Switzerland Reinsurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

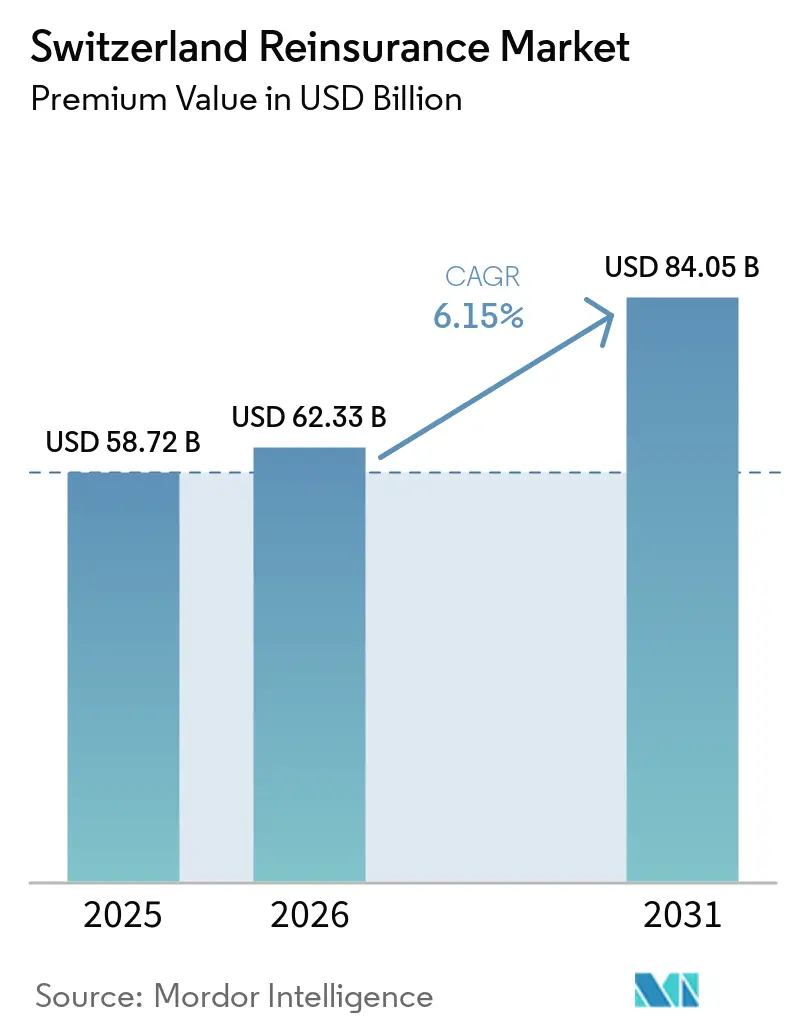

| Base Year Market Size (2025) | USD 58.72 Billion |

| Market Size (2026) | USD 62.33 Billion |

| Market Size (2031) | USD 84.05 Billion |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland Reinsurance Market Analysis by Mordor Intelligence

The Switzerland Reinsurance Market size in terms of premium value is expected to increase from USD 58.72 billion in 2025 to USD 62.33 billion in 2026 and reach USD 84.05 billion by 2031, growing at a CAGR of 6.15% over 2026-2031.

Demand is powered by climatically driven catastrophe losses, regulatory capital efficiencies under the Swiss Solvency Test (SST), and rising appetite for longevity-risk transfers from pension schemes. Swiss carriers pair deep modeling skills with ready access to capital-market instruments, allowing them to price complex risks such as cyber or secondary natural perils at premium levels. Digitalisation initiatives—including blockchain-enabled contracts and API-based distribution portals—compress operating costs and shorten underwriting cycles, further widening margins over continental peers. Scale advantages feed a virtuous loop: top players redeploy free cash to data analytics and climate-science research, reinforcing their leadership and raising entry barriers.

Key Report Takeaways

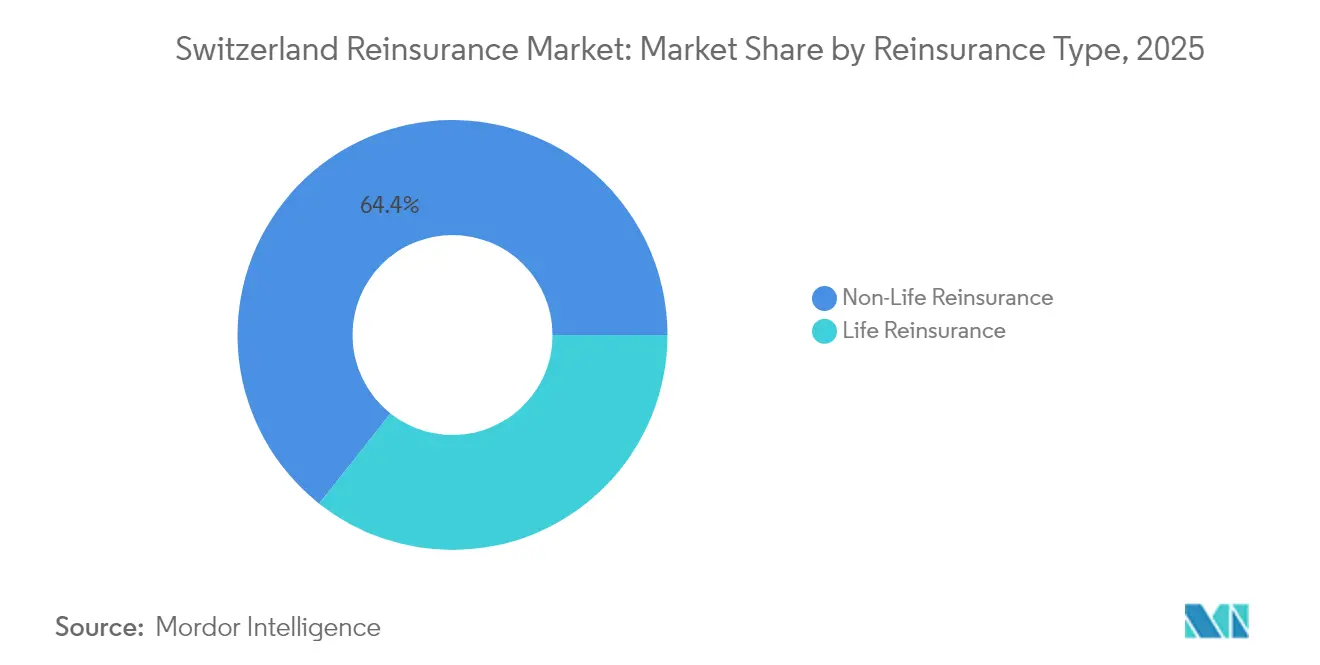

- By reinsurance class, Non-Life held 64.35% of Switzerland's reinsurance market share in 2025, while Life is projected to expand at a 6.78% CAGR to 2031.

- By treaty structure, Treaty business accounted for 70.74% share of the Switzerland reinsurance market size in 2025; Facultative lines are advancing at a 6.45% CAGR through 2031.

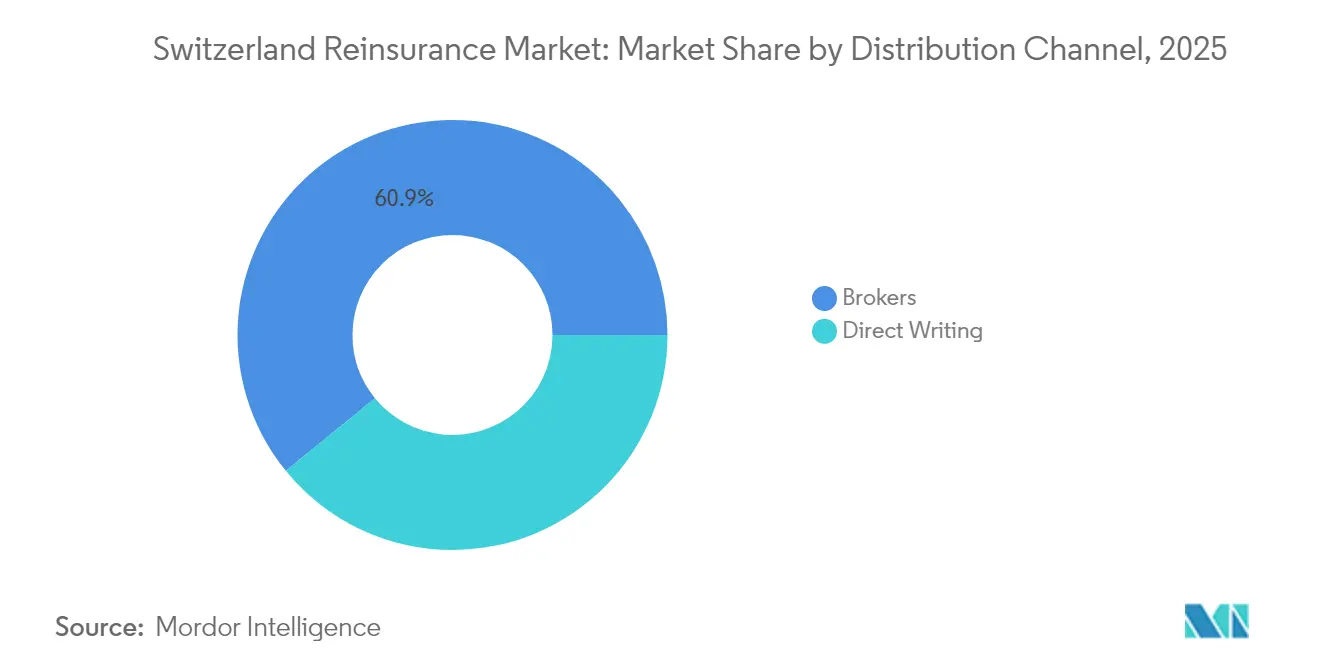

- By distribution channel, brokers led with 60.88% revenue share of the Switzerland reinsurance market in 2025, whereas direct writing is growing at a 6.60% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Switzerland contributes to a system defined not by any single country or region but by the interaction of many. The global reinsurance market data by Mordor Intelligence represents that combined structure.

Switzerland Reinsurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-change-driven catastrophe exposure | +1.8% | Global, concentrated in Europe & APAC | Long term (≥ 4 years) |

| Stricter SST / Solvency II capital rules | +1.2% | Switzerland and the European Union | Medium term (2-4 years) |

| Growth in longevity-risk transfer from pension funds | +0.9% | Switzerland, Germany, United Kingdom | Long term (≥ 4 years) |

| Rapid expansion of cyber-insurance requires reinsurance capacity | +1.1% | North America and Europe | Short term (≤ 2 years) |

| Parametric & blockchain-based reinsurance adoption | +0.7% | Switzerland, Singapore, and Bermuda hubs | Medium term (2-4 years) |

| ESG-linked reinsurance under Swiss Sustainable-Finance strategy | +0.5% | Switzerland, European Union | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Climate-Change-Driven Catastrophe Exposure

Swiss reinsurers are rewriting risk models as climate volatility converts once-seasonal perils into year-round threats. Insured natural-catastrophe losses topped USD 100 billion for five consecutive years through 2024, stressing legacy actuarial techniques [1]Financial Times, “Catastrophe Losses Surge Past USD 100 Billion for Fifth Year,” ft.com . The industry’s pivot toward secondary perils such as severe convective storms is notable: these events generated USD 64 billion of insured losses in 2024, much of it in European markets dominated by the Swiss group. To stay ahead, carriers are rolling out parametric covers linked to objective climate indices that trigger near-instant payouts, reducing loss-adjustment friction. This advisory-driven model deepens client stickiness by embedding reinsurers inside cedants’ catastrophe-planning cycles. The long-run implication is a predictable revenue stream tied to climate analytics rather than purely to underwriting margins.

Stricter SST / Solvency II Capital Rules

Regulatory frameworks once deemed burdensome are now competitive weapons. FINMA’s SST obliges firms to stress-test capital adequacy over a one-year horizon, rewarding those with sophisticated balance-sheet analytics. Swiss carriers translate these modelling investments into premium uplifts, as evidenced by Zurich Insurance Group’s 256% SST ratio in Q1 2025—well above local minima—and position themselves as safe counter-parties for global cedants [2]Zurich Insurance Group, “Q1 2025 Financial Update,” zurich.com . Meanwhile, the 2025 Solvency II review introduces macroprudential overlays that smaller rivals may find costly to implement, reinforcing the Swiss incumbents’ scale advantage. Lower capital-charge calibrations on longevity and equity risks also free surplus that can be redeployed toward longer-duration assets. The combined effect increases underwriting capacity while sustaining shareholder returns.

Growth in Longevity-Risk Transfer from Pension Funds

Longevity reinsurance has moved centre-stage as ageing demographics challenge pension solvency. Funded ratios for Swiss pension schemes reached 125.5% in Q1 2025 thanks to higher bond yields, prompting sponsors to lock in gains by offloading future longevity exposure. Reinsurers bundle biometric modelling with asset-liability management, offering turnkey solutions that satisfy both solvency and investment mandates. Healthy-ageing incentives embedded in newer contracts align participant wellness with insurer profitability, innovating beyond plain mortality swaps. Swiss expertise is now exported to rapidly ageing APAC and EU markets, extending revenue footprints worldwide.

Rapid Expansion of Cyber-Insurance Requiring Reinsurance Capacity

Cyber premiums are on a steep ascent, rising from infancy to an expected USD 16.6 billion globally by 2025, highlighting a vast protection gap. Capacity shortfalls have pushed Swiss reinsurers to pioneer cyber catastrophe bonds and proportional quota-shares that lure alternative investors. Data-sharing partnerships with cedants enhance loss-frequency models, enabling more precise pricing of ransomware and cloud-outage exposures. Parametric cyber triggers, based on aggregate-loss indices, mitigate ambiguity in attribution and speed up claims settlement. Short-term demand is concentrated in North America and Europe, but regulatory mandates in Asia suggest imminent spillover.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent low/negative yields on CHF assets | -1.4% | Switzerland & euro-linked books | Medium term (2-4 years) |

| Competition from ILS & other alternative capital | -0.8% | Global catastrophe zones | Short term (≤ 2 years) |

| High claims volatility from secondary perils | -1.1% | Europe, North America, and emerging APAC | Long term (≥ 4 years) |

| Swiss-franc appreciation squeezing price competitiveness | -0.9% | Global operations priced in non-CHF currencies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Low/Negative Yields on CHF Assets

The Swiss National Bank cut policy rates back to 0.50% in late 2024 and is guiding markets toward possible negative territory in 2025, pressuring investment returns [3]Fitch Solutions, “Switzerland Monetary Policy Outlook 2025,” fitchsolutions.com. Technical reserves denominated in CHF now earn razor-thin yields, forcing reinsurers to reweight toward illiquid private-credit or infrastructure assets. Currency appreciation compounds the problem by trimming export-priced premium flows and fanning deflation risks. Although diversification into foreign-currency assets offers yield relief, hedging costs can erode net spreads. Consequently, reinsurers raise underwriting prices or structure profit-sharing clauses to protect ROE in a low-rate regime.

Competition from ILS & Other Alternative Capital

Insurance-linked securities capital hit a record USD 107 billion at end-2024, giving cedants direct access to markets and squeezing traditional reinsurer margins [4]Global Reinsurance, “ILS Capital Reaches Record USD 107 Billion,” globalreinsurance.com . Investors prize parametric triggers and transparent loss definitions, attributes that standard reinsurance contracts have started emulating. Swiss Re’s co-management of GAM’s catastrophe-bond funds demonstrates incumbents’ shift from competitors to facilitators of ILS inflows. Yet, multi-year ILS capacity locks in rates earlier, limiting reinsurers’ ability to adjust prices post-event. To stay relevant, Swiss carriers now blend treaty expertise with capital-market execution, offering hybrid covers that share risk and fee income.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Reinsurance Type: Life Segment Accelerates Growth

Life business accounted for 35.65% of the 2025 premium but is forecast to rise faster than Non-Life, posting a 6.78% CAGR while the Switzerland reinsurance market expands at 6.15% overall. Heightened demand stems from pension funds hedging longevity risk as population ageing quickens across Europe and OECD economies. Higher interest rates also lift life insurers’ investment income, freeing budget to cede biometric risks. Conversely, Non-Life retains volume leadership owing to climate-driven property claims and rising asset values, but faces margin compression amid growing alternative capital. Swiss expertise in mortality modelling and cross-border regulation positions local carriers to capture longevity mandates in Germany, the UK, and Japan.

The Non-Life segment sustains its cash flow by leveraging property-catastrophe treaties and advanced coverage solutions in cyber, marine, and energy markets. Swiss reinsurers integrate real-time climate analytics to optimize aggregate limits, ensuring the protection of combined ratios and enhancing operational efficiency. Regulatory capital credits associated with longevity transactions improve return profiles, fostering the development of innovative offerings such as wellness-linked annuity hedges. This strategic approach reflects a focus on balancing risk and profitability while addressing evolving market demands. With competitive dynamics favoring growth, Life reinsurance is anticipated to emerge as the primary contributor to earnings expansion over the medium term.

By Treaty Type: Facultative Share Expands

Treaty contracts deliver efficiency through portfolio aggregation and thus represented 70.74% of premium in 2025; however, the Facultative business is set to outpace with a 6.45% CAGR to 2031. As insureds confront novel exposures—particularly cyber, environmental liability, and supply-chain interruption—they seek coverage terms beyond standard treaties. Facultative placements allow cedants to tailor sub-limits and triggers, commanding higher pricing multiples that bolster reinsurer margins. Swiss carriers have digitalised submission workflows, slashing quote-turnaround times from weeks to hours for complex facultative deals. That speed advantage reinforces client loyalty in specialty-line corridors.

Treaty income still underwrites the bulk of capacity in property-catastrophe and motor-quota shares, acting as a stable funding source for facultative risk experimentation. Artificial-intelligence triage of submissions frees underwriters to focus on bespoke deals with superior spreads. Swiss reinsurers’ capital-markets arms further enhance facultative offerings by embedding parametric add-ons financed by ILS investors. Market signals point to a balanced dual-model strategy where treaty portfolios fund facultative innovation.

By Distribution Channel: Direct Writing Gains Momentum

Brokers controlled 60.88% of premiums in 2025, reflecting their indispensable role in complex multi-cedant placements, yet direct writing is expected to achieve a 6.60% CAGR to 2031. Technology platforms enable cedants to tap reinsurer capacity through APIs that automate rating and documentation, slicing intermediation costs. Early adoption occurs in standardised quota-share and parametric contracts where loss-adjustment subjectivity is minimal. Swiss reinsurers simultaneously strengthen broker ties by co-creating analytic dashboards that deepen client engagement, preserving commissions on bespoke risks. The hybrid model balances cost efficiency with relationship depth across the product spectrum.

Brokers are expected to retain their leadership in multi-jurisdictional catastrophe and aviation placements due to their extensive global networks and strong negotiation capabilities. In contrast, digital portals are transforming the market by enabling smaller cedants to independently access top-rated reinsurers, a capability historically reserved for larger carriers. The data collected through these portals is being utilized to enhance underwriting algorithms and streamline product development processes. This evolution in distribution channels is equipping reinsurers with more comprehensive insights into cedant behavior, enabling better evaluation of portfolio quality. Consequently, the shift is reshaping traditional dynamics and fostering a more data-driven approach to reinsurance operations.

Geography Analysis

Swiss domestic premium benefits from the nation’s status as a global financial sanctuary, even though local cedants are modest in scale. FINMA’s openness to insurance-linked securities, coupled with ESG integration policies, ensures that Switzerland's reinsurance market remains a magnet for foreign sponsors seeking regulatory certainty. The strong franc, while dampening cost competitiveness for exports, bolsters reinsurers’ balance-sheet strength during global volatility, attracting flight-to-quality capital. Domestic market share concentration mirrors global rankings because parent groups book a substantial offshore premium through Swiss entities.

Regional catastrophe events—particularly severe convective storms—inject growth momentum into property programs. Swiss reinsurers embed parametric triggers to manage basis risk, differentiating their offerings from local rivals. Regulatory convergence under Solvency II eases passporting, enabling Swiss giants to bundle EU cover with global retrocession lines for cedants. The result is a dominant European footprint complemented by rising specialty-line penetration.

Beyond Europe, Asia-Pacific provides breakout potential, driven by low insurance penetration and regulatory mandates for cyber coverage in markets such as Singapore and China. Swiss carriers leverage treaty-plus-facultative structures to transfer typhoon, earthquake, and flood exposures into the capital markets. Local partnerships with national reinsurers offer distribution while preserving control over underwriting standards. Latin America and the Middle East also surface as growth pockets for energy and parametric drought products. Geographic diversification thus mitigates Swiss exposure to European economic cycles and broadens revenue resiliency.

The reinsurance market is analyzed by Mordor Intelligence across multiple other geographies. This is complemented by country-specific insights for Germany, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The Switzerland reinsurance market operates as an oligopoly, with the top five groups commanding a significant share of premiums and strategically allocating surplus funds toward advancements in next-generation risk analytics. Swiss Re posted USD 3.2 billion net income and 15% ROE for 2024, underscoring the profitability scale that empowers. Munich Re, SCOR, and Hannover Re follow suit with double-digit returns, supported by disciplined underwriting and alternative-capital partnerships. High barriers—a mix of regulatory capital floors, actuarial talent pools, and data infrastructure—deter new entrants and steer competition toward innovation rather than price wars.

Technology is the main battleground. Carriers deploy artificial-intelligence underwriting engines, blockchain claims protocols, and climate-data satellites to sharpen risk selection. SCOR’s Quantum Leap program exemplifies this digital pivot, targeting process automation and real-time portfolio steering. Swiss Re’s tie-up with GAM’s catastrophe-bond funds signals strategic realignment: incumbents aim to become conduits for alternative capital, earning fee income while preserving underwriting authority. Smaller reinsurers carve niches in aerospace, fine art or credit surety, areas where deep specialty knowledge offsets lack of scale.

Strategic deals illustrate the consolidation trend. Helvetia and Baloise merged in April 2025, forming Europe’s tenth-largest primary insurer and potential future cedant of scale. Zurich Insurance Group's robust 24.6% ROE and strong SST ratio provide the financial flexibility to pursue strategic bolt-on acquisitions or invest in greenfield digital initiatives. Everest Group’s reserve addition shows prudent responses to social-inflation trends, maintaining investor confidence even amid profit dips. Overall, competitive dynamics prioritise capital stewardship and tech-driven efficiency over traditional market-share grabs.

Switzerland Reinsurance Industry Leaders

Swiss Re

PartnerRe

SCOR Switzerland

Arch Re Europe

Munich Re

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Zurich's Property and Casualty business reported a 5% increase in insurance revenue and gross written premiums for Q1 2025, with its Swiss Solvency Test ratio improving to 256%, underscoring geographic and product-line expansion momentum.

- April 2025: Helvetia Holding and Baloise Holding will merge to form Helvetia Baloise Holding, becoming Switzerland's second-largest insurance group by business volume and the sector's largest employer. The new entity will hold a 20% market share in Switzerland and maintain strong positions in European markets.

- April 2025: Swiss Re, through its subsidiary Swiss Re Insurance-Linked Investment Advisors Corporation ("SRILIAC"), will assume the role of co-investment manager for GAM's portfolio of insurance-linked security (ILS) funds, including the GAM Star Cat Bond UCITS Fund.

- February 2025: SCOR reported sustained growth in preferred lines with attractive margins during the January 2025 P&C reinsurance renewals, signalling expansion into specialty segments with new treaty structures.

Switzerland Reinsurance Market Report Scope

Reinsurance is a practice where insurance companies transfer some portion of their risk portfolio to another party; these parties are called reinsurers. The Switzerland reinsurance market is segmented by type, application, by distribution channel, and mode. By type, the market is further segmented into facultative reinsurance & treaty reinsurance. By application, the market is further segmented into property & casualty reinsurance and life & health reinsurance. By distribution channel, the market is further segmented into direct and broker. And by mode, the market is further segmented into online and offline.

The report offers market size and forecasts for the Switzerland reinsurance market in value (USD) for all the above segments.

| Life Reinsurance |

| Non-Life Reinsurance |

| Treaty Reinsurance |

| Facultative Reinsurance |

| Direct Writing |

| Brokers / Intermediaries |

| By Reinsurance Type | Life Reinsurance |

| Non-Life Reinsurance | |

| By Treaty Type | Treaty Reinsurance |

| Facultative Reinsurance | |

| By Distribution Channel | Direct Writing |

| Brokers / Intermediaries |

Key Questions Answered in the Report

What annual growth rate is expected for the Switzerland Reinsurance Market through 2031?

The market is projected to expand at a 6.15% compound annual growth rate, rising from USD 58.72 billion in 2025 to USD 84.05 billion by 2031.

Which business line is growing fastest within the Switzerland Reinsurance Market?

Life reinsurance leads growth with a 6.78% forecast CAGR, driven by rising longevity-risk transfers from pension funds.

How large could the Life reinsurance segment become by 2031?

By 2031, life placements are anticipated to constitute approximately two-thirds of the total market premium, reflecting a significant share of the market's overall value.

How concentrated is the Switzerland reinsurance market?

The reinsurance market exhibits a high level of concentration, with the top five reinsurers accounting for a substantial portion of premiums, leading to an elevated market-concentration score.

What role does climate change play in Swiss reinsurance demand?

Persistent natural-catastrophe losses above USD 100 billion annually and USD 64 billion in secondary-peril losses during 2024 are pushing cedants toward Swiss reinsurers’ parametric and analytics-driven solutions.

How are Swiss reinsurers meeting surging cyber-insurance capacity needs?

They are structuring cyber catastrophe bonds, parametric quota shares and data-sharing partnerships that attract alternative investors and widen available capacity for cedants.

Page last updated on: