Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 8.78 Billion |

| Market Size (2031) | USD 10.81 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

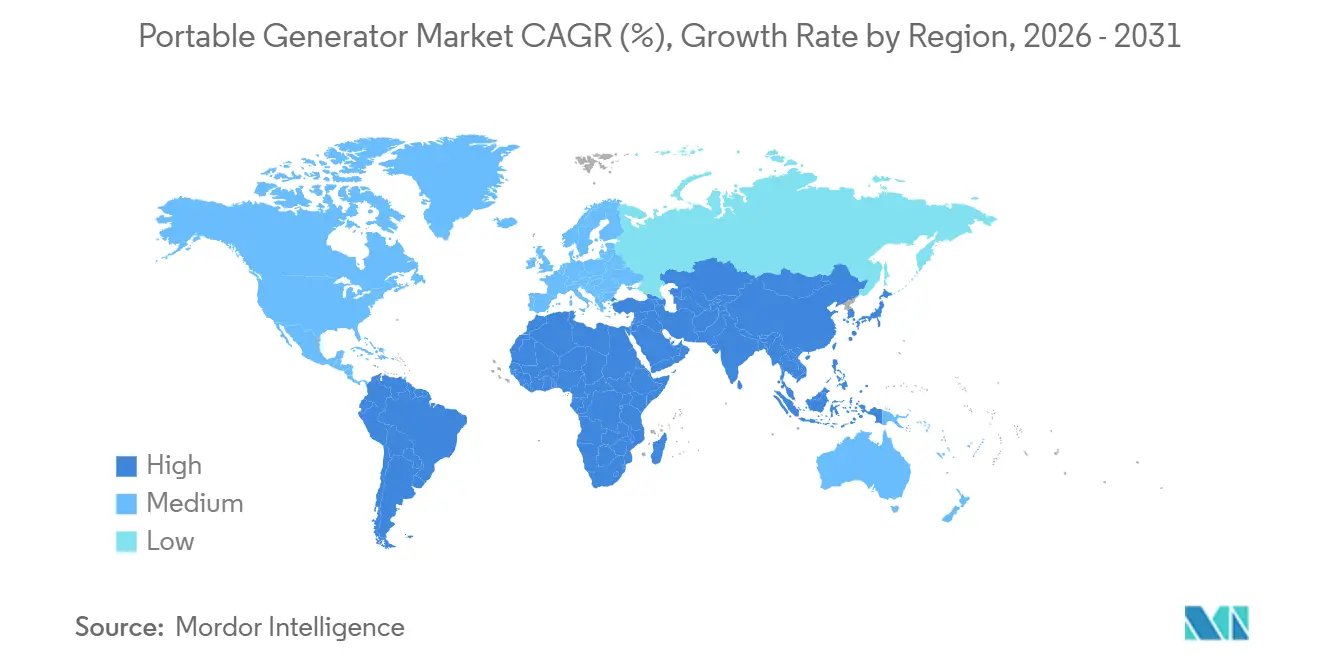

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Portable Generator Market Analysis by Mordor Intelligence

The Portable Generator Market size is expected to increase from USD 8.38 billion in 2025 to USD 8.78 billion in 2026 and reach USD 10.81 billion by 2031, growing at a CAGR of 4.23% over 2026-2031.

Growth stems from rising outage frequency, infrastructure spending across emerging economies, and the recreational-vehicle boom, yet the segment under 2 kW is ceding ground to lithium power stations and tightening small-engine emission rules. Manufacturers are therefore fast-tracking inverter and hybrid-solar designs, while residential buyers in North America pair generators with rooftop PV and battery storage to hedge utility-rate volatility.[1]U.S. Department of Energy, “2025 Residential Energy Storage Market Report,” energy.gov Asia-Pacific leads demand at 38.6% of 2025 revenue and will remain the fastest-growing region on the back of ASEAN construction pipelines and rural telecom densification in China.[2]Asian Development Bank, “Asian Development Outlook 2025,” adb.org North America retains the second-largest share as hurricane-exposed states embed backup-power attestations into mortgage underwriting and home-office workers prioritize power quality.

Key Report Takeaways

- By fuel type, gasoline units held 44.5% of portable generator market share in 2025, but solar-integrated models are advancing at a 9.7% CAGR to 2031.

- By power rating, the 5–10 kW band captured 47.9% of 2025 sales; in contrast, sub-5 kW models are rising at a 6.1% CAGR on urban-dweller demand.

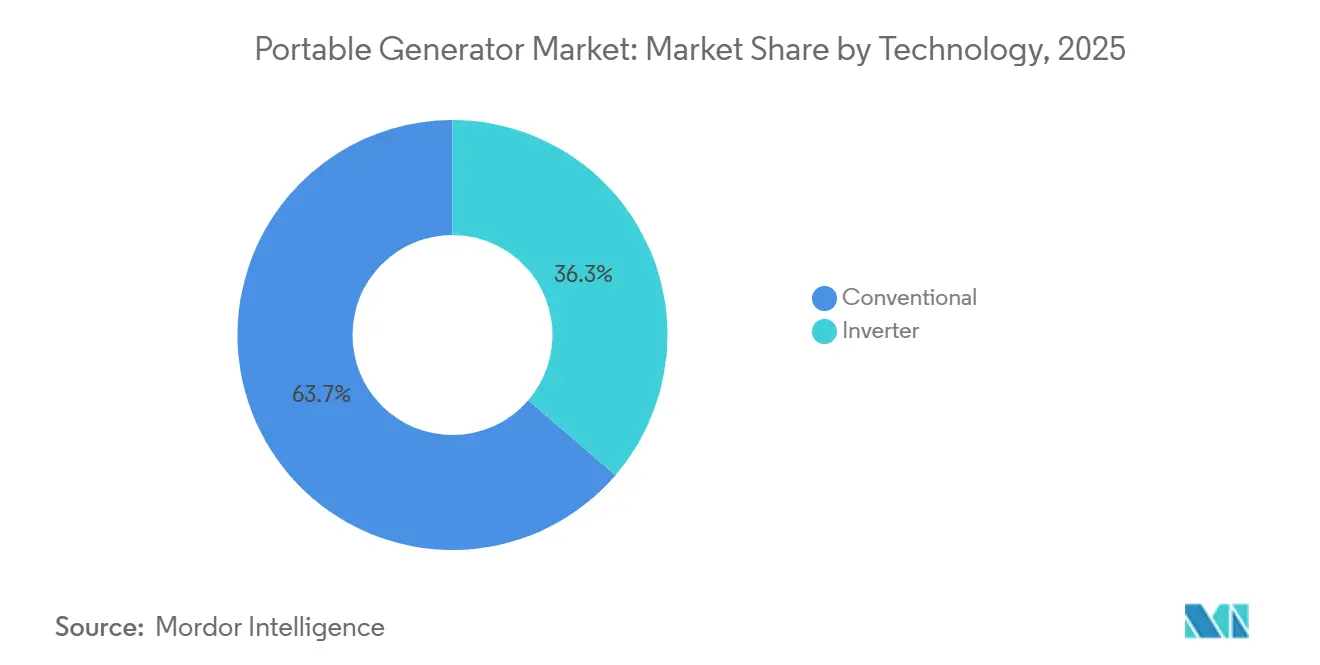

- By technology, conventional open-frame designs controlled 63.7% of 2025 revenue, while inverter technology is growing at a 5.3% CAGR through 2031.

- By application, emergency and standby use accounted for 70.2% of 2025 demand; recreational deployments are expanding at 8.8% CAGR to 2031.

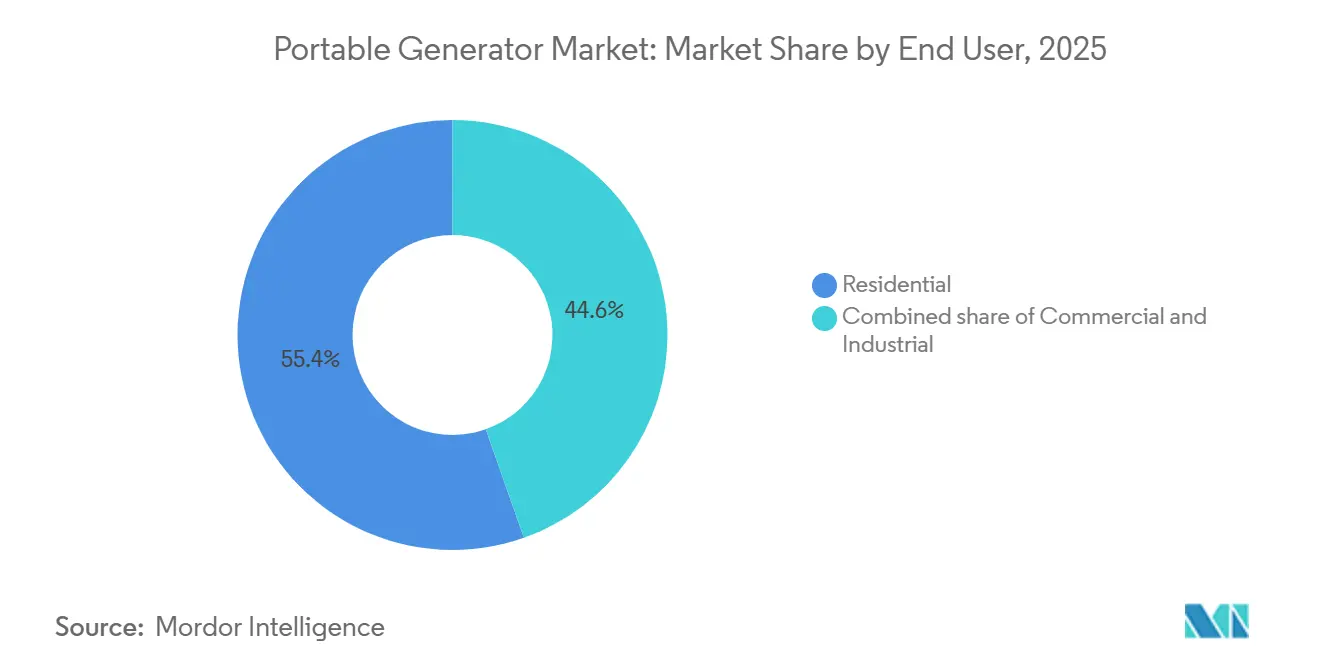

- By end user, residential buyers represented 55.4% of 2025 revenue, yet commercial demand is growing at a 5.6% CAGR on construction-site electrification and event-noise ordinances.

- By geography, Asia-Pacific commanded 38.6% of 2025 revenue and is set to advance at a 4.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Portable Generator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid outages & instability | +1.2% | North America, India, Brazil, South Africa | Medium term (2-4 years) |

| Residential backup-power growth | +1.0% | North America, Europe, Australia | Short term (≤ 2 years) |

| Emerging-economy construction boom | +0.8% | Asia-Pacific, Middle East, South America | Long term (≥ 4 years) |

| RV & outdoor-leisure surge | +0.6% | North America, Europe, Oceania | Short term (≤ 2 years) |

| Edge micro-data-center rollout | +0.3% | Global | Medium term (2-4 years) |

| Hybrid solar-diesel at telecom towers | +0.4% | Asia-Pacific, Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Frequency of Power Outages & Grid Instability

Climate-driven storms, drought-strained hydropower, and utility de-energization events are lengthening outage hours, elevating the value of on-site generation. U.S. households endured 8.2 outage hours in 2024, up 27% from 2019, while Texas and California accounted for 40% of national downtime.[3]U.S. Energy Information Administration, “Electric Power Monthly,” eia.gov India recorded 6.8 billion customer-hours of load-shedding during fiscal 2024-2025, with Uttar Pradesh, Bihar, and Jharkhand hardest hit. Brazil’s outage duration rose to 14.3 hours in 2024 amid record heat and drought-hit dams. South Africa imposed stage-4 and stage-5 load-shedding on 118 days in 2024, driving 2.1 GW of incremental standby capacity, 35% of which involved portable units. Alongside steep insurance deductibles for spoiled inventory and frozen pipes, these trends are broadening the portable generator market beyond traditional hurricane-prone zones.

Rapid Growth in Residential Backup-Power Demand

Mortgage lenders now require backup-power attestations in FEMA flood and wildfire zones, embedding generator costs into closing fees.[4]Federal Housing Finance Agency, “Guidance on Resilience Assets,” fhfa.gov Remote work intensifies outage pain points: 28% of U.S. employees work from home at least three days weekly and cite power reliability as a top-three relocation factor. Germany’s KfW financed EUR 87 million (USD 95 million) of home generator and battery upgrades for rural households in 2024. Australia’s Clean Energy Regulator found that 18% of 2024 rooftop-solar installs included a generator-ready hybrid inverter. Collectively, subsidies, insurance incentives, and telework economics lift attach rates above historical norms.

Expanding Construction Activities in Emerging Economies

Developing Asia plans USD 1.7 trillion of 2026 infrastructure outlays, with portable power filling grid-access gaps that stretch 6–18 months. India let 12,400 km of highway contracts and 1.2 million affordable-housing units during fiscal 2024-2025, mandating portable generators during monsoon instability. Saudi Arabia channeled USD 32 billion into NEOM and Red Sea construction in 2024, requiring Tier 4/Stage V compliant units at remote sites. The UAE’s Expo City and Masdar City expansions raised construction employment 9.2% in 2024, driving inverter-generator fleets on noise limits. ASEAN nations floated USD 89 billion in PPP tenders, all specifying temporary power for bridge, tunnel, and rural-electrification projects.

Recreational Vehicle & Outdoor Leisure Boom

U.S. RV shipments hit 487,000 units in 2024, and 68% of new trailers include generator-ready wiring. Camping participation reached 58.7 million households, with dispersed camping up 19% year-on-year. Europe logged 243,000 new motorhome registrations, 54% fitted with solar-battery packages still requiring a backup generator for air-conditioning. Australia and New Zealand counted 2.1 million caravan registrations, with 34% of domestic travelers choosing self-contained camping in 2024. Manufacturers respond with sub-3 kW inverter models under 20 kg and below 58 dBA to address overlapping urban-balcony and RV use cases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Small-engine emission regulations | -0.7% | U.S., EU, China | Short term (≤ 2 years) |

| Residential battery-storage adoption | -0.5% | North America, Europe, Australia, Asia-Pacific cities | Medium term (2-4 years) |

| Urban noise curfews | -0.3% | Global metro areas | Short term (≤ 2 years) |

| Lithium power stations cannibalizing <2 kW sales | -0.6% | North America, Europe, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Emission Regulations on Small Engines

The U.S. EPA’s Tier 4 rules for sub-19 kW spark-ignition engines took effect in January 2025, forcing three-way catalysts and closed-loop fueling that add USD 80–120 per unit. EU Stage V raises particulate-number limits, driving diesel particulate filters and SCR on portable diesels. China’s National IV standards mandate EFI and onboard diagnostics from July 2025. Japan now requires Tier-4-equivalent engines in all public-sector procurements. Compliance costs squeeze entry pricing and accelerate the shift toward inverter and hybrid-solar architectures.

Adoption of Residential Battery-Storage Systems

U.S. residential battery capacity passed 1.2 GWh in 2025; Tesla, Enphase, and LG Chem offer 10–20 kWh packs that keep essentials running overnight without fuel. California’s SGIP issued USD 287 million in 2024 rebates covering a quarter of battery install costs. Germany financed 47,300 battery loans in 2024 and now sees storage on 34% of new rooftop PV systems. Australia recorded 89,000 residential batteries in 2024 as feed-in tariffs fell. Batteries undercut generators on noise and emissions but falter in multi-day outages or high-inrush loads, sustaining opportunities for hybrid configurations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Solar-Integrated Models Disrupt Gasoline Incumbency

Gasoline units retained 44.5% portable generator market share in 2025, benefiting from widespread fuel availability and USD 400–1,200 pricing, yet solar-integrated hybrids are growing 9.7% CAGR on off-grid telecom and RV demand. Diesel models face weight and cost penalties from Stage V after-treatment, losing ground outside heavy-duty sites. Dual-fuel gasoline-propane designs win rural U.S. buyers who prize 18-month propane shelf life and lower carbon intensity.

Hybrid solar-battery-generator systems slash diesel use by up to 80% at African tower sites, trimming annual fuel logistics by USD 3,200 per node. Power-station brands such as Jackery and EcoFlow shipped 890,000 solar-ready units in 2024, combining foldable PV with 1–3 kWh batteries. Levelized energy costs drop below USD 0.30/kWh in high-insolation zones, a 40% edge over diesel-only setups.

By Power Rating: Compact Units Gain as Urban Density Rises

The 5–10 kW class represented 47.9% of the portable generator market size in 2025, addressing whole-home backup and food-truck power, yet sub-5 kW units are advancing 6.1% CAGR on apartment and tailgating use cases. Units above 10 kW remain industrial staples but face rental-fleet substitution.

Urban decibel caps, such as Los Angeles’ 60 dBA at 7 m, disqualify most open-frame models, pushing consumers toward compact inverters under 58 dBA. Tokyo and Singapore impose similar nighttime limits, spurring OEM acoustic enclosures. A 7 kW inverter weighing 55 kg meets 80% of single-family loads without permanent transfer switches, balancing portability with capacity.

By Technology: Inverter Adoption Driven by Sensitive Electronics

Conventional sets still held 63.7% of portable generator market revenue in 2025, thanks to price, yet inverter shipments are pacing a 5.3% CAGR on electronics protection needs. Inverters deliver sub-3% THD and ±2% voltage regulation, cutting fuel use 20–30% at partial loads.

The work-from-home cohort, 28% of U.S. employees, demands clean power for routers and monitors. FDA logged 1,847 medical device incidents in 2024 tied to poor power quality, steering home-care suppliers toward inverter bundles. Semiconductor cost declines are shrinking the inverter price premium to a projected 40% by 2031.

By Application: Recreational Segment Outpaces Emergency Standby

Emergency and standby accounted for 70.2% of 2025 revenue, yet recreational deployments are rising 8.8% CAGR to 2031 on RV and camping growth. Continuous-duty industrial use remains diesel-centric, but hybrids are nibbling share where fuel logistics are costly.

Europe’s motorhome registrations climbed to 243,000 in 2024, and 54% of buyers still include a generator despite solar-battery packages. In the United States, dispersed camping jumped 19%, underscoring lifestyle-driven generator demand.

By End User: Commercial Buyers Accelerate on Compliance Pressure

Residential users commanded 55.4% of 2025 sales, driven by mortgage and insurance mandates, while commercial demand is advancing 5.6% CAGR on construction electrification and event noise ordinances. Industrial miners and farmers keep diesel sets above 10 kW for continuous duty, but are piloting solar hybrids in fuel-fragile regions.

U.S. nonresidential construction outlays reached USD 1.08 trillion in 2024, with 78% of projects budgeting portable power. In the U.K., outdoor venues replaced half their gensets with inverters to meet 65 dBA festival limits, citing 3- to 5-year paybacks from lower fuel and sound-barrier rental costs.

Geography Analysis

Asia-Pacific controlled 38.6% of 2025 revenue, and the portable generator market size in the region will grow at a 4.9% CAGR through 2031 on infrastructure and rural-telecom build-outs. India logged 6.8 billion outage-hours, spurring residential and SME purchases, while China deployed 87,000 rural 5G base stations, 41% powered by solar-diesel hybrids. ASEAN PPP pipelines worth USD 89 billion specify portable units for bridge and tunnel works.

North America ranks second, anchored by the United States’ 142 million single-family homes. Outage hours rose to 8.2 in 2024, elevating attach rates, while Canada’s northern mines rely on hybrid gensets to offset USD 2.50-per-liter air-lifted diesel. Mexico’s near-shoring wave pushes construction demand, with 68% of industrial-park tenders in 2024 requiring temporary generators.

Europe’s growth hinges on emission-compliant inverters and hybrids amid high diesel costs. Germany’s rural-resilience loans covered 14,300 households in 2024, while Storm Arwen-style blackouts prompted U.K. compensation reforms that favor onsite backup. France warns of winter peak constraints, driving industrial standby installs, whereas Nordic markets see modest recreational growth tied to camper-van adoption.

Competitive Landscape

The top five players, Generac, Honda, Caterpillar, Cummins, and Kohler, held roughly 45% of 2025 revenue, indicating moderate concentration. Generac shipped 1.2 million portables and captured 34% of U.S. residential sales through cellular-connected monitoring that trims service calls by 18%. Honda commands 28% of the global inverter segment, leveraging 3-year warranties and a 140-country dealer network. Caterpillar and Cummins focus on hybridizing diesel sets with lithium buffers for telecom towers and mining camps.

Disruptors such as Jackery, EcoFlow, and Anker exploit lithium-iron-phosphate chemistries to slash operating costs for intermittent users. EcoFlow’s Delta Pro offers 3.6 kWh at 3.6 kW output for USD 3,699, sidestepping fuel and maintenance. Yamaha and Kohler now field hybrid engine-battery architectures that provide silent battery-only operation for light loads, reflecting convergence across combustion and storage tech. Patent activity centers on variable-speed controls and load-management software, with Kohler securing US11831194B2 for a controller that trims fuel 22% across duty cycles.

Portable Generator Industry Leaders

-

Generac Holdings Inc.

-

Honda Motor Co. Ltd.

-

Briggs & Stratton LLC

-

Caterpillar Inc.

-

Cummins Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Goal Zero introduced the Yeti 1500 portable solar generator, equipped with a 1,505 Wh lithium iron phosphate (LFP) battery, 2,000 W continuous output, and rapid AC/solar charging capabilities. This product is designed for emergency backup power and off-grid recreational applications.

- November 2025: Bobcat Company, a global leader in equipment innovation and worksite solutions, has unveiled the PG1140 portable generator. This new offering boasts improved output, streamlined logistics, and sophisticated load management, all packed into one portable power solution.

- August 2025: Generac has unveiled a new line of diesel generators tailored for the Indian market, promising reliable and efficient power for residential, commercial, and industrial uses.

- April 2025: At the Middle East Energy Exhibition, Kirloskar Oil Engines Limited unveiled the Optiprime Dual Core 1000 kVA generator, claiming it as the world's smallest. Tailored for industrial and commercial applications, this generator not only boasts compact efficiency and high performance but also emphasizes environmental sustainability.

Global Portable Generator Market Report Scope

A portable generator is a small, self-contained unit designed to provide electrical power in locations without access to a traditional power grid. It is commonly used during power outages or in areas where electricity is not readily available, such as on a construction site or in a rural area.

The portable generator market is segmented by fuel type, power rating, technology, application, end user, and geography. By fuel type, the market is segmented into gasoline, diesel, dual-fuel, LPG/propane, and solar-integrated. By power rating, the market is segmented into below 5 kW, 5 to 10 kW, and above 10 kW. By technology, the market is segmented into conventional and inverter. By application, the market is segmented into emergency/stand-by, prime/continuous, and recreational/outdoor. By end user, the market is segmented into residential, commercial, and industrial. The report also covers the market sizes and forecasts for the portable generator market across major regions. Market sizing and forecasts are provided for each segment based on value (USD).

By Fuel Type

| Gasoline |

| Diesel |

| Dual-Fuel (Gasoline-Propane) |

| LPG/Propane |

| Solar-Integrated |

By Power Rating

| Below 5 kW |

| 5 to 10 kW |

| Above 10 kW |

By Technology

| Conventional |

| Inverter |

By Application

| Emergency/Stand-by |

| Prime/Continuous |

| Recreational/Outdoor |

By End User

| Residential |

| Commercial |

| Industrial |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Fuel Type | Gasoline | |

| Diesel | ||

| Dual-Fuel (Gasoline-Propane) | ||

| LPG/Propane | ||

| Solar-Integrated | ||

| By Power Rating | Below 5 kW | |

| 5 to 10 kW | ||

| Above 10 kW | ||

| By Technology | Conventional | |

| Inverter | ||

| By Application | Emergency/Stand-by | |

| Prime/Continuous | ||

| Recreational/Outdoor | ||

| By End User | Residential | |

| Commercial | ||

| Industrial | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What was the portable generator market size in 2026?

The market was valued at USD 8.78 billion in 2026.

How fast will the portable generator market grow through 2031?

Revenue is projected to rise at a 4.23% CAGR, reaching USD 10.81 billion by 2031.

Which region leads portable generator demand?

Asia-Pacific generated 38.6% of 2025 revenue and is set to grow the fastest at a 4.9% CAGR.

Which power rating segment sells the most units?

Sets in the 5-10 kW band led with 47.9% of 2025 sales, serving whole-home and small-commercial loads.

Are inverter generators overtaking conventional models?

Inverters are growing at 5.3% CAGR thanks to low total harmonic distortion and fuel savings, although conventional units still hold a 63.7% revenue share.

How are emission rules affecting product design?

U.S. Tier 4, EU Stage V, and China National IV standards add catalyst and after-treatment costs, accelerating the shift toward inverter and hybrid solar-battery architectures that avoid small-engine penalties.

Page last updated on: