Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

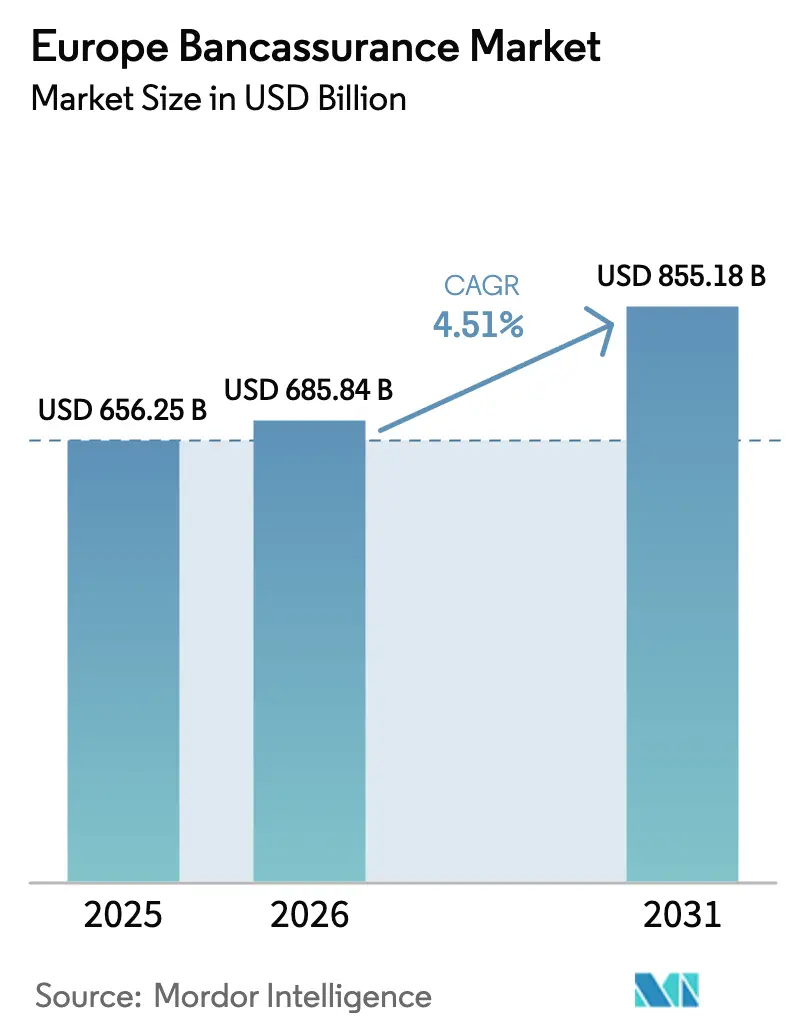

| Base Year Market Size (2025) | USD 656.25 Billion |

| Market Size (2026) | USD 685.84 Billion |

| Market Size (2031) | USD 855.18 Billion |

| Growth Rate (2026 - 2031) | 4.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Bancassurance Market Analysis by Mordor Intelligence

The Europe Bancassurance market size is expected to grow from USD 656.25 billion in 2025 to USD 685.84 billion in 2026 and is forecast to reach USD 855.18 billion by 2031 at 4.51% CAGR over 2026-2031. Growing capital efficiency unlocked by the Danish Compromise and CRR3 reforms lets banks hold insurance subsidiaries with lower risk-weighting, strengthening Common Equity Tier 1 ratios and encouraging deeper insurance integration. Life policies preserve their role as core revenue drivers, while demand for private health coverage accelerates on the back of aging populations and stretched public healthcare. Digital migration continues to reshape distribution as mobile apps embed instant policy issuance inside everyday banking journeys. Meanwhile, artificial intelligence (AI) adoption enables banks and insurers to personalize offers in real-time, reinforce cross-sell ratios, and lower servicing costs. Competitive differentiation, therefore, tilts toward institutions that combine strong capital positions, omnichannel reach, and data-driven underwriting.

Key Report Takeaways

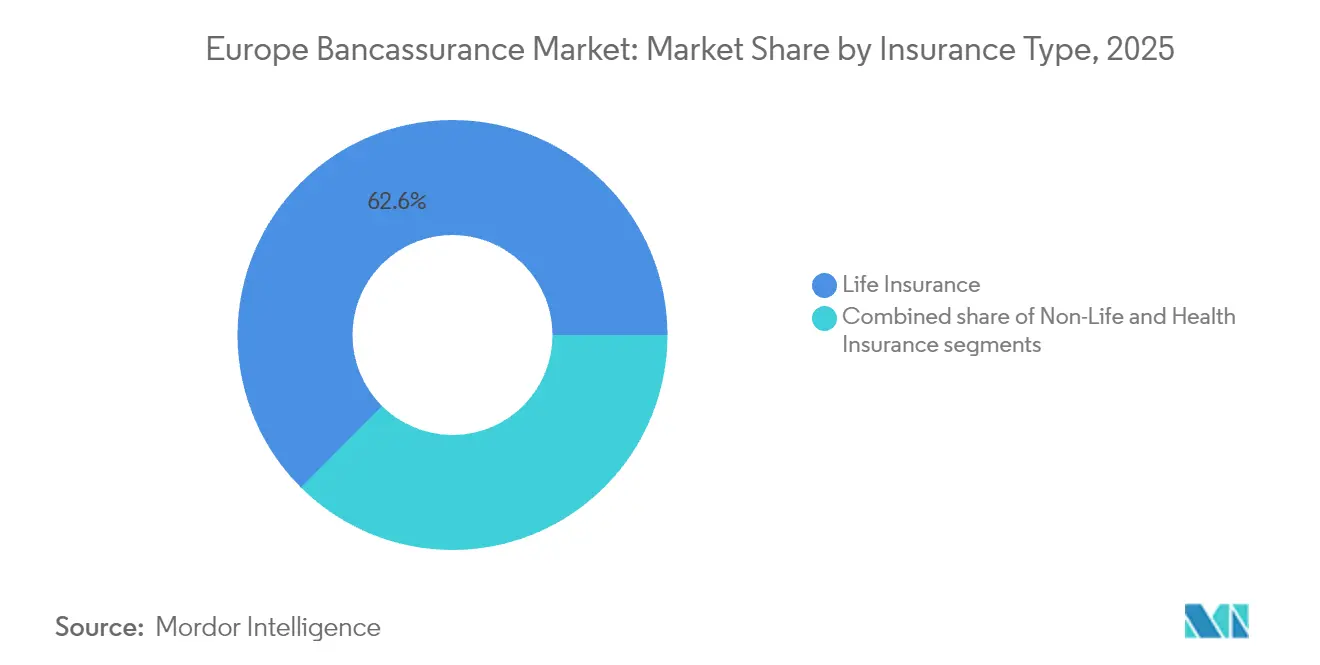

- By insurance type, life products held 62.55% of the Europe Bancassurance market share in 2025; health insurance is poised to grow at a 6.52% CAGR by 2031.

- By distribution channel, bank branches retained 67.75% revenue share in 2025, whereas mobile banking apps are projected to expand at an 8.10% CAGR through 2031.

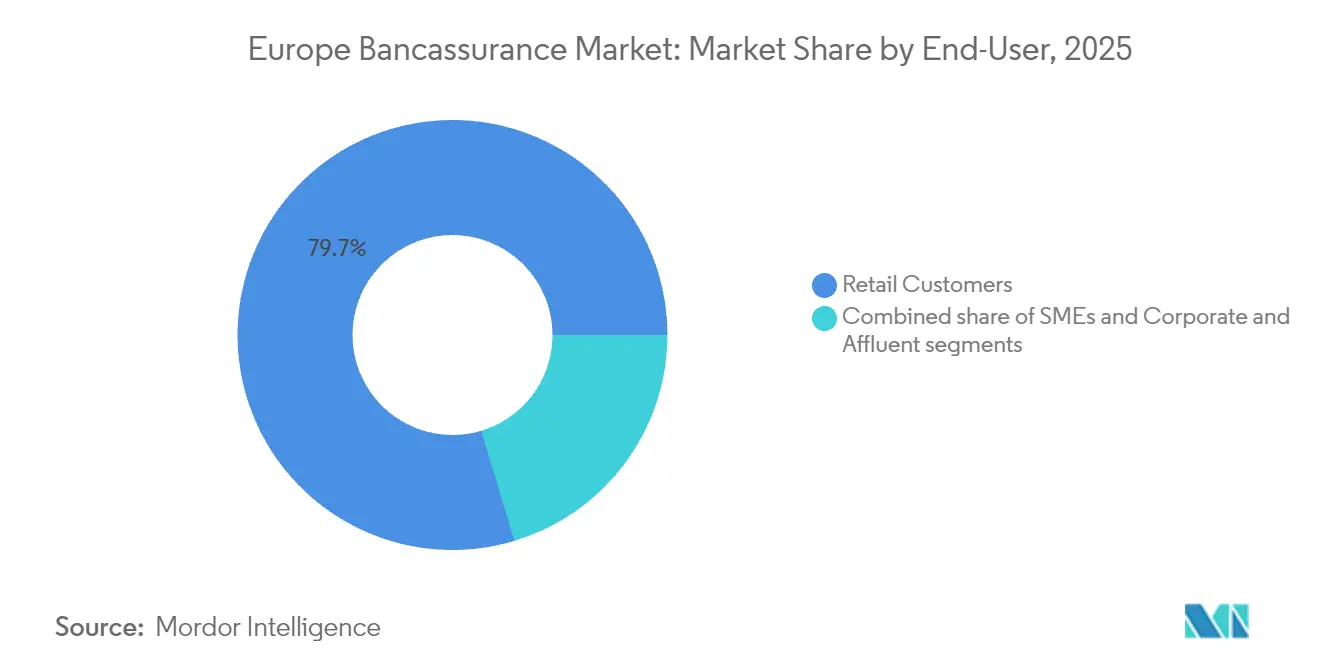

- By end-user, retail clients accounted for 79.65% of the Europe Bancassurance market size in 2025; the SME segment is expected to post the fastest rise with a 6.85% CAGR by 2031.

- By geography, France dominated with a 17.25% revenue share in 2025, while Poland is forecast to record a 7.55% CAGR, the highest in the region through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Bancassurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for retirement & protection products | +1.2% | Western Europe, particularly France and Germany | Long term (≥ 4 years) |

| Banks’ search for fee-based income amid NIM pressure | +0.8% | Mature European markets | Medium term (2-4 years) |

| Surge in digital channel adoption & data-driven cross-sell | +1.0% | Northern Europe, spreading to CEE | Short term (≤ 2 years) |

| Ageing branch networks leverage embedded advisory tools | +0.6% | Rural and suburban areas | Medium term (2-4 years) |

| Capital relief from Danish Compromise & CRR3 reforms | +0.7% | EU member states with sizeable banking sectors | Short term (≤ 2 years) |

| AI-powered hyper-personalisation via open-banking data | +0.9% | UK, Netherlands, Nordics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Retirement & Protection Products

Europe’s demographic shift magnifies the funding gap of statutory pension schemes and moves households toward private retirement savings vehicles. Swiss Re estimates an additional USD 1.56 trillion in life-premium potential between 2025 and 2034, creating sizable room for banks to deepen advisory-led sales of whole-life and annuity products[1]Swiss Re, “European Life Insurance Premium Potential,” swissre.com. Rising policyholder yields of 3.5% on traditional euro funds in 2025 make life contracts competitive versus deposits, boosting take-up among risk-averse savers. Banks utilize their account-level insights to bundle protection covers alongside personal loans and mortgages, thereby widening fee streams and strengthening customer stickiness. Countries with mature social security systems, such as France and Germany, show the strongest pivot to individual pension plans, a trend expected to persist throughout the decade.

Banks’ Search for Fee-Based Income Amid NIM Pressure

Competitive lending practices and uncertainties in macro-policy continue to constrain net interest margins (NIMs). By distributing insurance, banks can generate stable, capital-light fees, helping to offset the volatility in lending. This strategy diversifies revenue streams and reduces reliance on interest-based income, making banks more resilient to market fluctuations. A recent policy change, reducing the risk weight for insurance participation to 250%, has directly boosted returns on equity for integrated bancassurers. This regulatory adjustment enhances the attractiveness of bancassurance models, encouraging banks to forge tighter exclusivity agreements with their in-house or captive insurers to maximize collaboration. As a result, bank executives are now focusing on optimizing their product mix, with a target of elevating the share of non-interest income to over 40% by 2030, particularly among major groups in Western Europe. This shift reflects a broader trend of banks seeking to balance their income portfolios and adapt to evolving market dynamics[2]Crédit Agricole Assurances, “2024 Registration Document,” credit-agricole.com.

Surge in Digital Channel Adoption & Data-Driven Cross-Sell

In the wake of the pandemic, consumer habits have increasingly gravitated towards mobile platforms. Notably, 80% of retail banking clients now express a willingness to buy insurance directly through their banking apps. This shift highlights the growing importance of mobile channels in the Europe bancassurance market, where mobile distribution is experiencing significant growth with an 8.31% CAGR. This expansion is driven by the convenience of instant policy issuance and the effectiveness of tailored offers in improving conversion rates. Banks are capitalizing on transaction data to deliver hyper-personalized nudges, for instance, offering travel insurance immediately after a ticket purchase. Such strategies enhance customer engagement and streamline the insurance purchasing process. In the Nordic region, banks have already linked over 25% of new non-life policies to app-driven processes, demonstrating the scalability and efficiency of these embedded models. This trend underscores the transformative potential of mobile distribution in reshaping the bancassurance landscape.

AI-Powered Hyper-Personalisation via Open-Banking Data

The European Insurance and Occupational Pensions Authority (EIOPA) reports that 50% of non-life and 24% of life insurers had deployed AI solutions by 2024, chiefly in underwriting and claims[3]EIOPA, “Digitalisation Market Monitoring Report,” eiopa.europa.eu. With the help of open-banking interfaces, insurers can now access detailed cash-flow data, enhancing their underwriting processes. This advancement enables them to refine risk assessments and transition towards usage-based pricing models. Generali Switzerland has introduced an AI-driven assistant that addresses queries in multiple languages and streamlines basic claims processes. This innovation has boosted customer satisfaction scores by 12 points within its inaugural year. Furthermore, as machine-learning technologies evolve, there is a noticeable uptick in conversion rates for in-app insurance offers, resulting in acquisition costs that are now more economical than traditional branch or call-center methods.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented EU regulatory & tax rules | -0.5% | Cross-border operations | Long term (≥ 4 years) |

| Shrinking in-branch footfall post-COVID | -0.7% | Markets with dense branch networks | Medium term (2-4 years) |

| GDPR-driven limits on deep consumer-data mining | -0.4% | EU-wide | Short term (≤ 2 years) |

| BigTech / FinTech ecosystems disintermediating banks | -0.6% | UK, Netherlands, Nordics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented EU Regulatory & Tax Rules

Divergent national tax incentives, disclosure obligations, and product labeling raise compliance costs for pan-European bancassurers. Maintaining parallel product shells and IT configurations for each market erodes scale economics and slows time-to-market. Smaller cross-border entrants face heavier proportional burdens, effectively shielding dominant domestic bancassurers from aggressive competition. Progress on a truly harmonized European Insurance Single Market, therefore, remains pivotal to unlocking further growth. A harmonized regime would reduce regulatory friction, enabling firms to distribute standardized products across borders with greater efficiency. It would also enhance consumer confidence through consistent protections and disclosures, fostering deeper integration of the European insurance landscape.

BigTech / FinTech Ecosystems Disintermediating Banks

Digital ecosystems are seamlessly integrating payments, investments, and insurance into user-friendly interfaces. For example, Revolut now offers device and travel insurance directly through its app to over 30 million customers in Europe, sidestepping traditional banking routes and providing a more convenient alternative to traditional methods. Major tech companies utilize advanced engagement analytics to provide tailored micro-insurance at crucial moments, such as during travel bookings or device purchases, appealing to younger, urban clients who might have turned to traditional bank-centric insurers. This trend is pushing established banks to hasten their innovation efforts, adopt digital-first strategies, and enhance customer experiences to protect their market share in an increasingly competitive landscape.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Health Insurance Drives Premium Growth

Life products occupied 62.55% of the Europe Bancassurance market share in 2025, cementing their status as the largest revenue stream. Health lines are, however, growing faster at 6.52% CAGR as aging populations, lengthy public-sector waiting lists, and pandemic-induced awareness redirect households toward supplementary cover. For 2026-2031, the health segment is projected to add USD 27.4 billion in incremental premiums, equivalent to almost one-fifth of total market expansion. AXA’s blueprint illustrates the pivot: its European health portfolio achieved a 9% premium rise in 2024 and now targets an even split between retail and commercial lives covered.

Digital wellness platforms reinforce this momentum by bundling telemedicine and preventive-care services with insurance, building recurring engagement, and lowering claims ratios. Non-life products such as property and motor continue to benefit from bancassurers’ lending relationships. Mortgage origination offers natural cross-sell opportunities for home insurance, while auto loans anchor motor policy propositions. Although these sublines grow more slowly than health, their profit margins remain attractive due to low acquisition costs and bundled sales.

By Distribution Channel: Mobile Apps Challenge Branch Dominance

Bank branches still controlled 67.75% of written premiums in 2025, owing to deep customer relationships and in-person advisory comfort. Yet the Europe Bancassurance market size attributable to mobile channels is forecast to triple by 2031 on an 8.10% CAGR as consumers shift toward digital self-service. Embedded journeys cut onboarding to minutes and support pay-as-you-go covers, appealing to younger demographics who rarely visit branches. Insurtech enabler Qover embeds policies directly inside Revolut’s and N26’s banking apps, demonstrating a low-cost, pan-European rollout path.

Mid-single-digit shares of contact centers and web portals cater to intricate product demands and facilitate assisted sales. These channels play a crucial role in addressing customer needs that require personalized attention or detailed explanations, especially for complex insurance products. With the growing integration of AI in voice bots, it's projected that by 2027, these bots will handle 50% of inbound insurance inquiries. This automation is expected to streamline operations, reduce response times, and improve efficiency, enabling human agents to dedicate their time to providing more valuable and specialized advisory services, such as tailored policy recommendations and addressing unique customer concerns.

By End-User: SMEs Emerge as High-Growth Segment

Retail customers generated 79.65% of the Europe Bancassurance market size in 2025, reflecting a long-standing consumer focus. SMEs, though smaller at present, are on track to grow at 6.85% CAGR as regulatory requirements such as professional indemnity compel businesses to protect against operational risks. Banks already supplying credit lines can easily bundle property, liability, and key-person covers, lifting overall relationship profitability. The Europe Bancassurance market size for SME lines is projected to top USD 62.8 billion by 2031 if current growth rates persist.

While large corporations and affluent individuals continue to play a pivotal role in single-premium life and legacy wealth-transfer products, their growth is outpaced by SMEs and the mass affluent. It is largely due to already high penetration levels among blue-chip employers and high-net-worth individuals, which limits the potential for further expansion. In contrast, SMEs and the mass-affluent segments present untapped opportunities, driving faster growth in these categories as they increasingly adopt such financial products. Additionally, the evolving financial needs of SMEs and the growing awareness among the mass affluent about wealth management solutions contribute to the accelerated adoption of these products in these segments.

Geography Analysis

In 2025, France emerged as the dominant force in the European Bancassurance market, accounting for 17.25% of total premiums. This leadership is bolstered by enduring partnerships like Crédit Agricole/Predica and Société Générale/Sogecap. Life policies, enjoying favorable tax treatments, are integral to household savings in France, ensuring steady inflows even during economic downturns. The strong cultural acceptance of life insurance as a savings tool further reinforces France's position, making it a cornerstone of the European Bancassurance market.

Southern Europe, led by Italy and Spain, follows closely. These nations are reaping the rewards of consolidating banking sectors that rely on fee revenues for earnings stability. As households seek safeguards against economic uncertainties, life and credit-linked insurance are gaining traction. Italy's bancassurance market benefits from a well-integrated banking and insurance ecosystem, while Spain's focus on digital transformation is enhancing customer engagement and product accessibility. Germany, while a significant player, experiences a more tempered evolution. Its fragmented savings-bank structures and intricate regulatory landscape slow down the rapid expansion of bancassurance. However, with rising digital adoption and ongoing pension reform discussions, Germany sees potential for accelerated growth post-2026. The increasing awareness of retirement planning and the gradual shift toward digital platforms are expected to play a pivotal role in shaping Germany's bancassurance landscape.

Central and Eastern Europe are witnessing the swiftest growth rates. Poland leads the pack, boasting a 7.55% CAGR projected through 2031. Rising disposable incomes, a burgeoning mortgage market, and a notable protection gap fuel this growth. In 2025, Poland's bancassurance market recorded gross written premiums of USD 1.54 billion, marking a 3% increase from the previous year. Mobile-first banks are at the forefront of customer acquisition, with Revolut notably onboarding 4.5 million users in Poland and expanding their offerings to include device and travel covers. The region's growth is further supported by increasing financial literacy and government initiatives aimed at promoting insurance penetration.

The Netherlands and Nordic countries are emerging as digital innovation hubs. Here, open-banking APIs and national e-ID initiatives are streamlining instant policy issuance. These advancements are fostering a seamless customer experience, making insurance products more accessible and appealing. Switzerland's banking model, with its emphasis on wealth, is driving demand for high-value life and investment-linked contracts. The country's strong economic stability and affluent customer base provide a conducive environment for the growth of bancassurance. Belgium and Portugal, on the other hand, are enjoying steady mid-single-digit growth due to stable household savings rates. Elsewhere in Europe, while there is a collective movement towards EU prudential standards and a promise of economic modernization, the journey is moderated by regulatory fragmentation. The harmonization of regulations across the region remains a challenge, but ongoing efforts to address these disparities are expected to unlock further growth opportunities in the long term.

Competitive Landscape

The market structure is moderately concentrated. The top five players, Crédit Agricole Assurances, BNP Paribas Cardif, CaixaBank / SegurCaixa Adeslas, Intesa Sanpaolo Vita, and CNP Assurances collectively held half of 2024 premiums. Each operates an integrated bancassurance model that locks in proprietary distribution, generates diversified fee flows, and supports balance-sheet funding via predictable cash generation. Crédit Agricole, for instance, reported USD 45.41 billion in insurance revenue during 2024, underscoring the scale that captive bancassurance delivers.

Digital innovation is the primary competitive lever. By 2024, 50% of non-life insurers had rolled out AI underwriting modules, trimming average claims-handling time by 20% and improving loss ratios by up to 3 percentage points. BNP Paribas Cardif partnered with Plug-and-Play’s insurtech accelerator to source AI solutions for medical risk scoring, accelerating product development cycles. CNP Assurances focused on modular APIs that allow partners such as La Banque Postale to tailor pricing logic to specific customer segments.

Strategic partnerships are broadening the landscape. Belfius teamed up with health-insurance Alan and language-model developer Mistral AI to develop an AI-assisted medical network, signaling that traditional bancassurers want to own wellness ecosystems rather than just underwrite risk. At the same time, embedded-insurance specialists such as Wefox and Element court neobanks and e-commerce platforms threaten disintermediation. Incumbents respond by opening innovation labs, investing in venture funds, and selectively acquiring niche underwriters to reinforce capabilities.

Europe Bancassurance Industry Leaders

Crédit Agricole Assurances

BNP Paribas Cardif

CaixaBank / SegurCaixa Adeslas

Intesa Sanpaolo Vita

CNP Assurances

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Allianz, BlackRock, and T&D Holdings closed the USD 3.78 billion acquisition of Viridium Group, expanding their closed-end portfolio management scale in Germany.

- April 2025: Helvetia and Baloise unveiled merger plans that would create a leading Swiss composite insurer.

- January 2025: CNP Assurances and La Mutuelle Générale launched CNP Assurances Protection Sociale with an expected premium income above USD 937 million.

- November 2024: AXA Switzerland debuted addProtect, a digital bancassurance suite built on Additiv’s platform.

Europe Bancassurance Market Report Scope

Bancassurance refers to a collaborative setup between a bank and an insurance company, enabling the latter to offer its products to the bank's clientele. This report aims to provide a detailed analysis of the European bancassurance market. It focuses on the market dynamics, emerging trends in the segments and regional markets, and insights on the different types, along with key developments. The report also analyses the key players and the competitive landscape in the market.

The European bancassurance market is segmented by type of insurance and geography. By type of insurance, the market is further segmented into life insurance and non-life insurance. By geography, the market is further segmented into France, Italy, Germany, the United Kingdom, Finland, and the Rest of Europe. The report offers market size and forecasts for the bancassurance market in Europe in terms of value (USD) for all the above segments.

By Insurance Type

| Life Insurance |

| Non-Life Insurance |

| Health Insurance |

By Distribution Channel

| Bank Branch |

| Digital / Online Banking |

| Mobile Banking Apps |

| Contact-Centre / Phone |

| Affinity & Embedded (FinTech / Retail) |

By End-User

| Retail Customers |

| Small & Medium Enterprises (SMEs) |

| Corporate & Affluent |

By Country

| France |

| Italy |

| Spain |

| Germany |

| United Kingdom |

| Portugal |

| Belgium |

| Poland |

| Netherlands |

| Switzerland |

| Rest of Europe |

| By Insurance Type | Life Insurance |

| Non-Life Insurance | |

| Health Insurance | |

| By Distribution Channel | Bank Branch |

| Digital / Online Banking | |

| Mobile Banking Apps | |

| Contact-Centre / Phone | |

| Affinity & Embedded (FinTech / Retail) | |

| By End-User | Retail Customers |

| Small & Medium Enterprises (SMEs) | |

| Corporate & Affluent | |

| By Country | France |

| Italy | |

| Spain | |

| Germany | |

| United Kingdom | |

| Portugal | |

| Belgium | |

| Poland | |

| Netherlands | |

| Switzerland | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size of the Europe Bancassurance market?

The market generated USD 685.84 billion in 2026 and is projected to reach USD 855.18 billion by 2031.

Which insurance line is growing fastest in European bancassurance?

Health insurance leads growth with a forecast of 6.52% CAGR through 2031 due to aging demographics and demand for private healthcare.

How important are mobile apps for bancassurance distribution?

Mobile apps are the fastest-rising channel, expected to grow at an 8.10% CAGR and steadily erode the branch’s 67.75% share.

Which country is forecast to see the quickest expansion?

Poland is set to post a 7.55% CAGR as rising incomes and digital adoption lift insurance penetration.

Who are the leading players in the Europe Bancassurance market?

Crédit Agricole Assurances, BNP Paribas Cardif, and CNP Assurances collectively hold just over 35.1% of written premiums, leveraging exclusive bank partnerships.

What is the biggest challenge facing European bancassurers?

Regulatory fragmentation across EU states and competition from BigTech ecosystems constrain seamless cross-border scaling and demand rapid digital innovation to defend market share.

Page last updated on: