Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

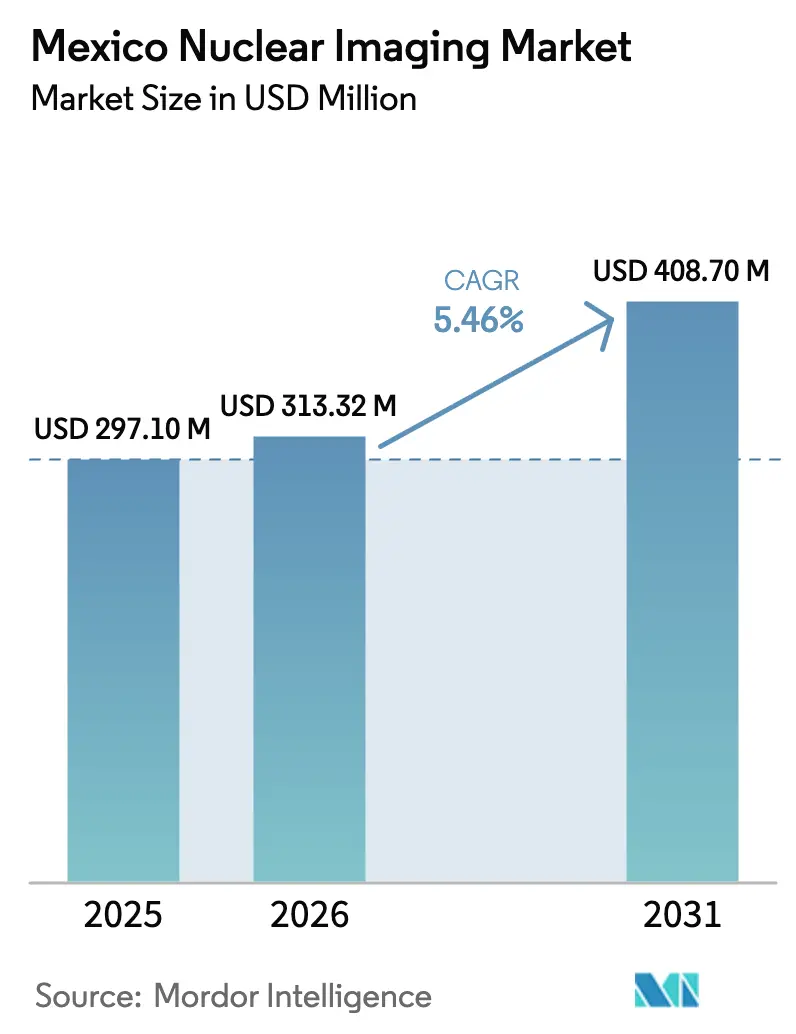

| Base Year Market Size (2025) | USD 297.1 Million |

| Market Size (2026) | USD 313.32 Million |

| Market Size (2031) | USD 408.7 Million |

| Growth Rate (2026 - 2031) | 5.46% CAGR |

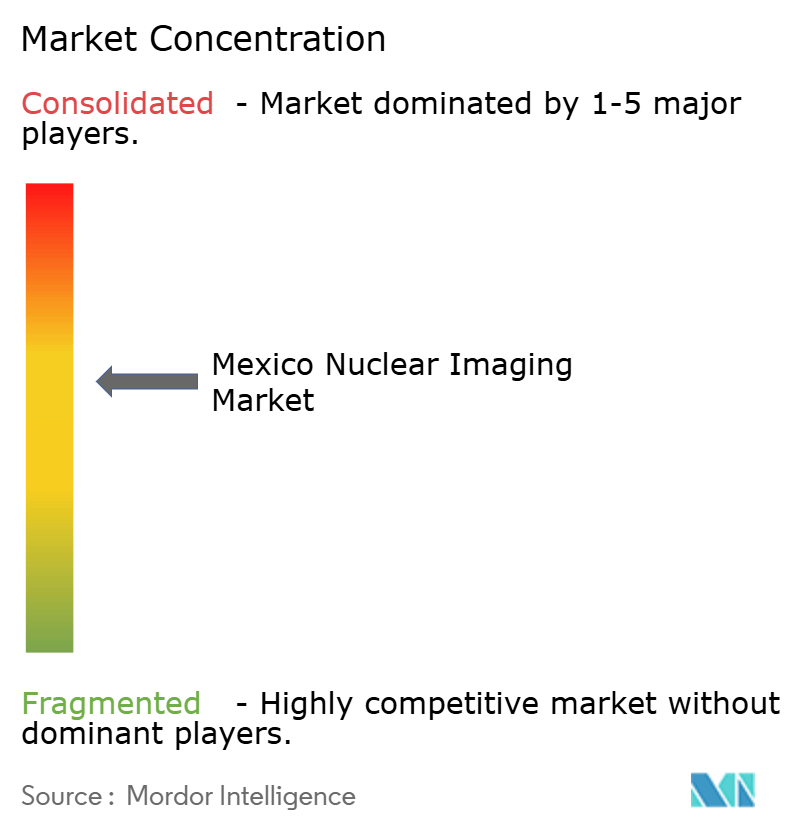

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Nuclear Imaging Market Analysis by Mordor Intelligence

The Mexico nuclear imaging market size is expected to grow from USD 297.1 million in 2025 to USD 313.32 million in 2026 and is forecast to reach USD 408.7 million by 2031 at 5.46% CAGR over 2026-2031. The upward trajectory is underpinned by sustained public and private investment in hybrid SPECT/CT and PET/CT systems, rising oncology and cardiology procedure volumes, and a modest but steady expansion of domestic PET radioisotope production capacity. Hospitals continue to dominate installed‐base counts, yet outpatient diagnostic chains are scaling rapidly, encouraged by shorter patient wait times and lower fee structures. Private nuclear pharmacies in Guadalajara and Monterrey add regional redundancy that reduces tracer transit hours, while cross-border supply chains with United States cyclotron operators support just-in-time deliveries of Fluorine-18. Workforce shortages and customs-related Mo-99 delays remain structural headwinds, although the government’s consolidated procurement program is expected to streamline equipment acquisition and lower isotope unit costs for public institutions.

Key Report Takeaways

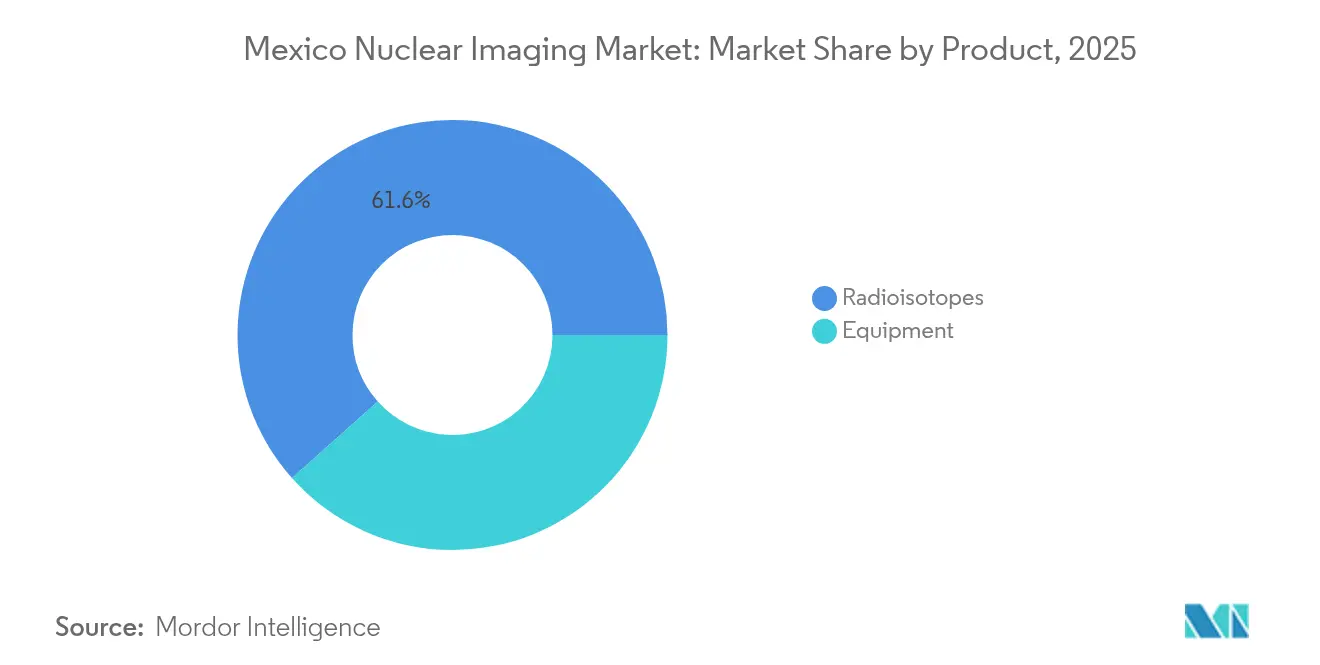

- By product, radioisotopes held 61.58% of Mexico nuclear imaging market share in 2025 and are projected to expand at a 5.58% CAGR to 2031.

- By application, SPECT captured 69.80% revenue share in 2025, while PET is advancing at a 5.88% CAGR through 2031 on expanding oncology indications.

- By end user, hospitals commanded 53.10% of the Mexico nuclear imaging market size in 2025, whereas diagnostic centers are forecast to grow at 5.95% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Nuclear Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cancer & CVD incidence | +1.0% | National, concentrated in Mexico City, Guadalajara, Monterrey | Medium term (2-4 years) |

| Public-sector imaging capex (INSABI, IMSS) | +0.9% | National, prioritizing underserved regions | Short term (≤ 2 years) |

| Hybrid SPECT/CT & PET/CT upgrades | +0.7% | Major metropolitan areas, private sector leading | Medium term (2-4 years) |

| Private nuclear-pharmacy build-out (Guadalajara, Monterrey) | +0.5% | Regional hubs with spillover to secondary cities | Long term (≥ 4 years) |

| Early adoption of total-body PET for paediatric oncology | +0.4% | Specialized pediatric centers in major cities | Long term (≥ 4 years) |

| Cross-border JIT tracer logistics with U.S. suppliers | +0.3% | Northern border regions, national distribution | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Cancer & Cardiovascular Incidence

Non-communicable disease prevalence continues to climb in Mexico, driving demand for myocardial perfusion imaging and FDG-PET scans. Cancer incidence is highest in Mexico City, Guadalajara, and Monterrey, and an aging population keeps procedure pipelines full for staging and response monitoring. Expanded IMSS-Bienestar coverage broadens access to molecular imaging among previously underserved households, lifting scan volumes at both public and private facilities. The IAEA ARCAL 2030 plan lists Mexico among nations in Latin America that must reinforce nuclear medicine capacity to meet oncology and cardiology workloads[1]International Atomic Energy Agency, “Agenda ARCAL 2030: Regional Strategic Profile for Latin America and the Caribbean 2022-2029,” iaea.org. The predictable patient base encourages capital allocation for hybrid scanners and in-house radiopharmacies.

Public-Sector Imaging Capex (INSABI, IMSS)

The federal consolidated procurement platform covering 2025-2026 earmarks multiyear budgets for high-tech equipment, radioisotopes, and service contracts across IMSS-Bienestar and ISSSTE hospitals. Centralized purchasing through state manufacturer Birmex aggregates volumes, improving supplier terms and shortening tender cycles. Public bids stipulate hybrid modality preferences, pushing vendors to package scanners, software, maintenance, and workforce training. Regional medical centers in secondary cities gain stable funding streams that justify nuclear medicine suite build-outs. Early purchase orders released in 2025 feature SPECT/CT systems and dedicated PET hot cells, signaling near-term volume for both equipment and consumables.

Hybrid SPECT/CT & PET/CT Upgrades

Clinical guidelines increasingly favor hybrid modalities that offer fused functional and anatomical datasets, especially for cardiology and oncology. SPECT/CT improves lesion localization, while PET/CT elevates lesion detectability and quantification. Private tertiary hospitals in Monterrey installed time-of-flight PET/CT during 2024, reporting throughput gains that trimmed per-patient scan slots by up to 20%. Vendors bundle AI reconstruction software that preserves image quality at lower tracer doses, minimizing radiation burden for patients. COFEPRIS has accelerated device review times for hybrid modalities after adopting the Equivalence and Recognition route in 2025, reducing import-to-clinical use lag by several months.

Private Nuclear-Pharmacy Build-out

Regional radiopharmacy capacity in Guadalajara and Monterrey is rising, with two Good Manufacturing Practice‐certified sites commissioned during 2024. Local Fluorine-18 production mitigates decay losses inherent in long trucking legs from Mexico City and compresses delivery windows to two hours for clinics within a 150 km radius. On-site synthesis modules enable higher batch frequency for niche tracers such as Ga-68 PSMA. Redundant output buffers facilities from customs-related Mo-99 supply gaps and reduces per-dose costs. Investors report break-even timelines within five years, supported by recurring consumables demand from diagnostic chains that operate extended clinic hours.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High equipment & maintenance costs | -0.7% | National, affecting smaller facilities disproportionately | Long term (≥ 4 years) |

| Limited reimbursement for advanced scans | -0.6% | National, private sector concentrated impact | Medium term (2-4 years) |

| Mo-99 supply delays at Mexican customs | -0.4% | National, border regions most affected | Short term (≤ 2 years) |

| Shortage of certified nuclear-medicine technologists | -0.3% | National, rural areas disproportionately affected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Equipment & Maintenance Costs

Capital intensity requirements for nuclear imaging equipment create significant barriers to market entry, particularly affecting smaller healthcare facilities and limiting geographic expansion beyond major metropolitan areas. PET/CT systems require investments exceeding USD 2 million, while ongoing maintenance contracts and isotope procurement create substantial operational expenses that strain facility budgets. The technical complexity of nuclear imaging systems necessitates specialized service agreements with original equipment manufacturers, often requiring international technician support that increases maintenance costs. Smaller diagnostic centers struggle to achieve sufficient patient volumes to justify hybrid system investments, creating market concentration among larger facilities with adequate financial resources. Currency fluctuations between the Mexican peso (MXN) and US dollar (USD) affect equipment procurement costs, as most nuclear imaging systems are imported from international manufacturers. Limited availability of local technical expertise increases dependence on expensive international service contracts and extends system downtime during maintenance procedures.

Mo-99 Supply Delays at Mexican Customs

Customs processing delays for Molybdenum-99 imports create critical supply chain vulnerabilities that directly impact SPECT imaging availability across Mexico's healthcare system. Mo-99's 66-hour half-life makes customs delays of 2-3 days particularly damaging, as isotope activity levels become insufficient for clinical use by the time they reach healthcare facilities[2]United States International Trade Commission, “Stable and Radioactive Isotopes,” usitc.gov. The regulatory complexity surrounding radioactive material imports requires specialized documentation and inspection procedures that contribute to processing delays at border crossings. Mexican customs authorities lack sufficient trained personnel familiar with radioisotope handling requirements, creating bottlenecks during peak import periods. Alternative supply routes through different border crossings provide limited relief, as all radioactive material imports require similar regulatory scrutiny and documentation. The supply chain disruptions force healthcare facilities to maintain larger isotope inventories or cancel procedures, both of which increase operational costs and reduce patient access to nuclear imaging services.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Radioisotopes Sustain a Consumables-Heavy Profile

Radioisotopes commanded 61.58% of the Mexico nuclear imaging market share in 2025. The Mexico nuclear imaging market size for radioisotopes is projected to rise at a 5.58% CAGR to 2031 as Technetium-99m continues to anchor SPECT demand. Consumables spending is recurrent, generating predictable cash flow for radiopharmaceutical vendors and prompting new entrants to establish GMP-grade production lines. Curium Pharma’s March 2025 acquisition of Monrol expanded Latin American Lutetium-177 output capacity and positions the firm to supply therapeutic isotopes for prostate cancer programs. PET tracers, led by Fluorine-18, log the fastest volume growth owing to oncology indications, and wider distribution of cyclotrons in tertiary cities further supports adoption. Capital equipment, while representing only 38.42% of 2025 value, exerts pivotal influence on long-term modality mix. Replacement cycles of 10-15 years shape tender calendars, allowing OEMs to introduce novel detector technologies and dose-reduction software that reinforce the hybrid migration trend.

Equipment procurement remains concentrated in high-acuity metropolitan hospitals that can shoulder million-dollar outlays and maintain qualified staff. Smaller facilities gravitate toward refurbished scanners or service subscriptions that bundle uptime guarantees and per-scan pricing. Currency risk persists because nearly all hardware is imported. Vendors that provide peso-denominated leasing, remote diagnostics, and on-site training win share, especially in diagnostic center chains expanding outside the capital. The expanding PET tracer portfolio, including Ga-68 and Zr-89, is expected to boost theranostics programs and tilt purchasing toward systems with time-of-flight and extended field-of-view capabilities.

By Application: SPECT Retains Scale, PET Gains Momentum

SPECT held 69.80% of 2025 revenue, reflecting entrenched clinical pathways for myocardial perfusion and thyroid imaging. Lower tracer cost and broader reimbursement underpin its dominance. Cardiology constitutes the largest SPECT workload, supported by Mexico’s high prevalence of ischemic heart disease, while neurology and thyroid contribute steady baseline volumes. PET revenue, although smaller, is set to expand faster through 2031 as oncologists adopt FDG-PET for early staging and therapy monitoring. Major private networks in Monterrey report double-digit annual PET scan growth since 2023, attributing the uptick to rising middle-income insurance penetration and physician familiarity with molecular imaging guidelines.

The expanding PET user base benefits from newly commissioned cyclotrons that reduce per-dose prices and enable same-day tracer access in secondary cities. Hybrid SPECT/CT upgrades inject incremental functional-anatomical quality into the legacy modality, extending its competitive runway versus PET. Intervention planning tools embedded in new software packages improve referring-physician confidence and sustain SPECT volumes. Specialty subsegments, such as infection imaging with tagged white blood cell tracers, remain niche but profitable, serviced mostly by academic hospitals conducting complex cases.

By End User: Hospitals Lead, Diagnostic Centers Accelerate

Hospitals accounted for 53.10% of 2025 revenue thanks to integrated oncology and cardiology programs that depend on in-house nuclear medicine units for multidisciplinary care. Teaching hospitals contribute a significant share of first-in-human tracer studies and complex pediatric protocols, aided by dedicated radiopharmacists and physicists. IMSS-Bienestar’s regional expansion is expected to bring new hybrid systems to medium-sized cities, unlocking latent demand among social security beneficiaries. The hospital channel also captures emergent therapeutic radioisotope use, including 177Lu-PSMA and 131I-MIBG treatments, which require specialized isolation wards.

Diagnostic centers, though still trailing, are registering a 5.95% CAGR through 2031 as outpatient care shifts away from inpatient campuses. GE HealthCare and Salud Digna have validated the hub-and-spoke model that links tier-1 imaging hubs to community spokes, enabling high patient throughput and consistent protocol execution. Chains leverage purchase scale to negotiate favorable isotope pricing and invest in cloud platforms that automate dose tracking and quality assurance. Academic and research institutes remain a focused niche, representing less than 5% of the Mexico nuclear imaging market; they function as engines for tracer innovation and workforce training.

Geography Analysis

The Mexico nuclear imaging market is geographically concentrated in three metropolitan areas that host the bulk of the installed scanner base and radiopharmacy sites. Mexico City accounts for the largest cluster of hybrid systems, reflecting its dense hospital ecosystem and high specialist headcount. Guadalajara and Monterrey follow, each supported by newly licensed private cyclotrons that shorten Fluorine-18 supply lines. The high density of PET and SPECT services in these corridors allows logistics firms to consolidate isotope deliveries, improving cost efficiency. Northern border states enjoy proximity to United States suppliers, receiving daily shipments of short-lived tracers under just-in-time arrangements that improve dose utilization.

Secondary cities such as León, Puebla, and Mérida register rising scan volumes as diagnostic center chains deploy refurbished SPECT cameras and partner with regional radiopharmacies for generator exchange programs. Public-sector tenders scheduled for 2025–2026 earmark hybrid scanners for IMSS-Bienestar hospitals in Chiapas and Oaxaca, signaling incremental expansion into underserved south-southeast regions. Infrastructure gaps persist, however, with limited technologist availability and irregular power grids constraining continuous operation of cyclotron facilities outside the main metros.

Cross-border dynamics introduce both resilience and fragility. While northern states benefit from fast-track agreements that expedite Fluorine-18 clearance, they also share exposure to Mo-99 congestion when customs stalls shipments at congested ports of entry. Coastal states rely on airfreight routes from central Mexico, adding cost premiums that restrain elective scan adoption. Government efforts to incentivize decentralization include tax credits for private radiopharmacy investments in states with below-average diagnostic imaging penetration. The IAEA’s regional cooperation programs have identified two new candidate sites for cyclotron deployment by 2027, which would elevate national PET tracer self-sufficiency above 90%.

Competitive Landscape

Competitive intensity in the Mexico nuclear imaging market remains moderate. No single vendor commands share across both capital equipment and consumables, which sustains pricing discipline and innovation. GE HealthCare, Siemens Healthineers, and Philips dominate high-end scanner bids by bundling AI reconstruction, service, and financing. Their multi-modal portfolios cater to both PET/CT and SPECT/CT upgrade pipelines. Curium, Novartis, and Bracco lead the radioisotope segment through differentiated product depth and aggressive in-country logistics footprints. Curium’s acquisition of Monrol gives it a head start in theranostics tracer supply, while Novartis leverages global Lu-177 production to support its radioligand therapy rollouts.

Mid-tier disruptors are capitalizing on unmet needs outside Mexico City. Regional radiopharmacy operators such as Pharmaconnect in Monterrey and Nuklear Labs in Guadalajara are gaining traction by offering same-day Fluorine-18 and scheduled Ga-68 deliveries on subscription plans. Service-as-a-solution models, where vendors retain scanner ownership and charge per study, are trialing in private chains to lower up-front capex. International OEMs partner with local engineering firms to expand field service capacity and keep downtime under 3%, a key requirement for high-volume outpatient centers.

Regulatory familiarity is a decisive moat. Firms with established COFEPRIS dossiers navigate variant submissions for detector upgrades more swiftly, granting a temporary sales window before rivals receive clearance. Training alliances with academic centers also amplify vendor brand presence and provide user feedback loops for product refinement. Although the top five players together hold well below 70% revenue share, incumbents retain durable advantages in service infrastructure, clinical education, and integrated solutions.

Mexico Nuclear Imaging Industry Leaders

Bracco Imaging Spa

GE Healthcare

Koninklijke Philips N.V

Siemens Healthineers

Canon Medical System

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Curium Pharma completed acquisition of Monrol to significantly expand Lutetium-177 capacity and PET footprint, positioning the company as a leading manufacturer of Lu-177 isotopes crucial for targeted radionuclide therapy.

- February 2025: Instituto Mexicano del Seguro Social announced plans to inaugurate 9 hospitals and 6 Family Medicine Units across 12 Mexican states in 2025, including the Hospital General de Zona in Tuxtla Gutiérrez.

- January 2025: IMSS-Bienestar initiated hybrid SPECT/CT installations at five regional hospitals to close diagnostic gaps in underserved cities.

Mexico Nuclear Imaging Market Report Scope

Nuclear medicine imaging procedures are non-invasive, with the exception of intravenous injections, and are usually painless medical tests that help physicians diagnose and evaluate medical conditions. These imaging scans use radioactive materials called radiopharmaceuticals or radiotracers. These radiopharmaceuticals are used in diagnosis and therapeutics.

Mexico's nuclear imaging market is segmented by product and application. Based on the product the market is segmented as equipment and diagnostic radioisotope. Based on application the market is segmented as SPECT application and PET application. The report offers the value (in USD) for the above segments.

By Product

| Equipment | PET/CT Scanners | |

| SPECT/CT Scanners | ||

| PET/MRI Scanners | ||

| Radioisotopes | SPECT Radioisotopes | Technetium-99m (Tc-99m) |

| Thallium-201 (Tl-201) | ||

| Gallium-67 (Ga-67) | ||

| Iodine-123 (I-123) | ||

| Other SPECT Isotopes | ||

| PET Radioisotopes | Fluorine-18 (F-18) | |

| Rubidium-82 (Rb-82) | ||

| Other PET Isotopes | ||

By Application

| SPECT Applications | Cardiology |

| Neurology | |

| Thyroid | |

| Other SPECT Applications | |

| PET Applications | Oncology |

| Cardiology | |

| Neurology | |

| Other PET Applications |

By End User

| Hospitals |

| Diagnostic Imaging Centers |

| Academic & Research Institutes |

| By Product | Equipment | PET/CT Scanners | |

| SPECT/CT Scanners | |||

| PET/MRI Scanners | |||

| Radioisotopes | SPECT Radioisotopes | Technetium-99m (Tc-99m) | |

| Thallium-201 (Tl-201) | |||

| Gallium-67 (Ga-67) | |||

| Iodine-123 (I-123) | |||

| Other SPECT Isotopes | |||

| PET Radioisotopes | Fluorine-18 (F-18) | ||

| Rubidium-82 (Rb-82) | |||

| Other PET Isotopes | |||

| By Application | SPECT Applications | Cardiology | |

| Neurology | |||

| Thyroid | |||

| Other SPECT Applications | |||

| PET Applications | Oncology | ||

| Cardiology | |||

| Neurology | |||

| Other PET Applications | |||

| By End User | Hospitals | ||

| Diagnostic Imaging Centers | |||

| Academic & Research Institutes | |||

Key Questions Answered in the Report

How large is the Mexico nuclear imaging market in 2026?

The Mexico nuclear imaging market size stands at USD 313.32 million in 2026.

What is the projected CAGR through 2031?

The market is forecast to grow at a 5.46% CAGR between 2026 and 2031.

Which product type holds the biggest share?

Radioisotopes contribute the largest slice, at 61.58% of 2025 revenue.

Why are diagnostics centers expanding quickly?

Outpatient chains offer shorter wait times and lower fees, supporting a 5.95% CAGR to 2031.

What supply chain issue most affects SPECT procedures?

Customs delays that slow Mo-99 generator imports can cut isotope activity below clinical thresholds.

Which companies lead equipment sales?

GE HealthCare, Siemens Healthineers, and Philips collectively top capital equipment bids.

Page last updated on: