Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

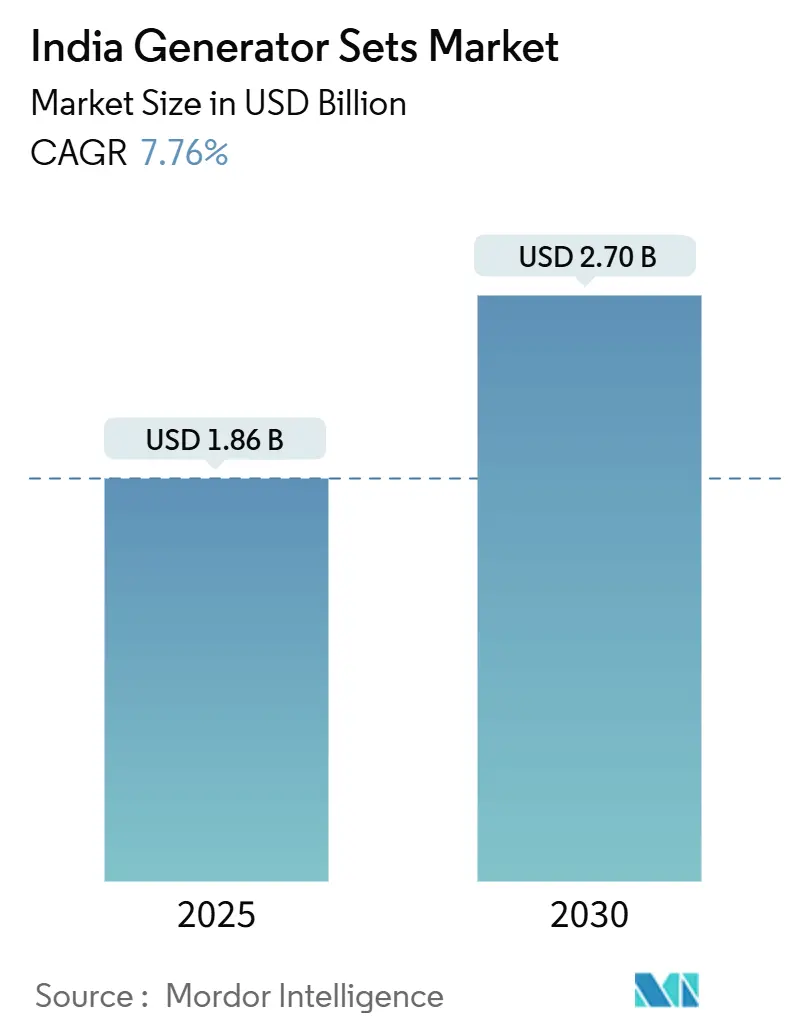

| Market Size (2025) | USD 1.86 Billion |

| Market Size (2030) | USD 2.70 Billion |

| Growth Rate (2025 - 2030) | 7.76% CAGR |

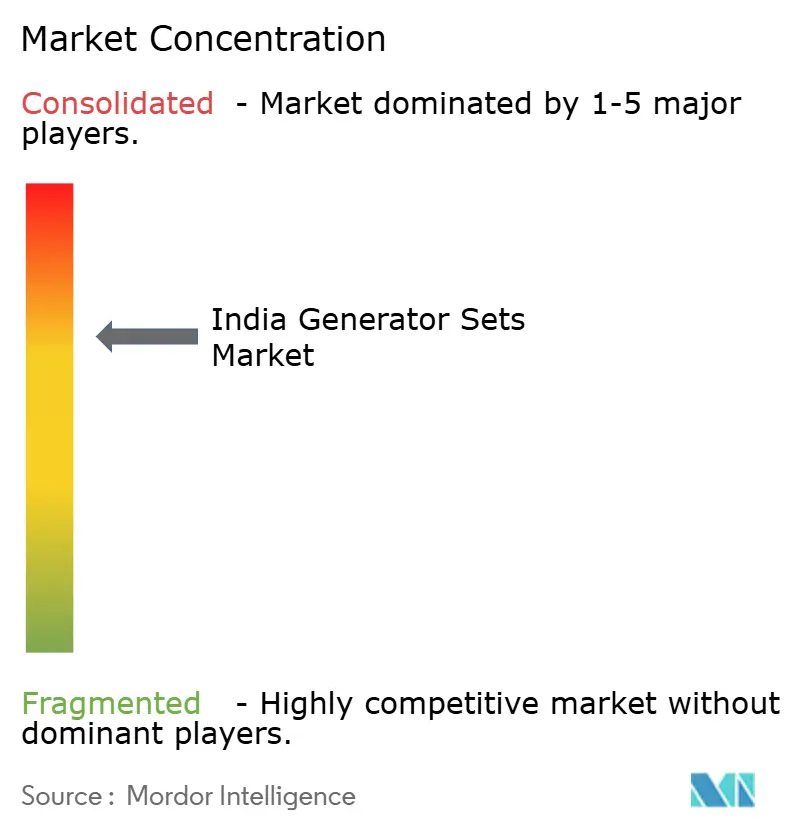

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Generator Sets Market Analysis by Mordor Intelligence

The India Generator Sets Market size is estimated at USD 1.86 billion in 2025, and is expected to reach USD 2.70 billion by 2030, at a CAGR of 7.76% during the forecast period (2025-2030).

Telecom densification, hyperscale data-center build-outs, and the Central Pollution Control Board’s CPCB-IV⁺ emission mandate are reshaping demand from episodic backup toward mission-critical infrastructure. Manufacturers are expanding capacity. Cummins India invested INR 600 crore (approximately USD 72 million) in its Phaltan plant, while Kirloskar Oil Engines commissioned an INR 250 crore (approximately USD 30 million) facility in Rajkot to keep pace with its robust order pipelines. Unreliable grid supply continues to underpin the purchase of gensets, with outage frequencies diverging sharply between industrialized Western states and climate-vulnerable northern regions. At the same time, rising construction outlays, record infrastructure spending, and growing acceptance of fuel-agnostic engines are expanding the application base. Volatile diesel prices and the growing penetration of lithium-ion UPS solutions temper, but do not derail, the long-term trajectory of the India generator sets market.

Key Report Takeaways

- By capacity, the segment below 75 kVA held 49.5% of the Indian generator sets market share in 2024, while the 75-375 kVA range is projected to advance at a 9.1% CAGR through 2030.

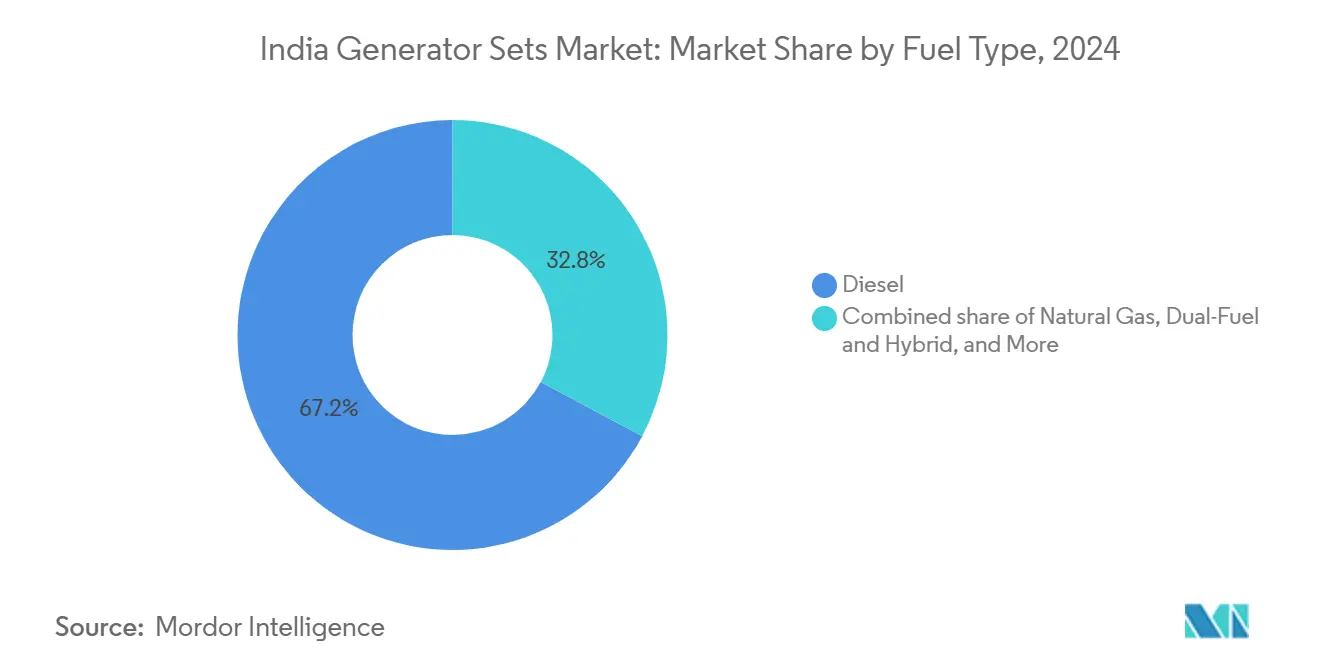

- By fuel type, diesel retained a 67.2% share in 2024; renewable and biofuel gensets are forecast to grow at a 13.5% CAGR to 2030 as CPCB-IV compliance accelerates replacement cycles.

- By application, standby power dominated with an 82.8% share in 2024, whereas micro-grid and hybrid support are poised for a 12.9% CAGR over 2025-2030.

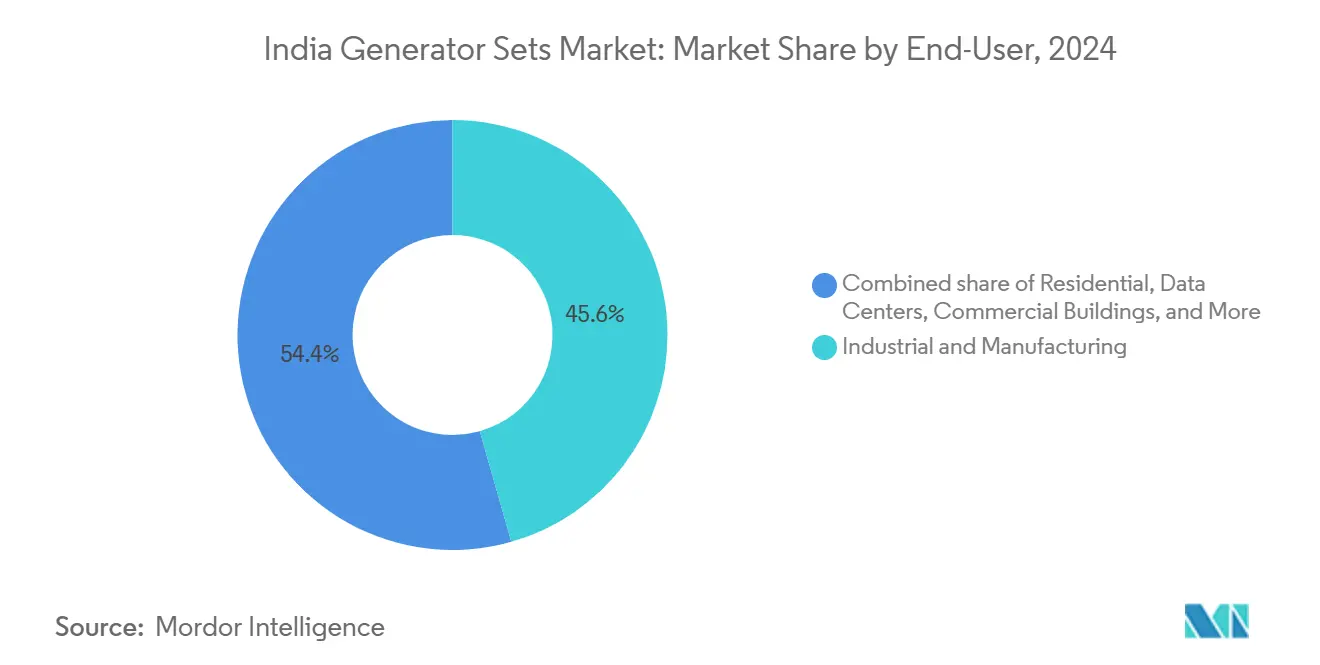

- By end-user, the industrial and manufacturing sector captured 45.6% of the Indian generator sets market size in 2024; data centers recorded the fastest growth at a 14.4% CAGR through 2030.

- Cummins India, Kirloskar Oil Engines, Mahindra Powerol, Greaves Cotton, and Caterpillar together accounted for roughly 57% of 2024 shipments, underscoring a moderately concentrated competitive field.

India Generator Sets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unreliable grid power and frequent outages | +1.8% | Uttar Pradesh, Bihar, Jharkhand | Medium term (2-4 years) |

| Expansion of telecom (5G) tower networks | +1.5% | Urban and peri-urban clusters nationwide | Short term (≤ 2 years) |

| Rising construction and real-estate activity | +1.2% | Maharashtra, Gujarat, Karnataka, Tamil Nadu, Delhi-NCR | Medium term (2-4 years) |

| Growing data-center capacity rollouts | +1.4% | Mumbai, Chennai, Hyderabad, Bengaluru, Delhi-NCR | Long term (≥ 4 years) |

| CPCB-IV⁺ mandate accelerating hospital genset replacement | +0.9% | Early adoption in Karnataka, Maharashtra | Short term (≤ 2 years) |

| Rooftop-solar plus diesel hybrid microgrids for agriculture cold-storage hubs | +0.6% | Punjab, Haryana, Uttar Pradesh, Maharashtra | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Unreliable Grid Power and Frequent Outages

Power-supply instability remains the strongest catalyst for the deployment of gensets. Northern states experience climate-induced voltage dips and feeder faults, prompting factories and hospitals to install multi-hour backup capacity, even when a grid surplus exists.(1)Central Pollution Control Board, “Emission Standards for Diesel Generator Sets,” CPCB, cpcb.nic.in Gujarat and Karnataka, despite higher renewable penetration, face intermittency during low-wind or cloudy spells that still trigger automatic genset starts. Studies from Delhi in 2024 linked unplanned diesel genset runtimes to measurable spikes in particulate emissions. The Ministry of Power aims to reduce technical and commercial losses to 12% by 2027, yet mission-critical users continue to treat gensets as non-negotiable insurance against outages.

Expansion of Telecom (5G) Tower Networks

By 2024, operators had erected 824,000 towers and nearly 3 million base transceiver stations, resulting in an aggregate energy demand of roughly 70 TWh per year.(2)TRAI, “Annual Report 2023-24,” TRAI, trai.gov.in Diesel remains the de facto fallback for 35-40% of these sites, particularly across rural and peri-urban footprints where grid access lags. Solar retrofits reduce daytime fuel burn; yet, most towers still depend on hybrid gensets for nighttime or low-irradiance periods. Department of Telecommunications guidelines now favor fuel-agnostic designs that switch seamlessly among diesel, natural gas, and biodiesel, stimulating an early-stage replacement cycle independent of equipment age.

Growing Data-Center Capacity Rollouts

India’s installed data-center load reached 950 MW in 2024 and is projected to surpass 2,000-2,100 MW by FY27, with USD 6-6.6 billion in fresh capital inflows. Tier-III and Tier-IV facilities require N+1 or 2N redundancy, resulting in 2-4 MW of genset backup for each new hyperscale hall. Operators are ordering CPCB-IV-compliant units upfront to avoid downtime during retrofit. AI workloads push rack densities higher, further increasing the baseline demand for backups.

Rooftop-Solar + Diesel Hybrid Microgrids for Agriculture Cold-Storage Hubs

Rising horticulture output and stricter cold-chain norms prompt farmers and cooperatives to combine rooftop solar with the right-sized generators. Energy Efficiency Services Limited pilots in Punjab and Haryana cut diesel consumption by nearly half while safeguarding 24/7 refrigeration. Hybrid deployments also mitigate price shocks when diesel hovers between INR 87 and INR 94 per liter, thereby bolstering the economics of perishable-produce hubs.(3)Petroleum Planning and Analysis Cell, “Diesel Price Data,” PPAC, ppac.gov.in

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter CPCB-IV⁺ emission norms raise CAPEX | -1.1% | National, acute in Delhi-NCR, Mumbai, Bengaluru, Chennai | Short term (≤ 2 years) |

| Volatile diesel prices erode operating-cost advantage | -0.9% | National, higher impact in states with frequent outages (UP, Bihar, Jharkhand) | Medium term (2-4 years) |

| Cheap lithium-ion UPS adoption in IT / ITES offices | -0.7% | Urban centers (Bengaluru, Hyderabad, Pune, Gurugram, Noida) | Medium term (2-4 years) |

| Emergency DG-set bans during NCR severe-AQI alerts | -0.5% | Delhi-NCR (Delhi, Gurugram, Noida, Ghaziabad, Faridabad) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter CPCB-IV⁺ Emission Norms Raise CAPEX

The new standards inflate unit prices 15-20% and require specialized after-treatment service networks.(4)Central Pollution Control Board, “Emission Standards for Diesel Generator Sets,” CPCB, cpcb.nic.in Smaller commercial establishments often delay upgrades, while larger corporates accelerate replacement to avoid non-compliance fines during air-quality emergencies. OEMs counter hesitation by bundling lease-plus-maintenance contracts that smooth capital outlays but elevate monthly operating expenses.

Volatile Diesel Prices Erode Operating-Cost Advantage

Pump prices oscillated between INR 87 and Rs 94 per liter in 2024-2025, squeezing users who run gensets for four or more hours daily. Facilities located in states with subsidized industrial tariffs sometimes find grid electricity cheaper than self-generation. The expansion of city-gas distribution, targeting 18,336 CNG stations by 2032, broadens the appeal of natural-gas gensets; however, the pipeline reach still covers less than one-third of industrial clusters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity: Mid-Range Units Capture Industrial Upgrades

The 75-375 kVA band contributed a 9.1% CAGR through 2030, outstripping the below-75 kVA tier, which nonetheless dominated with 49.5% of 2024 shipments. Mid-capacity gensets serve factory lines, Tier 2 data halls, and construction sites where space is limited but redundancy is crucial. Cummins India’s CPCB-IV⁺ portfolio now spans 20-2,500 kVA, signaling an industry-wide pivot from incremental tweaks toward full regulatory alignment. The India generator sets market size for the 75-375 kVA cluster stood at USD 0.62 billion in 2024 and is expected to reach USD 1.05 billion by 2030. Modular arrays of three or four 125 kVA machines are increasingly replacing single 400 kVA units, thereby limiting single-point failures and easing load balancing.

Aging fleets in mining and heavy industries sustain demand for 375-750 kVA and 750-2,000 kVA equipment, while sets exceeding 2,000 kVA remain a niche market, primarily used in pit mines and large pipeline pumps. Mahindra Powerol and Ashok Leyland leverage localized casting and machining bases to price competitively against imports. Labs and IT offices experiencing brief outages tend to lean toward lithium-ion UPS, but multi-hour downtime remains relevant in the Indian generator sets market.

By Fuel Type: Renewable and Bio-Fuel Gensets Challenge Diesel Dominance

Diesel’s 67.2% share remains entrenched because fuel supply chains and technician familiarity are well established. However, renewable, biofuel, and natural gas are projected to set a brisk 13.5% CAGR, reflecting tighter emission rules and rising corporate ESG targets. Greaves Cotton’s fuel-agnostic blocks accept blends up to B100 or switch to gas with minor control tweaks. The India generator sets market share for gas and biofuel variants is expected to increase from 12.4% in 2024 to 21% by 2030. The rollout of pipelines and mandated city-gas coverage expands the commercial case for gas-fired units, especially in western metropolitan areas and the Delhi-Mumbai Industrial Corridor.

Hybrid diesel-solar and dual-fuel systems are gaining popularity in agriculture, cold storage, and telecom tower backhaul, mitigating both fuel price swings and emission liabilities. NTPC’s 200 kW solar-hydrogen microgrid in Ladakh showcases frontier applications but remains costlier than diesel by a factor of two to three.(5)NTPC, “Solar-Hydrogen Microgrid Project, Ladakh,” Ntpc.co.in Until renewable genset capex narrows, diesel continues dominating heavy-duty (>750 kVA) classes within the India generator sets industry.

By Application: Micro-Grid and Hybrid Support Redefines Backup Power

Standby use accounted for 82.8% of 2024 installations, anchored by hospitals, data centers, and commercial real estate. Yet, micro-grid and hybrid support is the fastest-growing niche, with a 12.9% CAGR, buoyed by the economics of rooftop solar and batteries. Energy service companies now bundle 50 kWp PV arrays, 120 kWh lithium packs, and 100 kVA gensets into turnkey cold-chain offerings. IIT Bombay’s vanadium redox-flow pilot, paired with a diesel engine, cuts fuel bills by 60%, hinting at long-term disruption potential.

Prime and continuous power roles persist in mining, island resorts, and pipeline projects, whereas peak-shaving demand edges downward as commercial buildings adopt batteries to dodge high time-of-use tariffs. Rentals remain lucrative, with USD 2.3 billion in 2024, as Caterpillar adds 1,500 CPCB-IV⁺ units to its fleet to capitalize on public-works contracts funded by the FY25 capital outlay.

By End-User: Data Centers Outpace Industrial Manufacturing

Factories and process industries accounted for 45.6% of 2024 revenue, but hyperscale and colocation data halls grew more quickly. Data-center operators deploy multiple 2 MW strings to meet 2N redundancy, pushing the India generator sets market size for this end-user to USD 0.41 billion in 2024. A projected 14.4% CAGR is expected to lift the tally close to USD 0.95 billion by 2030. Healthcare leads regulated replacement demand thanks to CPCB-IV⁺ enforcement and state-run solar-hybrid schemes.

Mining, utilities, and oil and gas favor 750-kVA-plus sets capable of multi-shift duty. The residential and small-office segments predominantly use machines with a capacity below 75 kVA, yet in metros, some of this load migrates to silent lithium UPS solutions. Nevertheless, long-duration blackout risk keeps the India generator sets market firmly rooted in conventional diesel technology for high-power arenas.

Geography Analysis

Maharashtra, Gujarat, Karnataka, and Tamil Nadu generated more than 60% of the 2024 revenue. Maharashtra’s manufacturing gross value added rose 9.9% in FY25, and the Mumbai data-center hub adopted 4-6 MW backup clusters per facility, driving bulk orders for 750-2,000 kVA systems.(6)Ministry of Statistics and Programme Implementation, “Manufacturing Sector Growth Data FY25,” Mospi.gov.in Gujarat’s coastal SEZs experience fewer voltage fluctuations, yet monsoon transformer failures push industrialists to retain gensets as insurance.

Karnataka’s healthcare solarization plan accelerates the adoption of hybrid gensets, while Bengaluru’s IT corridor sustains demand below 75 kVA. Tamil Nadu’s automotive, electronics, and expanding Chennai data-center ecosystem also require mid-to-high capacity equipment. In the Delhi-NCR region, GRAP Stage-III/IV bans on non-CPCB-IV⁺ units during AQI spikes accelerate fleet renewal and prompt rental operators to swap their inventories.

Northern states, such as Uttar Pradesh and Bihar, exhibit a higher outage frequency, stimulating sales of compact sets. Agriculture-centric Punjab and Haryana see rooftop solar and diesel combos gaining traction as produce exporters require 24/7 refrigeration, according to EESL. Nationwide transmission upgrades under the INR 11.11 lakh-crore FY25 plan will not immediately displace backup demand for the India generator sets market because mission-critical sites still hedge against any residual grid risks

Competitive Landscape

The field is moderately concentrated, with the top five brands accounting for approximately 57% of 2024 shipments. Cummins India and Kirloskar Oil Engines expanded domestic capacity, while Mahindra Powerol and Greaves Cotton push fuel-agnostic lines that address emission compliance without altering customer fuel logistics. International majors such as Caterpillar, Generac, Kohler, and Rolls-Royce (MTU) enlarge rental fleets and introduce telematics-ready models catering to data-center clients that demand predictive maintenance.

Localization is the strategic cornerstone. Ashok Leyland’s INR 1,000 crore Hosur expansion enhances component self-reliance for high-output gensets designed for mining and construction. The Ministry of Heavy Industries targets 70-80% local content by 2030, prompting OEMs to partner with domestic casting, electronics, and after-treatment suppliers. Smaller disruptors, such as Hykon, experiment with battery-genset hybrids up to 240 kVA, addressing urban facilities that are sensitive to noise and emissions, although current price premiums limit rapid uptake.

White-space opportunities proliferate around gas gensets in pipeline-served cities, hybrid diesel-solar packages for agriculture cold chains, and modular, factory-assembled units for rental fleets serving road-building and metro-rail corridors funded under the FY25 capital program.

India Generator Sets Industry Leaders

Kirloskar Oil Engines Limited

Greaves Cotton Limited

Mahindra Powerol (M&M Ltd.)

Ashok Leyland Ltd. (Leypower)

Cummins India Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Cummins India commissioned its Rs 600 crore Phaltan facility, adding capacity for 50,000 CPCB-IV⁺ gensets per year.

- December 2024: Kirloskar Oil Engines opened an INR 250 crore plant in Rajkot, dedicated to the 75-375 kVA band.

- November 2024: Mahindra Powerol launched a telematics-enabled CPCB-IV⁺ lineup from 20-2,500 kVA.

- October 2024: Greaves Cotton unveiled fuel-agnostic engines that run on diesel, gasoline, or B100 biodiesel without requiring any hardware changes.

- September 2024: Ashok Leyland completed an INR 1,000 crore expansion at Hosur for more than 750 kVA gensets.

- August 2024: NTPC commissioned a 200 kW solar-hydrogen microgrid in Ladakh with diesel backup.

India Generator Sets Market Report Scope

The India generator sets market report includes:

By Capacity

| Below 75 kVA |

| 75 to 375 kVA |

| 375 to 750 kVA |

| 750 to 2,000 kVA |

| Above 2,000 kVA |

By Fuel Type

| Diesel |

| Natural Gas |

| Dual-Fuel and Hybrid |

| Renewable/Bio-fuel |

| Others |

By Application

| Standby Power |

| Prime/Continuous Power |

| Peak-Shaving |

| Rental/Temporary Power |

| Micro-grid and Hybrid Support |

By End-User

| Residential |

| Commercial Buildings |

| Industrial and Manufacturing |

| Data Centers |

| Healthcare Facilities |

| Oil and Gas |

| Utilities and Power |

| Mining and Construction |

| By Capacity | Below 75 kVA |

| 75 to 375 kVA | |

| 375 to 750 kVA | |

| 750 to 2,000 kVA | |

| Above 2,000 kVA | |

| By Fuel Type | Diesel |

| Natural Gas | |

| Dual-Fuel and Hybrid | |

| Renewable/Bio-fuel | |

| Others | |

| By Application | Standby Power |

| Prime/Continuous Power | |

| Peak-Shaving | |

| Rental/Temporary Power | |

| Micro-grid and Hybrid Support | |

| By End-User | Residential |

| Commercial Buildings | |

| Industrial and Manufacturing | |

| Data Centers | |

| Healthcare Facilities | |

| Oil and Gas | |

| Utilities and Power | |

| Mining and Construction |

Key Questions Answered in the Report

What is the current value of the India generator sets market?

The India generator sets market size reached USD 1.86 billion in 2025 and is projected to hit USD 2.70 billion by 2030.

Which capacity range is expanding the fastest?

Gensets rated 75-375 kVA grow at 9.1% CAGR through 2030, benefiting mid-sized factories and data halls.

Why are renewable and bio-fuel gensets gaining ground?

CPCB-IV? norms and corporate ESG targets drive a 13.5% CAGR for renewable and bio-fuel units despite diesels dominance.

How will data centers influence future demand?

Hyperscale and colocation sites push backup needs to 2-4 MW per facility, elevating data-center genset revenue at a 14.4% CAGR to 2030.

Which regions account for the bulk of sales?

Maharashtra, Gujarat, Karnataka, and Tamil Nadu together deliver over 60% of market revenue due to concentrated industry and data-center projects.

What is a key regulatory headwind?

CPCB-IV? emission standards raise genset CAPEX by 15-20% and accelerate fleet replacement schedules.

Page last updated on: