Taiwan Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

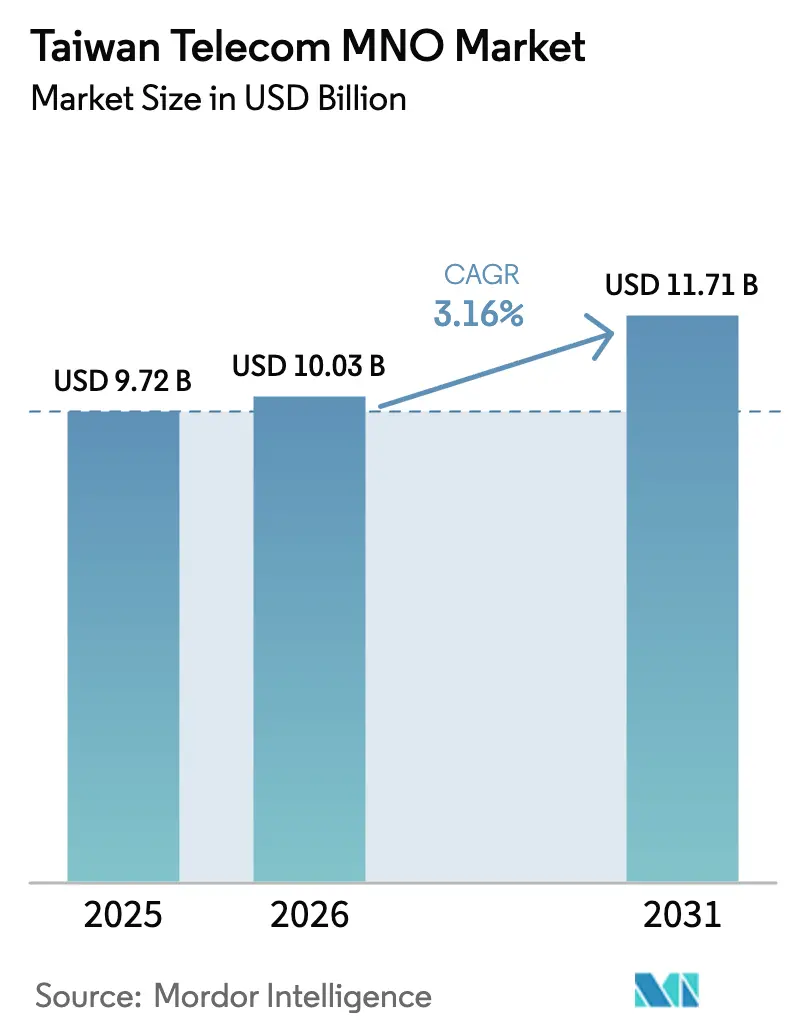

| Base Year Market Size (2025) | USD 9.72 Billion |

| Market Size (2026) | USD 10.03 Billion |

| Market Size (2031) | USD 11.71 Billion |

| Growth Rate (2026 - 2031) | 3.16% CAGR |

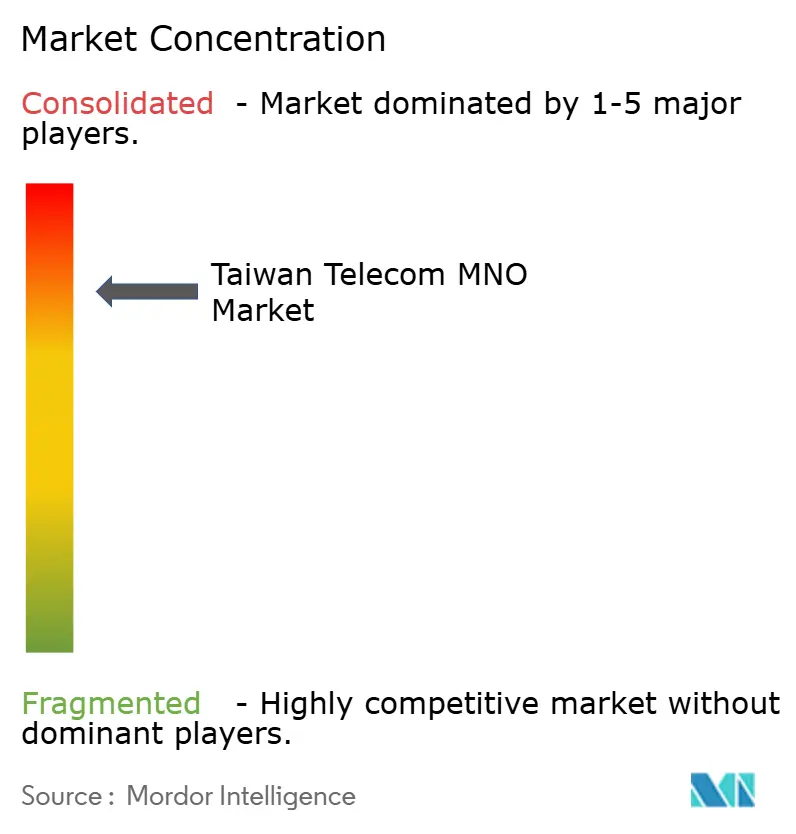

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taiwan Telecom MNO Market Analysis by Mordor Intelligence

The Taiwan Telecom MNO Market size was valued at USD 9.72 billion in 2025 and estimated to grow from USD 10.03 billion in 2026 to reach USD 11.71 billion by 2031, at a CAGR of 3.16% during the forecast period (2026-2031).

Robust enterprise digitalization, aggressive 5G monetization, and multi-orbit connectivity investments counterbalance flat voice revenues, ensuring steady expansion despite saturation. The consolidation to three nationwide operators helps unlock scale economies that finance dense 5G builds, new submarine cables, and satellite ground stations. Sub-6 GHz and mmWave spectrum deployments accelerate urban coverage, while NCC’s private-network policy spurs localized innovation in semiconductor corridors. Taiwan’s seismic exposure catalyzes redundant routing strategies, positioning submarine-satellite convergence as a differentiated service lever in the Taiwan telecom MNO market.

Key Report Takeaways

- By service type, data and internet services held 54.45% of the Taiwan telecom MNO market share in 2025, whereas IoT and M2M services are forecast to expand at a 3.27% CAGR through 2031.

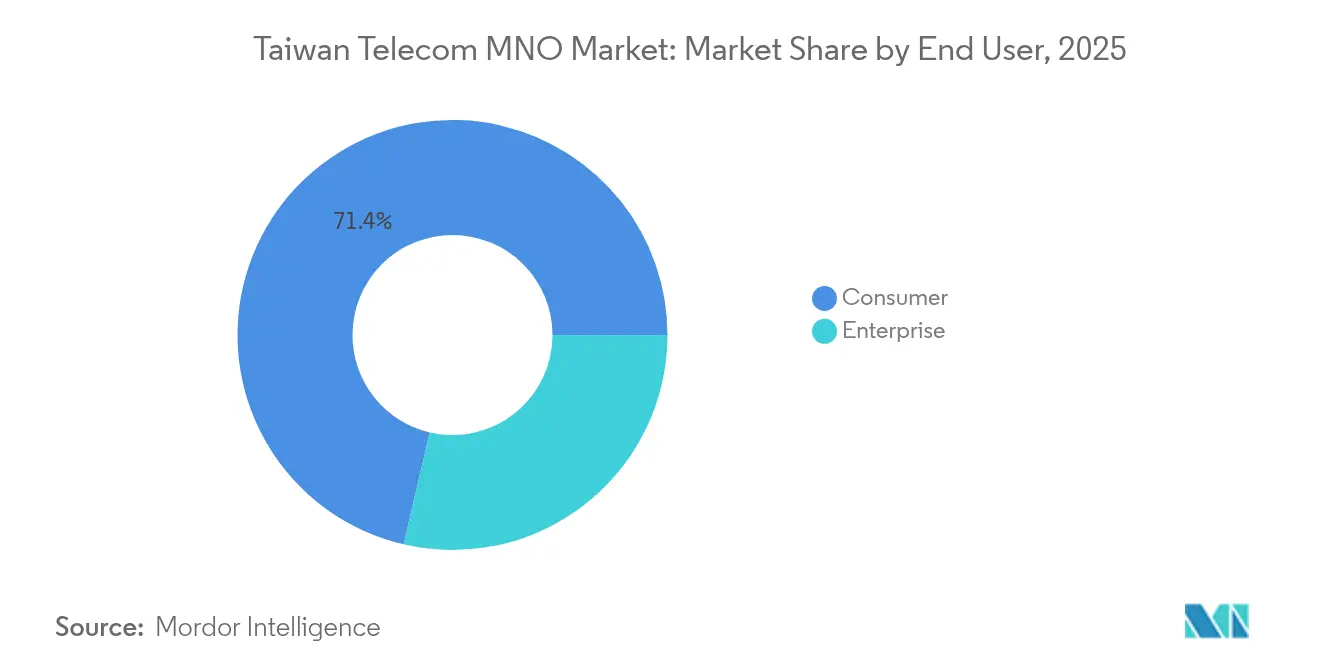

- By end-user, consumer connections captured 71.35% of the Taiwan telecom MNO market size in 2025, while enterprise services are advancing at a 3.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Taiwan Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G network rollouts and monetization | +0.8% | Taipei, Taichung, Kaohsiung metros | Medium term (2-4 years) |

| Soaring mobile-data consumption per user | +0.6% | Nationwide | Short term (≤ 2 years) |

| NCC’s pro-competition spectrum policy | +0.4% | Nationwide | Long term (≥ 4 years) |

| Private 5G demand from semiconductor fabs (TSMC, UMC) | +0.5% | Hsinchu Science Park and northern industrial belt | Medium term (2-4 years) |

| Satellite back-haul projects for island resiliency | +0.3% | Nationwide and outlying islands | Long term (≥ 4 years) |

| Cloud-gaming and XR partnerships needing ultra-low latency | +0.2% | Urban gaming clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G network rollouts and monetization drive enterprise revenue diversification

Operators crossed 10 million 5G subscriptions by December 2024, yet roughly 19.5 million users remain on 4G packages, creating headroom for upsell tiers [1]Johan Affandy, “The State of Taiwan’s 5G Network,” Ookla, ookla.com. Chunghwa Telecom’s Dynamic Network Solution automates slice provisioning, giving factories deterministic latency, while Taiwan Mobile’s USD 124 million Systex stake underscores a pivot to AI-enabled private 5G. The strategic shift centers on enterprise connectivity bundles, edge compute, SLAs, and cybersecurity, rather than pure data plans. As 5G Standalone coverage exceeds 90% of the population, differentiated slicing becomes the primary lever for ARPU uplift in the Taiwan telecom MNO market. Continuous spectrum re-farming and mmWave trials in Taipei’s Xinyi district signal long-term densification commitments.

Soaring mobile-data consumption strains network capacity and ARPU models

Average monthly data use surpassed 32 GB across all operators by January 2024, a figure rivaling regional leaders. Unlimited NTD 499 plans stimulate usage but erode margins, dropping Chunghwa Telecom’s mobile ARPU to USD 18.10 in 2024. Small-cell infill, massive MIMO upgrades, and carrier aggregation sustain median downlink speeds near 90 Mbps, yet incremental capex pressures balance sheets. The revenue squeeze accelerates product diversification into IoT connectivity, cloud gaming partnerships, and bundled streaming services. These high-engagement offerings help stabilize average revenue per account, preserving profitability in the Taiwan telecom MNO market.

NCC’s pro-competition spectrum policy enables private-network innovation

By April 2025, the regulator had cleared 74 private 5G licenses, well above its 50-site goal, covering smart factories, logistics hubs, and hospital campuses. The 4.8-4.9 GHz allocation allows enterprises such as AU Optronics and ASUS to design indoor-cell architectures without relying exclusively on MNO wholesale. This democratization pushes national operators toward collaborative managed-service models that bundle backbone, security, and edge processing. The liberalized framework differentiates Taiwan from markets where carriers retain sole spectrum control, catalyzing a services-led growth path for the Taiwan telecom MNO market.

Private 5G demand from semiconductor fabs creates niche high-value market

Hsinchu-based giants TSMC and UMC need microsecond-level determinism for lithography robots, prompting pilots of on-premise private 5G anchored by local edge servers. Operators co-design slice templates with OEMs to guarantee packet-error rates below 1e-5, command-and-control latency under 10 ms, and firmware air-updates with zero downtime. Premium SLA pricing generates higher revenue per connection than consumer enhanced-mobile-broadband contracts, supporting double-digit returns on specialized network investments. Geographic clustering of fabs enables shared infrastructure, further improving payback timelines inside the Taiwan telecom MNO market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Market saturation and flat voice revenues | -0.4% | Nationwide | Short term (≤ 2 years) |

| High spectrum/infrastructure CAPEX burden | -0.6% | Nationwide | Medium term (2-4 years) |

| Seismic risk to submarine and terrestrial fiber routes | -0.3% | Nationwide | Long term (≥ 4 years) |

| Shortage of 5G slicing/security talent | -0.2% | Technology hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Market saturation and flat voice revenues constrain traditional growth

Subscriber penetration above 120% forces churn-based competition, muting organic adds and compressing tariff ceilings. OTT messaging further cannibalizes voice, lowering call ARPU even as unlimited plans proliferate. Reduced rivalry post-mergers tempers price wars but also limits disruptive offerings. The scheduled 3G sunset in 2025 will push the last legacy users to 4G/5G bundles, after which upsell catalysts diminish. Sustained value creation in the Taiwan telecom MNO market will therefore hinge on digital-service adjacencies rather than core connectivity.

High spectrum and infrastructure capex burden pressures operator finances

Chunghwa Telecom earmarked USD 1.06 billion for 2025 capex covering the E2A trans-Pacific cable, terrestrial fiber hardening, and new AI data centers [2]台北時報, “CHT to lay new undersea cables,” Taipei Times, taipeitimes.com. Spectrum amortization from earlier auctions still weighs on EBITDA margins, while satellite ground-segment builds with OneWeb and Astranis add fresh strain. Although tower-sharing and RAN-sharing trim rural costs, they dilute network-quality differentiation. Operators must balance resilience mandates with shareholder returns, slowing discretionary innovation budgets within the Taiwan telecom MNO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data services dominate, IoT accelerates

Data and internet streams commanded 54.45% of the Taiwan telecom MNO market share in 2025, reflecting subscriber preference for high-definition video, mobile gaming, and cloud collaboration. Voice and SMS revenues continue to contract, yet still anchor cross-bundled pricing positioned as “unlimited basics.” OTT and PayTV add-ons, when integrated with fiber backhaul and mobile plans, raise ARPU stickiness. The IoT and M2M category, although contributing a smaller slice today, is advancing at a 3.27% CAGR through 2031, outpacing all other service lines. Factory automation, fleet telematics, and smart-utility metering underpin this ascent. Carriers increasingly re-package network APIs, security, and device management shells as platform services, broadening the revenue canvas inside the Taiwan telecom MNO industry.

Service-level margin dynamics differ sharply across sub-segments. High-bandwidth consumer data exhibits low incremental cost per gigabyte but also faces intense price pressure, while narrowband IoT commands higher per-bit economics thanks to SLA premium. Messaging’s future rests mainly on A2P and verification workflows, where two-factor authentication volumes remain resilient. Wholesale international transit supports enterprise VPNs but requires periodic price resets given regional submarine cable over-capacity. As these trends mature, the Taiwan telecom MNO market will see revenue mix migrate from traditional bit-pipe models toward platform-based and partnership-based monetization schemes, safeguarding long-term top-line stability.

By End-User: Enterprise momentum outpaces consumer maturation

Consumer lines still contributed 71.35% of the Taiwan telecom MNO market size during 2025, but revenue growth has largely plateaued. Operators rely on content bundles, loyalty programs, and device-financing plans to curb churn. In parallel, enterprise business grew at 3.51% CAGR, propelled by digital-factory retrofits in the semiconductor, petrochemical, and financial services verticals. Chunghwa Telecom’s enterprise portfolio booked a 10.2% year-over-year uplift in 2024; ICT-led sub-segments jumped 24.1%. Far EasTone likewise reports double-digit gains in cloud communication and data analytics solutions.

Corporate clients demand guaranteed latency, cybersecurity assurances, and integration with hyperscale clouds, enabling carriers to charge premium MRCs. Offshore wind farms and island-based logistics chains particularly value multi-orbit backup connectivity. Remote OT monitoring, AR-supported maintenance, and blockchain-secured supply-chain tracking figure among pilots converting to commercial contracts in 2025. Over the next five years, the Taiwan telecom MNO market share of enterprise lines is projected to expand by nearly 5 percentage points as industries digitize operations in line with government-backed “Twin Transformation” roadmaps. Operators that build consultative sales teams and vertical-specific solution stacks will capture disproportionate wallet share.

Geography Analysis

Population density along the western corridor, from Taipei to Kaohsiung, accounts for over 80% of nationwide traffic, enabling efficient network ROI. Northern Taiwan’s knowledge-economy nucleus secures the largest revenue slice, led by government, finance, and semiconductor headquarters. Central Taiwan, home to Taichung’s precision-machinery firms, exhibits the fastest enterprise data growth, assisted by NCC incentives for private 5G licensing. Southern city Kaohsiung, transitioning from heavy industry to green energy, demonstrates rising IoT connectivity spend tied to offshore wind maintenance fleets and smart-port logistics.

Eastern counties feature rugged terrain and low subscriber counts. Here operators deploy RAN-sharing to meet universal-service mandates without duplicative towers, achieving 95.47% rural 5G coverage in early 2025 . Outlying islands, Kinmen, Matsu, Penghu, depend on single-route submarine cables frequently damaged by fishing gear or seismic shifts. Redundant microwave relays and low-Earth-orbit satellite links now backstop those cables as part of the Ministry of Digital Affairs’ 700-terminal resiliency program.

Internationally, fifteen submarine systems converge on Taiwan’s western coast, funneling hyperscale traffic to Japan, the United States, and Singapore. Chunghwa Telecom’s USD 139.2 million stake in the E2A trans-Pacific build diversifies landing points and alleviates choke-point concentration. Political sensitivities limit direct mainland-China capacity, prompting carriers to reroute via Hong Kong or Guam. This geopolitical backdrop shapes investment calculus and reinforces the strategic imperative for satellite-fiber hybrids within the Taiwan telecom MNO market.

Competitive Landscape

Post-merger consolidation leaves Chunghwa Telecom, Taiwan Mobile, and Far EasTone controlling nearly the entire subscriber base, signifying a tight oligopoly. Chunghwa Telecom holds 37.9% of lines and 40.3% of revenue, leveraging extensive fiber, international gateways, and enterprise consultative depth to sustain leadership. Taiwan Mobile differentiates through aggressive fintech partnerships and bundled streaming content, while Far EasTone pursues AI-enabled network optimization and cloud-contact-center playbooks. Price competition has cooled, replaced by experiential and enterprise-solution races that underline a value-based rivalry.

Shared-infrastructure deals continue to proliferate. All three carriers co-fund small-cell densification in Taipei’s underground metro to hedge capex, yet each preserves independent spectrum blocks for service tiering. Strategic moves during 2024-2025 include Taiwan Mobile’s alliance with Lynk Global for direct-to-device satellite service, Far EasTone’s edge-compute JV with Microsoft, and Chunghwa Telecom’s Ericsson-backed 5G Advanced roadmap. Such initiatives emphasize service-stack layering rather than raw airtime pricing battles within the Taiwan telecom MNO market.

White-space opportunities revolve around private 5G, secure IoT orchestration, and satellite-backed SD-WAN for export-oriented SMEs. Competitive barriers stem from spectrum ownership, nationwide backhaul, and deeply rooted retail channels. Yet regulatory scrutiny remains active; NCC imposes quality of service benchmarks and merger remedies that mandate mid-band spectrum divestitures or MVNO capacity grants if competition deteriorates. Overall, the Taiwan telecom MNO industry is expected to evolve toward platform-centric competition where API exposure, edge services, and industry partnerships, not mere gigabyte allowances, shape market fortunes.

Taiwan Telecom MNO Industry Leaders

Chunghwa Telecom (Chunghwa Telecom Co., Ltd.)

Taiwan Mobile Co., Ltd.

Far EasTone Telecommunications Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Taiwan Mobile partnered with Phison to integrate NAND-based AI accelerators, cutting private-AI deployment costs by 90% and slashing rollout time by 30 days.

- March 2025: Chunghwa Telecom and Ericsson unveiled a joint framework for 5G Advanced and early 6G field trials, including a legal-sector-focused large-language-model “Tlibra”.

- March 2025: Chunghwa Telecom signed an MOU with Nokia targeting a commercial 6G launch by 2030, emphasizing AI-native orchestration and multi-orbit integration.

- November 2024: Taiwan Mobile executed a satellite-to-cell MoU with Lynk Global, extending coverage to maritime and mountainous zones.

- November 2024: Nokia broadened its 5G supply contract with Taiwan Mobile, introducing carrier-aggregation features for dense urban zones.

Taiwan Telecom MNO Market Report Scope

Basic telecommunications services encompass public network infrastructure, data transmission, and essential voice communication services. These include fixed and mobile phone services, network and data communication, and information services. In Taiwan's telecom market, vendors provide various services, spanning voice, video, Internet, and communication services. Voice services, whether wired or wireless, are a key facet of these offerings, driving market growth in Taiwan.

The Taiwanese telecom market report is segmented by services (voice services (wired and wireless), data and messaging services, and OTT and PayTV services). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the 2026 value of the Taiwan telecom MNO market?

The Taiwan telecom MNO market size stood at USD 10.03 billion in 2026.

How fast is the overall market expected to grow through 2031?

It is forecast to expand at a 3.16% CAGR, reaching USD 11.71 billion by 2031.

Which service type controls the largest revenue share?

Data and internet services lead with 54.45% of 2025 revenue.

Which segment is growing the quickest?

IoT and M2M connections are advancing at a 3.27% CAGR through 2031.

How concentrated is competition after recent mergers?

Three nationwide operators now command almost the entire subscriber base, yielding an oligopolistic market structure.

Why are satellite links gaining attention?

Taiwan’s seismic risk and submarine-cable vulnerability drive demand for multi-orbit backup to secure international connectivity.

Page last updated on: