Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

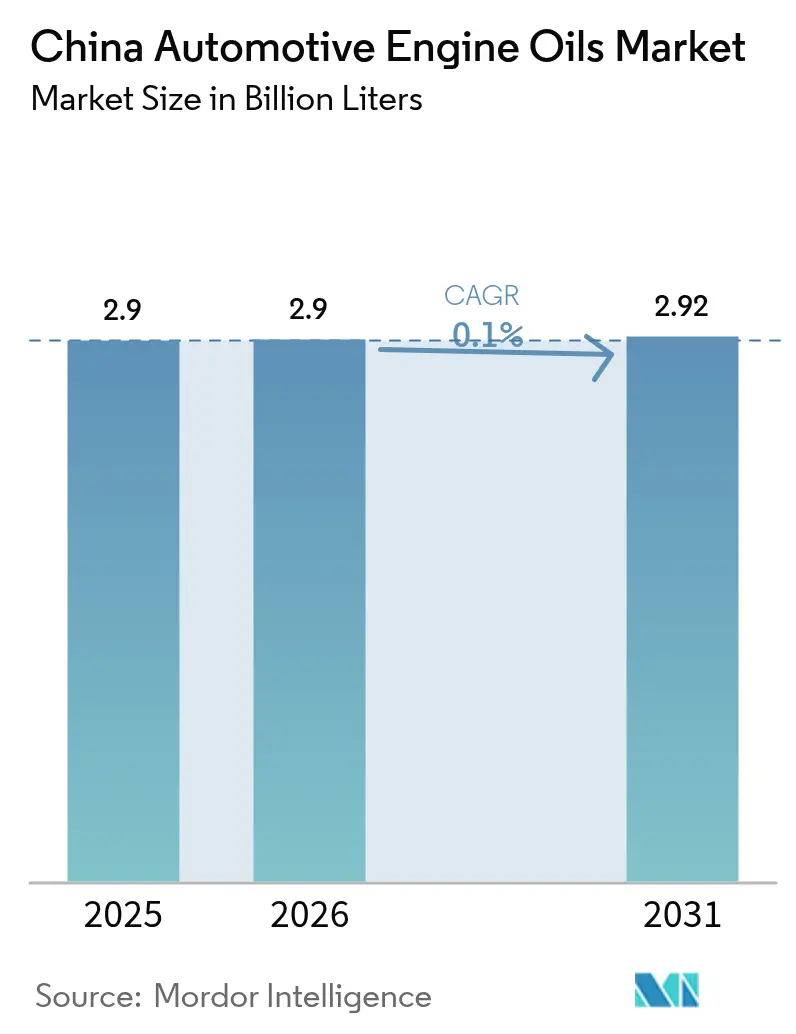

| Base Year Market Size (2025) | 2.90 Billion Liters |

| Market Volume (2026) | 2.9 Billion Liters |

| Market Volume (2031) | 2.92 Billion Liters |

| Growth Rate (2026 - 2031) | 0.10% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Automotive Engine Oils Market Analysis by Mordor Intelligence

The China Automotive Engine Oils Market size in 2026 is estimated at 2.9 billion liters, growing from 2025 value of 2.90 billion liters with 2031 projections showing 2.92 billion liters, growing at 0.10% CAGR over 2026-2031. This flat trajectory reflects the structural headwinds posed by rapid electrification, modest mileage growth, and longer drain intervals that collectively mute volumetric expansion. At the same time, regulatory upgrades such as China VI-b and the March 2025 roll-out of API SQ/ILSAC GF-7 continue to nudge the product slate toward low-viscosity, low-SAPS synthetics, lifting the average blend value even as liters stagnate. Competitive conduct remains disciplined because five leading suppliers already control most premium channels, allowing them to pass through the higher formulation cost tied to advanced additive chemistries without eroding margins. Still, regional and private brands are intensifying price competition in price-sensitive tiers in inland provinces, a dynamic that keeps retail prices from outpacing disposable incomes.

Key Report Takeaways

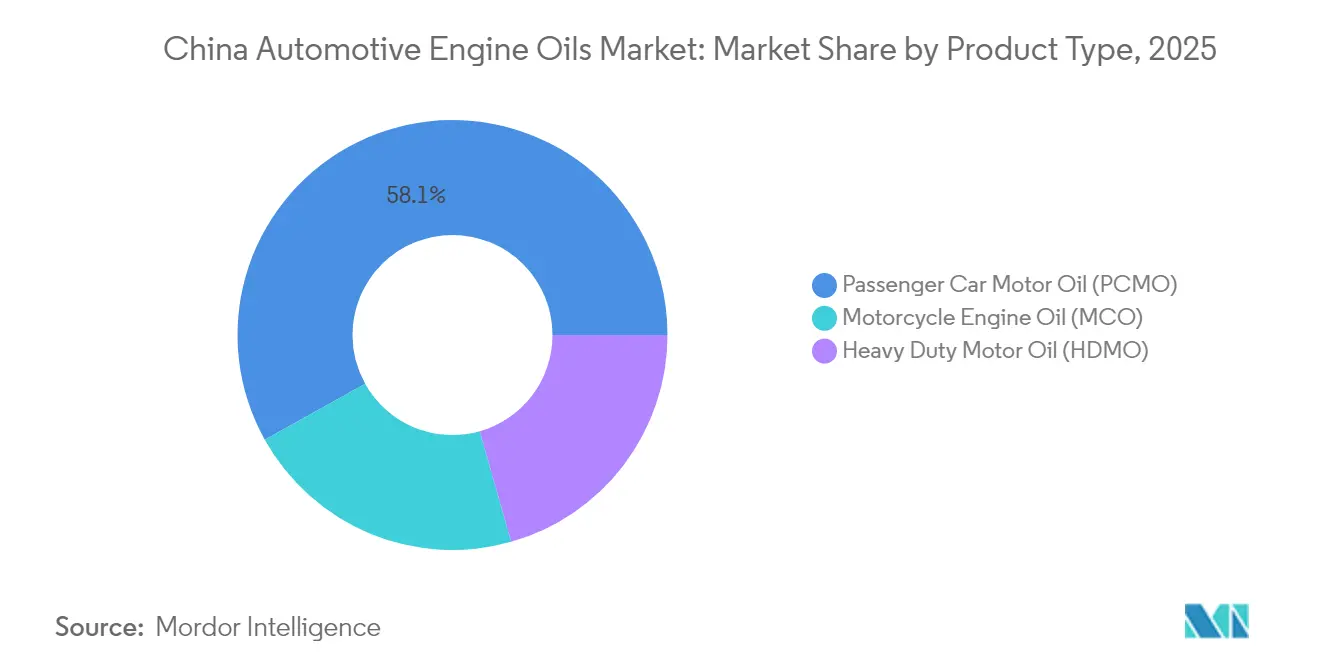

- By product type, passenger car motor oil led with a 58.10% revenue share in 2025, while motorcycle engine oil is projected to register the fastest growth of 0.15% CAGR through 2031.

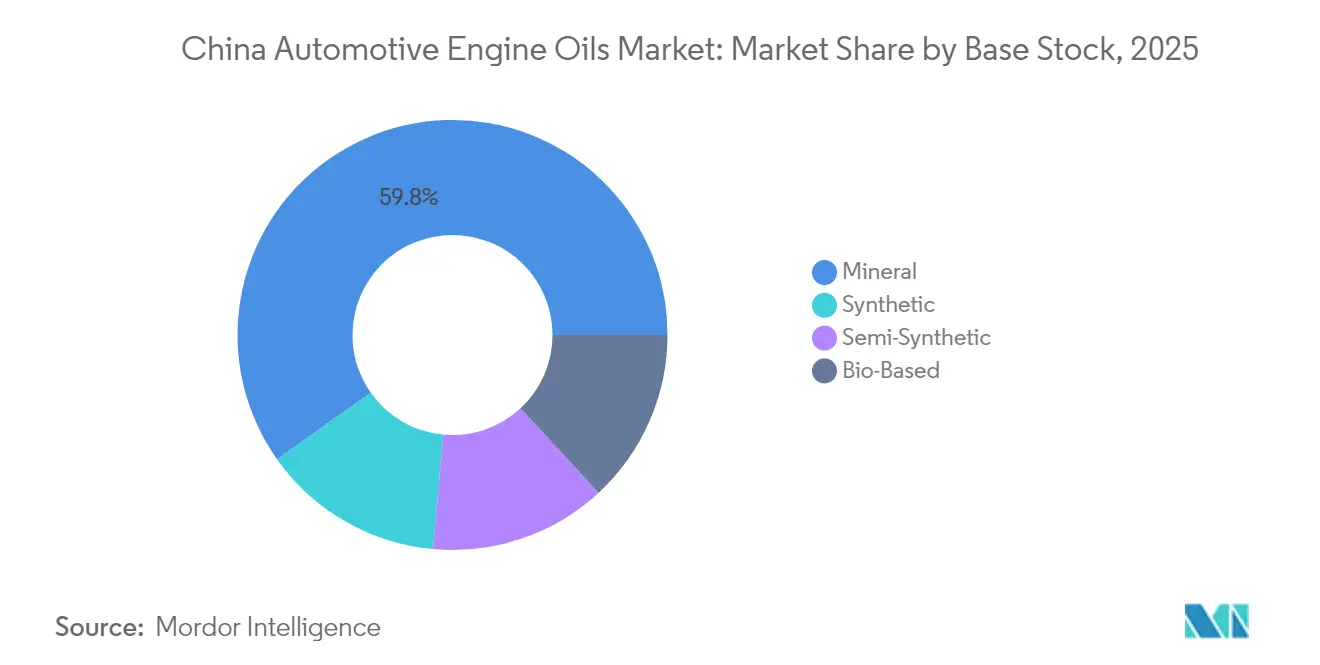

- By base stock, mineral formulations accounted for 59.80% of the China automotive engine oils market share in 2025, whereas synthetics are anticipated to grow at a 0.28% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vehicle parc and ageing fleet | +0.05% | National, strongest in Tier 2-3 cities | Medium term (2-4 years) |

| China VI-b emission norms | +0.03% | National, early adoption in metropolitan areas | Short term (≤ 2 years) |

| Turbo-GDI adoption in passenger cars | +0.02% | Coastal regions and Tier 1 cities | Medium term (2-4 years) |

| Expansion of IAM workshops and e-commerce | +0.02% | National, accelerated in rural markets | Long term (≥ 4 years) |

| Hybrid range-extender trucks | +0.01% | Industrial corridors and logistics hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle Parc & Ageing Fleet

The passenger-car parc continued to expand in 2025, adding a modest but steady flow of replacement demand despite the headline EV surge. Older ICE models dominate Tier 2-3 cities, where households postpone EV upgrades, translating into higher per-vehicle oil consumption and more frequent top-ups. Inland provinces, therefore, offer a multi-year buffer that slows the nationwide volume decline. Scrappage incentives and tighter inspection programs in coastal hubs, however, foreshadow a gradual shift that will ultimately cap this driver’s contribution to the China automotive engine oils market.

Stringent China VI-b Emission Norms Driving High-Performance Lubricants

China VI-b standards oblige formulators to cut SAPS levels and deliver fuel-economy-oriented viscosities such as 0W-20 while still protecting after-treatment hardware. Over 1,800 products were relicensed under API SQ/ILSAC GF-7 in the first nine months after the March 2025 start date. Tier 1 cities moved first, triggering a ripple of demand for fully-synthetic and high Group III blends that continues to widen inland. Compliance costs have squeezed small blenders and are accelerating mergers or supply agreements with base-oil majors, a trend reinforcing the concentrated character of the China automotive engine oils market.

Turbo GDI Adoption in Passenger Cars Boosting Synthetic Demand

Turbocharged gasoline direct-injection engines create higher thermal loads and fuel-dilution stress, forcing OEMs to mandate full synthetics to control LSPI and prevent turbo coking. Domestic brands have mainstreamed 1.5-to-2.0-liter turbo engines across C-segment sedans and compact SUVs, lifting 0W-20/5W-30 sales in coastal showrooms where such models dominate. As the technology diffuses inland, synthetic penetration climbs, underpinning the value resilience of the China automotive engine oils market even when unit volumes stall.

Expansion of IAM Workshops & E-Commerce Retail

Independent aftermarket chains and pure-play online stores are eroding the dealer channel’s share, particularly in secondary towns where price sensitivity is acute. E-commerce enables small workshops to source directly, shrinking procurement layers and lowering retail prices by 8-10% versus offline averages. While the model widens product access, it also invites counterfeit listings, prompting regulators to expand QR-code traceability mandates. The channel shake-up intensifies brand-positioning battles yet keeps the China automotive engine oils market competitive on shelf despite its volume plateau.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging EV penetration | −0.08% | National, fastest in Tier 1 and coastal cities | Short term (≤ 2 years) |

| Longer OEM drain intervals & monitoring | −0.03% | National, premium vehicle segments first | Medium term (2-4 years) |

| Crack-down on counterfeit oils | −0.02% | National, concentrated in rural and secondary markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Longer OEM Drain Intervals & Oil-Life Monitoring

Mainstream OEMs now quote service intervals at 7,500-8,000 km with fully synthetic 0W-20 and 5W-30 oils, and many premium marques pair that with in-vehicle algorithms that push drains out when operating conditions are mild. Although each sump fill is larger, annual per-car lubricant consumption falls roughly 20% compared with 2020 practices, pressuring the China automotive engine oils market size even as unit prices rise.

Crack-Down on Counterfeit Oils Causes Grey-Channel Destocking

Sweeps by provincial quality bureaus have shuttered dozens of small refilling plants and pushed distributors to purge unlicensed stock. Legitimate players win share, but the near-term destock phase removes low-price liters from the trade, trimming apparent demand. Rural outlets feel the effect most acutely, explaining the sharper short-term volume contraction in those provinces.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PCMO Dominance Faces Gradual Erosion

Passenger car motor oil contributed 58.10% of 2025 volume, confirming its historical role at the center of the China automotive engine oils market. A broad viscosity spread—from legacy 10W-40 for older compact cars to modern 0W-20 for turbo GDI models—keeps the category diverse. The Chinese ride-hailing fleet still relies on ICE sedans and therefore underpins baseline PCMO demand in urban cores. Nonetheless, battery-electric sedans and crossovers account for an ever-larger share of new registrations, chipping away at the internal-combustion aftermarket. Motorcycle engine oil, by contrast, posts a 0.15% CAGR through 2031 thanks to the resilience of two-wheelers in parcel-delivery and rural transport duty cycles.

The heavy-duty motor-oil segment faces twin forces: emission norms that necessitate CK-4 level performance and pilot electrification projects in urban distribution. Range-extender trucks temporarily cushion volumes because they still carry small diesel generators, but pure-electric drayage initiatives in the Pearl River Delta foreshadow future shrinkage. Overall, passenger-car oil will remain the single largest bucket, yet its share will ebb as electrification accelerates and two-wheeler delivery fleets find new momentum in inland regions.

By Base Stock: Mineral Oils Retain Volume Leadership Despite Synthetic Growth

Mineral oils held 59.80% share in 2025, reflecting legacy vehicle mix and price sensitivity in inland provinces. Still, synthetics are growing at 0.28% CAGR—nearly triple the overall China automotive engine oils market growth—driven by mandatory low-viscosity requirements tied to emission rules and OEM warranty conditions. Group III capacity additions by Sinopec and CNOOC have narrowed the cost delta between mineral and high-grade base oils, supporting a further shift toward synthetics. Semi-synthetics bridge the two extremes, giving value-conscious consumers a credible step-up path. Bio-based alternatives remain niche because finished oil prices would need to rise another 25% to offset feedstock cost and supply tightness.

Looking ahead, large blenders are pivoting toward higher Group III+ barrels to future-proof their portfolio, while regional independents cling to mineral offerings to maintain entry-level price points. The resulting stratification means mineral liters will fall steadily but not collapse, ensuring supply continuity for the ageing parc even as the premium tier claims incremental revenue.

Geography Analysis

China’s coastal conurbations, such as Shanghai, Shenzhen, and Guangzhou, account for a disproportionate share of synthetic sales, driven by stricter emission enforcement and higher premium-car density. Penetration of 0W-20 PCMO already exceeds 60% of engine oil changes in these cities. Tier 1 EV adoption further compresses volume, yet the wallet share per liter sold rises because service outlets upsell OEM-approved synthetics.

Inland Tier 2-3 cities like Chengdu, Wuhan and Zhengzhou display a different profile. The balance of price sensitivity and slower EV pick-up keeps mineral 10W-30 and 15W-40 grades relevant. Independent workshops dominate service occasions, and e-commerce platforms close the supply gap by offering two-day delivery of branded products at factory-store prices. This combination ensures that the China automotive engine oils market continues to record a measurable flow of mineral liters even when national statistics appear stagnant.

Northern provinces face large seasonal swings. Sub-zero winters in Heilongjiang force multi-grade selections, while Xinjiang’s desert freight corridors favor robust 15W-40 diesel oils for off-road and mining rigs. Southern regions, blessed with milder temperatures, are rapidly standardizing 5W-30 as a year-round grade. Collectively, these regional nuances keep the blend slate fragmented and provide natural hedges that soften nationwide downturns in any one application.

Competitive Landscape

The China automotive engine oils market is consolidated. International majors Shell, ExxonMobil, and Castrol anchor the premium channel, each running multiyear OEM fill programs and offering warranty-linked aftersales ranges. Shell renewed its global contract with BMW in January 2024, extending exclusivity across 150 countries, including China[1]Shell plc, “Shell remains supplier of engine oil to the BMW Group in Asia and RoW,” shell.com . Domestic oil champions CNPC and Sinopec leverage integrated refining chains to secure roughly half of mainstream PCMO and heavy-duty market turnover. Their national station networks provide unrivaled last-mile reach into rural markets.

Regional independents such as Longpan Technology compete through private-label partnerships with fast-fit chains and by offering bespoke formulations for two-wheelers and agricultural machines. Several have become acquisition targets as larger players look for localized brands to complement flagship labels. The arrival of API SQ/ILSAC GF-7 prompted a surge in licensing; the top five suppliers already list more than 900 formulations, underlining their technical depth and setting a hurdle for smaller entrants.

Capital expenditure focuses on high-grade base stocks. CNOOC is investing CNY 5 billion to revamp its Taizhou unit, raising high-end lubricant capacity from 600,000 t/y to 1.4 million t/y by 2027[2]Taizhou Medical High-tech Industrial Development Zone Management Committee, “With an additional investment of 5 billion yuan, this place will become the largest full-range high-end lubricant industrial base in the country,” cmc.gov.cn . The new lines will integrate Fischer-Tropsch base oils, enabling domestic substitution of imports. Partnerships between additive houses and local blenders are also tightening so as to share R&D costs for e-drive fluids and hybrid-compatible diesel oils.

China Automotive Engine Oils Industry Leaders

BP p.l.c.

China National Petroleum Corporation

China Petrochemical Corporation

Shell plc

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2024: Shell has renewed its partnership with the BMW Group for the Rest of the World (RoW) and Asian markets. Through 2027, Shell will remain the exclusive engine oil producer and supplier for the aftersales operations of all BMW Group brands across more than 150 countries, including China.

- April 2024: Shell Lubricants has unveiled three new products under its flagship Shell Helix Ultra brand, catering to enhanced industry standards and original equipment manufacturer (OEM) specifications, empowering customers to harness greater engine performance.

China Automotive Engine Oils Market Report Scope

By Product Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

Key Questions Answered in the Report

What is the current demand level for engine oils in China?

Demand stands at 2.9 billion liters in 2026, with only a marginal increase projected to 2.92 billion liters by 2031, reflecting a 0.10% CAGR.

How does electric-vehicle growth affect lubricant volumes?

EVs remove crankcase-oil demand entirely and, in coastal Tier 1 cities, already cut the conventional market by several percentage points per year.

Which base-stock category is gaining share fastest?

Fully synthetic formulations grow at 0.28% CAGR, the quickest rate among all base stocks thanks to emission-standards compliance.

Where do premium synthetics sell most strongly in China?

Coastal metros such as Shanghai and Shenzhen, where high luxury-car density and stricter emission rules drive 0W-20 and 5W-30 adoption.

What role do e-commerce platforms play in lubricant distribution?

Online channels lower acquisition costs for workshops and consumers, widen product choice, and intensify price competition nationwide.

Page last updated on: