Taiwan Automotive Lubricants Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

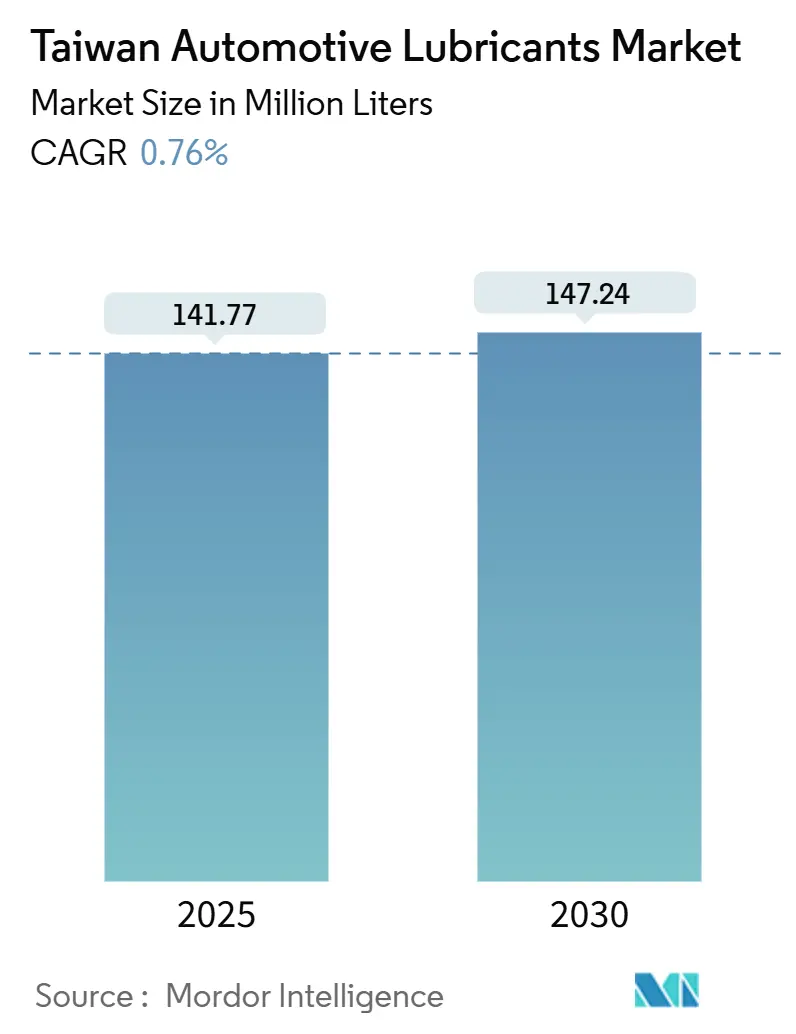

| Market Volume (2025) | 141.77 Million liters |

| Market Volume (2030) | 147.24 Million liters |

| Growth Rate (2025 - 2030) | 0.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taiwan Automotive Lubricants Market Analysis by Mordor Intelligence

The Taiwan automotive lubricants Market size is estimated at 141.77 million liters in 2025, and is expected to reach 147.24 million liters by 2030, at a CAGR of 0.76% during the forecast period (2025-2030). Mature vehicle ownership density, with 98.2 motorcycles and 36.3 cars per 100 residents, underpins a stable aftermarket that limits headline growth even as premium synthetics gain market share. Government incentives that extend EV replacement subsidies through December 2026 are nudging the fleet toward electrification, yet slower-than-expected battery-electric adoption in 2024 is sustaining demand for traditional lubricants, especially in the commercial segment. The tightness in base-oil supply after Japan’s 580,000-tonnes of Group I capacity cuts in 2023-2024 is pushing local blenders toward Group II formulations, reshaping their sourcing strategies. Meanwhile, carbon fees introduced at NTD 300 per tonne CO₂e from January 2025 are amplifying cost pressures and accelerating the pivot to low-viscosity, low-SAPS products.

Key Report Takeaways

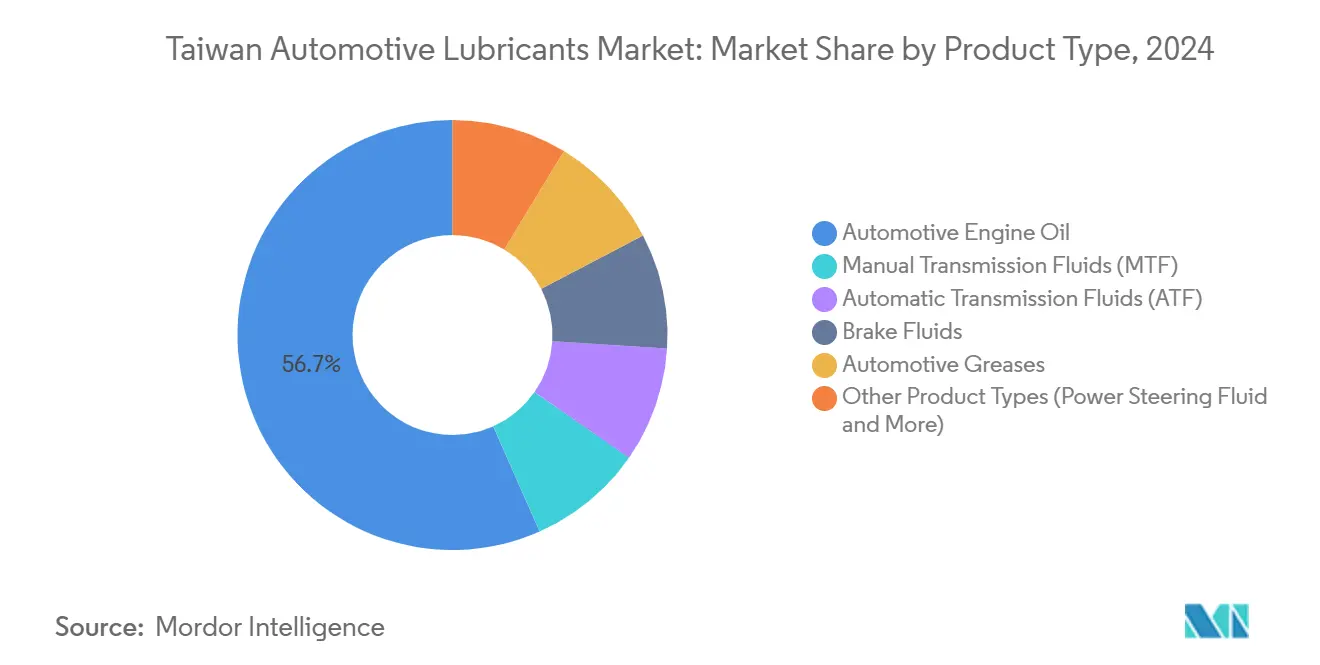

- By product type, automotive engine oil held 56.67% of the Taiwan automotive lubricants market share in 2024, while automatic transmission fluids are forecast to expand at a 0.89% CAGR through 2030.

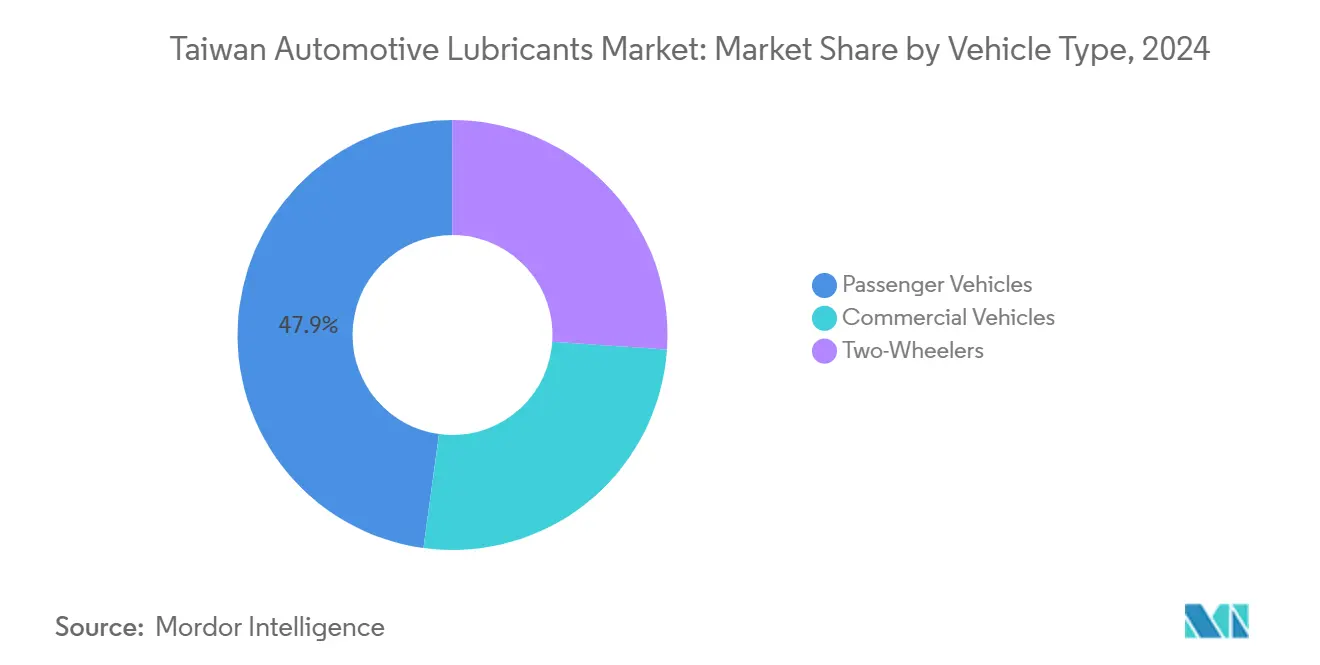

- By vehicle type, passenger vehicles accounted for 47.87% of the Taiwan automotive lubricants market size in 2024, while commercial vehicles were projected to record the highest growth at a 0.98% CAGR from 2025 to 2030.

Taiwan Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High vehicle-ownership density sustaining aftermarket demand | +0.2% | Nationwide, with Taipei, Taichung, Kaohsiung most dense | Long term (≥ 4 years) |

| Strong industrial and logistics backbone boosting commercial-fleet lubricant use | +0.3% | Nationwide, focus on western corridor | Medium term (2-4 years) |

| OEM service-interval extensions driving premium-synthetic uptake | +0.1% | Nationwide, premium urban segments | Long term (≥ 4 years) |

| Rising consumer focus on low-viscosity, low-SAPS eco-lubricants | +0.1% | Nationwide, early adoption in Taipei and Taichung | Medium term (2-4 years) |

| Electrified two-wheeler boom reshaping transmission-fluid mix | +0.1% | Urban areas with battery-swap infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Vehicle-Ownership Density Sustaining Aftermarket Demand

Taiwan’s compact geography and extensive service network, comprising more than 600 CPC stations and thousands of independent workshops, ensure convenient access to lubrication services[1]CPC Corporation, “Station Network and Lubricant Services,” cpc.com.tw. A cultural preference for professional maintenance means 90% of owners outsource oil changes, anchoring predictable volume flow through commercial channels. The Taiwan automotive lubricants market benefits from this service-centric ecosystem even as new registrations plateau. OEMs are lengthening drain intervals, yet the higher price points of synthetics offset volume attrition, and non-exclusive distribution rules enforced by the Fair Trade Commission preserve open competition across retail forecourts. Taken together, vehicular saturation establishes a substantial installed base that underpins steady aftermarket throughput.

Strong Industrial and Logistics Backbone Boosting Commercial-Fleet Lubricant Use

Manufacturing contributes approximately 33% of the island's GDP, and its role in the global semiconductor and electronics supply chains keeps freight demand robust. Heavy-duty trucks servicing export hubs and cross-strait feeders keep diesel engine oil demand resilient, providing a commercial anchor for the Taiwan automotive lubricants market. Logistics performance scores rank Taiwan among Asia’s leaders, reflecting road and port upgrades that raise equipment utilization rates and encourage fleets to adopt premium long-drain oils. Government subsidies of up to NTD 80,000 per truck for emission-control retrofits, effective through December 2025, further spur demand for low-SAPS formulations compatible with after-treatment systems. As e-commerce expands, last-mile delivery volumes increase, prompting operators to standardize on synthetics to minimize downtime and fuel consumption.

OEM Service-Interval Extensions Driving Premium-Synthetic Uptake

Premium import brands have centralized procurement that mandates OEM-approved synthetics capable of 15,000–20,000 km drains, compressing service frequency but expanding value per liter. Regulatory requirements to protect catalytic converters and diesel particulate filters endorse low-SAPS oils, and dealership channels promote factory-fill viscosity grades that exceed API SP and ACEA C3 specifications. The Taiwan automotive lubricants market, therefore, sees a strategic shift from volume to margin, as synthetics deliver 40–60% higher margins than conventionals. Suppliers that certify products to the latest OEM specs secure shelf space, while integrated distributors leverage bundled service packages to capture loyalty in a price-sensitive landscape.

Rising Consumer Focus on Low-Viscosity, Low-SAPS Eco-Lubricants

Carbon fees starting in 2025 internalize the environmental cost of fuel and lubricants, sharpening end-user sensitivity to efficiency. Low-viscosity grades such as 0W-20 are gaining popularity because they cut frictional losses and trim CO₂ output, aligning with the Environmental Protection Administration’s tighter PM2.5 targets. Local brand Guoguang highlights carbon-footprint labeling and recyclable packaging, leveraging a container-fee rebate scheme that discounts up to 45% on compliant packs[2]The News Lens, “Taiwan’s Low-Carbon Packaging Incentive,” thenewslens.com . Fleet managers in Taipei’s clean-air zones are now specifying fuel-saving lubricants as part of their ESG reporting, further supporting their adoption. For suppliers, sustainable formulas create differentiation while mitigating impending carbon-price escalations.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Maturity of on-road vehicle parc limits incremental volume growth | -0.3% | Nationwide, most in urban markets | Long term (≥ 4 years) |

| Base-oil cost and FX volatility compress distributor margins | -0.2% | Nationwide, import-dependent chains | Short term (≤ 2 years) |

| Intensifying price war from low-cost regional imports | -0.1% | Nationwide, commercial segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Maturity of On-Road Vehicle Parc Limits Incremental Volume Growth

Vehicle-ownership ratios are already among the highest worldwide, leaving limited headroom for fleet expansion. Fresh registrations mainly replace existing units, converting volume growth into a zero-sum game. Urban rail and high-speed rail options are compelling alternatives for younger citizens who prefer shared mobility, trimming long-term lubricant demand growth prospects. An aging population further dampens new-car sales, while government congestion-mitigation policies restrict the issuance of additional motorcycle licenses in Taipei and Kaohsiung. The Taiwan automotive lubricants market must therefore extract value through premiumization rather than relying on new-volume additions.

Base-Oil Cost and FX Volatility Compress Distributor Margins

Japan’s 580,000-ton Group I shutdown and Formosa Petrochemical’s Q2 2025 run cuts to 68% utilization force heavier reliance on imports. Since Taiwan imports 98% of its energy, any crude-linked spike or NTD depreciation quickly erodes working capital for mid-sized distributors. Hedging tools are limited, and spot buying magnifies exposure. Smaller blenders face cash-flow stress when dollar-denominated base oil invoices collide with time-lagged local-currency receivables. The Taiwan automotive lubricants market is seeing consolidation as financially stronger suppliers absorb weaker peers or sign long-term offtake deals to stabilize input costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oil Dominance Amid Transmission Fluid Growth

Engine oil remained the backbone of the Taiwanese automotive lubricants market in 2024, securing 56.67% of the market share. High motorcycle penetration keeps unit-level drain intervals short, while passenger-car owners favor professional workshops that recommend OEM-approved multigrades. Despite rising synthetic penetration, total liter sales of engine oil will only inch upward because EV diffusion is gradual. Automatic transmission fluid is expected to grow at a 0.89% CAGR as city traffic patterns increase demand for AT-equipped models, helping offset the slight contraction forecast for manual gearbox lubricants. Brake fluids and greases post flat trajectories, yet greases retain importance in humid coastal climates for wheel-bearing and chassis points. Low-viscosity 5W-20 and 0W-16 formulations gain traction as carbon fees sharpen the focus on fuel savings, a trend suppliers see as a hedge against stagnating volumes.

The push toward Group II and Group III base stocks continues as Japan’s Group I contraction squeezes high-viscosity supply, prompting reformulations that improve oxidation stability and meet API SP. Producers that qualify under the Environmental Protection Administration’s eco-label can command price premiums, aiding margin retention. For engine oil, synthetic blends are expected to reach 42% share by 2030, versus 36% in 2024, reflecting consumer acceptance of extended drains. Meanwhile, specialty e-fluids such as dielectric coolants and reduction-gear greases are small but expanding niches that promise fresh revenue streams. This diversification ensures the Taiwan automotive lubricants market size remains resilient even as ICE product demand plateaus.

By Vehicle Type: Commercial Vehicles Drive Growth Despite Passenger-Car Dominance

Passenger cars generated 47.87% of total lubricant demand in 2024, supported by an 8.7 million-unit fleet serviced through extensive dealership and independent workshop networks. City traffic accelerates the frequency of oil changes, despite longer OEM-recommended drain intervals, and premium European marques insist on low-SAPS synthetics to protect exhaust after-treatment systems. Two-wheelers contribute a sizable volume because of 14.5 million scooters, though electric scooter uptake will gradually compress engine oil consumption.

Commercial vehicles are the fastest-growing customer group, advancing at a 0.98% CAGR to 2030 on the back of strong logistics and industrial output. Semiconductor and precision-machinery exporters rely on just-in-time deliveries, making uptime crucial and driving the adoption of synthetic lubricants. Diesel-truck repair subsidies linked to emission upgrades compound the shift toward higher-spec 15W-40 CK-4 formulations, while off-highway equipment tied to public-works projects imports further volume. As fleets modernize, telemetry-driven maintenance scheduling utilizes oil-analysis data to optimize drain intervals, reinforcing the Taiwan automotive lubricants market’s shift from commodity volumes to value-added services, such as condition monitoring.

Geography Analysis

Northern Taiwan, anchored by Taipei and New Taipei City, is characterized by premium consumption, driven by higher disposable income and a dense concentration of luxury car ownership. OEM dealers cluster in the capital region, funneling demand toward fully synthetic 0W-20 and 0W-16 grades that align with extended service intervals. Urban clean-air regulations add catalytic-converter protection requirements, giving low-SAPS oils an edge. The concentration of electric motorcycle sales in Taipei further diversifies fluid needs, as battery-swap operators specify specialized reduction-gear lubricants.

Central Taiwan, centered on Taichung, stands as the manufacturing heartland. Precision-machinery plants and auto-parts exporters generate robust demand for industrial oils; yet, the same factories operate sizable truck fleets that increase heavy-duty engine oil usage. Taichung’s location along the west coast arterial speeds freight lanes to both northern ports and southern petrochemical complexes, making it a key nexus for lubricant distribution. Suppliers leverage this position to warehouse inventory closer to industrial customers, reducing lead times and mitigating base-oil shortages.

Southern Taiwan, encompassing Tainan and Kaohsiung, merges petrochemical activity with Asia’s seventh-largest container port. Formosa Petrochemical’s Mailiao refinery supplies part of the base-oil slate, lowering freight costs for regional blenders. Commercial fleets servicing petrochemical out-shipments prefer long-drain 10W-30 CK-4 oils to cut downtime. The region’s hot, humid climate also supports demand for high-temperature greases in port equipment. Environmental regulations controlling VOC emissions at refinery perimeters encourage adoption of bio-based degreasers, foreshadowing future lubricant formulation shifts across the Taiwan automotive lubricants market.

Competitive Landscape

The Taiwan automotive lubricants market is moderately consolidated, with the state-owned CPC Corporation anchoring supply through more than 600 retail stations and integrated refining, blending, and distribution assets, thereby granting it scale and nationwide reach. Private refiners such as Formosa Petrochemical complement the slate and focus on industrial users. International brands target premium segments by offering OEM-approved synthetics, aligning their marketing efforts with those of luxury-car dealerships. Supply-chain volatility is pushing competitors to secure long-term Group II supply contracts or diversify base-oil sourcing to the Middle East and the United States. Product differentiation increasingly rests on ESG credentials.

Taiwan Automotive Lubricants Industry Leaders

CPC Corporation, Taiwan

Exxon Mobil Corporation

Shell plc

ENEOS Corporation

BP p.l.c.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: PTT Lubricants has launched a new engine oil formula featuring the innovative "EVOTEC Technology" platform, addressing advancements in automotive technology and consumer demand for sustainability. The formula delivers three key benefits: reducing emissions for environmental conservation, enhancing engine durability under various conditions, and improving performance with better fuel efficiency.

- October 2024: SPARK-Lubricants launched operations in Taiwan, focusing on premium automotive applications and partnering with regional distributors for market entry

Taiwan Automotive Lubricants Market Report Scope

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Key Questions Answered in the Report

What is the projected volume for the Taiwan automotive lubricants market in 2030?

The market is expected to reach 147.24 million liters by 2030.

Which product category holds the highest share of lubricant demand?

Automotive engine oil leads with 56.67% of total demand in 2024.

Which vehicle segment will grow the fastest through 2030?

Commercial vehicles show the highest forecast growth at a 0.98% CAGR.

How will carbon fees affect lubricant formulations?

Fees of NTD 300 per tonne CO₂e effective 2025 incentivize low-viscosity, low-SAPS formulations that improve fuel economy and reduce emissions.

What supply-chain challenge is influencing base-oil sourcing?

Japan’s 580,000-tonnes Group I capacity cuts tighten regional supply, pushing Taiwanese blenders toward Group II imports.

Which new entrant targets premium lubricant customers in Taiwan?

SPARK-Lubricants entered in October 2024, positioning itself with additive-rich synthetics for high-performance vehicles.

Page last updated on: