Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

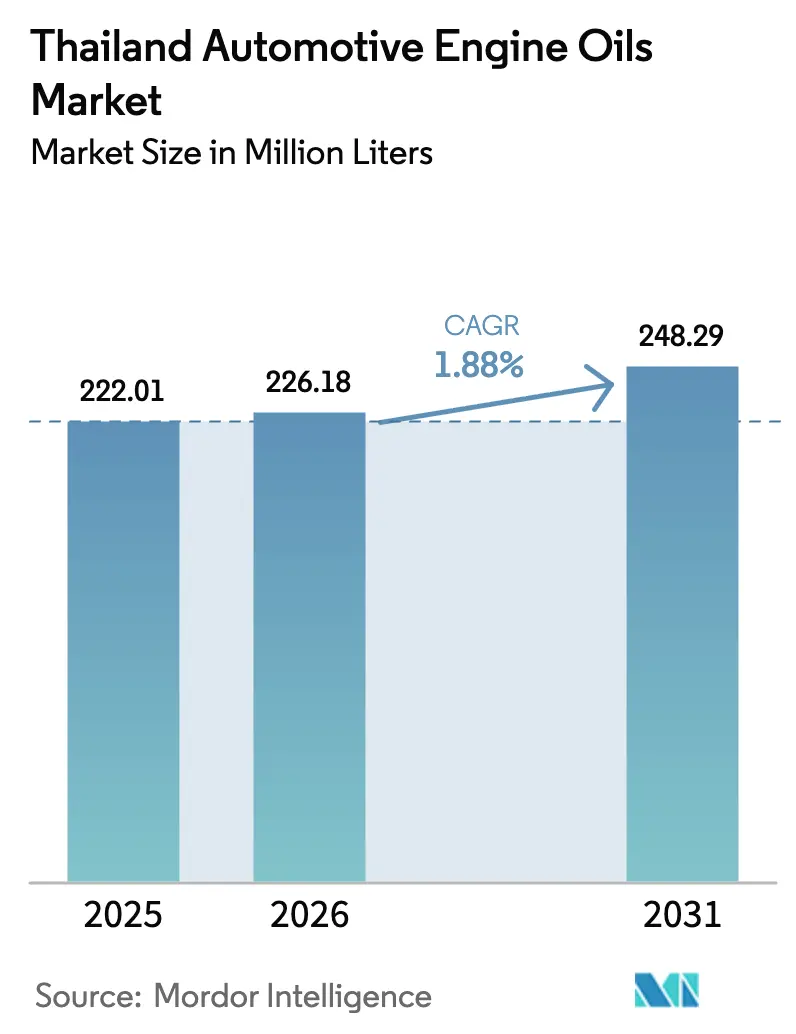

| Base Year Market Size (2025) | 222.01 Million Liters |

| Market Volume (2026) | 226.18 Million Liters |

| Market Volume (2031) | 248.29 Million Liters |

| Growth Rate (2026 - 2031) | 1.88% CAGR |

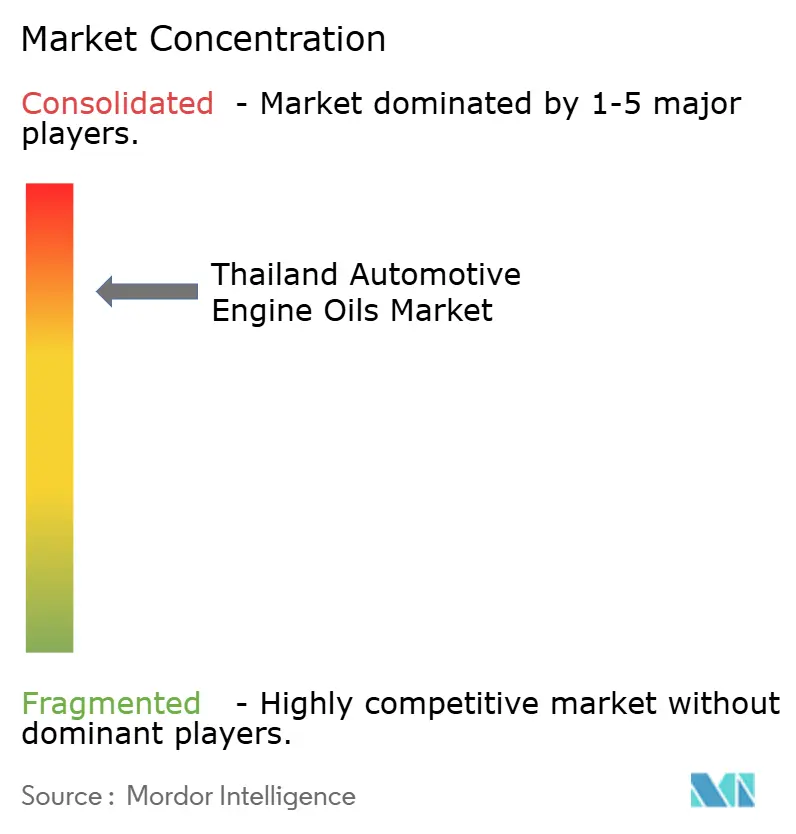

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Automotive Engine Oils Market Analysis by Mordor Intelligence

Thailand Automotive Engine Oils Market size in 2026 is estimated at 226.18 million liters, growing from 2025 value of 222.01 million liters with 2031 projections showing 248.29 million liters, growing at 1.88% CAGR over 2026-2031. Current expansion rests on steady vehicle output, stricter Euro 5 and Euro 6 emission limits, and rising demand for premium synthetic blends that safeguard modern engines. Japanese OEMs that anchor Thailand’s manufacturing base have moved quickly to recommend low-SAPS lubricants, channeling higher value into the aftermarket. Motorcycle production eclipses 3 million units a year, cushioning soft passenger-car demand and preserving lubricant volumes in urban delivery fleets. The Thailand automotive engine oils market also benefits from a dense service-center network that raises consumer awareness of routine maintenance, offsetting margin pressure from crude-oil swings.

Key Report Takeaways

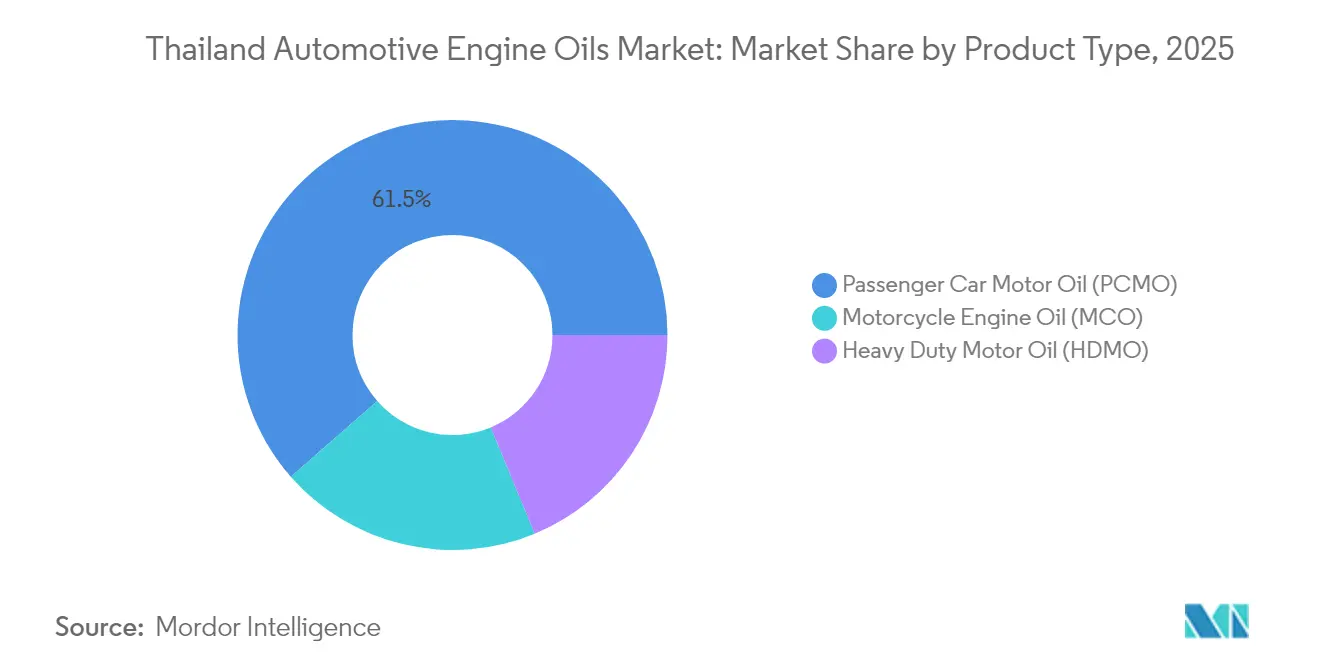

- By product category, passenger-car motor oil led with 61.45% of the Thailand automotive engine oils market share in 2025, while motorcycle engine oil is advancing at a 2.08% CAGR through 2031.

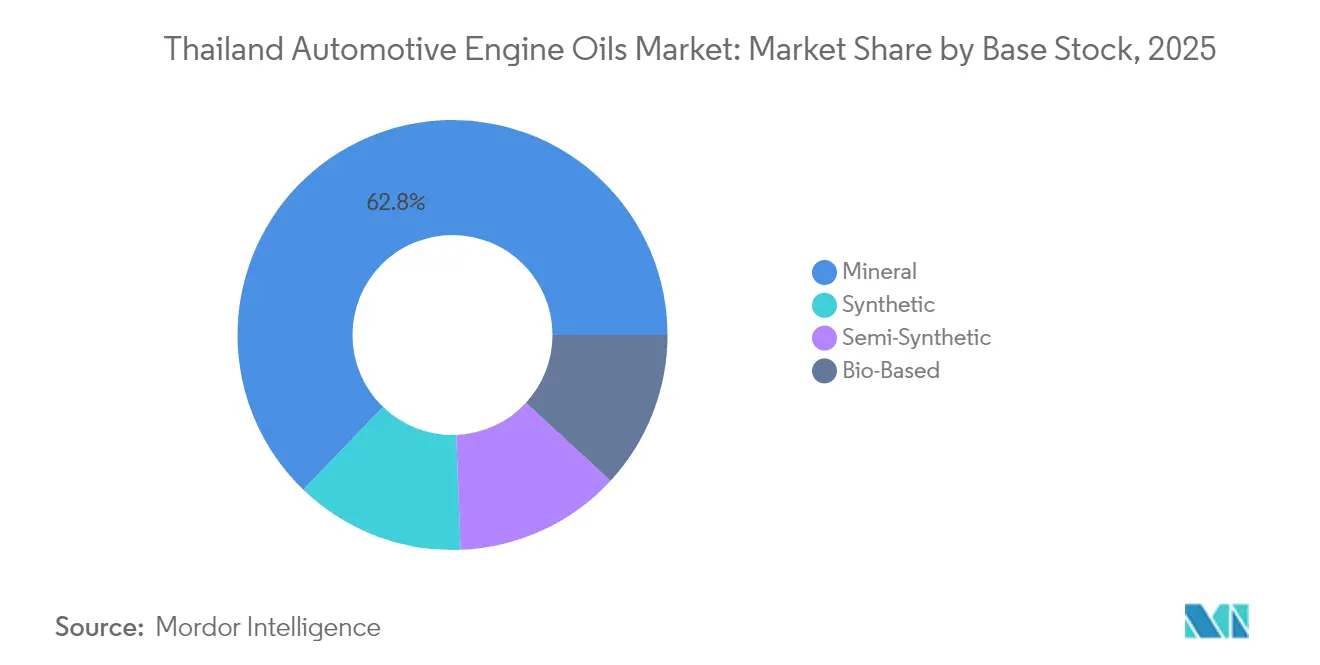

- By base stock, mineral oils held 62.80% of the Thailand automotive engine oils market size in 2025, and synthetic oils are projected to grow at a 2.33% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding vehicle population | +0.60% | Bangkok, Chonburi, Rayong industrial zones | Medium term (2-4 years) |

| Rising demand for premium and synthetic oils | +0.50% | Nationwide, early urban adoption | Short term (≤ 2 years) |

| Strong automotive manufacturing base | +0.40% | Eastern Economic Corridor | Long term (≥ 4 years) |

| Increasing maintenance and emission awareness | +0.30% | Nationwide | Medium term (2-4 years) |

| Growth in distribution and service networks | +0.20% | Urban to rural markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Vehicle Population Drives Consistent Lubricant Demand

Thailand’s vehicle parc continues to climb as domestic production targets 1.9 million units annually, led by Japanese OEMs that account for more than 70% of local output. In September 2025, Thailand recorded total sales of 48,350 units for passenger and commercial vehicles. Meanwhile, motorcycle sales surged to 134,440 units, driving a heightened demand for engine oils[1]The Thai Automotive Industry Association, “Thailand Automotive Statistics, September 2025,” taia.or.th . Continued logistics and e-commerce activity sustain light-truck and van fleets, balancing softer urban passenger-car purchases. Each newly registered vehicle underpins fresh demand in the Thailand automotive engine oils market, both at factory fill and in the aftermarket. Provincial governments improve road links that stimulate car ownership beyond Bangkok, broadening geographic consumption. Corporate fleet operators extend service contracts that lock in regular oil-change cycles, adding predictability to volume flow.

Premium Synthetic Lubricants Gain Traction from Regulatory Compliance

Euro 5 standards for diesel models came into force in January 2024, and Euro 6 rules for gasoline cars begin in January 2025, accelerating the switch to low-SAPS lubricants. OEM-specified full synthetics that meet ACEA C2, C3, and C5 grades extend drain intervals, curb tail-pipe pollutants, and protect after-treatment systems. Shell’s Helix Ultra and PTT’s EVOTEC lines exemplify premium offerings that now dominate showroom recommendations. Higher perceived engine-repair costs make owners receptive to high-value fluids, lifting the revenue mix inside the Thailand automotive engine oils market. The premium shift lessens exposure to crude-oil variability because additive content drives a larger share of finished-oil value.

Robust Manufacturing Base Anchors Long-Term Market Stability

Assembly plants in the Eastern Economic Corridor rely on engine oils for run-in, quality checks, and ancillary machinery, generating basal demand even when consumer sales fluctuate. The corridor’s integrated logistics make Thailand a regional export hub, ensuring that finished vehicles shipped to ASEAN markets carry Thai-sourced lubricants in their sumps. Multiyear investment agreements between Thailand and Japan on EV and bio-based materials endorse a production pipeline extending beyond 2030, which bodes well for the Thailand automotive engine oils market. The motorcycle cluster that turns out more than 3 million bikes annually further insulates lubricant volumes against cyclical passenger-car swings. Component makers also draw on process oils, bolstering the industrial side of demand.

Increasing Maintenance and Emission Awareness

Dealers and quick-lube chains now include emission-system warranty clauses that compel owners to stick to OEM-approved oils. Public education campaigns under the Fuel Control Act boost awareness that high-quality lubricants protect diesel particulate filters and catalytic converters, avoiding costly repairs. Service-center staff use handheld sensors to show sludge build-up, reinforcing the value of synthetic upgrades. As a result, the Thailand automotive engine oils market records rising acceptance of higher-priced SKU mixes. Insurance firms that bundle service packages further enhance routine-maintenance adherence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of electric vehicles | -0.40% | Nationwide, stronger in urban centers | Long term (≥ 4 years) |

| Volatile crude-oil and base-oil prices | -0.30% | Nationwide, Oil Fund price stabilization | Short term (≤ 2 years) |

| Fluctuating vehicle sales and production | -0.20% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Electric Vehicles Moderates Lubricant Use

Thailand’s 30@30 policy seeks a 30% EV production share by 2030, opening a slow but steady displacement path for spark-ignition engines. OEMs have announced battery-swap pilots for commercial fleets, pointing to eventual erosion in diesel-oil volumes. Although hybrids and range-extenders still need engine oil, the service interval lengthens, trimming per-unit demand. The Thailand automotive engine oils market will feel heavier impact in urban passenger-car segments where incentives cut EV sticker prices sharply. On the upside, EV-specific thermal-management fluids offer a new albeit smaller revenue stream for lubricant suppliers.

Fluctuating Vehicle Sales and Production Influence Short-Term Demand

Household debt near record highs constrains new-car purchases, and supply disruptions occasionally interrupt output schedules. Seasonal floods and weak farm incomes can dent rural motorcycle sales. While the automotive hub enjoys strong export demand, episodic declines in domestic registrations ripple into lubricant consumption. Flexible blending capacity and multi-channel sales strategies help cushion these shocks but cannot erase them entirely from the Thailand automotive engine oils market outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Passenger Cars Retain Volume, Motorcycles Accelerate Growth

Passenger-car motor oil contributed 61.45% of the Thailand automotive engine oils market share in 2025, reflecting the sizable car parc clustered in Bangkok and production centers. The segment leans on 5W-30 and 0W-20 viscosities aligned with Euro 5 rules, while hybrid-friendly low-viscosity grades are entering OEM aftersales programs. Demand spikes during festival travel months drive peak workshop throughput, reinforcing full-year stability. The Thailand automotive engine oils market for passenger-car oils is forecasted to experience steady growth through 2031, driven by emission mandates promoting the use of higher-value synthetic oils.

Motorcycle engine oil is forecast to be the fastest-growing category with a 2.08% CAGR, supported by annual output above 3 million units and rising gig-delivery services. Wet-clutch tolerant JASO MA2 formulations dominate, though scooter users increasingly opt for energy-saving synthetics that offer longer drains. The share gain of motorcycle oils offsets muted heavy-duty diesel demand, anchoring total market resilience. Broad availability of 1-liter packs through convenience stores lets brands tap impulse replacement purchases, enlarging the Thailand automotive engine oils market customer base.

By Base Stock: Mineral Grades Dominate, Synthetics Lead Value Expansion

Mineral oils represented 62.80% of the Thailand automotive engine oils market size in 2025, a legacy of local base-oil refining at IRPC’s 320 kiloton plant and Thai Oil’s Clean Fuel Project upgrades. Affordability keeps mineral volumes high in rural service shops and older vehicle fleets. However, crude volatility raises price risk, urging blenders to shift toward semi-synthetic mixes that command better margins.

Full synthetics are the fastest-growing base-stock group at 2.33% CAGR. OEM warranty clauses now cite ACEA and API 2025 standards that mineral oils cannot meet, moving the retail mix upward. Shell’s refinery upgrades and lubricant blending plant expansions underpin local supply, while PTT’s EVOTEC platform underscores government alignment on Euro 6 readiness. Although still below 30% volume share today, synthetics generate more than 45% of segment revenue, elevating profitability in the Thailand automotive engine oils market.

Geography Analysis

The Eastern Economic Corridor, spanning Chonburi, Rayong, and Chachoengsao, accounts for the largest regional share of volume because it hosts the majority of assembly plants and component suppliers. On-site fill oils, line-equipment fluids, and supplier contracts create a predictable offtake even when exports dip. Bangkok and its surrounding provinces contribute the largest aftermarket turnover, thanks to a dense population of passenger cars and motorcycles that rely on a web of service centers. Provincial migration into the capital adds incremental vehicles each year, maintaining fluid demand.

Northern hubs such as Chiang Mai and Lampang see growing two-wheeler ownership as tourism jobs raise incomes, shifting the regional balance inside the Thailand automotive engine oils market. Northeastern provinces, historically agricultural, are adopting pickup trucks that use heavier 15W-40 blends, providing diversity in product mix. Government road-building under the Transport Network Master Plan expands logistics corridors, lifting light-truck lubricant consumption outside the central plains.

Geographic demand will evolve unevenly once EV adoption accelerates. Bangkok’s charging infrastructure is expanding fastest, implying an earlier taper in combustion-engine oil sales there, while rural areas will retain conventional vehicles longer. Regional distributors are hedging by stocking EV coolant lines and importing gear-box oils for electric drivetrains, ensuring continuity in the Thailand automotive engine oils market during the transition.

Competitive Landscape

PTT Lubricants leverages its 190 FIT Auto shops and a storage capacity exceeding 263 million liters to maintain the largest share. As a state-backed refiner with integrated retail reach, it competes on availability and national pride branding. Shell focuses on technology leadership, winning the 2024 Asian Oil & Gas Award for maintenance innovation and maintaining its exclusive supply status with BMW Asia, thereby bolstering its premium persona. ExxonMobil expands its Mobil 1 workshop footprint by 30-50 sites yearly, reinforcing presence in premium passenger-car niches. PETRONAS addresses value-seeking consumers through its Nexta launch, bridging the price gap between mineral and full synthetics. LIQUI MOLY began local production in Thailand, cutting delivery times for motor oils across Asia and lowering the environmental footprint of imports[2]LIQUI MOLY GmbH, “LIQUI MOLY starts local production in Thailand,” liqui-moly.com .

Distribution density remains the key moat because it secures repeat aftermarket sales. All majors deploy oil-sampling kits and digital apps that track drain intervals, deepening customer stickiness in the Thailand automotive engine oils market. Marketing increasingly highlights compliance with Euro 6 emissions and reduced greenhouse-gas footprints, aligning with Thailand’s net-zero pledge. Suppliers also explore bio-based formulations; PTT Global Chemical’s tie-up with Toray on bio-nylon resin could deliver domestic feedstocks for sustainable esters.

Competition is intense but rational, with a handful of players controlling service-center channels and premium OEM recommendations. Mid-tier local blenders survive by offering private-label packs to dealer groups, while counterfeit pressure eases as QR-code traceability becomes standard. New entrants will find high barriers in logistics cost, dealer relationships, and brand credibility, limiting major share churn within the Thailand automotive engine oils market.

Thailand Automotive Engine Oils Industry Leaders

Bangchak Corporation

BP p.l.c.

Chevron Corporation

PTT Lubricants

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: LIQUI MOLY has commenced local production in Thailand to cater to the Asian market. This new facility enhances the speed of motor oil delivery while promoting environmental sustainability. The products manufactured in Thailand will be distributed not only within the country but across the entire Asian region.

- August 2024: PETRONAS unveiled PETRONAS Nexta, an automotive engine oil, in Thailand, targeting the affordable market segment with a premium lubricant solution. With an advanced formulation and high-quality ingredients, PETRONAS Nexta is designed to deliver optimal lubricant performance at a competitive price, enhancing the driving experience for consumers.

Thailand Automotive Engine Oils Market Report Scope

The Thailand Automotive Engine Oil is segmented by vehicle type. By vehicle type, the market is segmented into commercial vehicles, motorcycles, passenger vehicles) and by-product grade.

By Product Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

Key Questions Answered in the Report

How big is the Thailand automotive engine oils market in 2026?

The market stands at 226.18 million liters in 2026 and is forecast to hit 248.29 million liters by 2031, implying a 1.88% CAGR over 2026-2031.

Which segment leads current demand?

Passenger-car motor oil holds the largest volume share at 61.45% in 2025, driven by the large car parc concentrated in urban regions.

What is the fastest growing product category?

Motorcycle engine oil is projected to expand at a 2.08% CAGR through 2031 as delivery services and scooter ownership increase.

Why are synthetic oils gaining traction?

Euro 5 and Euro 6 emission regulations require low-SAPS formulations, and OEMs now recommend full synthetics to protect modern after-treatment devices.

How will EV adoption affect lubricant sales?

The 30@30 policy will reduce traditional engine-oil demand over the long run, especially in cities, but opens avenues for EV-specific thermal-management fluids.

Page last updated on: