Southeast Asia And Oceania Automotive Engine Oils Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

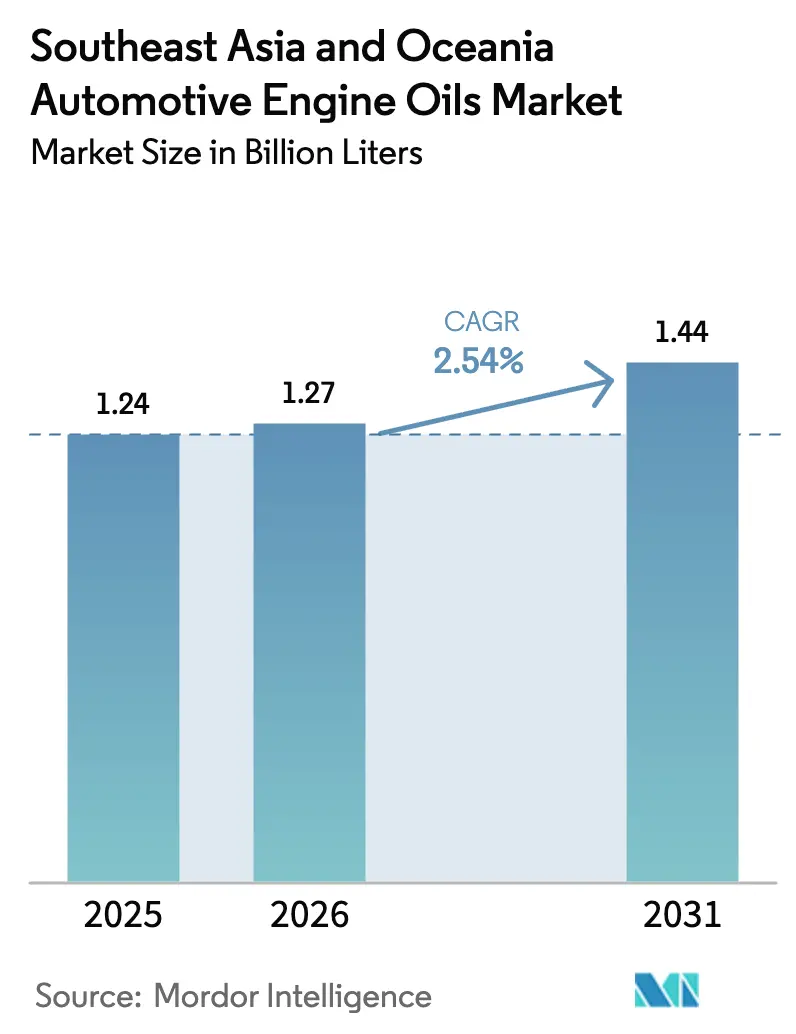

| Base Year Market Size (2025) | 1.24 Billion liters |

| Market Volume (2026) | 1.27 Billion liters |

| Market Volume (2031) | 1.44 Billion liters |

| Growth Rate (2026 - 2031) | 2.54% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia And Oceania Automotive Engine Oils Market Analysis by Mordor Intelligence

The Southeast Asia and Oceania Automotive Engine Oils market size is expected to grow from USD 1.24 billion in 2025 to USD 1.27 billion in 2026 and is forecast to reach USD 1.44 billion by 2031 at 2.54% CAGR over 2026-2031. Demand stability reflects the expansion of last-mile delivery fleets, cyclical mining activity, and persistent reliance on two-wheelers, even as electrification initiatives gradually gain traction. Integrated oil majors are deepening their regional blending capacity to shorten supply chains, while regulatory moves toward Euro 5/6 standards are shifting product mixes toward low-viscosity synthetics. Fleet digitization enables predictive maintenance, spurring uptake of premium synthetics despite total liters per vehicle trending lower. Meanwhile, motorcycle-centric urban mobility and resource-driven heavy-duty equipment usage are expected to anchor near-term volumes across ASEAN and Oceania.

Key Report Takeaways

- By product type, passenger car motor oil led with a 63.45% share of the Southeast Asia and Oceania automotive engine oils market in 2025. Motorcycle engine oil is advancing at a 2.67% CAGR through 2031.

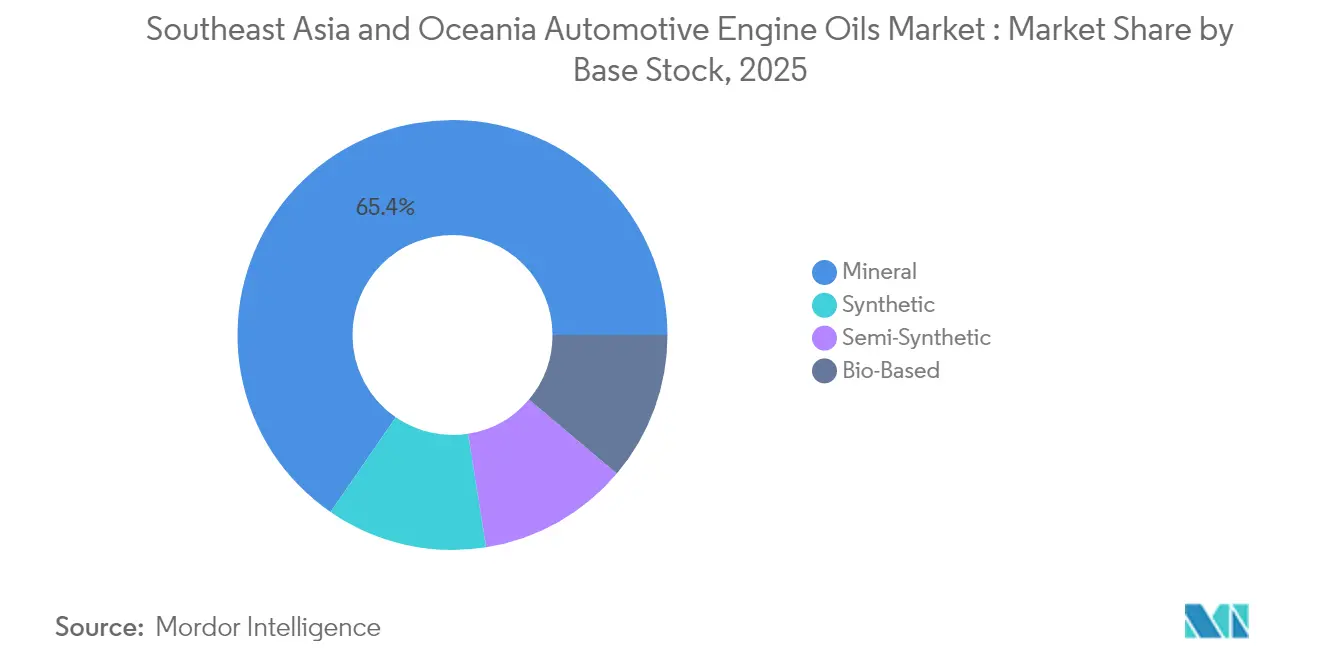

- By base stock, mineral formulations accounted for 65.40% of the Southeast Asia and Oceania automotive engine oils market size in 2025, while synthetic formulations posts the fastest growth at a 2.86% CAGR to 2031.

- By geography, Indonesia captured 30.20% of the Southeast Asia and Oceania automotive engine oils market size in 2025, while Australia posts the fastest growth at a 3.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia And Oceania Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging two-wheeler parc sustaining MCO volumes | +0.8% | Indonesia, Thailand, Vietnam, Philippines | Medium term (2-4 years) |

| E-commerce last-mile fleets shortening drain intervals | +0.6% | Urban hubs across ASEAN, Australia | Short term (≤ 2 years) |

| Mining and agricultural up-cycle in Oceania boosting HDMO | +0.4% | Australia, New Zealand | Long term (≥ 4 years) |

| Government fuel-economy mandates driving low-viscosity synthetics | +0.5% | Thailand, Malaysia, Singapore | Medium term (2-4 years) |

| Fleet subscription/telematics-led predictive servicing | +0.3% | Commercial fleet segments globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Two-Wheeler Parc Sustaining MCO Volumes

Indonesia recorded a growth in motorcycle sales in 2023. Similar scooter-centric mobility patterns in Thailand and Vietnam result in a high frequency of engine oil changes in humid, stop-start traffic. Younger urban populations view two-wheelers as an affordable mode of transportation, so 10W-30 and 15W-40 grades remain staple products. Lubricant makers position mid-tier semi-synthetics to address rising disposable incomes without pricing out cost-sensitive riders. Consequently, the Southeast Asia and Oceania automotive engine oils market continues to derive more than one-quarter of its total volume from motorcycle applications.

E-Commerce Last-Mile Fleets Shortening Drain Intervals

Same-day delivery expectations are compressing maintenance cycles for ride-hailing cars and two-wheelers, which now log higher annual mileage than privately owned vehicles. Telematics dashboards track lubricant condition, but limited charging infrastructure keeps many parcel-delivery businesses reliant on internal-combustion vans. As a result, the Southeast Asia and Oceania automotive engine oils market benefits from higher demand elasticity tied to booming online retail.

Mining and Agricultural Up-Cycle in Oceania Boosting HDMO

Rising iron-ore and coal prices revive Australian mine expansions, pushing haul-truck engine utilization hours upward and lifting heavy-duty motor oil needs. OEM manuals for Caterpillar and Komatsu equipment specify 15W-40 CK-4 oils to handle abrasive dust and high load factors. New Zealand’s dairy and vineyard sectors modernize tractors and harvesters, boosting demand for universal tractor transmission oils. Distributors in Perth and Brisbane report quarterly stock-outs of 200-liter drums during harvest and construction peaks. This operating intensity supports a premium mix, reinforcing revenue resilience within the Southeast Asia and Oceania automotive engine oils market.

Government Fuel-Economy Mandates Driving Low-Viscosity Synthetics

Thailand’s roadmap toward Euro 5/6 emissions, following its adoption of Euro 4 in 2012, requires OEMs to use 0W-20 or 0W-16 oils that reduce pumping losses[1]Binh Pham Hoa et al., “Status of Vehicle Emission Standards in the ASEAN Region,” Journal of Sustainable Development Innovations, jsi.aspur.rs. Malaysia’s 2024 lubricant certification scheme penalizes poor-quality blends, opening shelf space for high-performance synthetics. Singapore already taxes carbon emissions, nudging fleet owners toward fuel-efficient lubricants. Japanese GLV-2 draft specs influence hybrid passenger cars assembled in ASEAN, stimulating demand for very high viscosity index base stocks. Consequently, synthetic volumes increase by 2.93% annually, outpacing the overall growth of the Southeast Asia and Oceania automotive engine oils market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating BEV and e-2W penetration in urban hubs | -0.9% | Urban centers across ASEAN, Australia | Medium term (2-4 years) |

| Extended-drain synthetics lowering litres/vehicle | -0.4% | Premium vehicle segments globally | Short term (≤ 2 years) |

| High import dependence for additives (FX and freight volatility) | -0.3% | Import-dependent markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating BEV and e-2W Penetration in Urban Hubs

Jakarta, Bangkok, and Manila roll out incentive packages that reduce the purchase prices of electric motorcycles[2]Japan International Cooperation Agency, “Data Collection and Confirmation Survey on Electrical Motorcycle Industry Development and Strengthening of Supply Chain in Indonesia: Final Report,” jica.go.jp. Grab pilots battery-swap scooters that run oil-free powertrains, directly displacing conventional MCO liters. Australian states offer rebates on electric vans for urban freight, reducing diesel HDMO demand in metro corridors. While electrification uptake outside megacities remains slow, policy momentum is reallocating research and development budgets toward driveline fluids and thermal-management coolants, rather than crankcase oils, capping long-term volume upside for the Southeast Asia and Oceania automotive engine oils market.

Extended-Drain Synthetics Lowering Litres/Vehicle

Modern 0W-20 full synthetic oils allow drain intervals of 15,000–20,000 kilometers, which is double the conventional mineral oil recommendations. OEM warranty booklets for hybrid passenger cars now endorse 12-month service cycles, cutting annual oil change visits by half. Fleet managers who utilize predictive analytics through cloud-based dashboards report a decrease in lubricant purchase volume after switching to premium synthetics. Although liter losses are partly offset through higher per-liter margins, bulk-driven distributors must recalibrate sales targets in the Southeast Asia and Oceania automotive engine oils market toward value rather than sheer volume.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PCMO Dominance Faces MCO Growth Challenge

Passenger car motor oil accounts for 63.45% of the Southeast Asia and Oceania automotive engine oils market share in 2025, reflecting expanding car ownership across Indonesia, Thailand, and Malaysia. OEM shifts toward 5W-30 and 0W-20 viscosities gain traction in Singapore and Australia, driving up synthetic penetration and average selling prices. Heavy-duty motor oil is closely tied to freight, mining, and infrastructure cycles; sustained commodity exports keep Australian workshop bays busy servicing haul trucks and bulldozers. Motorcycle engine oil, however, is projected to post a 2.67% CAGR through 2031, underpinned by the dominance of scooters in urban mobility.

Synthetic MCO blends with molybdenum-based friction modifiers record the highest year-on-year growth within the segment, as ride-hailing riders seek better throttle response and longer clutch life. Premiumization remains gradual because consumer price sensitivity supports multi-brand stocking at informal kiosks. Consequently, distributors pursue channel segmentation, reserving flagship synthetics for e-commerce and workshop channels while allocating price-fighter brands to roadside stalls.

By Base Stock: Mineral Oils Retain Share Despite Synthetic Advancement

Mineral oils held 65.40% of the Southeast Asia and Oceania automotive engine oils market in 2025. Group I and II base stocks from Thai Oil and GS Caltex feed domestic blenders, enabling sharp pricing during promotional campaigns. Semi-synthetic offerings bridge the gap by bundling mineral content with synthetic components to meet API SP performance standards at mid-tier pricing. Group III+ synthetics, however, grow at a rate of 2.86% per year, driven by government emission roadmaps and OEM hybrid launches. Singapore imports PIONA-controlled base oils via the Jurong terminals and reships the drums to Malaysia and Vietnam under bonded arrangements, underscoring the regional supply interdependence.

Bio-based esters account small portion of Southeast Asia and Oceania's automotive engine oils market size, but they see niche uptake in marine outboard motors around the Great Barrier Reef, where biodegradability carries significant ecosystem value. Market education campaigns by specialty formulators emphasize oxidative stability and seal compatibility, countering concerns about compatibility with older engines. Looking ahead, synthetic share gains are expected to accelerate after 2027 as more ASEAN capitals align their fuel-economy taxation schemes with United Nations regulations.

Geography Analysis

Indonesia accounts for 30.20% of the 2025 regional volume, driven by its multi-million-unit motorcycle fleet and growing light-duty vehicle assembly base. Domestic distribution channels remain fragmented, so majors invest in branded kiosks and mobile vans to ensure product authenticity. Gradual electrification lowers long-run mineral MCO prospects but supports opportunities in e-transmission and coolant fluids.

Thailand and Malaysia are projected to present mid-single-digit growth, anchored by established component export industries. Thailand’s move toward Euro 6 dictates 0W-16 supply readiness, while Malaysia’s 2024 marking system for engine oils weeds out counterfeits, favoring multinationals with quality labs. Vietnam and the Philippines exhibit rising car penetration, yet they retain mineral oil dominance due to price sensitivity, thereby maintaining distribution models skewed toward wholesale-retail channels rather than service-center contracts.

Australia delivers the fastest 3.45% CAGR through 2031, thanks to mine expansions in Pilbara and coal seam gas projects in Queensland. Heavy equipment overhaul cycles accelerate lubricant consumption, despite modest growth in the vehicle population. Environmental policies encourage the adoption of CK-4 and FA-4 categories, prompting fleet managers to adopt full synthetics. New Zealand’s dairy and horticulture industries are adopting universal tractor oils compatible with Tier 4-Final engines, contributing to steady off-highway demand. Overall, Oceania generates high revenue per liter, thereby increasing profitability for suppliers that meet ISO 14001 supply-chain criteria.

Competitive Landscape

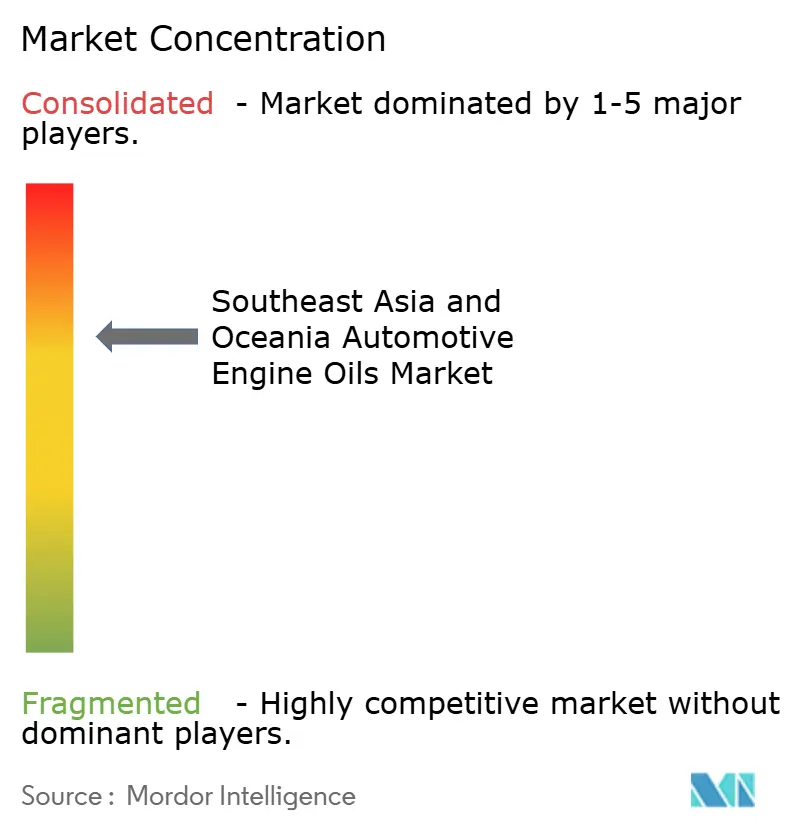

The Southeast Asia and Oceania automotive engine oils market is moderately concentrated. Telematics-enabled service bundles differentiate market leaders. Regional refiners integrate upstream base-oil supply with downstream branding, enabling consistent pricing despite fluctuations in feedstock prices. Niche importers focus on performance enthusiasts, highlighting the long tail of brand proliferation as regulations become tighter. Investment in dynamic inventory systems, tamper-evident packaging, and small-pack e-commerce SKUs is increasing, reflecting an evolution from commodity sales toward consumer-centric marketing. Overall, a supplier's competitive advantage hinges on blending flexibility, data-driven service capabilities, and distribution reach across thousands of islands and land borders.

Southeast Asia And Oceania Automotive Engine Oils Industry Leaders

Shell plc

PETRONAS Lubricants International

Exxon Mobil Corporation

BP p.l.c.

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: TOTALENERGIES subsidiary Lubrilog launched a PFAS-free Plastogrease range for automotive actuators, anticipating regulator restrictions on per- and polyfluoroalkyl substances.

- June 2025: BP p.l.c. initiated a process to divest its Castrol lubricants arm, valued at up to USD 10 billion, as part of a wider USD 20 billion disposal plan scheduled to be completed before 2027.

Southeast Asia And Oceania Automotive Engine Oils Market Report Scope

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| Malaysia |

| Singapore |

| Thailand |

| Vietnam |

| Indonesia |

| Philippines |

| Australia |

| Others (New Zealand, Cambodia and Myanmar) |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

| By Geography | Malaysia | |

| Singapore | ||

| Thailand | ||

| Vietnam | ||

| Indonesia | ||

| Philippines | ||

| Australia | ||

| Others (New Zealand, Cambodia and Myanmar) | ||

Key Questions Answered in the Report

How large is lubricant demand across Southeast Asia and Oceania in 2026?

Total demand is estimated at 1.27 billion liters, with a forecasted annual increase of 2.54% to 2031.

Which product category holds the biggest share today?

Passenger car motor oil captures 63.45% of the total 2025 volume, driven by expanding car ownership and OEM viscosity shifts.

Why is Australia the fastest-growing market in the region?

Mining and agricultural equipment modernization lifts heavy-duty motor oil usage, producing a 3.45% CAGR through 2031.

What factors accelerate synthetic lubricant adoption?

Emission rules moving toward Euro 5/6, OEM hybrid launches, and telematics-enabled fleet maintenance all push demand for low-viscosity synthetics.

How will EV penetration affect engine oil sales?

The uptake of battery-electric and electric two-wheelers, especially in urban hubs, reduces crankcase oil demand, thereby trimming growth.

Page last updated on: