Chemicals & Materials

2nd JuneUnlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

The Japan Automotive Engine Oil Report is Segmented by Product Type (Passenger Car Motor Oil (PCMO), Heavy Duty Motor Oil (HDMO), and Motorcycle Engine Oil (MCO)), Base Stock (Mineral, Synthetic, Semi-Synthetic, and Bio-Based). The Market Forecasts are Provided in Terms of Volume (Litres).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

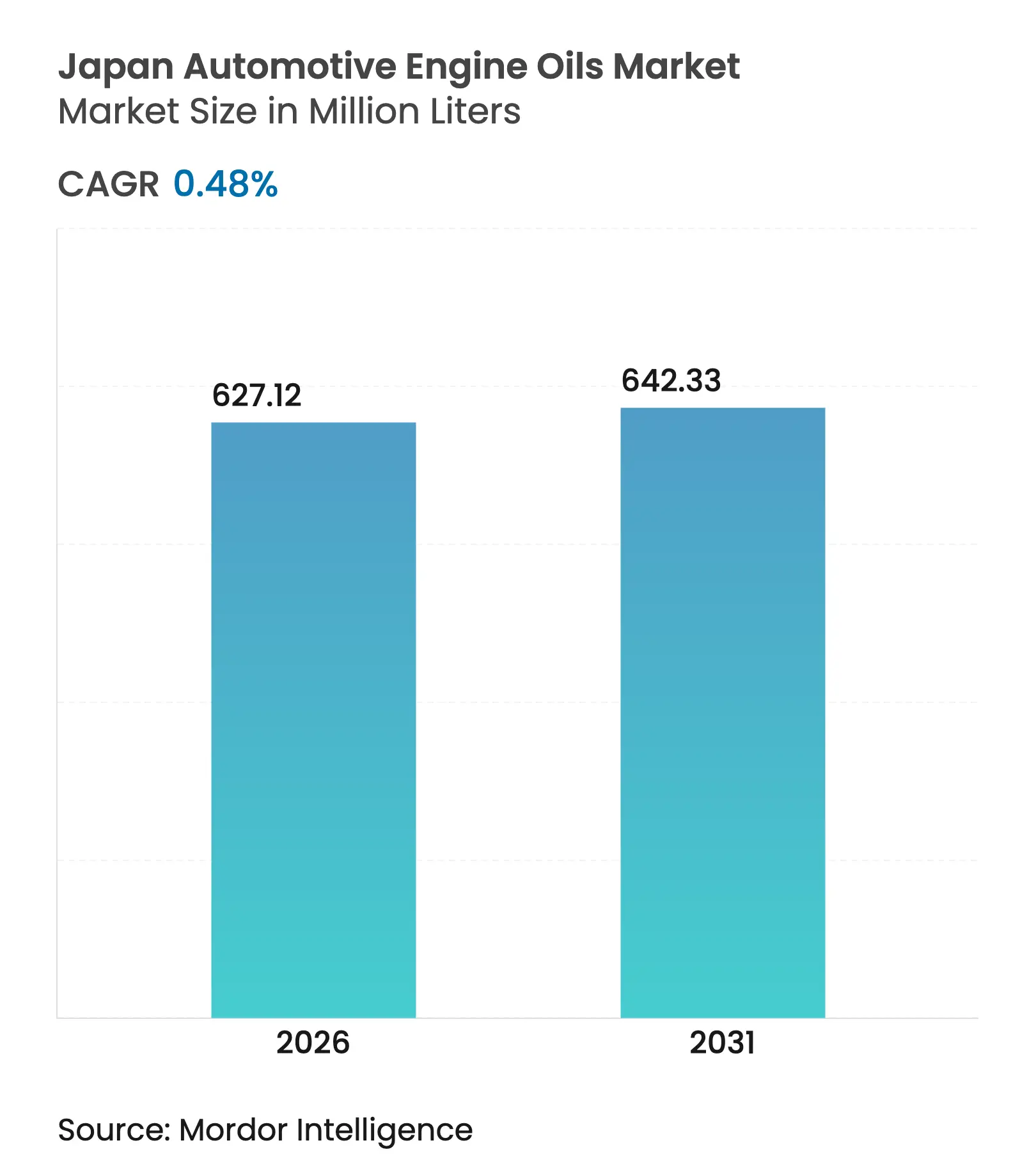

| Market Volume (2026) | 627.12 Million liters |

| Market Volume (2031) | 642.33 Million liters |

| CAGR | 0.48 % |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Japan Automotive Engine Oils Market size was valued at 624.12 Million liters in 2025 and estimated to grow from 627.12 Million liters in 2026 to reach 642.33 Million liters by 2031, at a CAGR of 0.48% during the forecast period (2026-2031). This modest trajectory reflects a mature vehicle parc, rapid electrification, and the industry’s accelerating pivot toward extended-drain synthetic formulations. Ultra-low-viscosity oils (0W-20 and below) account for an estimated 89-95% of factory fills as OEMs chase stringent corporate average fuel-economy targets. Mandatory nationwide “Shaken” inspections create predictable service intervals that partly cushion volume erosion, while start-stop-ready synthetics gain traction alongside Japan’s world-leading hybrid penetration. OEM-branded lubricants dominate replacement demand because factory-fill partnerships embed long-term brand loyalty inside dealer networks.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stricter CAFE-equivalent fuel-economy norms

Stricter CAFE-equivalent fuel-economy norms

| +0.3% | Nationwide, early adoption in Tokyo and Osaka | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+0.3%

|

Geographic Relevance

:

Nationwide, early adoption in Tokyo and Osaka

|

Impact Timeline

:

Medium term (2-4 years)

|

Hybrid-fleet expansion requiring start-stop-ready

synthetics

Hybrid-fleet expansion requiring start-stop-ready

synthetics

| +0.2% | Urban centers countrywide | Long term (≥ 4 years) | |||

Mandatory “Shaken” inspections sustaining oil-change

volumes

Mandatory “Shaken” inspections sustaining oil-change

volumes

| +0.1% | Nationwide | Long term (≥ 4 years) | |||

OEM factory-fill partnerships locking in branded sales

OEM factory-fill partnerships locking in branded sales

| +0.2% | Assembly hubs in Aichi, Kanagawa and others | Medium term (2-4 years) | |||

Quick-lube and e-commerce channels widening premium-oil

access

Quick-lube and e-commerce channels widening premium-oil

access

| +0.1% | Major cities, spreading to suburbs | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Stricter CAFE-Equivalent Fuel-Economy Norms Drive Ultra-Low-Viscosity Adoption

Japan targets a fleet average of 25.4 km per liter by 2030, a 32% jump over 2016 levels[1]International Energy Agency, “Fuel Economy Standards on Light-Duty Vehicles,” iea.org . Achieving this goal hinges on 0W-16 and 0W-8 formulations that reduce pumping losses without sacrificing wear protection. The Ministry of Land, Infrastructure, and Transport and METI use a corporate-average compliance framework that pressures every OEM to spec friction-modified synthetics across model ranges. Toyota and ENEOS jointly advanced the new JASO GLV-2 standard, enabling ultra-high-viscosity-index oils suited to electrified drivetrains. As Japanese hybrids operate engines at lower temperatures, lubricant chemistries must balance very-low-temperature fluidity with adequate high-temperature shear stability to preserve catalytic-converter durability.

Hybrid-Fleet Expansion Demanding Start-Stop-Capable Synthetics

Hybrids captured 18% of Japan’s new light-duty sales in 2019, the highest share among major economies. Start-stop events can exceed 500,000 cycles over a vehicle life, making film retention and additive robustness critical. ENEOS and Idemitsu validated new Group III+ basestock blends that retain viscosity after repeated micro-oxidation episodes during regenerative-braking shutdowns. Dealer workshops report rising demand for SP-rated synthetics labeled “Hybrid-Approved,” indicating consumer acceptance of premium price points in exchange for warranty adherence and fuel-economy retention.

Mandatory “Shaken” Inspections Sustaining Regular Oil-Change Volumes

Every passenger vehicle undergoes a mandatory Shaken test at year three and every two years thereafter. The program enforces OEM-recommended maintenance and emission checks, effectively anchoring oil changes at roughly 12- to 18-month intervals even as drain limits lengthen. Service operators align promotional bundles around inspection windows, keeping volume attrition below the pace implied by synthetic adoption. Inspection documentation requirements also encourage continued use of OEM labels because such proof simplifies resale and insurance procedures.

OEM Factory-Fill Partnerships Locking in Branded Oil Sales

OEM genuine oils supply 75% of Japan’s passenger-car lubricant demand, dwarfing the 10-15% penetration in China and India. Factory-fill contracts embed brand preference at purchase, while dealer loyalty programs reinforce repeat sales. ENEOS supplies Toyota, Nissan, and Mazda; Idemitsu services Honda, Subaru, and Daihatsu, and both firms maintain in-house additive development to meet proprietary engine tests. Global brands face protracted approval cycles and high localization hurdles, constraining new entrants despite attractive margins on synthetics.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

EV penetration eroding long-term ICE-oil demand

EV penetration eroding long-term ICE-oil demand

| -0.4% | Nationwide, fastest in megacities | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

-0.4%

|

Geographic Relevance

:

Nationwide, fastest in megacities

|

Impact Timeline

:

Long term (≥ 4 years)

|

Wide price gap between premium synthetics and mineral oils

Wide price gap between premium synthetics and mineral oils

| -0.2% | Price-sensitive consumer segments | Short term (≤ 2 years) | |||

Longer drain-interval technology lowering liters per

vehicle

Longer drain-interval technology lowering liters per

vehicle

| -0.1% | Premium-vehicle segments | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

EV Penetration Eroding Long-Term ICE-Oil Demand

Government subsidies, toll exemptions, and a growing public-charging network lifted battery-electric registrations 72% year on year in 2024. Full EVs eliminate engine oil use, while range-extender hybrids halve consumption. The Petroleum Association of Japan projects lubricant production sliding to 2.3 million kiloliters by 2030, versus 2.6 million kiloliters in 2023, mirroring falling gasoline throughput. Industry leaders therefore diversify into e-fluids, thermal-management coolants and hydrogen fuel partnerships to hedge revenue risk.

Wide Price Gap Between Premium Synthetics and Mineral Oils

Fully synthetic 4-liter packs retail at JPY 5,800 (USD 37.6) versus JPY 1,900 (USD 12.3) for mineral equivalents at mass-merchandise outlets. The 200-300% differential discourages cost-conscious owners who perceive oil as a commodity, especially in rural prefectures where annual mileage is low. Education programs from JASO and OEM dealers stress total-cost-of-ownership benefits, but price sensitivity remains a headwind while wage growth stagnates.

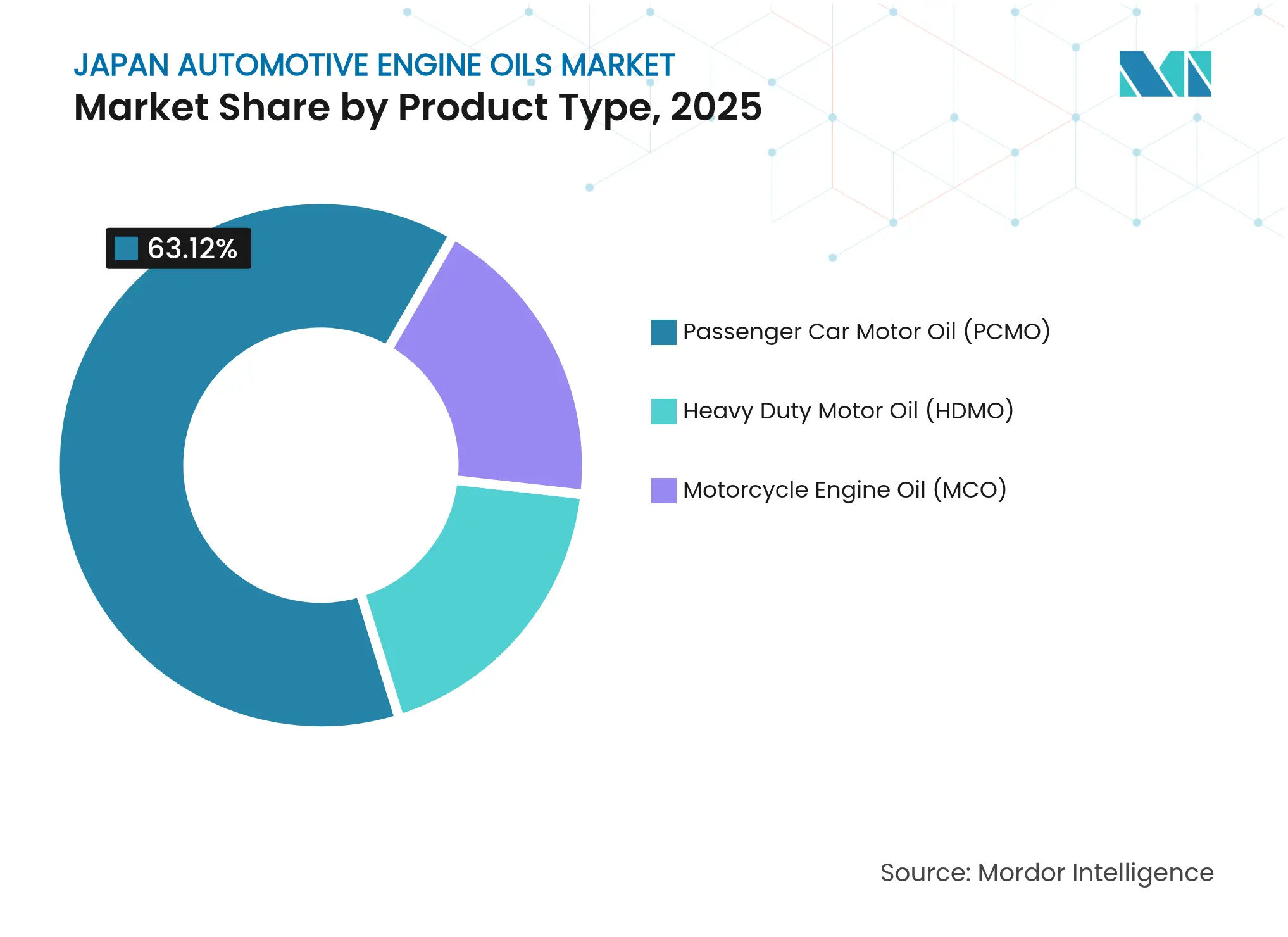

By Product Type: Passenger Car Motor Oil (PCMO) Dominates While MCO Accelerates

PCMO generated 63.12% of 2025 volume, underpinning the Japan automotive engine oil market through the country’s 61 million-unit passenger-car fleet. Nearly all new car models specify 0W-20 or thinner, cementing demand for Group III synthetics that deliver fuel-economy gains without warranty risk. The segment also benefits from high loyalty to OEM-genuine labels, reinforcing stable premium pricing.

Motorcycle Engine Oil records the fastest 0.74% CAGR as two-wheel registrations rose to 376,720 units in 2023 and micro-mobility trends expand scooter use in crowded urban corridors. JASO MA2 specifications for wet-clutch performance differentiate premium offerings, and Japanese riders show strong brand affinity toward domestic suppliers. Heavy-duty motor oil faces stagnation because electrified logistics pilots and hydrogen fuel-cell trucks gain government support, though construction and marine niches provide resilience.

Note: Segment shares of all individual segments available upon report purchase

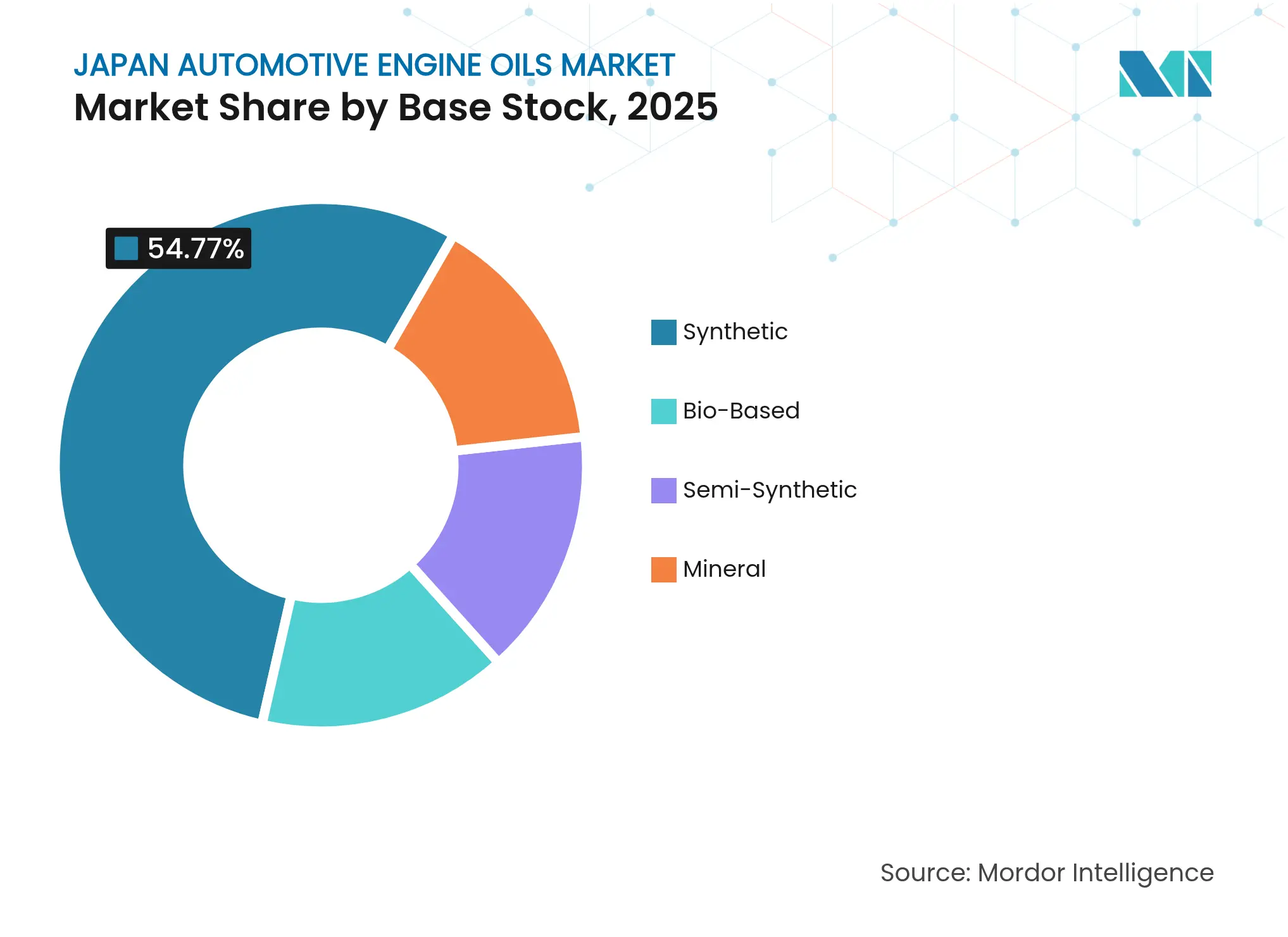

By Base Stock: Synthetic Oils Lead, Bio-Based Formulations Emerge

Synthetic grades captured 54.77% of 2025 consumption as OEM drain intervals extended beyond 10,000 km and ultra-low viscosities required higher VI base oils. Blenders favor hydrocracked Group III+ stocks, while a small share of Group IV PAOs targets high-performance and motorsport niches. The Japan automotive engine oil market size for synthetic products is forecast to add 8.9 million liters by 2031 despite flat overall demand, reflecting continued mineral-to-synthetic conversion.

Bio-based oils posted the quickest 0.61% CAGR on the back of Idemitsu’s IFG Plantech Racing launch in 2024, the first API SP product with over 80% plant-derived content. Government net-zero ambitions foster pilot programs for re-refining waste oils and integrating esterified vegetable bases. Semi-synthetics retain relevance among cost-sensitive drivers seeking partial fuel-economy benefits without the full synthetic price premium, whereas conventional mineral oils gradually lose share outside legacy fleets.

Note: Segment shares of all individual segments available upon report purchase

Japan’s archipelagic layout concentrates 68% of the population in three major metropolitan areas—Kanto, Chubu, and Kansai—driving premium lubricant demand in dense dealer networks. Tokyo alone accounts for roughly 17% of national PCMO volume due to high passenger-car density, stringent emission controls, and affluent consumers who favor OEM service packages.

Regional production clusters around Aichi Prefecture (Toyota), Kanagawa Prefecture (Nissan), and Hiroshima Prefecture (Mazda) tether factory-fill demand to nearby blending plants. These industrial zones benefit from just-in-time logistics and captive service channels that reinforce OEM-genuine brand dominance. Rural prefectures such as Hokkaido and Tohoku display a higher HDMO mix because of commercial agriculture and snow-removal fleets requiring higher-viscosity multigrades.

Japan relies on imports for 94.7% of its crude supply, mostly from the Middle East, making exchange-rate swings and maritime freight costs key input risks. Nineteen refineries provide sufficient base-oil output, yet declining transport-fuel throughput forces continuous capacity optimization. Consolidation reduced the national service-station count to 27,414 in March 2024 from 60,421 in 1995, prompting lubricant marketers to pivot toward e-commerce, quick-lube chains and dealer-installed “subscription” oil programs.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

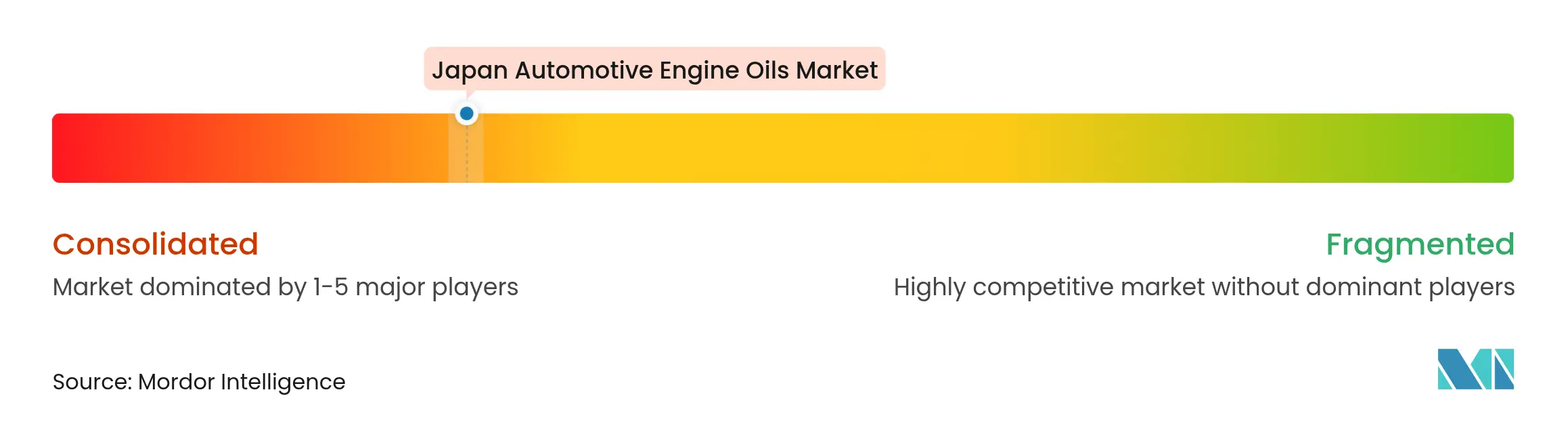

Market Concentration

The market is consolidated in nature. Recent diversification includes a USD 97 million stake in Danish e-methanol producer C2X and joint ventures for synthetic rubber, signaling hedging against flattening lubricant demand. ExxonMobil and TotalEnergies remain active in premium segments but struggle to breach entrenched OEM partnerships. High JASO certification costs, language-specific marketing, and strict end-user loyalty raise market-entry barriers, leaving collaborative research and development with domestic assemblers as the most viable route for newcomers.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Volume)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

8. Key Strategic Questions for CEOs

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

Unlocking Growth in India’s Luxury Beauty & Skincare Market

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.