded 15% in 2024, requiring ultra-clean process oils for printed circuit board fabrication. Bangladesh’s pharmaceutical exports climbed on the back of export-processing zone incentives, prompting purchases of food-grade and high-purity hydraulic fluids. Diversification is steering procurement toward higher-performance synthetics, reshaping product specifications within the South Asia lubricants market.

Synthetic Lubricant Penetration Accelerates Performance Requirements

OEM warranty clauses and fleet cost optimization drove the adoption of synthetic lubricants in India’s automotive sector in 2024. Domestic refiners have commissioned Group III base-oil units, lowering import dependence and spurring wider availability. Industrial buyers now specify synthetic gear oils and hydraulic fluids for critical assets in power generation, mining, and construction, thereby prolonging equipment life and reducing unscheduled downtime.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Base-oil price volatility | -0.4% | Import-dependent Bangladesh and Sri Lanka | Short term (≤ 2 years) |

| Grey-market recycled lubricants | -0.3% | India, Pakistan, Bangladesh | Medium term (2-4 years) |

| Accelerated EV penetration | -0.2% | Urban India, emerging metros | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Base Oil Import Dependency Creates Pricing Volatility Exposure

Roughly 60% of regional base-oil demand is met through imports, exposing formulators to currency swings and supply disruptions. India imported 1.2 million tonnes in 2024, and premium Group III feedstocks suffered sharper price spikes, squeezing margins for synthetic blends.

Accelerated EV Adoption in Urban Clusters Lowers ICE Lubricant Volumes

Electric two-wheelers and passenger cars are gradually displacing gasoline equivalents in major Indian cities, dampening demand for crankcase oils. The pace remains uneven, with heavy-duty trucks and construction machinery likely to retain lubricant-intensive internal combustion platforms for the foreseeable future.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oils Retain Scale While Industrial Grades Outpace

Automotive engine oil captured 29.84% of South Asia's lubricants market share in 2024 due to the sizeable on-road vehicle parc and intermittent servicing schedules. Industrial engine oil posted the quickest climb at a 3.36% CAGR on the back of power-generation builds and construction equipment fleet growth. Transmission fluids and gear oils benefited from heavier truck configurations, whereas hydraulic fluids tracked the utilization of construction machinery. Process oils, especially rubber process oil, gained traction in pharmaceutical and food processing lines, meeting global quality standards.

Metalworking fluids experienced a lift from Make in India–driven electronics and precision engineering output, steering buyers toward low-viscosity synthetics for improved tool life. Turbine and transformer oils remained stable, buffered by grid reinforcement projects. Collectively, industrial products are nudging the South Asia lubricants market mix toward higher-margin specialty grades.

By End-User Industry: Automotive Still Largest, Industrial Growing Faster

The automotive segment accounted for 45.75% of the South Asia lubricants market size in 2024, with commercial vehicles consuming a disproportionate volume due to their high annual mileage and stricter maintenance cycles. According to the Society of Indian Automobile Manufacturers (SIAM), the industry produced 3.10 crore vehicles in FY 2024-25, including passenger vehicles, commercial vehicles, three-wheelers, two-wheelers, and quadricycles, up from 2.84 crore vehicles in FY 2023-24[1]Society of Indian Automobile Manufacturers, “Performance of Indian Auto Industry in 2024-25,” siam.in.

Industrial applications are advancing at a 3.25% CAGR to 2030 as power, steel, textiles, and cement plants raise usage of turbine, hydraulic, and gear oils. Rural two-wheelers continue to underpin engine oil demand, balancing partial urban electrification losses.

Heavy equipment lubrication remains resilient, serving the construction, mining, and agricultural sectors, all of which benefit from government infrastructure pipelines. Marine and aerospace niches add incremental requirements for high-performance greases and biodegradable oils. Over time, industrial growth momentum is expected to rebalance overall demand, lessening the automotive share of the South Asia lubricants market.

By Base Stock Type: Mineral Oils Predominate but Bio-Based Options Gain

Mineral oils held a 57.78% share in 2024 due to their cost competitiveness and extensive supply chains. Synthetic variants have been strengthened due to longer drain intervals and temperature resilience sought by fleet operators, while semi-synthetic blends have captured mid-range price points. Bio-based formulations are projected to grow at a 3.12% CAGR, aided by domestic vegetable-oil feedstock and regulatory incentives such as India’s EPR scheme.

Investments in Group II/III refining units are reducing foreign dependency for high-grade base stocks, improving availability and price stability of synthetics. As ESG reporting becomes mainstream, industrial buyers are piloting renewable esters for hydraulic systems in environmentally sensitive sites, supporting future share gains within the South Asia lubricants market.

Geography Analysis

India’s 86.07% share underscores its pivotal role in regional demand, with a 3.69% CAGR through 2030 driven by manufacturing diversification, freight corridor roll-outs, and sustained power-plant maintenance. The domestic refining slate of around 250 million tonnes offers partial base-oil self-sufficiency, though premium synthetics still rely on imports. EPR legislation enacted in 2024 is expected to push recyclers toward formal channels, likely improving feedstock traceability and spurring the adoption of bio-based products.

Bangladesh, benefiting from growth in automotive volumes and revived textile exports, which amplify demand for process oils and metalworking fluids. Infrastructure projects such as the Padma Bridge and Dhaka Metro support the consumption of construction equipment lubricants. Pakistan’s recovery from prior fiscal stress boosts cement and steel output, thereby driving industrial oil demand.

Sri Lanka, the smallest segment, shows a gradual rebound after its 2022 crisis; transshipment activities at Colombo Port and agricultural mechanization open niche demand for marine and farm machinery oils. SAARC trade facilitation has improved cross-border flows; however, tariff disparities and divergent quality codes continue to fragment the South Asian lubricants market. Harmonization initiatives and mutual recognition pacts are expected to streamline regional distribution over the medium term.

Competitive Landscape

The South Asia lubricants market is moderately consolidated, with state-owned giants leveraging integrated refining and multi-tier retail networks to secure leading volume positions. International majors focus on premium synthetics, pursuing technology partnerships and co-branding with OEMs to defend price premiums. Shell India launched an API SQ-compliant Shell Helix Ultra line with new packaging aimed at premium car owners[2]Shell Press Release, “Shell Helix Ultra API SQ Launch,” shell.com. Strategic plays center on local base-oil capacity, supply-chain digitalization, and expansion into secondary towns through micro-warehouse models. New entrants are capitalizing on bio-based niches by sourcing palm and coconut esters to produce biodegradable hydraulic fluids, whereas service-oriented disruptors are utilizing IoT sensors for predictive oil analysis, thereby extending lubricant life and reducing downtime. Regulatory tightening through EPR and BIS-updated specifications favors compliant brands, raising entry hurdles for informal players and gradually shifting market share toward organized manufacturers in the South Asian lubricants market.

South Asia Lubricants Industry Leaders

Indian Oil Corporation Ltd

BP p.l.c.

Bharat Petroleum Corporation Limited

Hindustan Petroleum Corporation Limited

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Chevron Corporation invested USD 30 million in an automated blending plant in Pakistan to expand capacity beyond 70 million liters.

- June 2025: BP p.l.c. initiated a potential USD 10 billion divestment of its Castrol division as part of a USD 20 billion portfolio realignment.

- June 2025: PETRONAS Lubricants International won Mahindra’s aftermarket service-fill contract, becoming the exclusive distributor of Maximile vehicle fluids.

South Asia Lubricants Market Report Scope

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| India |

| Bangladesh |

| Sri Lanka |

| Pakistan |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

| By Geography | India | |

| Bangladesh | ||

| Sri Lanka | ||

| Pakistan | ||

Key Questions Answered in the Report

What is the projected demand for lubricants in South Asia by 2030?

The region is expected to consume 7.56 billion liters of lubricants by 2030, up from 6.50 billion liters in 2025 at a 3.07% CAGR.

Which base-stock segment is expanding the fastest?

Bio-based lubricants are forecast to grow at a 3.12% CAGR due to regulatory incentives and corporate sustainability targets.

How significant is India within the regional market?

India commands 86.07% of the overall volume in 2024 and maintains the quickest geographic growth at 3.69% CAGR through 2030.

What segments underpin industrial lubricant growth?

Power generation, construction equipment, and diversified manufacturing collectively drive higher demand for turbine, hydraulic, and gear oils.

How will electric vehicles influence lubricant demand?

EV adoption in urban centers is expected to reduce lubricant demand for passenger cars and two-wheelers, but heavy-duty transport and industrial machinery continue to support overall volumes.

Page last updated on: