Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.9 Billion |

| Market Size (2031) | USD 8.92 Billion |

| Growth Rate (2026 - 2031) | 8.64% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gas Generator Market Analysis by Mordor Intelligence

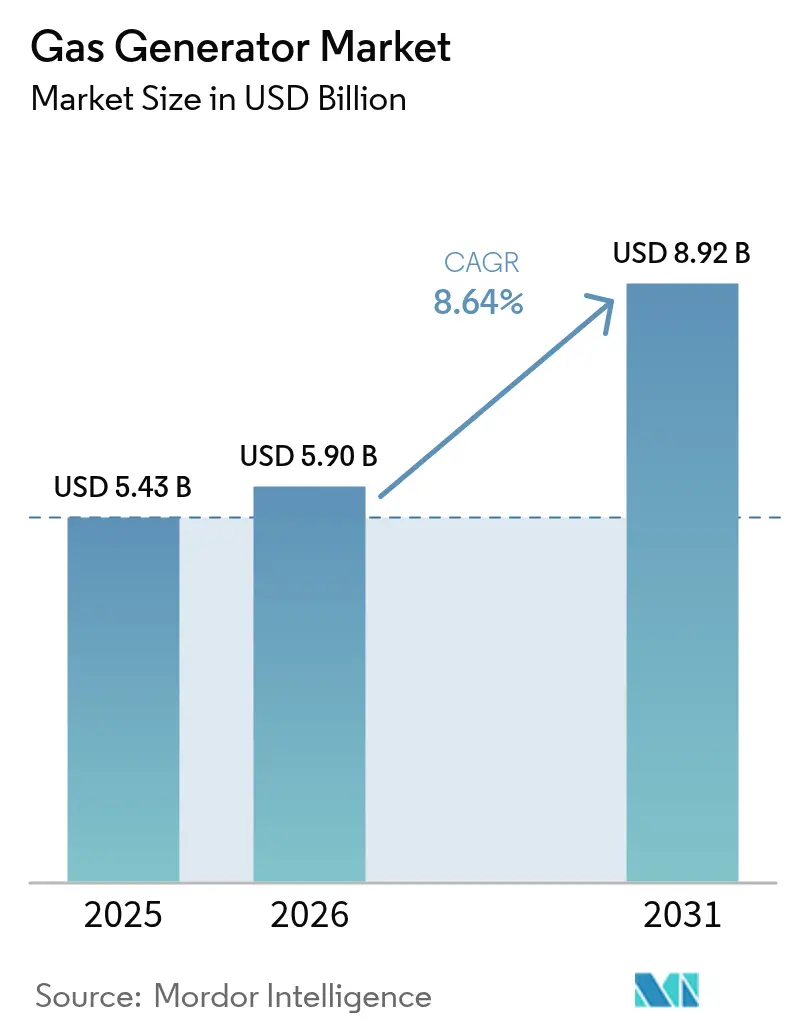

Gas Generator Market size in 2026 is estimated at USD 5.9 billion, growing from 2025 value of USD 5.43 billion with 2031 projections showing USD 8.92 billion, growing at 8.64% CAGR over 2026-2031.

Robust expansion relies on data-center buildouts, resilience investments for extreme-weather events, and widening pipeline access that anchor natural-gas sets in distributed power strategies. Buyers view gas machines as an efficient bridge technology because operating costs are 20-30% lower than those of diesel, coinciding with sharply lower NOx and CO₂ emissions.[1] Commercial facilities, industrial campuses, and residential neighborhoods, therefore, specify gaseous units to meet uptime and sustainability targets, while regulators tighten particulate and noise limits that restrict the deployment of diesel engines.[2] Service providers reinforce this demand by bundling remote monitoring, predictive maintenance, and fuel-flex options that future-proof capital outlays. Meanwhile, data-center developers turn to on-site natural-gas generation for both standby and peak-shaving roles, creating a high-growth outlet for the gas generator market and accelerating adoption across all kVA classes.

Key Report Takeaways

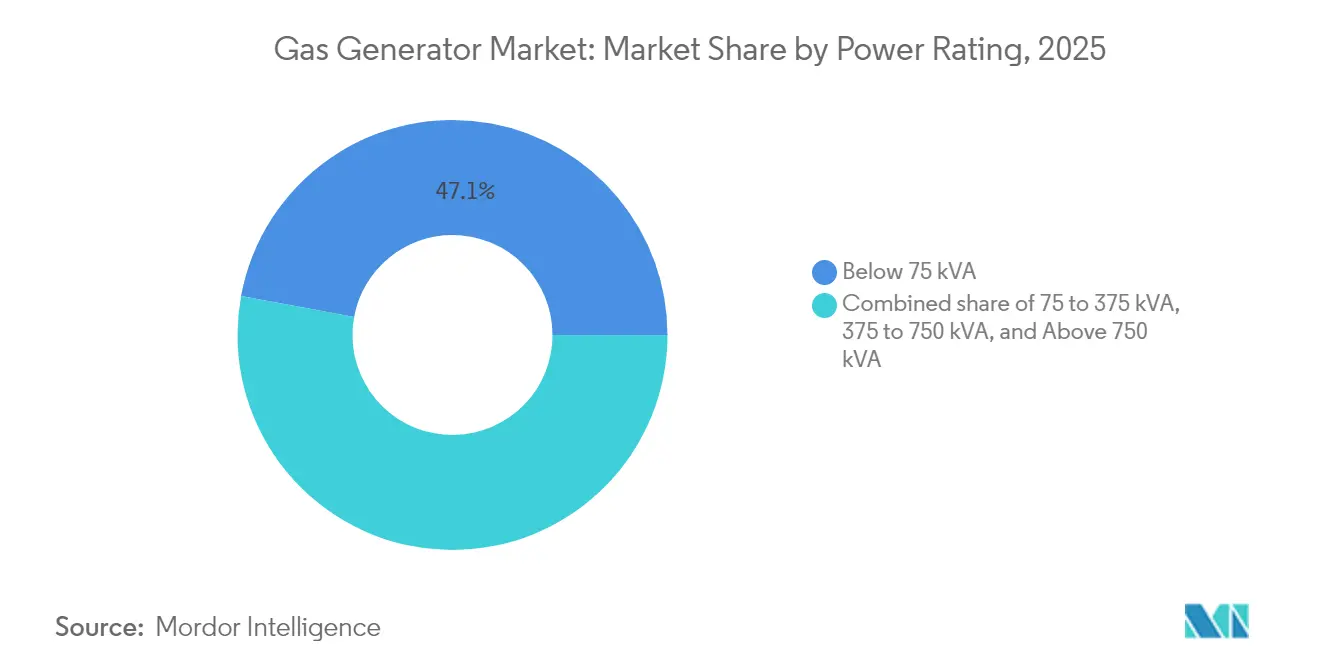

- By power rating, the below 75 kVA segment held 47.10% of the gas generator market share in 2025, and the 75–375 kVA class is projected to expand at a 9.62% CAGR through 2031.

- By application, standby power commanded 50.75% of the gas generator market size in 2025, while peak-shaving is advancing at a 10.19% CAGR through 2031.

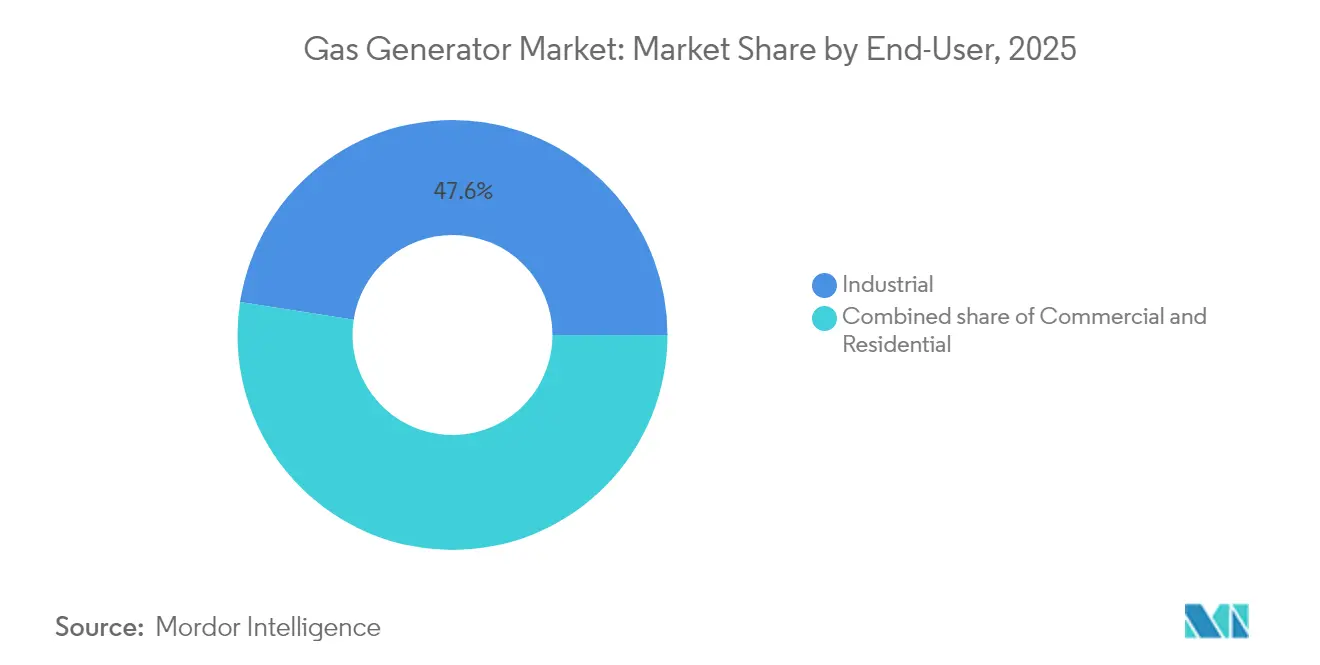

- By end-user, industrial facilities captured a 47.55% share of the gas generator market size in 2025 and are projected to grow at a 9.03% CAGR between 2026 and 2031.

- By geography, North America accounted for 35.05% of the revenue in 2025, whereas the Asia Pacific registered the fastest 9.31% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gas Generator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of natural-gas pipeline infrastructure | 1.8% | North America & APAC core, spill-over to Europe | Medium term (2-4 years) |

| Lower OPEX & emissions versus diesel gensets | 1.5% | Global | Short term (≤ 2 years) |

| Backup-power boom in data-centers & hospitals | 1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Extreme-weather events driving standby installations | 0.9% | North America, Europe, APAC coastal regions | Short term (≤ 2 years) |

| Growth of CHP-ready micro-gas generators | 0.7% | Europe & North America, emerging in APAC | Long term (≥ 4 years) |

| Diesel-genset phase-outs in air-quality non-attainment zones | 0.6% | California, European urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Natural-Gas Pipeline Infrastructure

Widening pipeline networks cuts delivered fuel costs and expands siting flexibility for the gas generator market. The United States alone added 17.8 Bcf/d of new capacity in 2024 through projects such as Mountain Valley Pipeline and Permian takeaway lines, reinforcing supply security for distributed assets. India mirrors this trend as city-gas distribution grids expand to underserved districts, supporting a 60% rise in national demand by 2030.[3]International Energy Agency analysts, “India’s Natural Gas Demand Set for 60 % Rise by 2030,” International Energy Agency, iea.org Consistent fuel availability, particularly for the 75–375 kVA class, benefits commercial and light-industrial loads, while also underpinning the economics of peak-shaving schemes that rely on predictable gas pricing. Continued investment—another 7.3 Bcf/d set to enter service from the Permian Basin—locks in a structural tailwind for the gas generator market across both mature and emerging economies.

Lower OPEX & Emissions Versus Diesel Gensets

Natural-gas units slash running costs by capitalizing on the global fuel-price gap and by minimizing oil changes, filter swaps, and after-treatment upkeep. Operators typically realize a 20-30% lower annual expenditure compared to comparable diesel sets, a saving that is amplified wherever carbon fees apply. California’s Tier 5 off-road rules illustrate the regulatory swing: tougher NOx ceilings push buyers toward gas models that comply without urea injection or particulate filters. The cost-emissions advantage therefore accelerates adoption in industrial parks, shopping malls, and municipal facilities—settings where life-cycle economics and environmental scorecards now matter as much as initial purchase price.

Backup-Power Boom in Data-Centers & Hospitals

Cloud hyperscalers and hospital systems demand 99.999% availability, pushing orders for more than 375 kVA higher. Goldman Sachs expects an additional 47 GW of U.S. data-center load by 2030, with natural gas accounting for 60% of that requirement. GE Vernova is already designing city-scale solutions that bundle multiple multi-megawatt gas blocks to meet AI-driven power density requirements. Hospitals follow suit after outage-related care disruptions, adopting dual-fuel engines that prioritize gas for lower emissions while retaining diesel for contingency. This mission-critical surge ensures sustained demand across the 375–750 kVA and over 750 kVA classes, stabilizing aftermarket service revenue streams for OEMs.

Extreme-Weather Events Driving Standby Installations

More intense hurricanes, heatwaves, and ice storms translate directly into higher residential and commercial generator sales. Hurricane Milton’s 2024 landfall lifted Generac’s share price by 8% as order volume spiked for <75 kVA sets. Texas supermarkets and fuel stations installed microgrids powered mainly by natural gas after grid failures underscored business-interruption risk.[4]California Air Resources Board staff, “Tier 5 Off-Road Engine Standards,” California Air Resources Board, arb.ca.gov Above-average Atlantic storm activity further disrupted Gulf Coast energy hubs, reinforcing the standby value proposition. Insurance carriers now factor backup generation into premium calculations, nudging property owners toward permanent solutions. The pattern reclassifies generators from optional amenities to essential infrastructure across coastlines and wildfire-prone regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sparse gas-grid access in remote areas | -1.2% | Rural regions globally, particularly developing markets | Long term (≥ 4 years) |

| Volatile natural-gas pricing | -0.8% | Global, with regional variations | Short term (≤ 2 years) |

| Competition from hydrogen & fuel-cell solutions | -0.6% | Europe & Japan leading, expanding globally | Long term (≥ 4 years) |

| Tightening urban noise & methane-slip rules | -0.4% | Urban centers in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sparse Gas-Grid Access in Remote Areas

Extending pipelines to low-density territories remains uneconomical, limiting gas generator penetration in areas where mines, farms, or islands rely on diesel or LPG. A comprehensive Energies review shows that remote microgrid planners still prefer transportable fuels because the capital expenditure for pipe extensions cannot be recouped at modest load factors. Arctic operations face reliability challenges that favor on-site fuel storage over reliance on pipelines.[5]International Energy Agency analysts, “India’s Natural Gas Demand Set for 60 % Rise by 2030,” International Energy Agency, iea.org Without virtual-pipeline or small-scale LNG logistics, adoption of below-75 kVA and 75–375 kVA stalls in these regions. Consequently, gas-set suppliers must pair offerings with LPG kits or hybrid PV-battery packages to stay relevant off-grid.

Volatile Natural-Gas Pricing

Henry Hub averaged USD 2.21/MMBtu in 2024 but could double to USD 4.00 by 2026, squeezing peak-shaving economics. European TTF prices linger near USD 11/MCF amid LNG competition and constrained Russian flows. Commodity swings complicate life-cycle cost calculations and can reopen the door for diesel or battery storage in price-sensitive sectors. Industrial buyers hedge exposure with fixed-price supply contracts, yet volatility still curbs uptake in emerging markets. Stabilizing policies or index-linked service packages will be vital to sustain long-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Rating: Mid-range sets accelerate while small units retain the lead

The <75 kVA class claimed 47.10% of the gas generator market share in 2025, confirming its dominance in homes and small businesses, where modest loads and quick installation are most important. In contrast, the 75–375 kVA band is projected to post a 9.62% CAGR, the fastest pace among all ratings, as commercial buildings and light-industrial plants enhance resilience after recent outage spikes. The gas generator market size for units above 375 kVA is expanding as data center and hospital projects specify multi-megawatt blocks; however, those tiers together still trail the entry and mid-range segments in total value.

Manufacturers strengthen the 75–375 kVA offering through modular frames that parallel easily and through digital controllers that support peak-shaving cycles. Remote monitoring reduces service visits, improving lifetime economics compared to diesel sets. Meanwhile, models below 75 kVA are gaining traction in new-home construction programs that pre-wire for permanent backup, such as Generac’s partnership with Texas builders. Across all ratings, fuel-flexible designs that can accept future hydrogen blends help protect asset life as decarbonization targets become tighter.

By Application: Peak-shaving rises even as standby power stays dominant

Standby duty held 50.75% of the gas generator market size in 2025, reflecting the fundamental need for uninterrupted electricity in safety-critical uses. Healthcare campuses, telecom hubs, and municipal facilities continue to view on-site gas units as the surest hedge against grid failures. Peak-shaving records a 10.19% CAGR to 2031 as demand-charge tariffs rise and utilities reward fast-response capacity that alleviates network stress.

Growth in peak shaving stems from commercial customers that run generators for a few hours each month to flatten their load profiles and from industrial sites that dispatch units during price spikes. Modern engines tolerate frequent start-stop cycles and integrate with building-energy management systems, allowing one asset to switch between standby, peak-shave, and limited prime roles. Prime or continuous duty remains a niche for off-grid mines, construction camps, and remote oil and gas pads where pipeline access exists but the bulk grid does not.

By End-User: Industrial plants anchor volume while homes show the quickest lift

Industrial facilities captured 47.55% of 2025 revenue, the highest share among end users, and are projected to expand at a healthy 9.03% CAGR as process electrification advances. Fertilizer, refining, and chemicals operations in India and the United States utilize gas sets for both backup and combined heat and power, leveraging fuel availability and waste heat recovery to reduce overall energy costs. Commercial buildings follow, installing mid-range ratings that balance space constraints with the rising need for power quality.

Residential demand grows the fastest due to heightened awareness of outage risk and the spread of neighborhood gas mains. Builder programs fold small generators into mortgage packages, easing upfront cost barriers. Remote diagnostics and subscription maintenance make ownership simpler, encouraging adoption beyond traditional storm-prone states. Together, these patterns confirm that every customer tier now views gas technology as a flexible tool for enhancing reliability, controlling costs, and reducing carbon footprints.

Geography Analysis

North America accounted for 35.05% of the gas generator market share in 2025, driven by the world’s largest pipeline grid and a policy shift away from diesel engines. The United States alone placed 17.8 Bcf per day of new pipe in service during 2024, ensuring ample fuel for behind-the-meter assets across the Gulf Coast and Appalachia. Data-center clusters in Virginia and Texas utilize multi-megawatt gas blocks that serve both standby and peak-shaving roles, while supermarkets and municipal pumps employ 150 kVA to 300 kVA frames for storm resilience. California regulations that phase out diesel gensets in non-attainment counties further channel spending toward cleaner spark-ignition models, cementing regional leadership.

The Asia Pacific is projected to post the fastest 9.31% CAGR through 2031, as pipeline build-out, LNG imports, and industrial modernization converge. India’s natural-gas demand is set to climb 60% by 2030, and city-gas distribution schemes now reach secondary towns, unlocking a broad base for <375 kVA equipment. In China, factory automation drives tighter power-quality specs that favor on-site gas generation, while provincial incentive programs reimburse up to 20% of capital cost for high-efficiency CHP units. Japan and South Korea pair pilot hydrogen-ready engines, yet natural gas remains the primary fuel for backup and grid-support duties until the costs of reen hydrogen call.

Europe maintains gradual expansion despite high TTF prices that squeeze fuel-cost advantages. Energy-security policies in Germany and the Netherlands are driving combined heat and power retrofits, while silent enclosures that meet 65 dB(A) city limits open up opportunities in densely populated urban districts. Hybrid systems that combine gas engines with battery storage enable facilities to pass stringent grid-interconnection tests, sustaining demand in both the 75–375 kVA and 375–750 kVA ranges. South America and the Middle East & Africa register accelerating orders as new cross-border pipelines and LNG terminals unlock supply, though sparse rural grids still cap penetration in remote provinces.

Regulatory Landscape

Regulation increasingly differentiates gas generators by duty cycle, installation type, and safety certification, tightening the compliance pathway for both stationary and portable units. In January 2026, the US Environmental Protection Agency finalized amendments to 40 CFR Part 60 Subpart KKKKa for stationary combustion turbines, with applicability tied to units constructed, modified, or reconstructed after December 13, 2024. It also introduced a subcategory for stationary temporary combustion turbines with a BSER requirement of 25 ppm NOx when firing natural gas.

For smaller and portable equipment, product safety and fuel-connection requirements are getting more prescriptive at the standard level. ANSI/PGMA G300-2023 for portable generators reached its mandatory compliance effective date in January 2026, adding clearer requirements for natural gas and LPG models, including markings and installation-related provisions, which increases the emphasis on certified designs and documented conformance for OEMs and channel partners.

Competitive Landscape

Established vendors shape a moderately concentrated field by combining engine manufacture, electronics, and digital service into unified offerings that span every kVA class. Generac deepened vertical control with the April 2025 purchase of MOTORTECH, gaining ignition, mixer, and knock-detection subsystems that raise efficiency across the 75–375 kVA tier. Caterpillar invests in its Active Management Platform, enabling fleet-wide dispatch and predictive maintenance that enhances peak shaving and prime applications for commercial and industrial users. Deutz broadened its scope from engines to full generator sets through the June 2024 acquisition of Blue Star Power Systems, positioning for growth in U.S. municipal and telecom projects.[6]Deutz Communications, “Deutz Acquires Blue Star Power Systems,” RER Magazine, rermag.com

Fuel flexibility becomes a core differentiator as Cummins launches HELM™ platforms that share blocks yet accept natural gas today and hydrogen blends tomorrow, protecting customer capital during the energy transition. Mitsubishi Heavy Industries leads hydrogen-engine pilots, targeting a 500 kW package for release in fiscal 2026 that will serve data-center and industrial loads while maintaining compatibility with natural gas. HD Hyundai Infracore secured state backing to develop 500 kWe hydrogen generators, intensifying future competitive pressure on legacy gas sets.

Digital support services reinforce stickiness. Caterpillar and Generac offer cloud dashboards that track run hours, fuel flow, and emissions, thereby reducing downtime and revealing potential upsell paths for analytics subscriptions. Smaller disruptors focus on micro-CHP units that hit 35.2% AC electrical efficiency and operate on natural gas, biogas, or hydrogen, appealing to European apartment blocks and U.S. universities. Collectively, players that integrate remote monitoring, fuel agility, and hybrid-system readiness are best positioned to capture the next wave of demand in the gas generator market.

Gas Generator Industry Leaders

-

Generac Holdings Inc.

-

Caterpillar Inc.

-

General Electric Company

-

Cummins Inc.

-

Kohler Co.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Data-center and grid-resilience buildouts continue to create whitespace for larger-frame gas generators and packaged, fast-deployable power blocks that can support both standby and limited dispatch roles. In 2026, multiple US utility and cooperative actions reinforced the near-term addressable base for gas-fired capacity additions and related balance-of-plant demand: Duke Energy received approval from the Public Service Commission of South Carolina for a 1,365 MW natural gas combined-cycle facility in Anderson County (March 2026), and the South Carolina Public Service Commission also approved a 2,180 MW project proposed by Dominion Energy South Carolina and Santee Cooper (June 2026). These programs translate into procurement pull-through for prime movers, controls, and ancillary systems, where gas-generator OEMs and packagers can bundle microgrid controls, remote monitoring, and service contracts aligned to uptime requirements.

Fuel-flex and low-carbon readiness are also influencing product roadmaps and tender specifications. GE Vernova and IHI reported a full-scale F-class gas turbine test achieving 100% ammonia combustion (March 2026), and Japan's NEDO highlighted a pathway toward commercial deployment of 2 MW-class ammonia mono-fuel gas turbine technology for industrial cogeneration following completion of development in fiscal 2025. For gas generator suppliers, this supports investment in retrofit kits, controls calibration, and enclosure and safety-system designs that reduce conversion time for end users managing tightening local emissions and decarbonization constraints while maintaining firm power capability.

Recent Industry Developments

- July 2026: Rolls-Royce Solutions opened a USD 24 million logistics and assembly expansion in Mankato, Minnesota, adding about 250,000 square feet and targeting a doubling of production capacity for mtu Series 4000 generator sets. The added footprint increases throughput for high-power backup applications and helps shorten lead times for large, mission-critical projects.

- June 2026: Generac announced a global supply agreement with a leading hyperscale data center operator to provide backup power generators. The deal signals a shift toward multi-site, standardized procurement by hyperscalers, favoring suppliers that can deliver scale, service coverage, and consistent product configurations across regions.

- June 2024: DEUTZ completed its acquisition of Blue Star Power Systems, expanding from engines into full generator-set offerings for the United States. The combination broadened DEUTZ's access to municipal, telecom, and industrial standby channels and strengthened its ability to package and service gas-driven genset solutions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The gas generator market, for this methodology, covers revenue from gas-fueled generator sets sold for standby, prime or continuous, and peak shaving power needs, across residential, commercial, and industrial users, and across major regions.

Scope exclusions: We exclude diesel and gasoline gensets, as well as upstream natural gas production equipment that does not generate electricity.

Segmentation Overview

-

By Power Rating

- Below 75 kVA

- 75 to 375 kVA

- 375 to 750 kVA

- Above 750 kVA

-

By Application

- Standby

- Peak Shaving

- Prime/Continuous

-

By End-User

- Industrial

- Commercial

- Residential

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- NORDIC Countries

- Russia

- Rest of Europe

-

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clean demand and supply picture for gas generator sets by region and common power ratings. We used public sources such as the U.S. Energy Information Administration for gas use and power trends, the International Energy Agency for electricity reliability and generation mix context, and the World Bank for macro indicators that shape commercial and industrial load growth.

To keep the model grounded, we also reviewed sources such as UN Comtrade trade statistics for generator-related flows, government energy and environment agencies for emissions and permitting direction, and association and standards bodies for typical rating and compliance references. We then combined those inputs with company filings, investor presentations, product catalogs, and trusted press coverage to understand pricing movement and product mix changes. Select paid subscriptions were used only to speed up company financials screening, patent scanning, and shipment or trade look-ups where public series were incomplete. The specific examples above are not exhaustive, and many other public sources were checked as part of data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm what portion of demand comes from standby versus prime use, how buyers choose kVA ranges, and how pricing changes with gas type and installation needs. We spoke with manufacturers, distributors, rental and service channel stakeholders, EPC and installer stakeholders, and large end users so assumptions could be corrected when desk indicators were too broad. For a global market, inputs were balanced across APAC, EMEA, and the Americas to reduce regional bias in adoption and replacement cycles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 16% | APAC: 45% |

| Mid tier: 56% | Functional/Unit leaders: 38% | EMEA: 35% |

| Smaller Players: 19% | Managers: 46% | Americas: 20% |

Market-Sizing & Forecasting

Sizing was built using a top-down model where regional electricity demand growth, outage sensitivity in key end users, and gas availability indicators were used to reconstruct the likely generator demand pool, which is then split by application and kVA bands. To keep the totals realistic, the outputs were cross-checked with selective bottom-up approximations using sampled price by kVA range, channel checks on unit movement, and supplier roll-ups where coverage was strong enough.

A few inputs that mattered in the model were the share of installations that are standby versus prime or continuous, kVA mix shifts toward mid-range sets, replacement cycles tied to operating hours and maintenance practices, the pace of new commercial and industrial project additions, and regional emissions rules that influence switching from diesel to gas. Where bottom-up data was missing for smaller countries, gaps were handled through proxy ratios from comparable markets and then adjusted after primary feedback.

For forecasting, scenario analysis was used so adoption could be stressed under different assumptions for grid reliability, fuel price spreads, and project activity. The final growth path was selected only after it matched what interviewees saw for lead times, utilization, and typical pricing behavior across regions.

Data Validation & Update Cycle

Validation was done by comparing the modeled totals against independent signals, such as trade movement direction, installed base replacement logic, and whether the implied price per kVA stayed within realistic bands. When a region or application showed a sudden jump, the driver was traced back to its input series and then re-tested with alternative assumptions before sign-off.

Before release, the work goes through multi-step internal checks where another analyst reviews the math, the inputs, and the story so any variance is explained in plain terms. If large discrepancies appear versus fresh public updates or what primary contacts are seeing, follow-ups are triggered and the model is corrected. Reports are refreshed annually, and interim updates are made when there is a material market event. Right before delivery, a final pass is done so clients receive the most current view.

Mordor Intelligence's Gas Generator Market Sizing Compared With Other Published Estimates

Published market sizes for gas generators can vary even when they look like they are describing the same product, because scope choices and timing choices differ. The biggest drivers tend to be whether rental and service revenues are counted, whether portable units are mixed with stationary sets, and how the analyst treats currency conversion and base-year price levels.

The main gap comes from whether the estimate is strictly for gas generator sets by kVA and application, or whether it also adds adjacent revenues like long-term service contracts and broader generator categories. In Mordor Intelligence, the total is kept to equipment revenues aligned to standby, peak shaving, and prime use across defined kVA bands, with pricing and regional mix validated through interviews before the final number is locked.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.90 B (2026) | |

| Industry Publisher A | USD 6.41 B (2024) | Uses an earlier base year and a broader gas-type framing, and the power capacity buckets are stated in kW which can shift how mid and large units are mapped into the total. |

| Market Publisher B | USD 5.80 B (2025) | Mixes portable and stationary categories more explicitly and appears to use a different starting year and price level, which can move the implied average selling price versus an application-led kVA model. |

Across the three figures, the spread is explained more by scope and year choice than by any single demand driver. When the definition is kept tight around gas-fueled generator set equipment and the kVA and application mix is checked with market participants, the resulting total becomes easier to replicate and easier to track over time.

Key Questions Answered in the Report

What CAGR does the global gas generator market expect between 2026 and 2031?

The market is forecast to advance at an 8.64% CAGR, growing from USD 5.9 billion in 2026 to USD 8.92 billion by 2031.

Which power-rating segment grows fastest through 2031?

Units rated 75–375 kVA show the quickest 9.62% CAGR as commercial and light-industrial sites expand backup and peak-shaving capacity.

Why are natural-gas generators replacing diesel units?

Operators gain 20-30% lower operating costs and easier compliance with stricter NOx standards, especially in California and Europe.

Why are companies replacing diesel with gas generators?

Operators gain 20-30% lower operating costs and easier compliance with strict NOx rules, especially in California and European cities.

Which region leads overall revenue today?

North America holds about 35.05% of 2025 revenue thanks to its extensive pipeline network and emissions policies that discourage diesel.

Where is demand expanding the most rapidly?

Asia Pacific posts the highest 9.31% CAGR, driven by India’s pipeline build-out and China’s industrial modernization.

How are vendors preparing for hydrogen adoption?

Leading manufacturers launch engines that run on natural gas now yet can accept hydrogen blends or 100% hydrogen in future upgrades.

Page last updated on: