Financial Services and Investment Intelligence

29th JulyWealth Management Intelligence for the Middle East

4 Min Read

The Europe Online Insurance Market Report is Segmented by Insurance Type (Life Insurance, Health Insurance, Property & Casualty, Specialty Lines), Customer Segment (Retail/Individual, SME/Commercial, Large Enterprise/Corporate), Device Platform (Mobile App, Desktop/Web), and Geography (United Kingdom, Germany, France, Spain, Italy, BENELUX, NORDICS, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

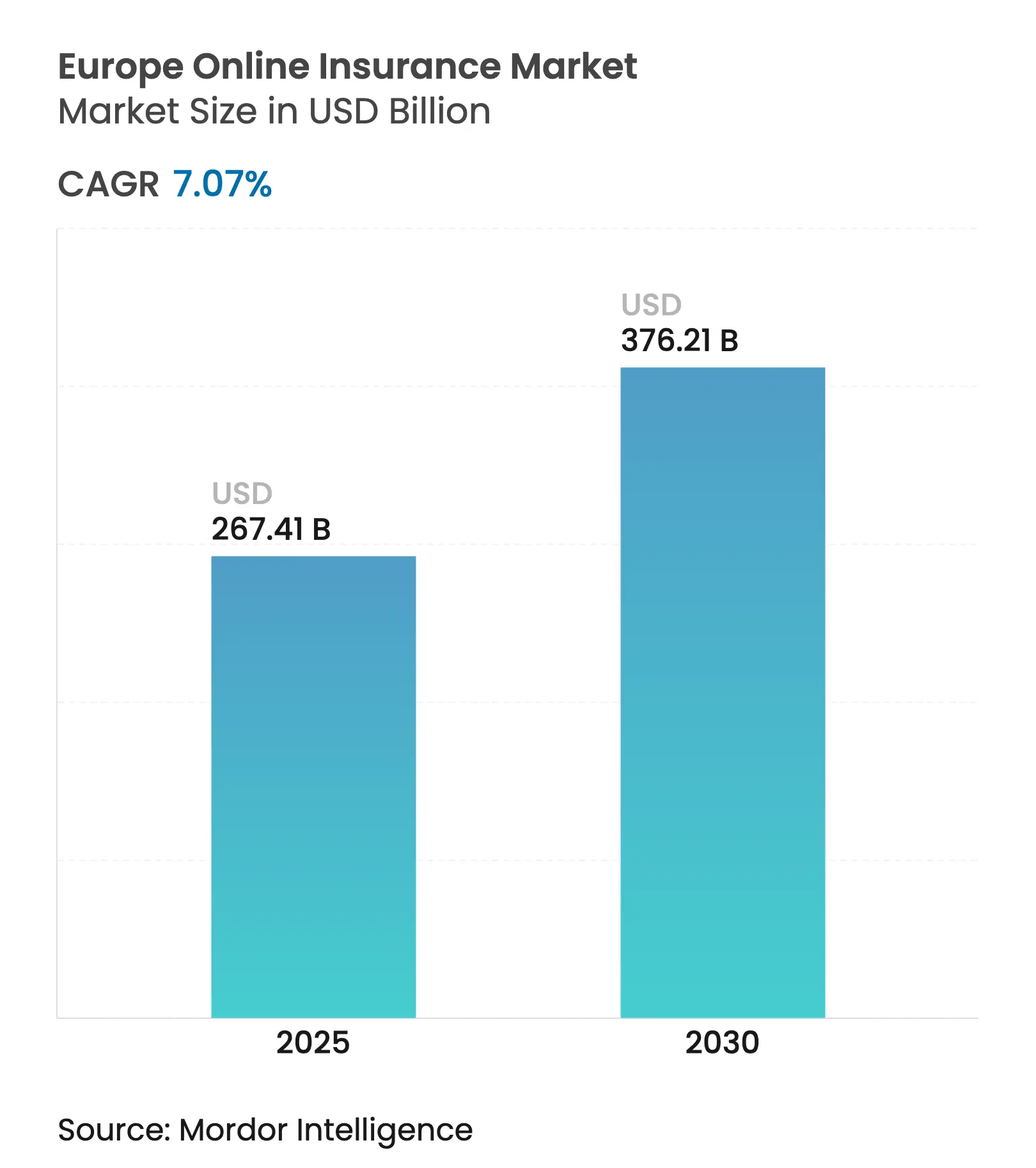

| Market Size (2025) | USD 267.41 Billion |

| Market Size (2030) | USD 376.21 Billion |

| Growth Rate (2025 - 2030) | 7.07 % CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Europe online insurance market size stood at USD 267.41 billion in 2025 and is forecast to reach USD 376.21 billion by 2030, reflecting a 7.07% CAGR across the period. Sustained digital-first consumer behavior, open-finance mandates such as the Financial Data Access (FIDA) regulation, and heightened cyber-resilience rules under DORA continue to reconfigure the competitive order. Property & Casualty remains the volume anchor, while specialty cyber and pet lines pull the fastest incremental demand. Embedded distribution partnerships with auto and e-commerce brands are lowering acquisition costs, and mobile apps are turning claims filing into a smartphone activity for millions of European policyholders. Cross-border compliance spending, by contrast, is discouraging small carriers from scaling pan-EU footprints, paving the way for deeper consolidation led by well-capitalized incumbents.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Accelerating smartphone-driven digital adoption

Accelerating smartphone-driven digital adoption

| +1.8% | EU-wide; strongest in Nordics and Germany | Medium term (2-4 years) |

(%) Impact on CAGR Forecast

:

+1.8%

|

Geographic Relevance

:

EU-wide; strongest in Nordics and Germany

|

Impact Timeline

:

Medium term (2-4 years)

|

EU open-finance & e-ID regulations easing onboarding

EU open-finance & e-ID regulations easing onboarding

| +1.2% | Early adoption in Netherlands and Estonia | Long term (≥4 years) | |||

COVID-catalyzed consumer shift to remote services

COVID-catalyzed consumer shift to remote services

| +0.9% | Highest stickiness in Southern Europe | Short term (≤2 years) | |||

Embedded insurance via mobility & e-commerce platforms

Embedded insurance via mobility & e-commerce platforms

| +1.5% | Germany, France, UK | Medium term (2-4 years) | |||

Usage-based/telematics pricing attracting Gen-Z drivers

Usage-based/telematics pricing attracting Gen-Z drivers

| +0.8% | UK, Germany, France | Medium term (2-4 years) | |||

SME cyber-cover boom under NIS2 & DORA compliance

SME cyber-cover boom under NIS2 & DORA compliance

| +1.1% | Financial hubs across EU | Short term (≤2 years) | |||

| Source: Mordor Intelligence | ||||||

Accelerating Smartphone-Driven Digital Adoption

Saturation smartphone penetration above 85% is now the default across large European economies. Flagship carriers such as AXA report that more than one in three P&C policies sold in 2024 originated on mobile, a share that doubled in two years[1]AXA Group, “2024 Integrated Report,” axa.com. Nordic regulators have mainstreamed national e-ID schemes, permitting instant coverage binding without paperwork, which is pushing claim severity down through faster loss reporting. German millennials download insurer apps primarily for motor and pet lines, forcing laggards to overhaul legacy portals or lose renewal cohorts. High build costs and GDPR audits inhibit smaller mutuals, thereby amplifying the scale edge of pan-EU groups that already operate secure mobile architectures.

EU Open-Finance & e-ID Regulations Easing Onboarding

The FIDA rulebook, entering force in 2026, enables insurers to source verified customer banking data, compressing quote times from days to minutes. Netherlands and Estonia prove the concept: carriers there cut onboarding drop-off rates by double digits once real-time bank feeds replaced manual uploads. Broader datasets improve fraud analytics while letting underwriters finesse pricing for thin-file applicants such as micro-entrepreneurs. Comparison portals risk disintermediation as incumbents plug open-finance APIs directly into branded journeys. Yet privacy activists remain vocal, requiring insurers to escrow data locally and run routine consent refreshes, a compliance overhead that favors enterprises with mature governance teams.

COVID-Catalyzed Consumer Shift to Remote Services

Remote policy servicing transitioned from contingency plan to baseline expectation during pandemic lockdowns. Generali’s 2024 numbers show video claims inspections now cover 55% of household losses across Spain and Italy, slashing settlement-cycle days by half. Virtual walk-throughs and AI document reading tools sustain these gains even as on-site adjusters return. Embedded trip-cancellation add-ons bundled at airline checkout are grabbing spend once directed toward agent-sold policies. However, branch-centric life insurers must retrain existing tied networks for hybrid advisory roles or watch margins erode under fixed-cost pressure.

Embedded Insurance via Mobility & E-Commerce Platforms

Allianz switched on factory-installed coverage for every Jaguar Land Rover vehicle sold in Europe, auto-activating when drivers sign the infotainment screen. Qover’s plug-and-play APIs now power parcel-loss policies across multiple continental marketplaces, lifting attachment rates above 60% for high-value electronics. German and French regulators fast-track approvals so long as premiums are displayed pre-checkout, which removes the paperwork bottleneck. Ultimately, carriers integrating deep into merchant ecosystems capture behavioral data that enriches renewal pricing. Implementation costs, including endpoint cyber-hardening and multi-country VAT handling, remain prohibitive for sub-scale players.

Restraints Impact Analysis

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Fragmented EU compliance inflating pan-regional costs

Fragmented EU compliance inflating pan-regional costs

| -1.4% | Most acute in smaller markets | Long term (≥4 years) |

(%) Impact on CAGR Forecast

:

-1.4%

|

Geographic Relevance

:

Most acute in smaller markets

|

Impact Timeline

:

Long term (≥4 years)

|

Advice-heavy life & savings products resist full

digital

Advice-heavy life & savings products resist full

digital

| -0.8% | Germany, Austria | Medium term (2-4 years) | |||

Rising digital-acquisition costs on comparison sites

Rising digital-acquisition costs on comparison sites

| -1.1% | UK, Germany, France | Short term (≤2 years) | |||

Funding winter throttling pan-EU insurtech scale-ups

Funding winter throttling pan-EU insurtech scale-ups

| -0.9% | Startup hubs across EU | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Fragmented EU Compliance Inflating Pan-Regional Costs

Despite Solvency II and IDD, national transpositions still diverge on policy disclosures, tax stamping, and reserve accounting[2]S&P Global Ratings, “European Insurance Outlook 2025,” spglobal.com. Multi-market insurers juggle as many as 27 document templates per product line, elevating legal spend and time-to-launch. Smaller carriers surrender potential growth because cloning systems for each jurisdiction dilute already-thin tech budgets. Regulatory sandboxes help, but only a few member states open them to foreign insurers, limiting harmonization upside. Consolidation remains the strategic workaround, allowing scale leaders to amortize compliance tooling over larger premium bases.

Advice-Heavy Life & Savings Products Resist Full Digital

German BaFin rules demand suitability assessments on unit-linked offerings, forcing video or phone consultation checkpoints that fracture otherwise sleek funnels. Return-guarantee features add complexity unsuited to mobile screens, and consumers still value in-person reassurance for 20-year commitments. Hybrid robo-advisor pilots improve efficiency, yet conversion hovers at <25% against agent channels where personal trust drives sign-off. Nevertheless, generational turnover promises gradual digitization provided regulators sanction simplified benefit illustrations. Until then, pure-play online life insurers allocate disproportionate marketing budgets just to match branch-network volumes.

By Insurance Type: Specialty Lines Drive Innovation

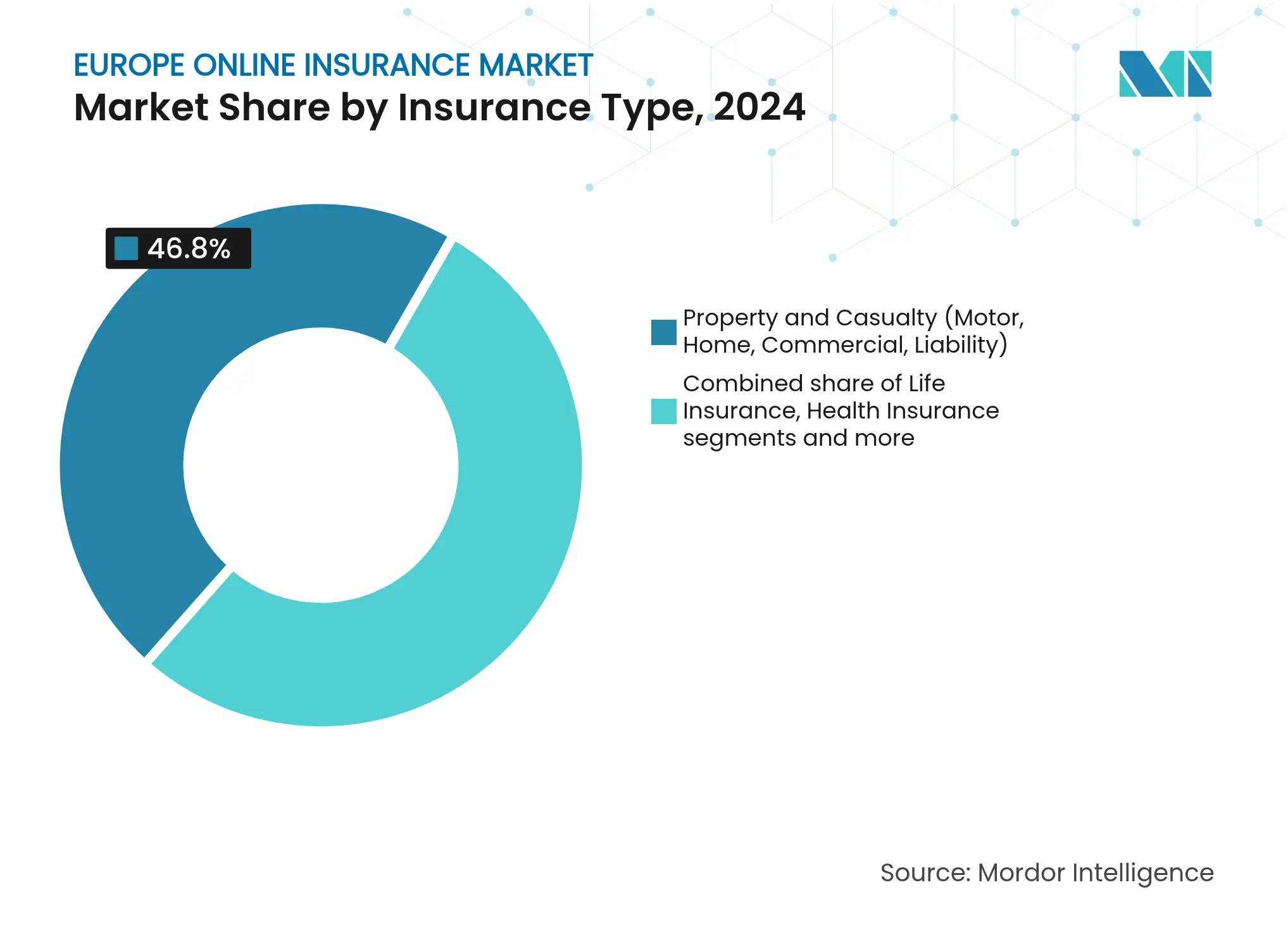

Specialty Lines generated less than one-fifth of premiums in 2024, yet the category is forecast to post an 8.23% CAGR through 2030, handily exceeding the broader Europe online insurance market. Cyber coverage expansion alone will inject multibillion-dollar premium pools due to mandatory DORA compliance. Pet insurers ride demographic shifts such as rising single-person households and increased spend on veterinary telehealth, pushing attachment rates on wellness platforms. Travel insurers are launching parametric micro-covers that pay automatically at defined disruption thresholds, turning claims into real-time transactions. Marine pleasure-craft covers are migrating online as instant quote engines replace broker phone calls.

Property & Casualty still held 46.8% of the Europe online insurance market share in 2024, proving that standardized policies favor digital comparison. Home and motor lines remain sticky, but modest saturation means growth hovers in low single digits. Innovation is tilting toward modular add-ons, flood top-ups, gadget riders, that let consumers adjust protection levels mid-term. Life insurers cautiously test simplified-issue term products online, yet heavy advisory rules impede full automation. Health carriers pursue ecosystem plays, bundling wellness apps, digital pharmacies, and preventive analytics to secure lifetime value.

Note: Segment shares of all individual segments available upon report purchase

By Customer Segment: SME Digital Transformation Accelerates

Once reliant on local brokers, SMEs now utilize instant-issue portals that can underwrite professional liability in under five minutes. With regulatory pushes like NIS2, supply-chain directives, and ESG reporting, fresh exposures arise, best managed by cloud-native underwriting as usage data enables granular risk differentiation, premium affordability improves, rewarding firms that prioritize cybersecurity hygiene or maintain telematics-monitored fleets. In 2024, while retail and individual customers account for 70.1% of revenue, their growth slows as penetration levels off in mature markets. Cross-sell opportunities prove potent; carriers seamlessly upsell gadget covers and dental add-ons within personal-lines dashboards.

The SME boom reshapes servicing models: digital risk-assessment questionnaires draw on sector benchmarks and link to training modules, reducing loss frequency. Invoice-embedded credit insurance helps micro-exporters secure working capital as banks trust automated default scoring. Yet owner-managers still seek live chat reassurance, prompting insurers to maintain hybrid call centers. Onboarding friction dips as KYC pulls company registry data in real time, a leap that vaults SME satisfaction scores above 80% in pilot cohorts. Commercial expansion is forecast to lift the share of the European online insurance market to roughly one-third by the decade's end.

By Device Platform: Mobile Momentum Builds

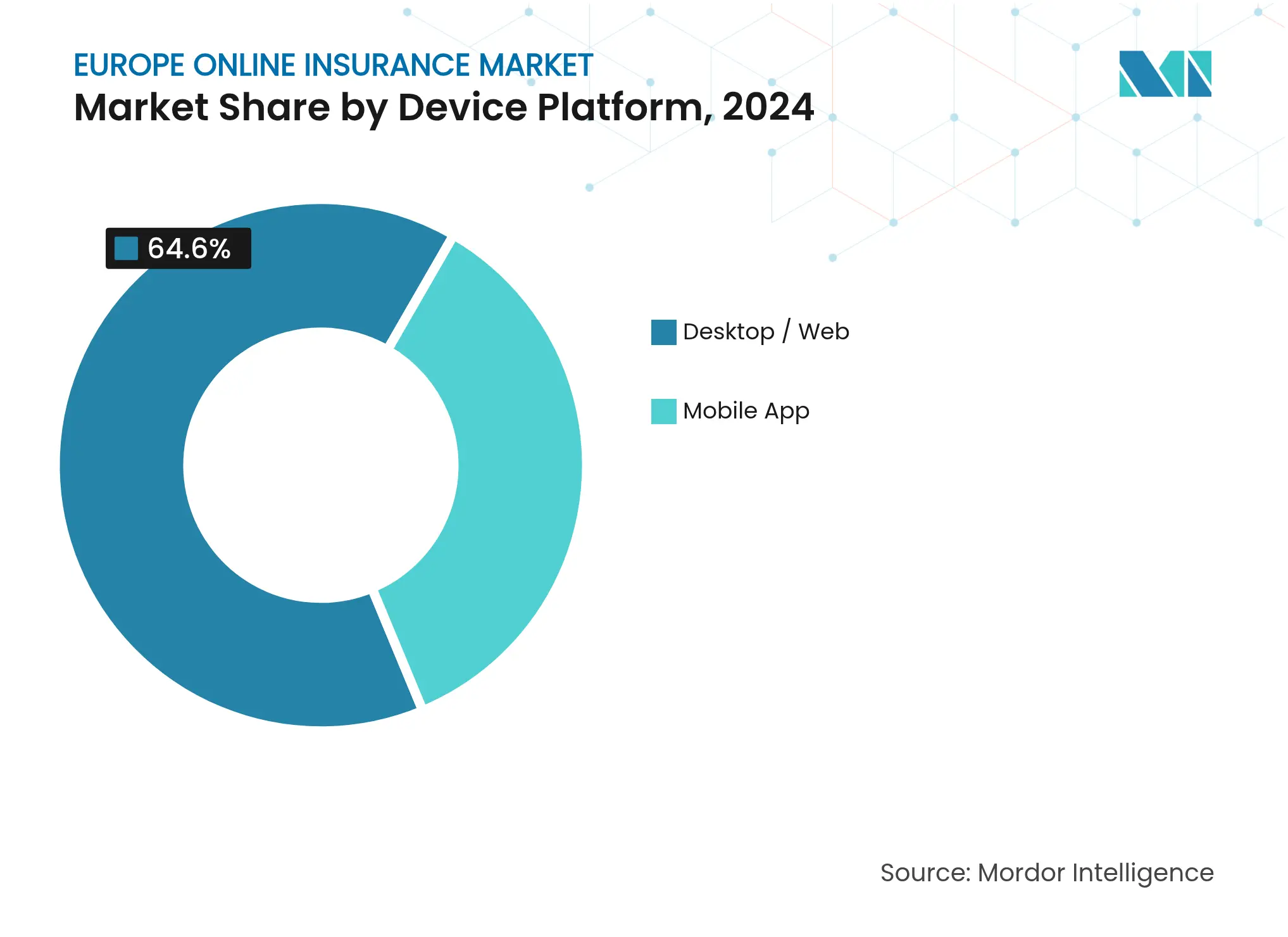

Desktop journeys dominated early e-commerce waves, locking in 64.6% of premium flow in 2024; nonetheless, mobile is registering an 8.91% CAGR through 2030 as handset screens enlarge and biometrics simplify log-ins. Claims photos, GPS location stamps, and push notifications cut adjuster calls, shrinking indemnity leakage. Telematics apps harness phone accelerometers to score braking and cornering, driving personalised motor pricing. Responsive design keeps complex fleet or life illustrations on larger screens yet syncs data with app wallets for on-the-go edits. Progressive web apps bridge offline situations, caching policy data when roaming networks drop.

Transactional experience parity across devices has become a hygiene factor. Policyholders routinely start quotes on work laptops and bind on phones during commutes, forcing back-end orchestration that tracks interactions seamlessly. 5G rollout allows high-resolution video inspections, accelerating total-loss settlements. Voice-based virtual assistants, meanwhile, pilot appointment scheduling and beneficiary updates, opening an access channel for visually impaired customers. Security upgrades, passkeys, and device-level encryption counter phishing spikes and keep regulators satisfied that mobile does not undercut consumer protection standards.

Online Insurance Market in the United Kingdom

The United Kingdom retains leadership in the European online insurance market with a 27.5% revenue share in 2024, boosted by an entrenched price-comparison culture and early telematics uptake. Post-Brexit divergence complicates passporting, yet London’s supervisory sandbox accelerates embedded innovation, letting carriers pilot parametric flood covers city-wide. Germany’s sizeable economy is unlocking digital latency; smartphone-centric Gen-Z cohorts push motor and pet insurers to overhaul UX, and federal digital-identity rollouts trim KYC time. France balances innovation and vigilance; the ACPR insists on transparent AI underwriting, yet green-lighting cross-industry data-share pacts that power embedded merchant offers.

Spain headlines growth at a 7.85% CAGR to 2030 as national recovery funds bankroll SME digitization and autonomous-vehicle pilot zones. Italy, fresh from distribution reform, speeds product approvals. Generali’s direct arm halved time-to-market for modular home packages, luring urban millennials who skipped legacy agent channels[3]Generali Group, “Product Innovation Roadmap 2025,” generali.com. BENELUX shows open-banking maturity; Dutch carriers auto-prefill quotes via PSD2 feeds, elevating bind rates. Nordics continue topping digital engagement indices but face growth ceilings; insurers pivot to value-added prevention services to defend renewals.

Central and Eastern Europe represent the long-run upside: Poland’s fast-growing e-commerce base seeds demand for embedded shipment protection, while Hungary’s regulator endorses remote claims for hail-damaged autos, slicing turnaround times. However, disparate tax treatments and file-and-use rules prolong launch cycles. Carriers that calibrate pricing to lower average income levels without diluting coverage stand to gain early loyalty in these under-penetrated markets. Cross-border digital IDs envisioned by the EU wallet program may finally allow unified platform operations, stripping out redundant middle layers and unleashing next-wave cost efficiencies.

Online Insurance Market in Italy

Italy's online insurance market is experiencing remarkable transformation, projected to grow at approximately 9% annually from 2024 to 2029. Despite traditionally favoring conventional insurance distribution channels, the market is witnessing a significant shift in consumer behavior and digital adoption. The Italian Insurance Association's findings reveal an increasing acceptance of digital policies, with 47% of recent insurance buyers expressing satisfaction with their digital purchases. This digital transformation is particularly evident in the online health insurance sector, where technological innovations enabling real-time health data transmission are driving growth. The market's evolution is further supported by insurtech initiatives, exemplified by significant investments in digital infrastructure and customer-centric solutions. The integration of digital channels with traditional insurance expertise is creating a hybrid model that appeals to both tech-savvy consumers and those who value personal guidance. Insurance companies are increasingly focusing on developing user-friendly digital platforms while maintaining the personal touch that Italian consumers traditionally value. The market's digital maturity is particularly evident in the motor insurance sector, where online channels have gained significant traction.

Online Insurance Market in Germany

Germany's online insurance market demonstrates remarkable technological sophistication and innovation in digital insurance services. The country stands out for having the most extensive network of internet channels for insurers across Europe, with German insurance firms particularly active in the online space. The market's strength lies in its robust insurtech ecosystem, with Germany hosting the widest selection of insurtechs in Europe. The digital transformation is particularly evident in simple products such as motor vehicle liability and travel cancellation insurance, which have gained significant online traction. The market benefits from strong government support through initiatives like the Digital Hub program, which includes InsurLab, the largest insurtech initiative in Germany. The emergence of neo-insurers alongside traditional insurance companies has created a dynamic competitive environment, driving innovation in digital user interfaces and customer experience. The importance of a mobile-first philosophy and context-based approaches has become increasingly significant, with insurance providers investing heavily in modern data infrastructure and innovative solutions.

Online Insurance Market in France

France's online insurance market exhibits a unique blend of traditional insurance values and digital innovation. The French market's distinctive characteristic lies in its balanced approach to digitalization, where online channels complement rather than replace traditional distribution methods. The market has witnessed significant developments in insurtech, with notable success stories like Alan in the health insurance segment demonstrating the potential for digital-first insurance solutions. The health crisis has accelerated digital adoption, with a dramatic increase in website and customer area usage. Insurance providers are responding by developing omnichannel approaches that allow seamless customer assistance across all platforms. The market is characterized by strong customer loyalty to traditional insurers, even as they expand their digital capabilities. French insurers are focusing on creating digital experiences that maintain the high level of service and personalization that French consumers expect, while leveraging technological innovations to improve operational efficiency and customer engagement.

Online Insurance Market in Other Countries

The virtual insurance landscape across other European countries presents a diverse picture of digital adoption and market maturity. Countries like Denmark showcase advanced digital integration with 80-90% of insurance sales occurring online, while markets such as Bulgaria and the Czech Republic are still in the early stages of digital transformation. The Nordic region, particularly Norway, demonstrates strong digital adoption in non-life products, while Eastern European markets are gradually building their digital infrastructure. Countries like Spain and Portugal are developing their online insurance capabilities, focusing on creating user-friendly digital platforms while maintaining traditional distribution strengths. Switzerland, Belgium, and the Netherlands each bring unique approaches to digital insurance, influenced by their specific market conditions and consumer preferences. This diversity in digital maturity across European markets creates opportunities for innovation and knowledge sharing, contributing to the overall evolution of the European online insurance sector.

Market Concentration

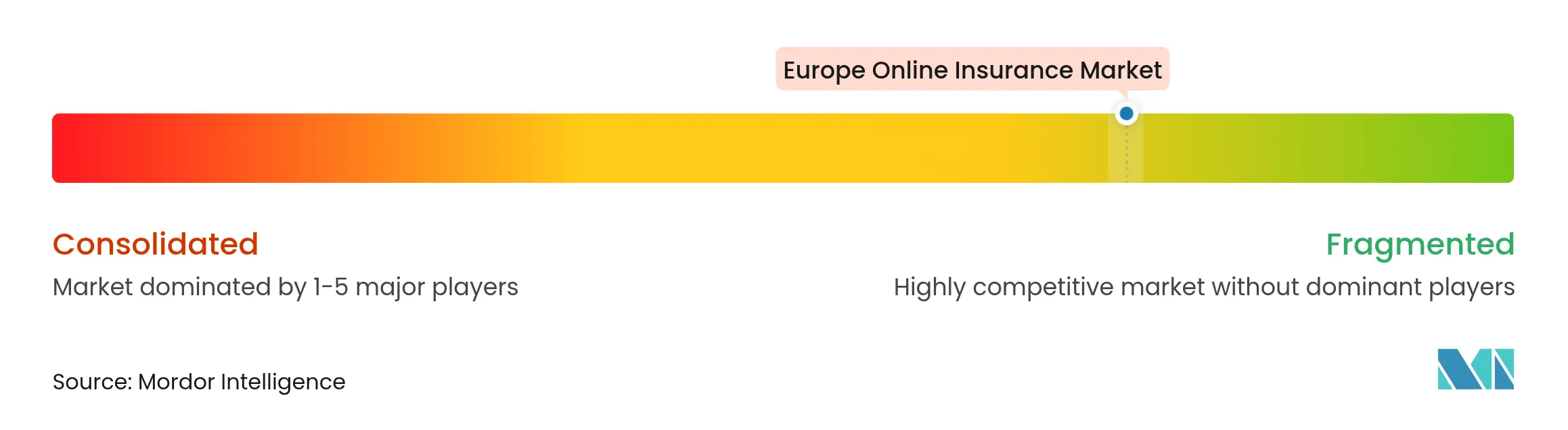

Europe’s online insurance arena displays mid-level concentration: the top five carriers account for a little over half of the premium pool, leaving ample space for challengers. Incumbents led by Allianz, AXA, and Generali funnel double-digit budget shares into AI underwriting cores and omnichannel CRM, targeting a sub-90-second quote-to-bind outcome. Aviva’s USD 4.6 billion absorption of Direct Line catapults its UK market heft and gifts a scalable cloud tech stack [SPGLOBAL.COM]. Helvetia’s pursuit of Baloise aims to unlock shared DevOps and claims robotics, signaling that regional champions view size as a prerequisite for cybersecurity investments now mandated under DORA.

Insurtechs like Wefox and Alan carve niches on slick UX and subscription-style policies; yet rising reinsurance costs and capital scarcity have slowed their multi-country sprints. Embedded specialists such as Qover emerge as pivotal partners, supplying white-label capacity to ride-hailing and electronics retailers without foreground branding. Brokers respond by curating risk-prevention ecosystems, bundling IoT sensors with coverage to retain advisory relevance. Meanwhile, reinsurers develop off-the-shelf risk engines, letting mid-tier carriers outsource analytics and compete on brand rather than data science.

Strategic technology themes converge on cloud migrations, zero-trust cyber frameworks, and algorithmic fraud detection that flags anomalous FNOL patterns within seconds. Early adopters report a 20% drop in claim-handling expense ratios after shifting to AI triage. Carriers lacking capital for full builds opt for modular SaaS connections, though integration debt poses long-term technical risk. The competitive outcome will likely hinge on those master’s low-touch service at an industrial scale while continuing to meet evolving regulatory guardrails.

*Disclaimer: Major Players sorted in no particular order

1. Table of Contents – Europe Online Insurance Market

2. Introduction

3. Research Methodology

4. Executive Summary

5. Market Landscape

6. Market Size & Growth Forecasts (Value)

7. Competitive Landscape

8. Market Opportunities & Future Outlook

Online insurance is one can buy insurance online by sitting at home or office without visiting an agent or company. The Europe online insurance market is segmented by Type (life and non-life insurance), and Geography (Germany, France, United Kingdom, Italy, and the Rest of Europe.). The market sizes and forecasts are provided in terms of value (USD billion) for all the above segments.

Wealth Management Intelligence for the Middle East

4 Min Read

Driving Growth in the Embedded Insurance Market

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.