Australia Lubricants Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

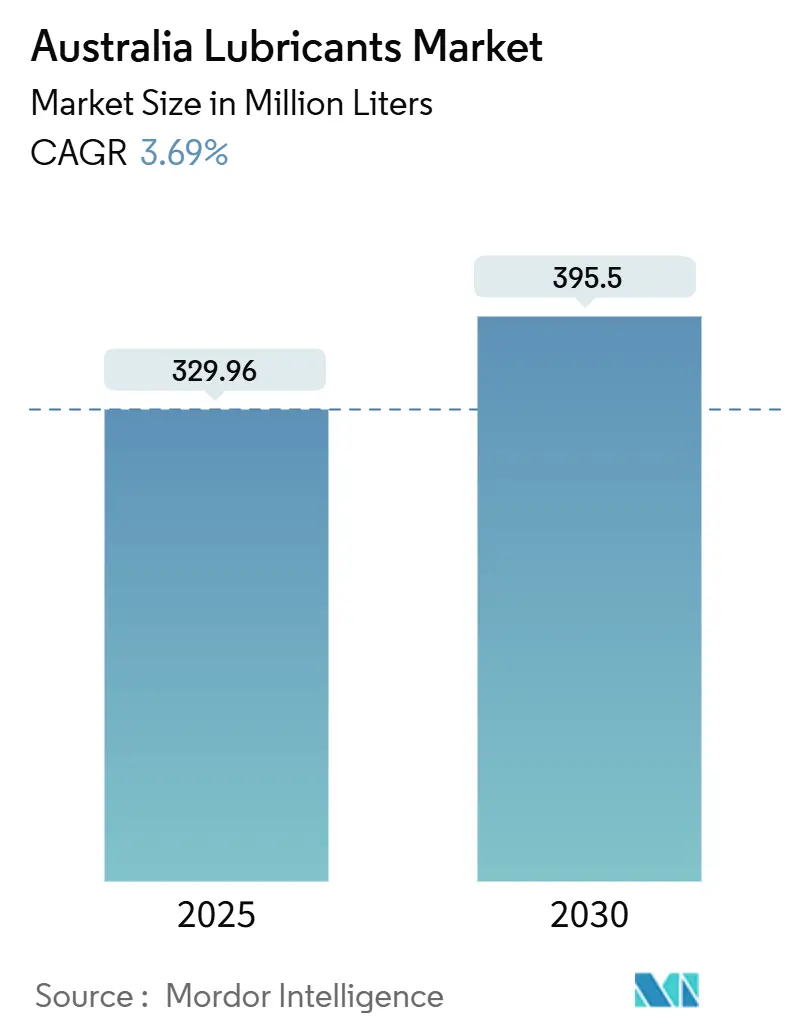

| Market Volume (2025) | 329.96 Million liters |

| Market Volume (2030) | 395.5 Million liters |

| Growth Rate (2025 - 2030) | 3.69% CAGR |

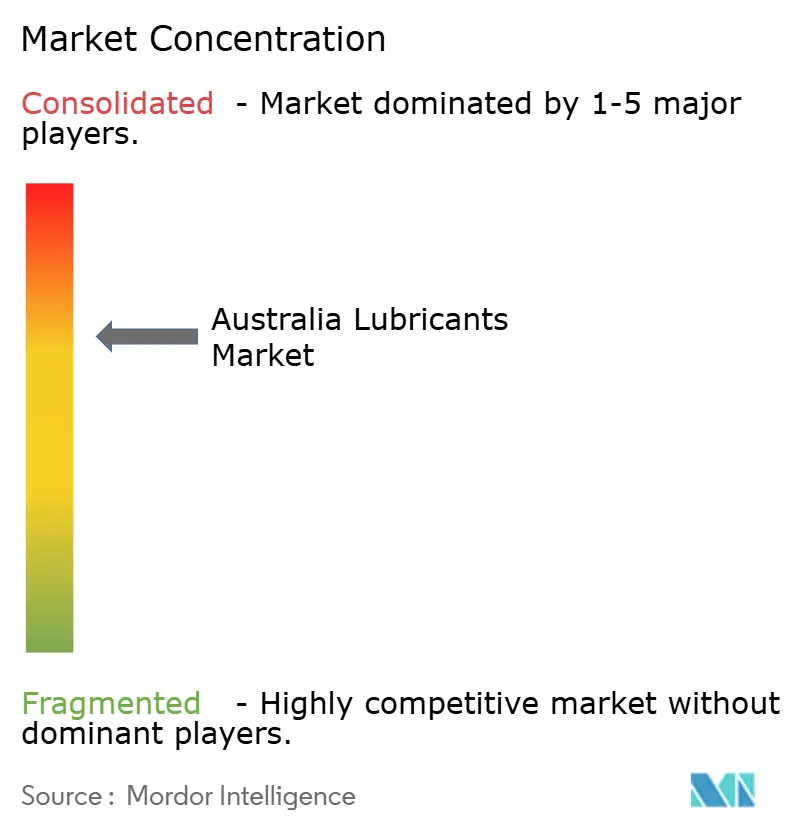

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Lubricants Market Analysis by Mordor Intelligence

The Australian Lubricants Market size is estimated at 329.96 million liters in 2025, and is expected to reach 395.5 million liters by 2030, at a CAGR of 3.69% during the forecast period (2025-2030). This moderate expansion reflects the Australian lubricants market's continued ability to serve a large pool of internal-combustion vehicles, even as electric-vehicle (EV) uptake accelerates. High-performance synthetics for mining and construction equipment, a fast-growing parcel-delivery fleet, and a rebound in local manufacturing have reinforced volume momentum. Regulatory incentives under the Product Stewardship for Oil (PSO) program are promoting the adoption of recycled oil, while also incurring compliance costs that favor large, branded suppliers. Strategic plant upgrades confirm that the Australian lubricants market retains attractive margins despite structural shifts toward lower-viscosity fluids and EV-specific products.

Key Report Takeaways

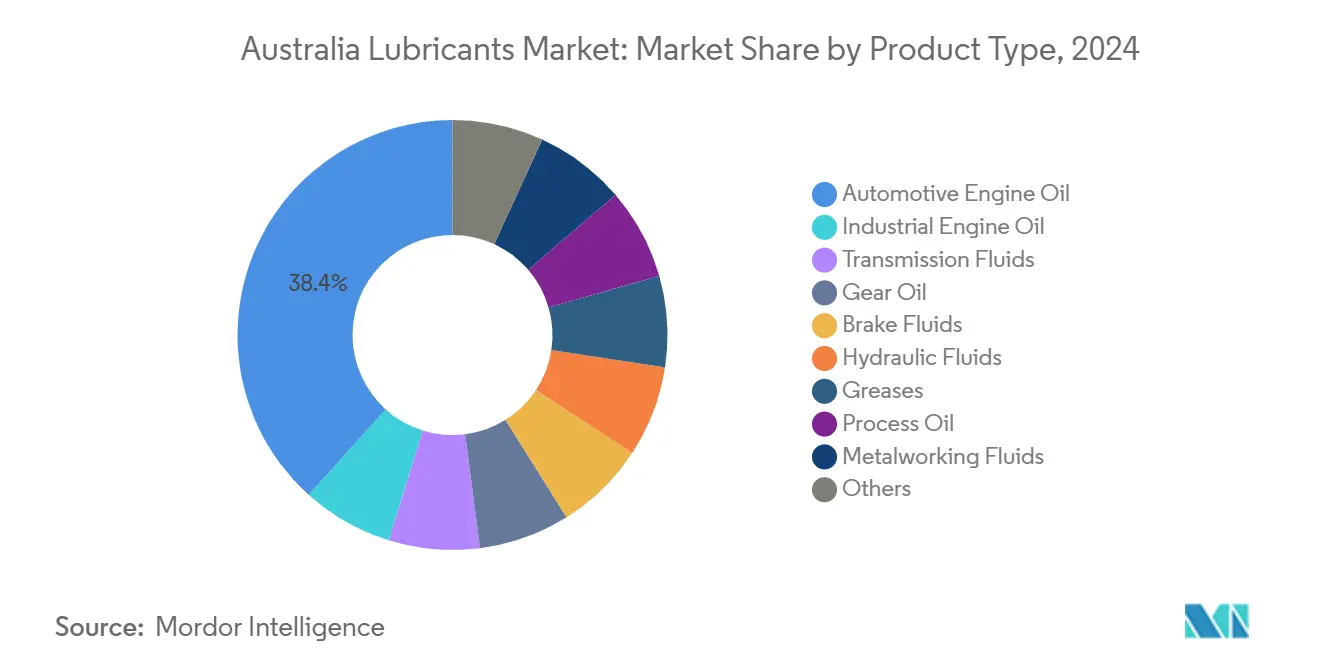

- By product type, automotive engine oil captured 38.35% of the Australian lubricants market share in 2024, while industrial engine oil is forecast to post the fastest 4.12% CAGR through 2030.

- By end-user, the automotive segment held 67.91% of the Australian lubricants market share in 2024, whereas industrial applications are projected to grow at a 3.95% CAGR to 2030.

- By base stock, mineral-oil grades commanded 62.13% of the Australian lubricants market size in 2024, and bio-based lubricants are anticipated to expand at a 4.57% CAGR over the same period.

Australia Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic rebound in manufacturing and exports | +1.2% | National, concentrated in NSW, VIC, QLD industrial hubs | Medium term (2-4 years) |

| Expansion of commercial-vehicle fleet and e-commerce logistics | +1.8% | National, with early gains in Sydney, Melbourne, Brisbane corridors | Short term (≤ 2 years) |

| Industrial automation driving high-performance synthetics | +0.9% | National, spill-over to mining regions WA, QLD | Long term (≥ 4 years) |

| Biodiesel (B20) mandate raising oil-change frequency | +0.4% | National, regulatory compliance framework | Medium term (2-4 years) |

| Renewable-energy build-out boosting turbine and transformer oils | +0.7% | National, concentrated in wind/solar development zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-pandemic manufacturing recovery accelerates industrial lubricant demand

A resurgence in domestic manufacturing is driving an increase in industrial volumes within the Australian lubricants market. Steel mills, food processors, and packaging lines are upgrading their machinery and shifting to predictive maintenance schedules that favor premium synthetic lubricants. Mining sites in Western Australia and Queensland now specify Group III and poly-alpha-olefin blends to handle extreme thermal loads. PETRONAS offers telemetry-enabled Fluid-i tanks, allowing operators to schedule replenishment remotely, thereby reducing downtime and validating higher unit prices. As factories pursue export growth, extended-drain oils cut servicing visits, directly supporting a 3.95% CAGR for industrial volumes.

Commercial-vehicle fleet expansion drives volume growth despite electrification

Heavy freight on the Sydney-Melbourne-Brisbane triangle has risen sharply. Truck operators prefer low-ash oils that protect Euro VI after-treatment systems and lengthen service intervals over long line-haul distances. Although EV-powered delivery vans are entering metropolitan fleets, diesel rigs still dominate interstate corridors, sustaining demand for high-TBN engine oils, axle lubes, and transmission fluids.

Industrial automation investments elevate synthetic-lubricant penetration

Robotics and CNC upgrades raise temperature stability and cleanliness requirements, moving factories toward Group III and GTL-based synthetics. Lower-viscosity SAE 0W-20 formulations, initially developed for passenger cars, are now being applied to gearboxes and hydraulic systems, resulting in measurable energy savings. Shell supplies GTL base oils from its Pearl plant, enabling formulations with stronger oxidative stability that cut oil-related machine stoppages for high-precision processes.

Biodiesel mandate implementation alters lubricant service patterns

National blending targets of up to B20 improve fuel lubricity but can dilute crankcase oils through fuel ingress, prompting operators to shorten drain intervals. Specialized additive packs protect against nitration and seal swelling, and fleet depots are revising laboratory testing routines to detect base-number depletion earlier. As HVO trials progress, lubricant marketers are developing cross-compatible formulations to address differing solvent properties.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid EV uptake shrinking ICE lubricant pool | -2.1% | National, accelerated in urban centers Sydney, Melbourne, Brisbane | Short term (≤ 2 years) |

| Escalating PSO levy and tighter waste-oil rules | -0.8% | National, regulatory compliance framework | Medium term (2-4 years) |

| Grey-market recycled lubes pressuring prices | -0.4% | National, concentrated in industrial regions NSW, VIC, QLD | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid EV uptake shrinking ICE lubricant pool

Electric vehicle registrations have increased in 2024[1]Australian Competition and Consumer Commission, “Report on the Australian Petroleum Market – June 2024,” accc.gov.au. EVs lack moving pistons and require fewer fluids, trimming mid-term demand for passenger-car engine oils in the Australian lubricants market. Castrol has pivoted by supplying factory-fill EV coolants to three-quarters of global vehicle makers, demonstrating first-mover advantage in this nascent niche.

Escalating PSO levy and tighter waste-oil rules

The PSO levy increased in 2023, which in turn raised input costs for blenders and distributors. Large suppliers can absorb compliance overheads more easily than small independent companies, leading to consolidation across the Australian lubricants market. At the same time, state-level hazardous-waste tracking raises paperwork for industrial users, nudging them toward suppliers that offer closed-loop collection programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine oils maintain lead while synthetics widen

The automotive engine oil category accounted for 38.35% of the Australian lubricants market share in 2024, underscoring the enduring reliance on light-duty internal combustion cars. The Australian lubricants market size for industrial engine oils is projected to increase the fastest, at a 4.12% CAGR, as mining haul trucks and construction equipment prefer high-viscosity, Group III blends suited to long idle periods and high dust exposure. Transmission and hydraulic fluids serve loaders, excavators, and agricultural machinery that operate year-round across extreme climates. Gear oils benefit from higher axle loads and the widespread use of multi-trailer road trains.

Growing wind-turbine installations are driving demand for low-temperature turbine oils with strong water-separation properties, while transformer-oil volumes are mirroring grid-upgrade projects in regional locations. Grease usage shows steady gains in quarry plants where centralized lubrication systems reduce manual maintenance. Metalworking fluids support rolling and machining at downstream metals plants, and process oils find application in rubber, plastic, and food-grade uses.

By End-User Industry: Automotive volumes dominate but industrial CAGR leads

In 2024, automotive users accounted for 67.91% of total demand; however, the pool is forecast to grow slowly as EV penetration increases. Heavy trucks, buses, and off-road vehicles offset some decline through higher-capacity sumps and rigorous duty cycles, especially on transcontinental freight routes. Passenger-car lubricant sales will soften gradually but remain material through 2030 because the on-road fleet skews older than ten years.

Industrial users collectively represent the fastest-growing group with a 3.95% CAGR, driven by robotics adoption, commodity-export expansion, and power-generation upgrades. Mining firms now deploy oil-condition monitoring to avoid catastrophic gearbox failures that can cost hundreds of thousands of dollars per hour. Grid investment tied to renewable capacity requires turbine and transformer oils that combine dielectric strength with biodegradability, creating a small yet rapidly growing niche within the Australian lubricants market.

By Base Stock Type: Mineral grades lead, synthetics and bio-lubes climb

Mineral-oil formulations retained a 62.13% volume share in 2024 thanks to attractive unit pricing and entrenched distributor familiarity. Nonetheless, the Australian lubricants market size for synthetics is expected to rise as OEM warranty requirements shift toward lower viscosity and extended drain intervals. Semi-synthetic blends bridge the price gap and gain favor among owner-operators of mixed fleets. Bio-based lubricants, although still at a relatively low volume, achieve the fastest 4.57% CAGR because PSO incentives and public-sector procurement guidelines prioritize renewable inputs.

Geography Analysis

New South Wales and Victoria together account for a significant portion of the total volumes, driven by dense vehicle ownership, robust port logistics, and a diversified manufacturing base. The Australian lubricants market benefits from deep-water terminals at Port Botany and the Port of Melbourne, which streamline bulk oil imports following the closure of local refineries in 2021. Queensland ranks third, driven by coal and metallurgical production that requires heavy earth-moving fleets, which need premium synthetics with high film strength in humid tropical climates.

Western Australia relies heavily on iron-ore exports and remote LNG operations, drawing on Karratha-based blending capacity opened by Viva Energy in 2025 to mitigate supply chain risk for miners[2]Viva Energy, “Pilbara Lubricants Hub,” vivaenergy.com.au . South Australia and the Northern Territory form smaller but important pockets linked to defense shipbuilding, rare-earth mineral processing, and tourism transport. Climate variations compel suppliers to stock multigrade oils, which deliver cold-start protection in alpine areas and oxidation resistance above 40 °C in outback sites. Expansive geography also means service contractors prefer suppliers that maintain mobile oil-analysis labs and strategically placed depots to reduce freight lead times.

Regional adoption of EVs is highest in metropolitan Sydney and Melbourne, resulting in reduced light-duty engine oil turnover. Conversely, rural road-train operators continue to specify 15W-40 or 10W-30 diesel oils with boosted detergent packs. The interplay keeps overall consumption on a modest upward trajectory even as product mixes pivot toward synthetics and specialty fluids across the Australian lubricants market.

Competitive Landscape

The Australian lubricants market is moderately consolidated. Global brands dominate through licensing deals, import infrastructure, and technical support programs. Shell, via Viva Energy, leads premium segments and leverages its Pearl GTL base-oil stream to market long-drain Helix and Rimula lines. Digital service bundles are emerging as a key differentiator. PETRONAS offers cloud dashboards that track fluid life and recommend resupply windows, while Castrol’s predictive analytics help fleet managers schedule mid-drain top-offs. Suppliers able to integrate oil analysis, telemetry, and on-site engineering support are best positioned to defend share as the Australian lubricants market pivots toward value-added service models.

Australia Lubricants Industry Leaders

BP p.l.c.

Shell plc

Chevron Corporation

Exxon Mobil Corporation

FUCHS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Viva Energy invested USD 25 million in a Karratha lubricants hub to serve remote Pilbara mines, streamlining bulk deliveries and cutting lead times for offshore facilities.

- June 2025: BP p.l.c. began exploring a sale of its Castrol division, valued at up to USD 10 billion, as part of a wider USD 20 billion divestment plan by 2027.

- December 2024: Liqui-Moly introduced a new range of generalist motor oils tailored for Australian conditions, formulated in Germany and produced in Thailand.

Australia Lubricants Market Report Scope

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Key Questions Answered in the Report

How large is the Australian lubricants market in 2025?

The Australian lubricants market size stands at 329.96 million litres in 2025 and is projected to grow steadily to 395.50 million litres by 2030.

Which segment grows fastest through 2030?

Industrial engine oils record the quickest 4.12% CAGR, benefiting from mining expansion and factory automation.

What share do automotive users hold?

Automotive applications account for 67.91% of total 2024 volumes, with heavy trucks cushioning the impact of rising EV sales.

Why are synthetics gaining ground?

OEM drain-interval extensions, high-temperature mining work, and lower-viscosity engine designs push demand toward Group III and GTL-based synthetics.

How does the PSO levy affect suppliers?

The levy lifts per-litre costs and compliance duties, encouraging consolidation among blenders that can absorb the administrative burden.

What opportunities emerge from renewable energy?

Wind-turbine gearboxes and grid transformers require specialty oils with superior water resistance and dielectric performance, opening a high-margin niche.

Page last updated on: