Industrial Generator Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

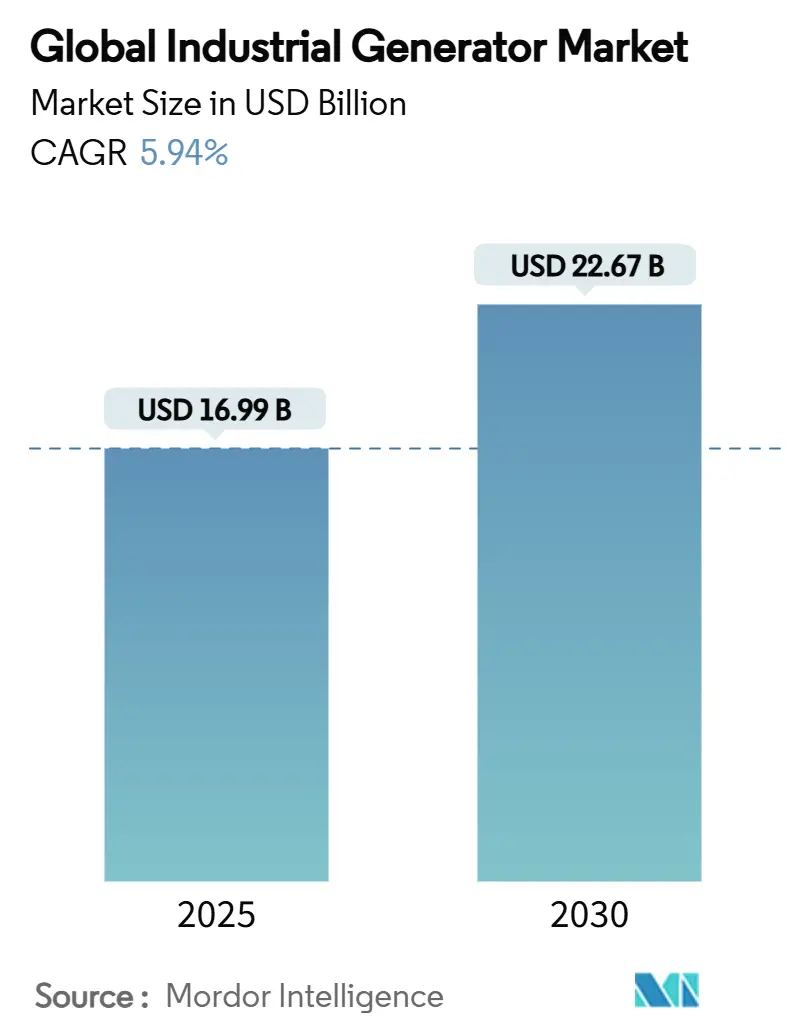

| Market Size (2025) | USD 16.99 Billion |

| Market Size (2030) | USD 22.67 Billion |

| Growth Rate (2025 - 2030) | 5.94% CAGR |

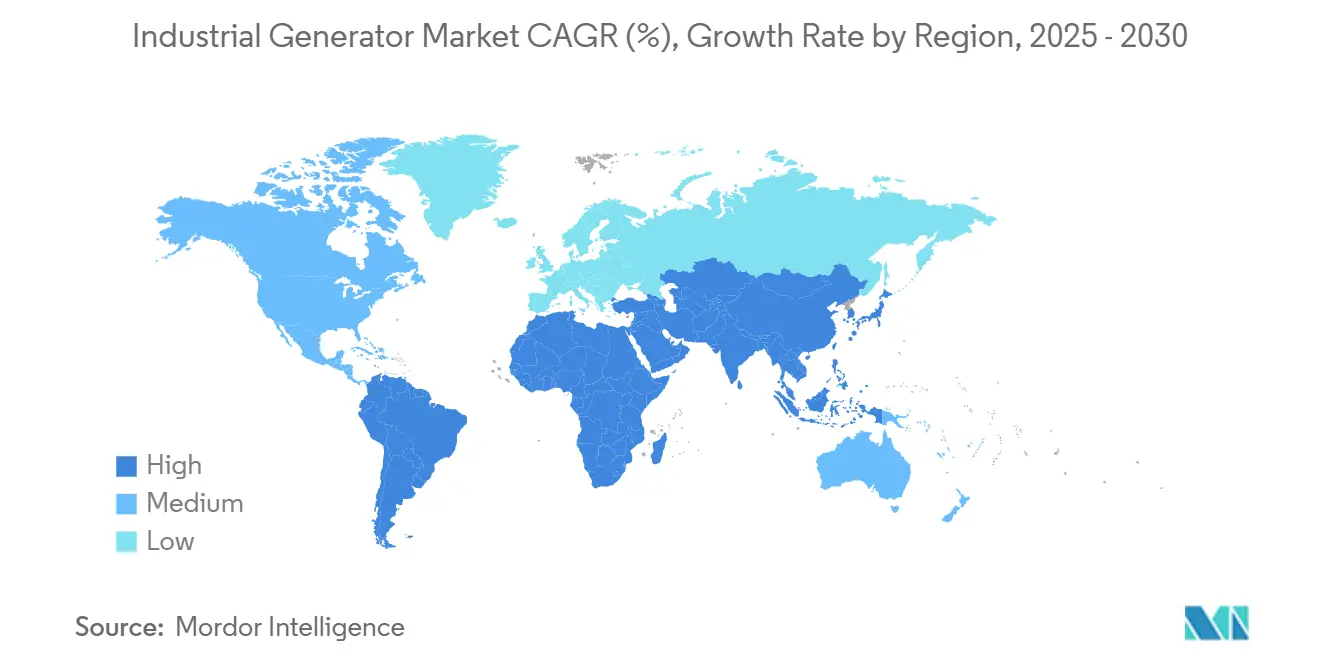

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Generator Market Analysis by Mordor Intelligence

The Global Industrial Generator Market size is estimated at USD 16.99 billion in 2025, and is expected to reach USD 22.67 billion by 2030, at a CAGR of 5.94% during the forecast period (2025-2030).

Extreme-weather outages, surging data-center construction, and cyber-resilience mandates are accelerating demand, while hybrid and hydrogen-ready technologies are reshaping product roadmaps. Diesel units retain a commanding presence, yet dual-fuel and hybrid sets are scaling rapidly as operators seek emission compliance and fuel flexibility. Mid-range power ratings between 75 kVA and 750 kVA anchor mainstream purchases, but machines with power ratings above 2,000 kVA are gaining traction in hyperscale facilities. Regionally, the Asia-Pacific leads current shipments and posts the fastest growth, driven by unprecedented digital infrastructure spending and a manufacturing resurgence.

Key Report Takeaways

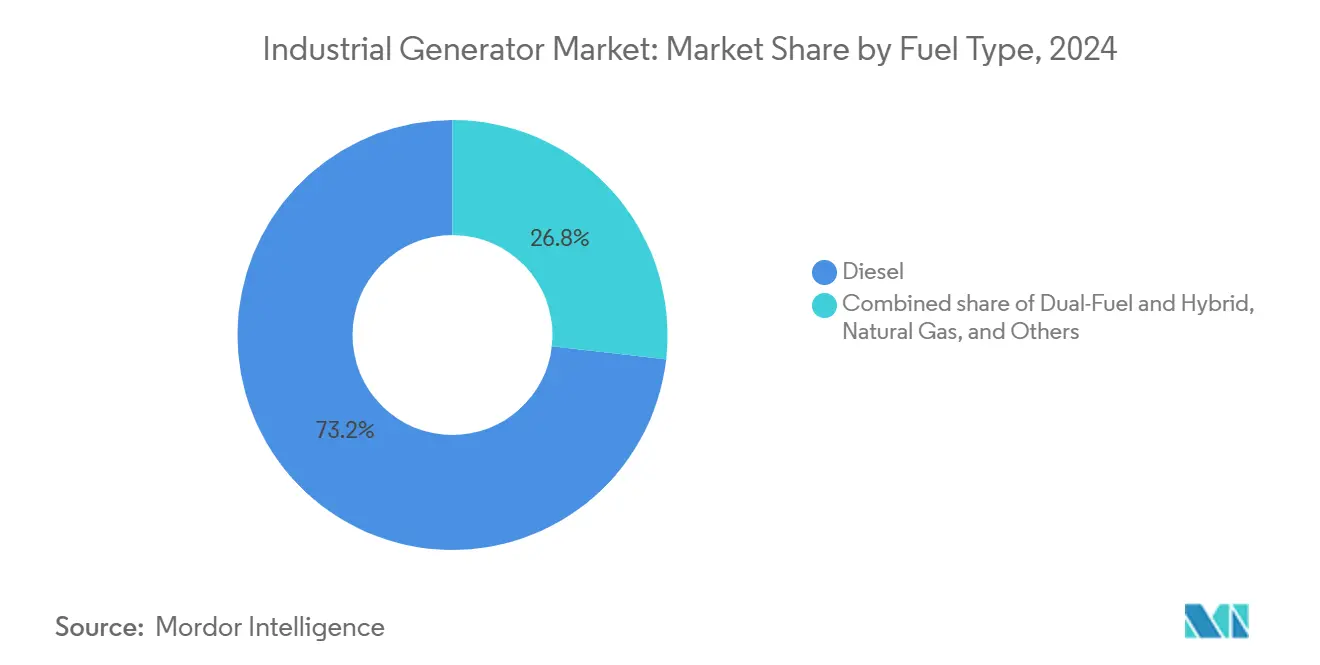

- By fuel type, diesel held a 73.2% market share in the industrial generator sector in 2024; dual-fuel and hybrid systems are projected to show the highest CAGR of 10.8% through 2030.

- By power rating, the 75–750 kVA segment commanded a 46.9% share of the industrial generator market size in 2024, while sets above 2,000 kVA are expanding at an 8.5% CAGR.

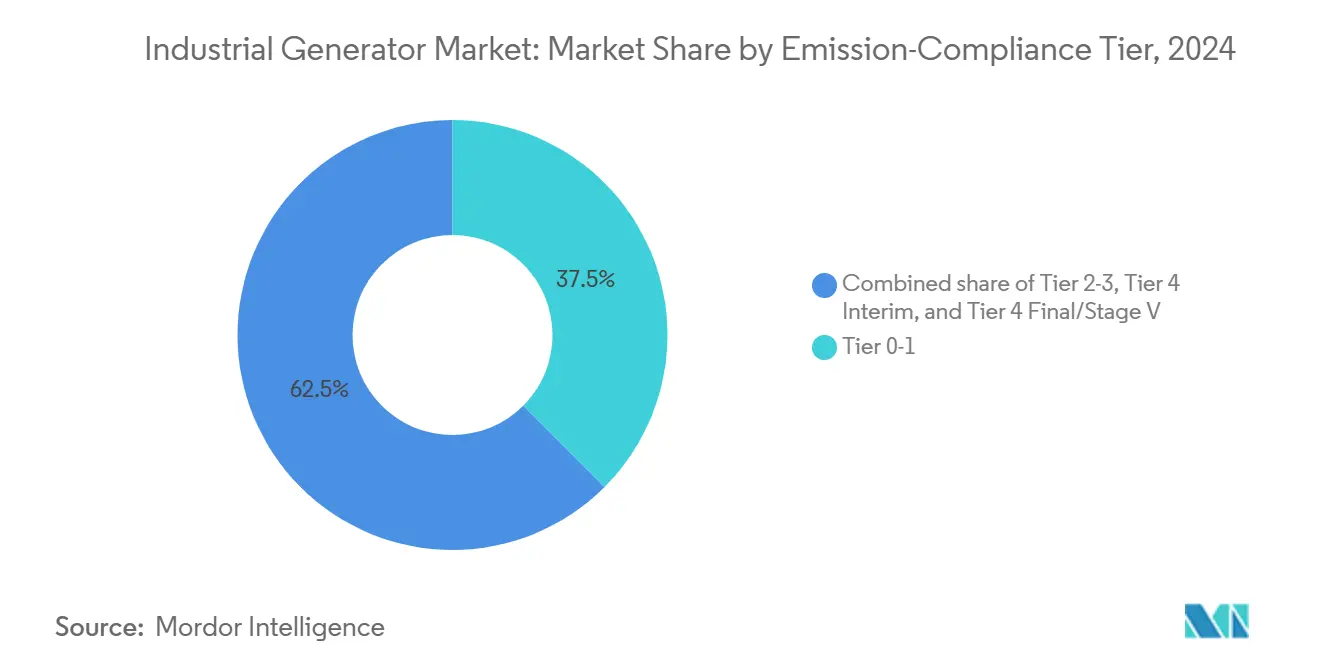

- By emission-compliance tier, tier 0-1 accounted for 37.5% of the industrial generator market size in 2024, whereas tier 4 final/stage V is expanding at a 7.2% CAGR.

- By application, standby power accounted for 55.1% of the industrial generator market size in 2024; the microgrid and hybrid support segment is projected to advance at an 8.9% CAGR.

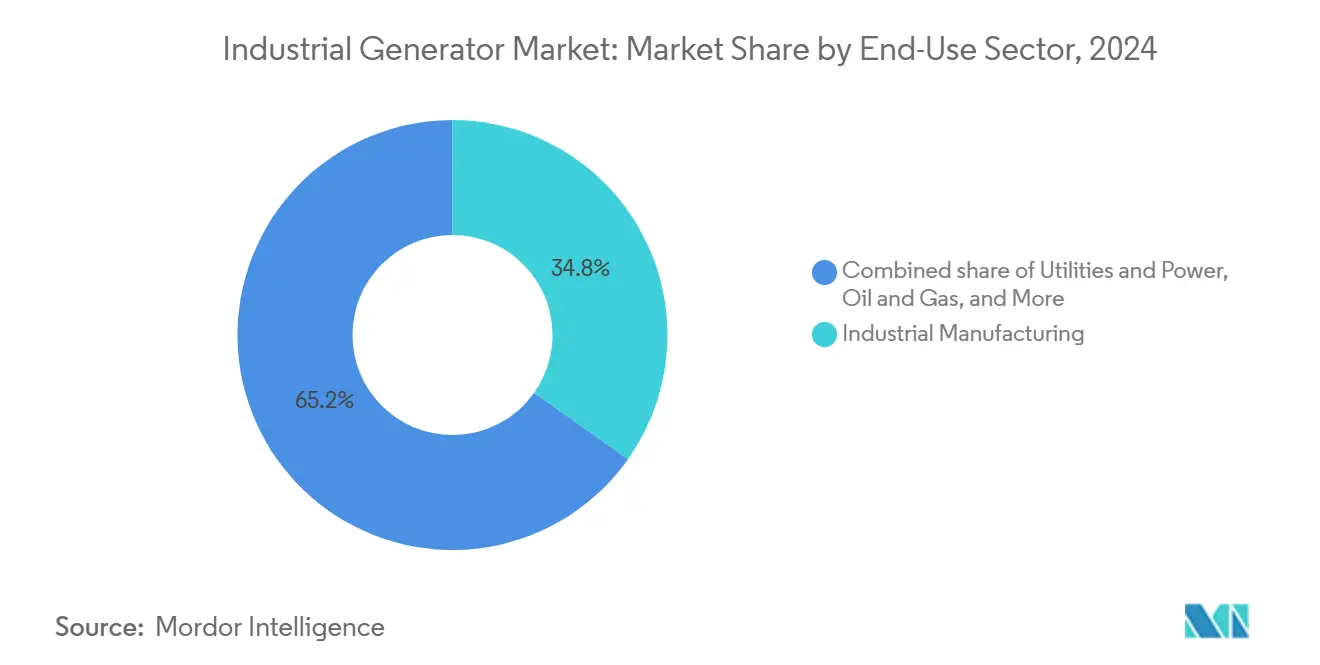

- By end-user sector, the industrial manufacturing segment captured 34.8% of the industrial generator market size in 2024, while the utilities and power segment is projected to grow at an 8% CAGR.

- By geography, the Asia-Pacific region led with a 40% industrial generator market share in 2024 and is expected to log a 7% CAGR through 2030.

Global Industrial Generator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extreme-weather–driven outage frequency | +1.8% | Global, with acute impact in North America and Asia-Pacific | Short term (≤ 2 years) |

| Data-center capacity boom | +1.5% | Global, concentrated in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Remote mining microgrid rollout | +0.9% | APAC, MEA, and South America | Long term (≥ 4 years) |

| Hydrogen-ready retrofit interest | +0.7% | Europe and North America, spill-over to APAC | Long term (≥ 4 years) |

| Cyber-resilience mandates for critical infra | +0.6% | North America and Europe | Medium term (2-4 years) |

| Emerging-market gas-pipeline build-out incentives | +0.4% | MEA and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extreme-Weather–Driven Outage Frequency

Weather-related blackouts more than doubled from 2014 to 2023; 2024 alone saw 1.2 billion hours of lost power in the United States.[1]“Extreme Weather Leads to 1.2 Billion Power Outage Hours,” CNBC.com Hurricanes and wildfires are stressing grids, prompting factories, refineries, and logistics hubs to specify larger standby sets with faster synchronization to microgrids. Texas microgrid projects now range between USD 2 million and USD 5 million per megawatt, underscoring the economic premium on resilience. Manufacturers are embedding advanced paralleling controls, allowing gensets to island seamlessly during disturbances. The persistent gap between grid reliability and industrial uptime needs is anchoring baseline demand for the industrial generator market.

Data-Center Capacity Boom

Global data-center power demand is rising at a 16% CAGR, forecast to reach roughly 130 GW by 2028. Hyperscalers now dictate generator specifications that emphasize rapid load acceptance and lower emissions. Caterpillar’s USD 725 million Indiana expansion will boost the U.S. supply of large, natural-gas sets purpose-built for AI workloads. Operators are increasingly favoring gas over diesel for improved sustainability and long-term cost, nudging the industrial generator market toward dual-fuel and hydrogen-ready designs. The Asia-Pacific region is expected to double its data-center capacity within five years, adding more than 2 GW annually and accelerating regional uptake.

Remote Mining Microgrid Rollout

Hybrid microgrids at Australian, African, and Andean mines blend solar, wind, and battery assets with diesel or gas backup to secure 24/7 power. Mount Isa’s 88 MW solar-diesel system demonstrates how generators continue to be indispensable for maintaining grid-forming stability despite increasing renewable energy penetration. Vendors are integrating AI-driven controllers to modulate genset output in tandem with variable renewable energy sources, thereby reducing fuel consumption without compromising reliability. The magnitude of critical minerals projects across APAC and MEA positions remote microgrids as a long-tail growth engine for the industrial generator market through 2030 and beyond.

Hydrogen-Ready Retrofit Interest

Wärtsilä’s 100% hydrogen-ready engine plant, set to open for orders in 2025, signals a pivotal technological shift.[2]Wärtsilä Corporation, “100% Hydrogen-Ready Engine Announcement,” Wartsila.com Caterpillar and Rolls-Royce are similarly advancing hydrogen-hybrid platforms under DOE-funded programs. Early adopters view retrofit kits as a hedge against looming carbon-pricing schemes. The IEA projects that hydrogen use in power generation will rise from 17 Mt in 2030 to 51 Mt by 2050, thereby enlarging the serviceable upgrade pool for existing fleets.[3]U.S. Energy Information Administration, “2024 Hurricane Season Disruptions,” EIA.gov

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Tier-5/Stage-V diesel emission rules | -0.8% | Global, with stringent enforcement in Europe and North America | Short term (≤ 2 years) |

| Fuel-price volatility (diesel & gas) | -0.6% | Global | Short term (≤ 2 years) |

| Solar-plus-storage cost decline | -0.9% | Global, accelerated adoption in APAC and North America | Medium term (2-4 years) |

| Urban demand-response programs cutting genset need | -0.4% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Tier-5/Stage-V Diesel Emission Rules

Tier 4 Final mandates up to 99% particulate reduction, forcing OEMs to bolt on diesel particulate filters and selective catalytic reduction modules. The EPA’s 2027 heavy-duty rule expands in-use compliance horizons, raising cost and complexity. Rolls-Royce’s approval of Hydrotreated Vegetable Oil for mtu engines reduces lifecycle CO₂ emissions by 90% without requiring hardware changes, offering operators a compliance workaround. These regulations accelerate migration toward gas and hybrid technologies, but can delay immediate purchasing as buyers weigh technology bets.

Fuel-Price Volatility

Spot diesel rose as much as 28 % in 2024 during refinery outages, while U.S. Henry Hub gas swung between USD 1.6 and USD 3.8 per MMBtu. Budget unpredictability complicates operating-cost projections, nudging facilities toward dual-fuel sets able to arbitrage real-time fuel spreads. Rental fleets bear the brunt, frequently repricing contracts to cover fuel surcharges. High volatility can postpone replacement cycles, tempering near-term growth in the industrial generator industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Diesel Dominance Faces Hybrid Challenge

Diesel sets generated 73.2% of 2024 shipments, underscoring ingrained fuel logistics and reliability advantages. However, dual-fuel and hybrid machines are forecast to grow at a 10.8% CAGR, benefiting from falling natural-gas prices and hydrogen-ready retrofits. Natural-gas models appeal to data centers seeking lower total cost of ownership and smoother air-quality permitting. The other categories—biofuel, LPG, and hydrogen—remain niche but post double-digit growth as OEMs, such as Mitsubishi Heavy Industries, finalize 500 kW hydrogen prototypes.

Operators prize dual-fuel sets for fuel-switch flexibility during price spikes. Compressed natural gas at USD 2.99 /GGE undercuts gasoline parity, while liquefied natural gas at USD 4.86 /DGE edges diesel parity in many regions. This price spread, paired with emission benefits, amplifies hybrid adoption. Consequently, the industrial generator market is rebalancing its fuel mix toward cleaner combustion paths without sacrificing reliability.

By Power Rating: Mid-Range Leadership, Large-Scale Acceleration

The 75–750 kVA class held 46.9% share in 2024, forming the backbone of small-to-mid industrial and commercial facilities. Growth continues as emerging economies urbanize and digitize. Above 2,000 kVA units, although accounting for just 7% of the volume, are tracking an 8.5% CAGR in hyperscale data-center demand. Rolls-Royce’s latest MTU Series 1600 lifts output to 996 kW, reinforcing a trend toward denser power envelopes.

Large-frame sets now feature grid-tie inverters and black-start capabilities, enabling participation in utility capacity markets. As hyperscalers chase 99.999% uptime, specification sheets increasingly call for N+2 redundancy, which multiplies the unit counts per site. This swell in top-end demand boosts the overall industrial generator market size and stimulates vertical investment across engine blocks, alternators, and digital controls.

By Emission-Compliance Tier: Legacy Systems Persist, Clean Technology Advances

Tier 0-1 machines still account for 37.5% of the global inventory, predominantly in emerging markets that lack strict regulations. Conversely, Tier 4 Final/Stage V sets are expected to log a 7.2% CAGR through 2030 as Europe and North America tighten emission permits.[4]California Air Resources Board, “Tier 4 Engine Inventory,” Carb.ca.gov Caterpillar’s active-regeneration platform mitigates load-bank costs, easing the leap to fully compliant models.

Regions with intermediate standards gravitate toward Tier 2-3 or Tier 4 Interim units, reflecting cost–compliance trade-offs. Sustainability pledges from multinationals are nonetheless accelerating the pivot to top-tier engines. As a result, the industrial generator market is bifurcating between low-cost, legacy imports and premium, clean-tech systems, a dynamic that is likely to persist until regulatory harmonization closes the gap.

By Application: Standby Power Dominance, Microgrid Innovation

Standby duty accounted for 55.1% of shipments in 2024, primarily driven by hospitals, semiconductor fabs, and financial trading floors. Yet, microgrid and hybrid support are advancing at an 8.9% CAGR as campuses seek autonomy from fragile grids. Duisburg port’s climate-neutral terminal, powered by mtu Series 4000 hydrogen engines, exemplifies the new grid-forming role generators play within renewable clusters.

Peak-shaving deployments utilize AI-driven forecasting to dispatch gensets during tariff spikes, thereby trimming operational costs while reducing emissions hours. Rental fleets serve construction booms and disaster relief, keeping a baseline churn in emerging regions. Collectively, these diverse duty cycles fortify volume resilience for the industrial generator market across economic cycles.

By End-Use Sector: Manufacturing Foundation, Utilities Expansion

Industrial manufacturing captured 34.8% of 2024 demand, reflecting high sensitivity to outages that jeopardize throughput. Utilities and the wider power sector, however, are expected to headline future growth at an 8% CAGR as grid operators procure fast-start gas sets for capacity and frequency regulation. American Municipal Power’s 20 MW behind-the-meter deal in Michigan signals utility appetite for distributed assets.

Oil and gas, mining, and construction remain rugged use cases, valuing durability over emissions. Healthcare and telecom applications maintain strict uptime SLAs, favoring premium compliant models. Sectoral diversification shields the industrial generator industry from downturns in a single sector, underpinning steady aggregate growth.

Geography Analysis

Asia-Pacific commanded 40% industrial generator market share in 2024 and is on track for a 7% CAGR thanks to USD 27 billion invested in Indian data centers and China’s manufacturing rebound. Hyperscalers are adding 2 GW of capacity annually across the region, and relaxed emissions rules in select countries keep diesel cost-competitive. Japan and South Korea drive demand for ultra-clean gas sets, while ASEAN infrastructure projects sustain mid-range diesel volumes. Policy momentum favoring hydrogen in Australia and Singapore suggests early niches for H₂-ready machines, broadening the technological mix.

North America ranks second, bolstered by 1.2 billion outage hours in 2024 and over 80 GW of data-center capacity needed by 2030. Texas epitomizes resilience investment with microgrid construction costs of USD 2 million–USD 5 million per MW. Stringent Tier 4 rules are pivoting sales toward gas and hybrid units, as evidenced by Caterpillar’s Indiana expansion. Canada’s deregulated markets foster merchant-plant opportunities, with MTU gas gensets entering peak-demand service in Alberta.

Europe emphasizes Stage V compliance and renewable energy integration, maintaining a steady yet selective procurement profile. Germany, France, and the Nordics channel incentives into hydrogen pilot projects, driving early adoption of fuel-flexible engines. The Middle East and Africa are leveraging gas pipeline expansions to replace diesel imports, while new mining concessions in Zambia and Saudi Arabia support the development of hybrid microgrids. South America’s copper and lithium operations require high-horsepower sets at altitude; Chile and Peru increasingly pair them with solar-storage hybrids for fuel savings. Collectively, geographical diversification secures multi-regional growth lanes for the industrial generator market.

Competitive Landscape

The industrial generator market remains moderately fragmented with incumbents leaning on scale, vertical integration, and R&D intensity. Caterpillar, Cummins, Rolls-Royce Power Systems, Generac, and Wärtsilä headline global revenue. Generac has acquired Pramac, MOTORTECH, and Captiva Energy Solutions to plug geographic and control-system gaps. Kohler Energy’s spinout to Rehlko under Platinum Equity signals private-equity interest in recurring aftermarket revenue.

Technology differentiation pivots on hydrogen readiness, alternative fuels, and digital remote monitoring. Wärtsilä’s 100% H₂-ready plant secures first-mover status, while Rolls-Royce invests USD 75 million in Aiken to ramp up mtu Series 4000 engines for data centers. Partnerships with cloud providers feed predictive-maintenance analytics, slashing downtime and parts waste. Mid-tier Asian OEMs focus on price-competitive diesel exports but increasingly license EU aftertreatment to access regulated markets.

Aggressive capex by hyperscalers compresses lead times, pushing vendors toward localized manufacturing and just-in-time alternator supply. Service contracts account for more than 35% of top-line revenue at leading firms, cushioning cyclical swings in new units. Overall, consolidation pressures persist; yet, regional specialists retain niches in rental, marine, and defense applications, thereby sustaining competitive diversity.

Industrial Generator Industry Leaders

Caterpillar

Cummins

Generac

Rolls-Royce (MTU)

Kohler

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Rolls-Royce introduced upgraded MTU Series 1600 sets up to 996 kW, compatible with HVO for 90% CO₂ cuts.

- November 2024: GE Vernova unveiled the LM6000VELOX 100% hydrogen-fueled turbine for South Australia’s Whyalla plant.

- August 2024: HD Hyundai Infracore won a USD 1 billion Korean project to develop 500 kW hydrogen generators.

- May 2024: Mitsubishi Heavy Industries completed the evaluation of a 500 kW green-hydrogen generator. Engineers successfully operated a 6-cylinder hydrogen engine, equipped with advanced safety features, on 100% hydrogen fuel, ensuring stability across all phases.

Global Industrial Generator Market Report Scope

| Diesel |

| Natural Gas |

| Dual-Fuel and Hybrid |

| Others (Renewable/Bio-fuel, LPG, Hydrogen-ready, etc.) |

| Below 75 kVA |

| 75 to 750 kVA |

| 750 to 2,000 kVA |

| Above 2,000 kVA |

| Tier 0-1 |

| Tier 2-3 |

| Tier 4 Interim |

| Tier 4 Final/Stage V |

| Standby Power |

| Prime/Continuous Power |

| Peak-Shaving |

| Rental/Temporary Power |

| Micro-grid and Hybrid Support |

| Industrial Manufacturing |

| Oil and Gas |

| Mining and Construction |

| Utilities and Power |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Fuel Type | Diesel | |

| Natural Gas | ||

| Dual-Fuel and Hybrid | ||

| Others (Renewable/Bio-fuel, LPG, Hydrogen-ready, etc.) | ||

| By Power Rating | Below 75 kVA | |

| 75 to 750 kVA | ||

| 750 to 2,000 kVA | ||

| Above 2,000 kVA | ||

| By Emission-Compliance Tier | Tier 0-1 | |

| Tier 2-3 | ||

| Tier 4 Interim | ||

| Tier 4 Final/Stage V | ||

| By Application | Standby Power | |

| Prime/Continuous Power | ||

| Peak-Shaving | ||

| Rental/Temporary Power | ||

| Micro-grid and Hybrid Support | ||

| By End-Use Sector | Industrial Manufacturing | |

| Oil and Gas | ||

| Mining and Construction | ||

| Utilities and Power | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the industrial generator market?

The industrial generator market size is USD 16.99 billion in 2025.

How fast is demand for industrial generators growing?

Industry revenue is forecast to increase at a 5.94% CAGR between 2025 and 2030.

Which region leads global purchases of industrial generators?

Asia-Pacific holds 40% of 2024 shipments and maintains the fastest regional growth at 7% CAGR.

Why are data centers influencing generator specifications?

Hyperscalers require high-capacity, fast-responding, lower-emission sets, pushing adoption of gas and hydrogen-ready engines.

How do emission rules affect generator choices?

Tier 4 Final and Stage V regulations drive buyers toward advanced aftertreatment or alternative-fuel models to remain compliant.

Are hydrogen-ready generators commercially available yet?

Yes, Wärtsilä opened orders for a 100% hydrogen-ready engine plant in 2025, with deliveries slated for 2026.

Page last updated on: