Taiwan Automotive Engine Oils Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

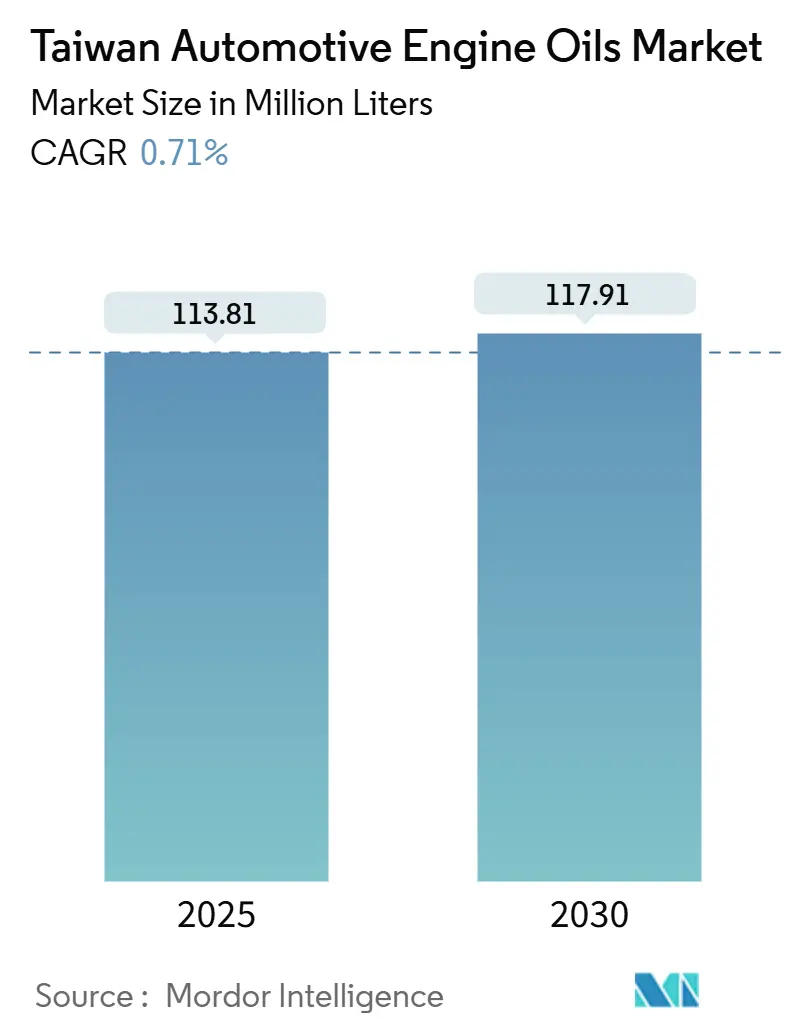

| Market Volume (2025) | 113.81 Million liters |

| Market Volume (2030) | 117.91 Million liters |

| Growth Rate (2025 - 2030) | 0.71% CAGR |

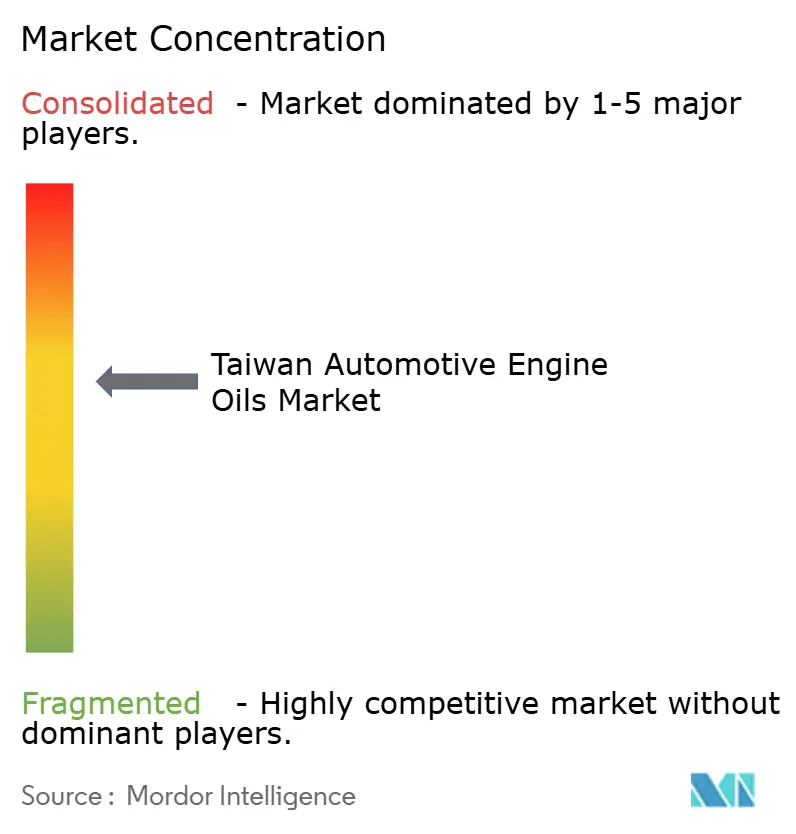

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taiwan Automotive Engine Oils Market Analysis by Mordor Intelligence

The Taiwan Automotive Engine Oils Market size is estimated at 113.81 million liters in 2025, and is expected to reach 117.91 million liters by 2030, at a CAGR of 0.71% during the forecast period (2025-2030). Vehicle stock expansion, a scooter-centric mobility culture, and rising synthetic adoption help offset the structural demand erosion caused by electrification. Market resilience is anchored in the island’s substantial registered vehicle fleet, which sustains a sizable lubricant throughput. Supply security, however, remains vulnerable because all base-oil refining capacity is concentrated within a 100-mile coastal corridor, and 99.75% of crude is imported. Global brands are repositioning portfolios toward EV-centric fluids, signaling that traditional volumes in the Taiwan automotive engine oil market will plateau well before 2030.

Key Report Takeaways

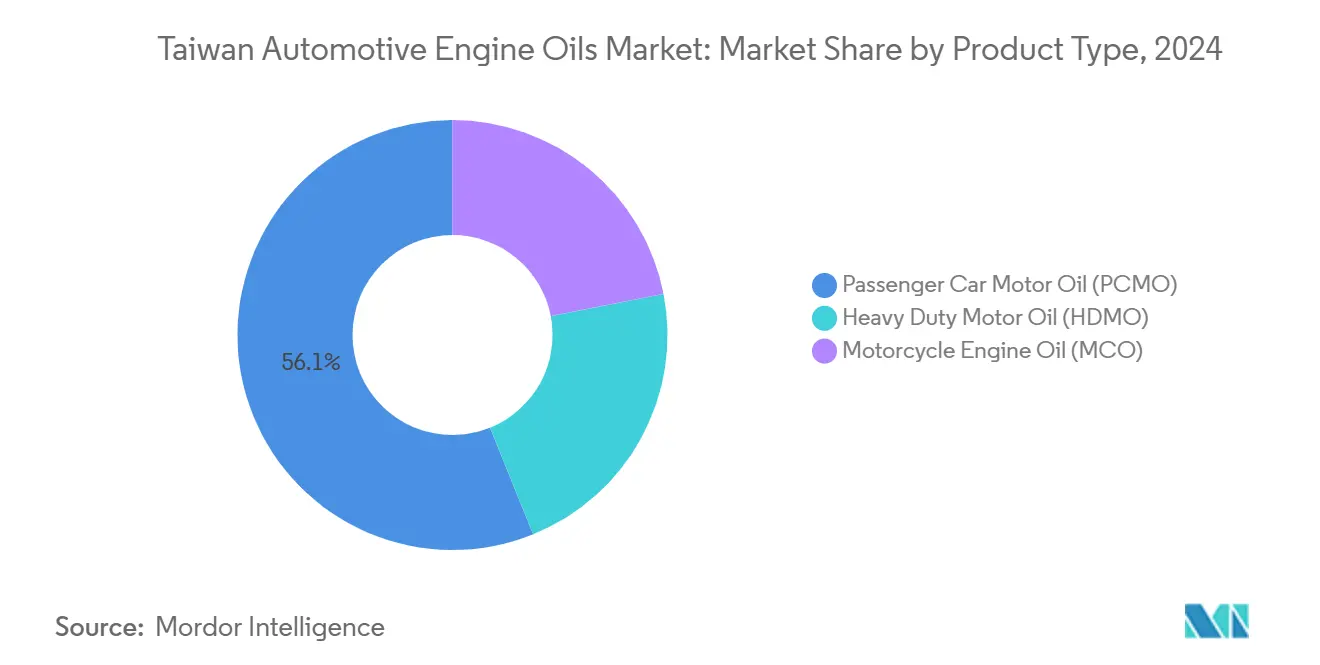

- By product category, passenger car motor oil led with a 56.12% share of the Taiwan automotive engine oil market in 2024, while motorcycle engine oil recorded the fastest growth rate of 0.89% through 2030.

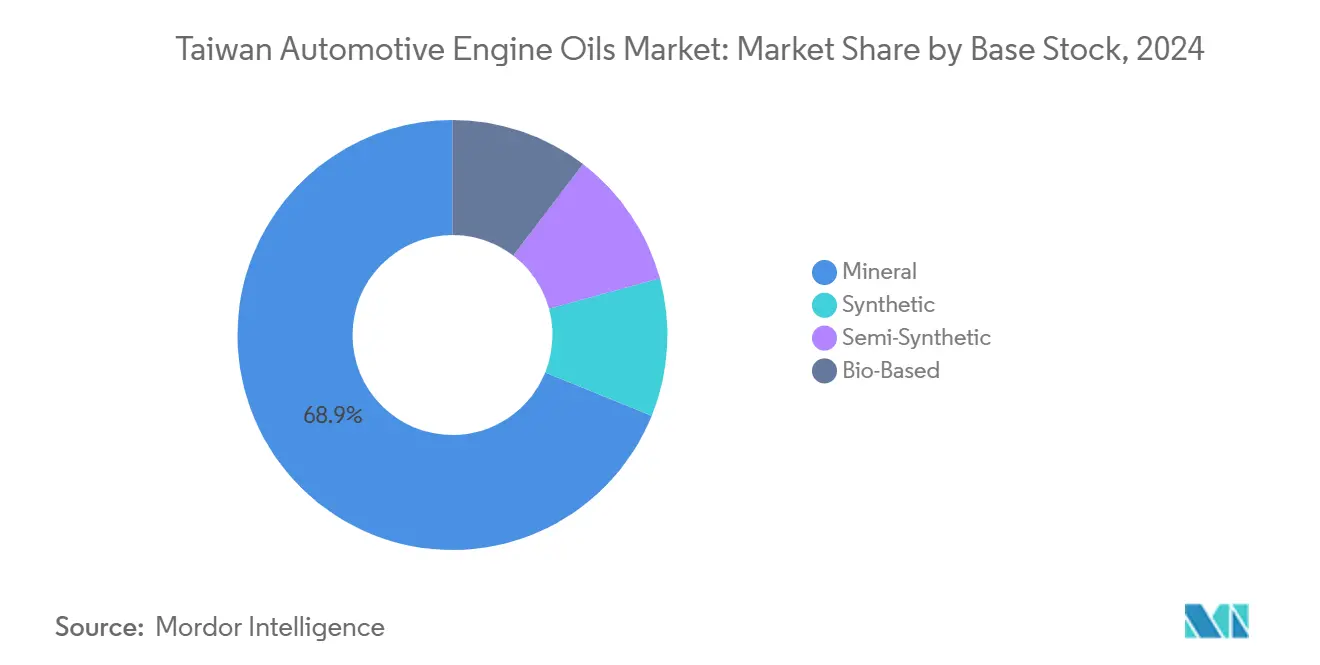

- By base stock, mineral oils held 68.87% share of the Taiwan automotive engine oil market size in 2024, whereas full synthetics are projected to expand at a 0.97% CAGR to 2030.

Taiwan Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising passenger-vehicle parc and extended ownership | +0.3% | Taiwan nationwide, concentrated in urban centers | Medium term (2-4 years) |

| High two-wheeler/scooter parc boosting MCO demand | +0.2% | Taiwan nationwide, highest in Taipei and New Taipei | Short term (≤ 2 years) |

| Growth in light-commercial and last-mile fleets | +0.2% | Urban centers, e-commerce hubs | Medium term (2-4 years) |

| Government oil-recycling subsidies spurring premium synthetics | +0.1% | Taiwan nationwide | Long term (≥ 4 years) |

| Telematics-based subscription maintenance uptake | +0.1% | Corporate fleets, urban areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Passenger-Vehicle Parc and Extended Ownership

Taiwan’s passenger-vehicle registrations climbed to an all-time high in 2024, underpinning more than half of lubricant demand despite EV headwinds. Consumers are delaying replacement as economic uncertainty and range anxiety temper EV purchases, lengthening ownership cycles and increasing the frequency of per-vehicle service occasions. The renewal incentive, which grants up to NTD 50,000 in tax relief for scrapping cars over 10 years old, paradoxically directs some buyers toward newer internal-combustion models rather than electric vehicles. Locally assembled vehicles, which still account for 52% of all cars sold, require diverse OEM-specific formulations to sustain variety in the Taiwanese automotive engine oil market. Extended ownership also prompts motorists to opt for premium synthetics to prolong engine life, nudging value growth even as total liters increase only marginally.

High Two-Wheeler/Scooter Parc Boosting MCO Demand

Taiwan hosts the world’s densest two-wheeler population, resulting in steady motorcycle engine oil throughput. Government plans to ban gasoline scooters by 2035 were shelved after industry backlash, underlining the cultural entrenchment of ICE two-wheelers. Electric scooters captured a small portion of new sales in 2024, prolonging the service life of the existing gasoline fleet. The average scooter usage necessitates short drain intervals, which intensify lubricant consumption. Brands such as PTT Lubricants have leveraged this demand with 4T synthetic blends tailored for high-temperature stop-and-go riding, reinforcing value migration toward premium MCO.

Growth in Light-Commercial and Last-Mile Fleets

E-commerce volume growth has swelled Taiwan’s light-commercial vehicle parc. Fleet operators are embracing smaller vans and micro-trucks to navigate congested city streets, creating concentrated demand for heavy-duty multigrade lubricants. While firms like FedEx pilot electric tricycles, most urban delivery fleets remain ICE-powered; expansion in absolute vehicle count offsets lubricant savings per EV deployed. Frequent stop-start cycles in Taipei and Kaohsiung raise thermal stress, driving uptake of synthetics with superior oxidation stability. Corporate fleet consolidation also favors bulk-purchase contracts, reinforcing volume visibility for suppliers entrenched in the Taiwan automotive engine oil market.

Government Oil-Recycling Subsidies Spurring Premium Synthetics

Taiwan’s Resource Circulation Administration levies a recycling fee on lubricants but grants discounts for products that meet eco-design standards, thereby improving the cost-benefit equation for full synthetic lubricants. 90% of the used oil collected is diverted to energy recovery, underscoring the scale of the circular economy. Carbon pricing of NTD 300/tCO2e, effective January 2025, further penalizes frequent oil changes, incentivizing extended-drain synthetics with lower lifecycle emissions. OEMs respond by approving lower-viscosity grades such as 0W-16, accelerating the premium shift. As synthetics gain favor, suppliers benefit from higher unit margins even if total liters grow slowly.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating BEV, e-scooter and e-2W adoption | -0.4% | Taiwan nationwide, concentrated in urban centers | Medium term (2-4 years) |

| Extended-drain synthetic oils lowering consumption | -0.2% | Taiwan nationwide, premium vehicle segments | Long term (≥ 4 years) |

| Cross-strait geopolitical risk delaying investments | -0.1% | Taiwan nationwide, supply chain impacts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating BEV, E-Scooter and E-2W Adoption

Taiwan’s 2050 net-zero roadmap targets EV penetration by 2030 and complete ICE phase-out by 2040, directly shrinking lubricant demand pools. BEV registrations leapt in 2023, eroding PCMO volumes even from a low base. Gogoro’s network of battery-swap kiosks anchors a rapidly scaling electric scooter ecosystem, accelerating MCO displacement. Crude demand could fall by 2040, pressuring base-oil economics and prompting refiners to reassess local production. Suppliers must diversify into EV thermal fluids to offset volume attrition in the Taiwan automotive engine oil market.

Extended-Drain Synthetic Oils Lowering Consumption

Advanced Group II and Group III base stocks enable drain intervals of 15,000–20,000 miles, reducing the need for annual oil changes per vehicle. Shell’s BMW-specific LL22FE++ 0W-12 formula exemplifies OEM-approved ultra-low-viscosity blends that slash consumption without compromising protection. ExxonMobil’s new EHC 340 MAX base stock, launched in 2025, supports higher viscosity indices and oxidative stability, further lengthening service intervals. As Taiwanese consumers migrate toward synthetics for fuel economy gains, liter age per car declines even if spending per fill rises. This structural shift moderates volume growth in the Taiwanese automotive engine oil market, prompting suppliers to shift from volume-driven to value-driven strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PCMO Dominance Faces MCO Growth

The Taiwan automotive engine oil market size for passenger car motor oil accounts for 56.12% share of the total volume. PCMO retains the broadest viscosity range, from 0W-8 for late-model hybrids up to 20W-50 for aging imports, reflecting a mixed fleet where 52% of vehicles are locally assembled and the rest imported. OEM factory-fill alliances with Shell, TotalEnergies, and Idemitsu support multigrade demand, while aftermarket channels remain fragmented among more than 6,000 independent workshops. Despite headwinds from battery-electric cars, annual new ICE car sales sustain baseline demand for internal combustion engine (ICE) cars.

Motorcycle engine oil is projected to post the fastest 0.89% CAGR to 2030, outpacing every other product type. Daily scooter use in dense urban corridors leads to oil changes roughly every 3,000 km, driving recurring purchases. Brands tailor 4T formulations with higher detergent content and shear stability to cope with Taiwan’s humid, stop-start conditions. Marketing partnerships with ride-hailing platforms, such as iRent and GoShare, expand bulk-sale channels for MCO suppliers, thereby cushioning future EV erosion. HDMO, while essential for growing last-mile fleets, remains a stable but slower-growing niche due to limited heavy-truck penetration on the island.

By Base Stock: Mineral Dominance with Synthetic Acceleration

Mineral formulations captured 68.87% of the Taiwan automotive engine oil market share in 2024. Competitive retail pricing, combined with widespread compatibility with older engines, keeps conventional oils popular, particularly in secondary cities and rural districts. Domestic refiners CPC and Formosa Petrochemical supply most Group I and Group II base oils, ensuring reliable feedstock streams for mineral blends and holding back a rapid shift to synthetics.

Synthetic volumes, however, are forecast to expand at a 0.97% CAGR through 2030 on the back of government recycling-fee rebates and OEM fuel-economy mandates. Extended-drain capability lowers lifetime service costs, offsetting the price premium over mineral. ExxonMobil’s EHC 340 MAX supply from Singapore, commencing 2025, secures higher-VI feedstock that underpins 0W-12 and 0W-16 formulations targeting hybrid applications[1]ExxonMobil Basestocks, “ICIS Asian Base Oils Conference Recap,” exxonmobil.com . Semi-synthetics serve as a transition option, especially in the light-commercial segment, offering oxidation resistance at modest premiums. Bio-based oils have a low share, limited by cost and performance trade-offs, despite a plentiful supply of waste cooking oil.

Geography Analysis

The Taiwan automotive engine oil market size is entirely generated within a single national geography, yet shows clear regional nuances, with northern municipalities accounting for the majority of PCMO and MCO volume in 2025, owing to vehicle density clustering around Taipei, New Taipei, and Taoyuan. The island’s west-coast highway spine funnels most commercial traffic, concentrating HDMO consumption along logistics corridors linking Taichung Port and Kaohsiung Harbor, where light-commercial fleets stage intercity movements.

Central Taiwan, anchored by Taichung’s precision-manufacturing hub and supported by a high mix of SME-owned delivery vans and motorcycles used for parts transportation. Local governments there promote fleet telematics subsidies that reduce unplanned downtime, indirectly boosting the adoption of premium synthetics formulated for extended drain life. The eastern counties, constrained by mountainous terrain and lower incomes, together account small portion of national lubricant demand. Mineral multigrades dominate retail shelves, reflecting price sensitivity and sparse service networks.

Southern metros, led by Kaohsiung, contribute to the balance of the Taiwan automotive engine oil market. The region’s petrochemical complex anchors refinery output, ensuring a ready supply of Group I brightstock and influencing local pricing competitiveness[2]Sciences Po Paris, “Taiwan’s Energy Strategy,” sciencespo.fr . Port operators’ shift toward LNG and electrified yard tractors is beginning to erode auxiliary-engine lubricant volumes, yet heavy off-road machinery in construction projects sustains niche HDMO requirements. Cross-strait geopolitical risks loom largest here because refineries and tank farms are situated within potential conflict zones, prompting contingency stockpiling that temporarily boosts distributor sales whenever tensions escalate.

Competitive Landscape

The Taiwan Automotive Engine Oils Market is moderately consolidated. Global majors, regional specialists, and state-affiliated marketers compete in a medium-concentration field. Domestic refiner CPC markets the “Mirage” and “Repsol-CPC” lines through 650 company-owned stations, capturing price-sensitive mineral sales and ensuring feedstock security. Strategic moves center on higher-VI synthetics, extended-drain additives, and bundled fleet solutions. Several players now embed telematics hardware in bulk contracts to lock in lubricant offtake over 3-year horizons, mirroring software-as-a-service tactics. Marketing spend is shifting from mass media to in-app loyalty programs on car-maintenance platforms.

Taiwan Automotive Engine Oils Industry Leaders

Shell plc

CPC Corporation, Taiwan

Exxon Mobil Corporation

BP p.l.c

FUCHS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP p.l.c initiated a process to sell its Castrol lubricants division, valuing the unit at up to USD 10 billion under a broader USD 20 billion divestment roadmap.

- May 2025: TotalEnergies has launched next-generation Quartz engine oils that meet the API SQ and ILSAC GF-7 standards, specifically designed for turbocharged and GDI engines.

- November 2024: PTT Lubricants introduced the EVOTEC Technology platform in Taiwan, featuring advanced formulations designed to enhance environmental, endurance, and efficiency performance.

Taiwan Automotive Engine Oils Market Report Scope

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

Key Questions Answered in the Report

How large is Taiwan’s automotive engine oil demand in 2025?

The volume stands at 113.81 million liters, with a forecasted 0.71% CAGR to 2030.

Which product category leads lubricant consumption?

Passenger car motor oil holds a 56.12% share of the national volume in 2024.

What is the fastest-growing segment through 2030?

Motorcycle engine oil posts the highest 0.89% CAGR, thanks to a significant scooter fleet.

Why are synthetics gaining traction in Taiwan?

Recycling-fee rebates and stricter fuel-economy rules push consumers toward extended-drain synthetic formulations.

How will electrification affect lubricant volumes?

Government targets for 30% EV penetration by 2030 and a 2040 ICE phase-out will gradually erode traditional engine oil demand despite short-term growth pockets.

Page last updated on: