Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

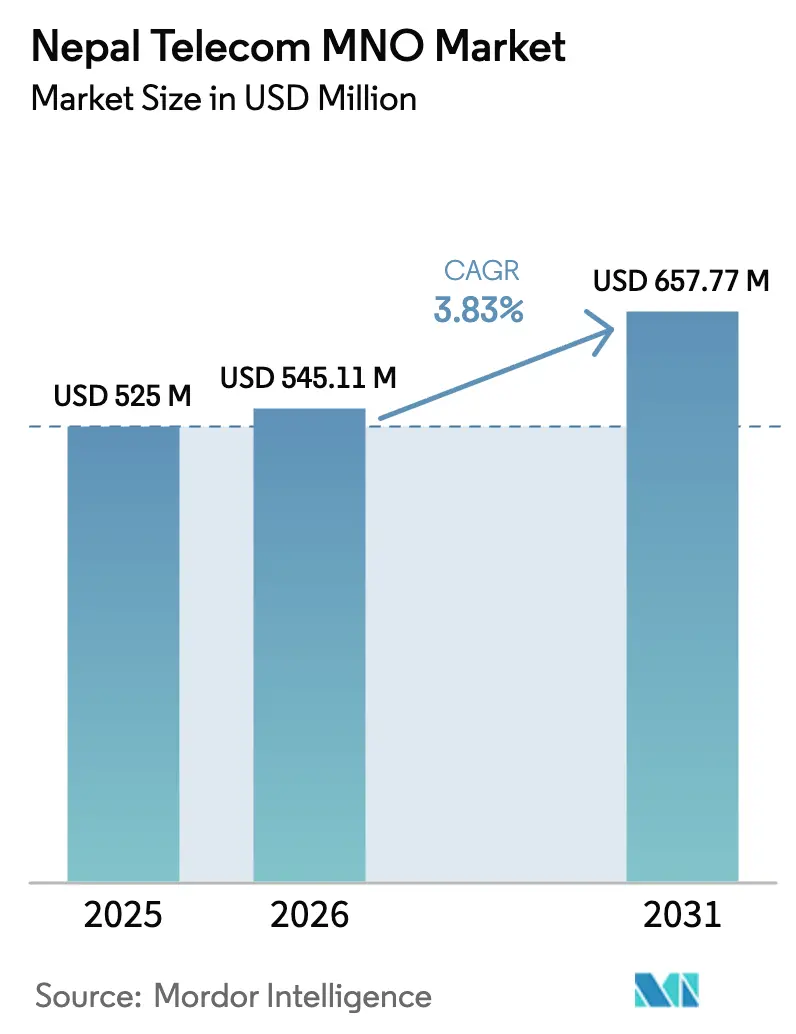

| Base Year Market Size (2025) | USD 525 Million |

| Market Size (2026) | USD 545.11 Million |

| Market Size (2031) | USD 657.77 Million |

| Growth Rate (2026 - 2031) | 3.83% CAGR |

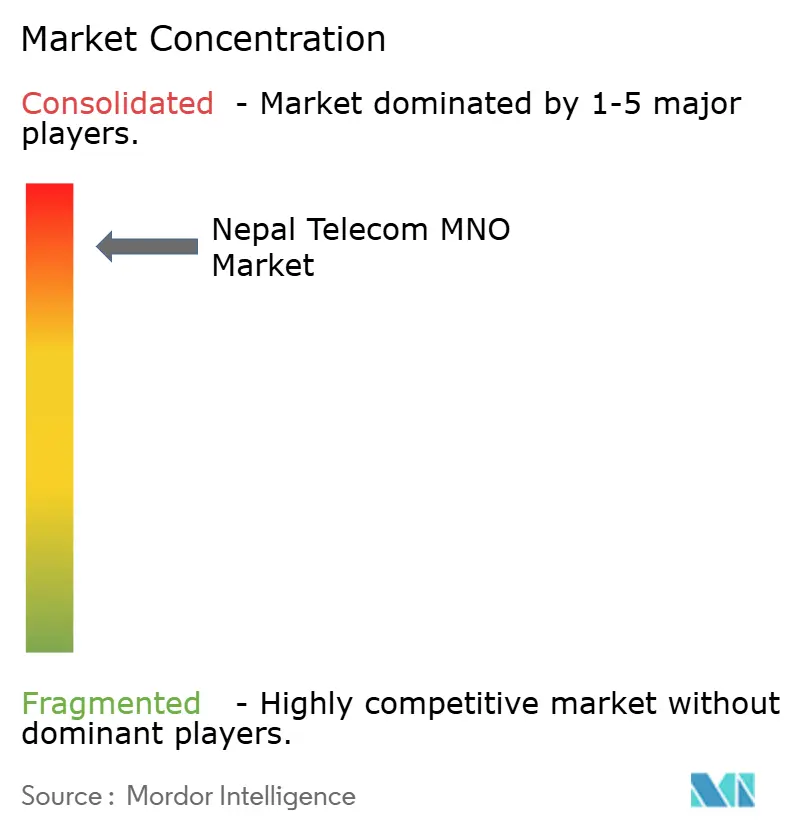

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nepal Telecom MNO Market Analysis by Mordor Intelligence

The Nepal Telecom MNO Market size was valued at USD 525 million in 2025 and estimated to grow from USD 545.11 million in 2026 to reach USD 657.77 million by 2031, at a CAGR of 3.83% during the forecast period (2026-2031).

The ongoing shift reflects mobile penetration above 130%, a widening array of data-centric services, and deliberate spectrum re-farming that balances 4G densification with staged 5G investment. Operators have responded to falling voice revenues by prioritizing digital payment integration and OTT collaboration, while the new Telecommunications Bill 2081 (2024) seeks to open ownership rules that previously curtailed foreign capital inflows. Sustained subsidies under the Digital Nepal Framework are closing rural coverage gaps, yet geopolitical equipment scrutiny and power-grid instability in mountainous terrain inflate capital and operating costs. Competitive intensity within the two-player structure has sharpened around enterprise connectivity, digital wallets, and IoT solutions that promise stickier margins than prepaid voice.

Key Report Takeaways

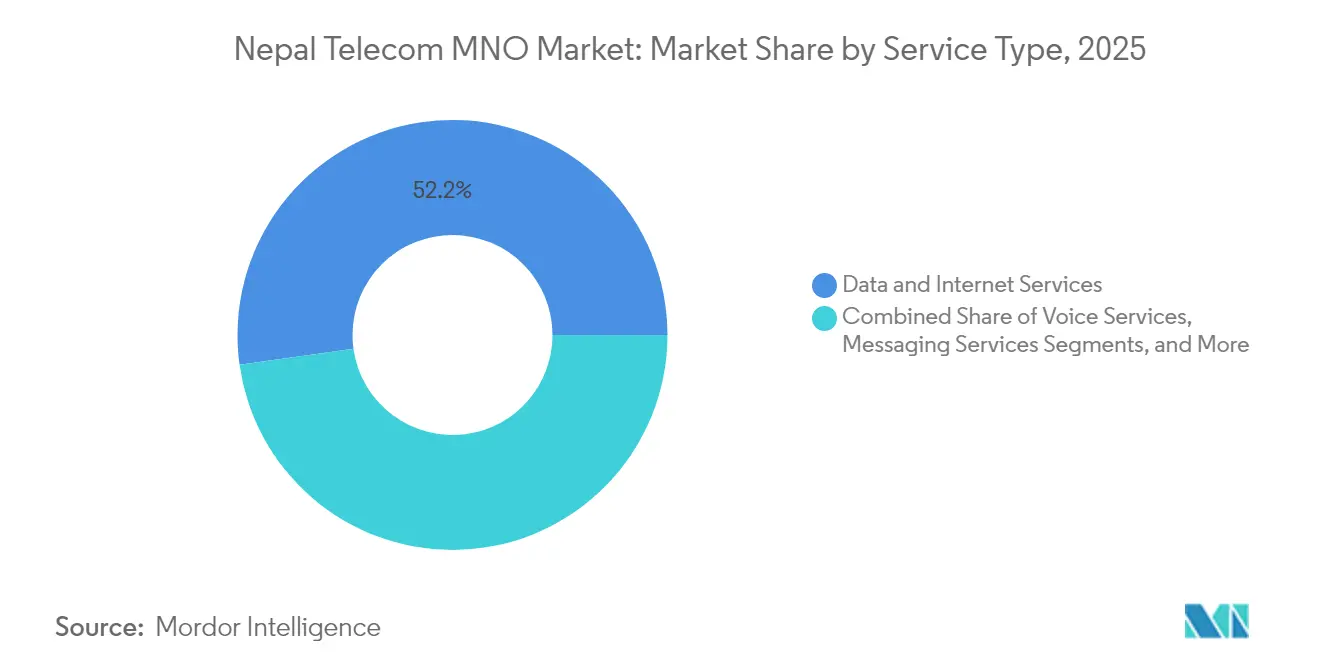

- By service type, data and internet services held 52.21% of Nepal Telecom MNO market share in 2025, while IoT and M2M services are advancing at a 4.05% CAGR through 2031.

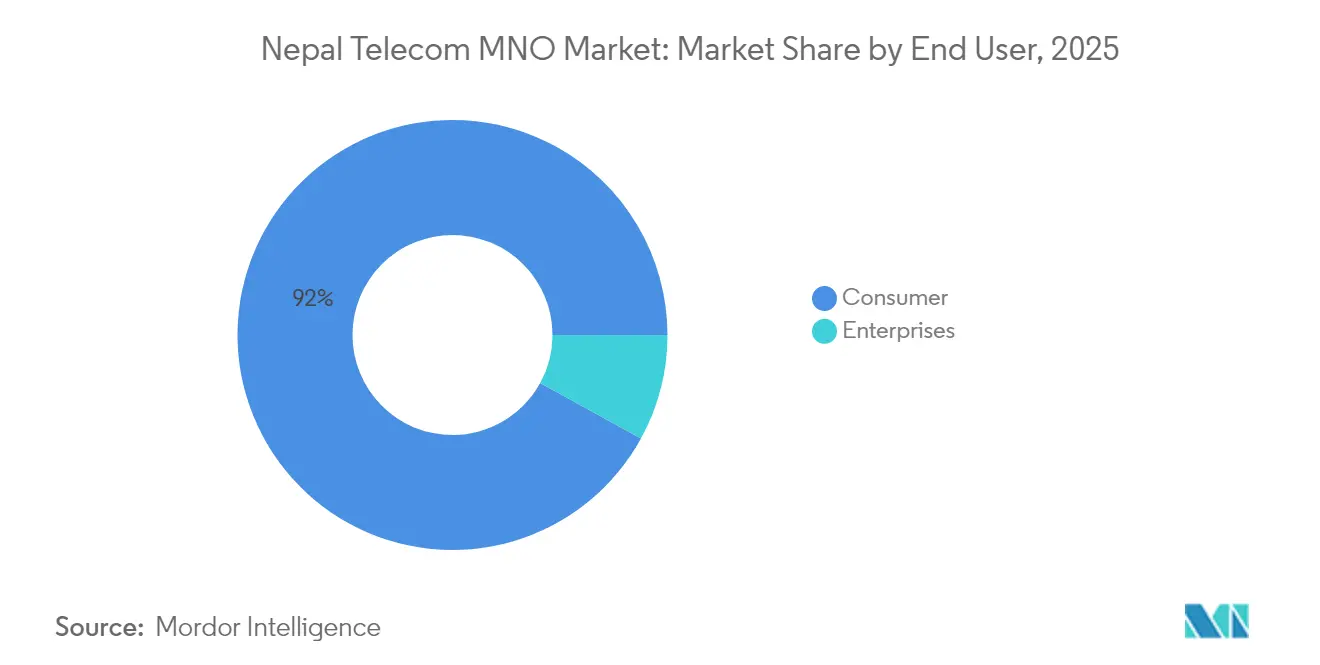

- By end user, consumer accounts for 92.01% of the Nepal Telecom MNO market size in 2025; enterprise services register the fastest trajectory at a 4.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nepal Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 4G coverage expansion and imminent 5G pilots | +1.2% | National urban corridors | Medium term (2-4 years) |

| Surging mobile data demand fueled by video and OTT apps | +0.9% | Nationwide, urban skew | Short term (≤ 2 years) |

| Digital Nepal Framework subsidies for rural broadband | +0.7% | Remote districts | Long term (≥ 4 years) |

| Smartphone penetration surpassing 70% of population | +0.6% | National, semi-urban lift | Medium term (2-4 years) |

| USSD-based mobile payments unlocking feature-phone spending | +0.4% | Rural, semi-urban | Short term (≤ 2 years) |

| Connectivity demand in trekking and mountaineering corridors | +0.3% | High-altitude regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

4G Coverage Expansion and Imminent 5G Pilots

Operators are densifying 4G sites to satisfy immediate capacity needs even as they finalize spectrum and financing plans for nationwide 5G. Nepal Telecom completed multi-province 5G trials but still weighs a Rs 50-60 billion capital requirement and unresolved frequency pricing, while the regulator stands ready to license commercial services within a week of fee settlement [1]Krishana Prasain, “Broadband internet extended to remote areas in 41 districts,” kathmandupost.com. Ncell’s strategic 3G shutdown frees spectrum for VoLTE and boosts data throughput without proportional tower additions. Targeted 5G rollout in Kathmandu Valley receives direct budgetary support, signaling public-private commitment to a phased deployment model that protects near-term returns and readies the Nepal Telecom MNO market for advanced enterprise applications. Infrastructure-sharing agreements under discussion can lift rural coverage economics, reducing cost per megabyte and supporting first-mover differentiation in service quality.

Surging Mobile Data Demand Fueled by Video and OTT Apps

Monthly data usage of 4 GB per SIM remains modest relative to regional peers, yet double-digit user growth in TikTok, YouTube, and localized OTT libraries is bending network traffic curves upward. QR-based payments now expand 230% per year, tying data demand directly to daily commerce rather than discretionary video streaming. The temporary TikTok ban wiped an estimated NPR 3 billion in annual operator revenue, illustrating both the upside and policy risk of content-centric business models. Digital wallets such as Khalti and IME Pay leverage data bundles as loyalty incentives, giving operators incremental average revenue per user while embedding them deeper into consumer transaction flows [2]Bipin Budhathoki, “Best Digital Wallets in Nepal: eSewa vs Khalti vs IME Pay (2025 Comparison),” bipinbudhathoki.com.np. Rising app sophistication heightens latency sensitivity, motivating subscribers to pay premiums for consistent throughput.

Digital Nepal Framework Subsidies for Rural Broadband

Universal-service levies have amassed more than NPR 10 billion, financing fiber backhaul and microwave hops that bring 41 districts onto broadband maps. Healthcare digitization across 2,481 facilities and distance-learning pilots in 72 schools anchor recurring traffic that improves project payback periods. Government capital offsets lower private risk, encouraging tower-sharing consortiums and opening the Nepal Telecom MNO market to community Wi-Fi cooperatives that buy wholesale bandwidth. By aligning subsidy disbursement with coverage obligations instead of technology mandates, policymakers create flexibility for operators to deploy cost-optimized radio mixes that fit terrain and density. Sustained annual budget allotments of NPR 7.72 billion to the ministry through 2026 provide planning certainty for multi-year rollouts. Resulting parity in rural access will widen the addressable base for enterprise IoT in agriculture and tourism.

Smartphone Penetration Surpassing 70% of Population

Smartphone adoption crosses 70% in 2025, sharply up from 62% in 2023, and catalyzes a platform leap from USSD to app ecosystems. Feature-phone users migrate to low-cost Android devices bundled with free data, expanding the Nepal Telecom MNO market beyond basic connectivity. VoLTE activation, supported by handset upgrades, improves call quality and spectrum efficiency, letting operators reclaim 3G bands for LTE. Agricultural apps such as GeoKrishi reach 51,000 farmers, validating mobile-first extension services that lock subscribers into data plans. Cross-border digital payment tie-ups with Indian and Chinese gateways could add further impetus as commerce volumes tick upward, reinforcing the device-driven data revenue flywheel.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory uncertainty on license renewal and foreign ownership | -0.8% | Nationwide | Medium term (2-4 years) |

| ARPU erosion from price wars and OTT substitution | -0.6% | Urban heavy | Short term (≤ 2 years) |

| Grid-power instability driving high network OPEX | -0.4% | Mountainous regions | Long term (≥ 4 years) |

| High telecom-specific taxes on data services | -0.3% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Uncertainty on License Renewal and Foreign Ownership

Foreign equity caps and opaque renewal terms amplify investment risk. Axiata’s 2024 exit from Ncell underlines how ownership constraints can push global operators to divest, trimming external know-how and capital inflows. Parliament’s recommendation to nationalize Ncell by 2029, concurrent with license expiry, clouds cash-flow forecasts and discourages multiyear 5G commitments [3]New Business Age Ltd., “Government to Take Control of Ncell's Assets after 5 Years,” newbusinessage.com. The Telecommunications Bill 2081 seeks to streamline renewal procedures and ease shareholding ceilings, yet final clauses remain pending, delaying certainty for network vendors and financiers. Heightened policy risk also tempers strategic interest from satellite entrants that might otherwise partner on rural broadband.

ARPU Erosion from Price Wars and OTT Substitution

Falling ARPU slices operator margins. Nepal Telecom’s FY 2023/24 revenue declined to NPR 42.11 billion, while nine-month profit plunged 48.6%, illustrating aggressive price discounting and OTT cannibalization [4]Nagarik Network, “Nepal Telecom's profit drops by 48.6 percent in first nine months of current FY,” myrepublica.nagariknetwork.com . Unlimited chat packs and cheap VoIP undermine international calling tariffs, historically a high-yield product. Both operators vie for subscribers in a saturated base, often swapping customers rather than adding new ones. OTT-fueled data-only plans shift revenue mix toward lower-margin gigabyte sales unless upsold with fintech or content bundles. Without sustained monetization innovation, price wars risk ratcheting down the Nepal Telecom MNO market growth below its forecast trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue Transformation

Data and internet services contribute 52.21% of Nepal Telecom MNO market revenue in 2025, reflecting the transition from legacy voice to high-bandwidth connectivity. Voice services continue to shrink against free OTT alternatives, while OTT and PayTV carve a niche among urban youth who binge-watch localized streaming. IoT and M2M post a 4.05% CAGR through 2031, propelled by agriculture sensor pilots and smart-city lighting projects that anchor enterprise demand. The Nepal Telecom MNO market size for data-centric offerings is projected to reach USD 357.2 million by 2031, representing more than half of total operator receipts. Operators buttress that outlook with VoLTE, Wi-Fi calling, and bundled cloud storage, broadening ticket sizes without massive infrastructure overhaul.

Innovative data pricing, such as social-media-only passes and zero-rating for mobile banking, helps offset the revenue lost from the TikTok ban and similar policy shocks. Ncell’s certification under stringent data-center directives reassures enterprise clients about information security, a prerequisite for lucrative cloud back-haul contracts. Nepal Telecom’s automated roaming launch in 2024 widens retail and business addressable bases across 75 partner networks, supporting upsell of travel data packs. Such multiproduct strategies diversify earnings and tether value to consumption rather than subscriber counts, keeping the Nepal Telecom MNO market resilient against saturation.

By End User: Enterprise Growth Outpaces Consumer Maturation

Consumer lines represent 92.01% of 2025 subscriptions but grow slowly as penetration tops 130%. Enterprises, in contrast, expand at a 4.92% CAGR through 2031 as banks, hotels, airlines, and government agencies digitize workflows in line with Digital Nepal Framework mandates. Nepal Telecom’s dedicated corporate broadband packages already clock 14,000 customers, while Ncell’s enterprise LTE private network trials target manufacturing clusters outside Kathmandu. The Nepal Telecom MNO market size accruing from enterprise solutions is forecast to reach USD 51.4 million by 2031, equal to 7.82% of total operator revenue.

Growth catalysts include the health sector’s telemedicine platform linking 2,481 facilities and tourism operators installing LTE Wi-Fi at lodges on the Everest Base Camp trail, where hourly Wi-Fi charges range from USD 5 to USD 12. Financial services provide another lift as mobile banking accounts hit 26.5 million, requiring encrypted, low-latency links to central clearing systems. Together, these use cases raise corporate willingness to pay for service-level agreements and managed security, sustaining margins in the Nepal Telecom MNO industry.

Geography Analysis

Kathmandu Valley anchors more than two-thirds of operator revenue in 2025, aided by dense population, 4G saturation, and imminent 5G launch backed by a specific budget line in the FY 2025/26 national appropriation. Average revenue per line in the valley is 1.4 times the national norm due to higher data and streaming appetite. The Nepal Telecom MNO market size tied to the valley is forecast to grow at a 3.32% CAGR as new apartment complexes adopt fiber-to-the-tower backhaul for internal Wi-Fi distribution.

The Terai belt, stretching along the Indian border, contributes significant prepaid volumes. Cross-border e-commerce flows spur demand for cheaper data bundles, while seasonal migrant workers rely on VoIP for remittances. Government-funded tower builds under the Digital Nepal Framework have lifted 4G coverage above 85% of the population in Terai districts, narrowing the urban-rural digital divide and enlarging the Nepal Telecom MNO market opportunity outside Kathmandu.

Mountainous provinces experience the most pronounced cost challenges. Grid unreliability pushes operators to diesel generators, adding NPR 7-10 per kilowatt-hour to site costs. Nonetheless, tourism corridors in Everest, Annapurna, and Langtang sustain premium Wi-Fi tariffs, which partly offset the capex load. The NPR 10.3 billion Karnali Tourism Master Plan earmarks spectrum-compatible infrastructure, signaling public funding alignment with private network rollouts that may yield a 5.78% CAGR for high-altitude segments through 2031.

Competitive Landscape

Nepal’s mobile ecosystem is a duopoly. Nepal Telecom leverages majority state ownership to win rural coverage subsidies and critical national backbone projects. Ncell, owned by Spectrlite UK since 2024, counters with speedier commercial execution and customer-experience innovations. Combined, the two firms control 100% of subscriptions, driving a concentrated but still contestable Nepal Telecom MNO market.

Strategic differentiation relies on network quality and vertical integration. Nepal Telecom leads 5G trials and is slated to spin off 30% equity to the public, aiming to enhance governance without shedding state influence. Ncell gains first-mover cachet by earning the country’s inaugural Tier III data-center certificate, raising its profile with fintech and e-governance clients. Both embrace tower-sharing talks to curb overlapping capex while jockeying for enterprise IoT contracts in agriculture and logistics.

Potential market disruption looms from satellite LEO entrants such as Starlink. Although regulatory debates on landing rights and user-terminal licensing are ongoing, the prospect of blanket rural coverage pressures the incumbents to accelerate quality upgrades. Meanwhile, the regulator contemplates incentivizing ISP mergers to cement backbone resilience, indirectly affecting mobile backhaul costs and reinforcing the competitive dynamics in the Nepal Telecom MNO market.

Nepal Telecom MNO Industry Leaders

Nepal Telecom

Ncell Axiata Limited (Spectrlite)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Ncell secures certification under Nepal’s new data-center directive, positioning the operator for government and enterprise hosting contracts.

- January 2025: The Nepal government unveils a plan to dilute its Nepal Telecom to about 61.53% by floating 30% shares to the public, targeting improved corporate governance.

- April 2024: Ncell expands 4G sites in Lumbini and Bagmati provinces, raising average downlink speeds in secondary cities.

Nepal Telecom MNO Market Report Scope

The report provides an in-depth analysis of the telecommunication industry in Nepal.

The market studied is segmented by service (voice services (wired, wireless), data and messaging services, and OTT and pay TV). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

End-user

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Nepal Telecom MNO market in 2026?

It stands at USD 545.11 million and is projected to reach USD 657.77 million by 2031 at a 3.83% CAGR.

Which service type leads operator revenue?

Data and internet services command 52.21% of total receipts in 2025, reflecting the pivot away from voice.

What is driving enterprise segment growth?

Government e-governance mandates and rising demand for secure, high-quality connectivity across finance, health, and tourism lift enterprise revenue at a 4.92% CAGR.

When will 5G become commercially available in Nepal?

Operators can receive licenses within weeks once spectrum fees are settled, with first launches planned for Kathmandu Valley under the FY 2025/26 budget.

How does smartphone adoption influence market dynamics?

With 70% of the population using smartphones in 2025, data-rich applications, digital wallets, and IoT solutions are boosting traffic and monetization opportunities.

What risks threaten operator profitability?

ARPU erosion from price wars and OTT substitution, plus regulatory uncertainty around license renewal and ownership caps, pose the main headwinds.

Page last updated on: