Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

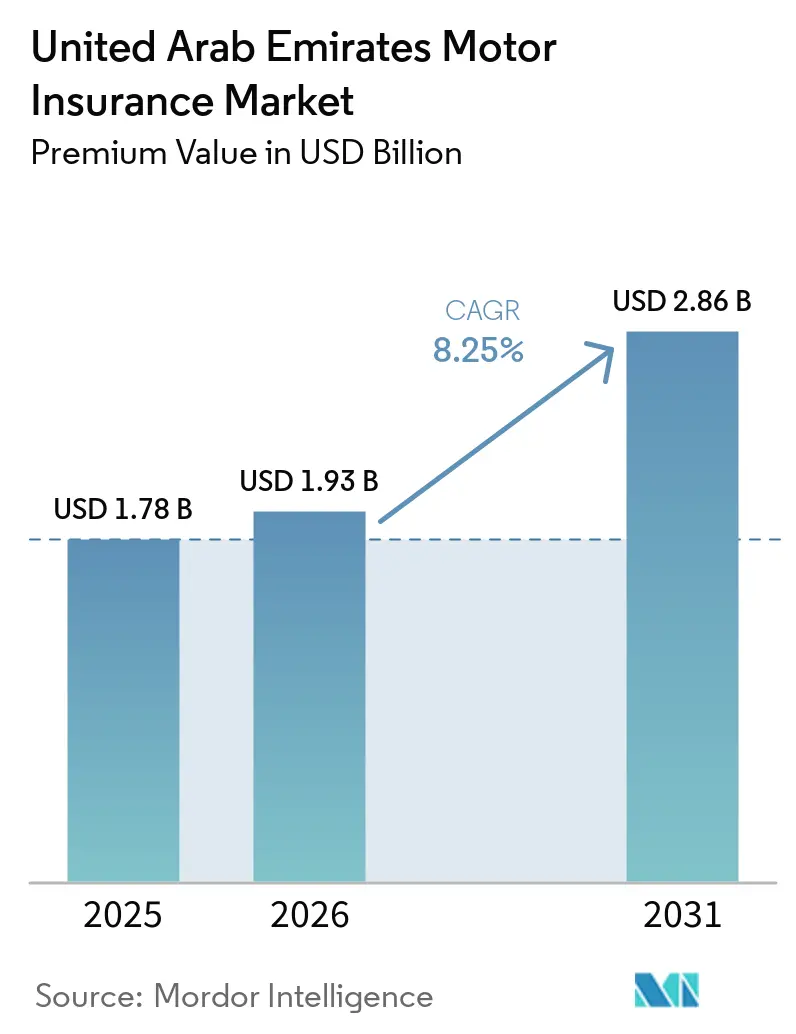

| Base Year Market Size (2025) | USD 1.78 Billion |

| Market Size (2026) | USD 1.93 Billion |

| Market Size (2031) | USD 2.86 Billion |

| Growth Rate (2026 - 2031) | 8.25% CAGR |

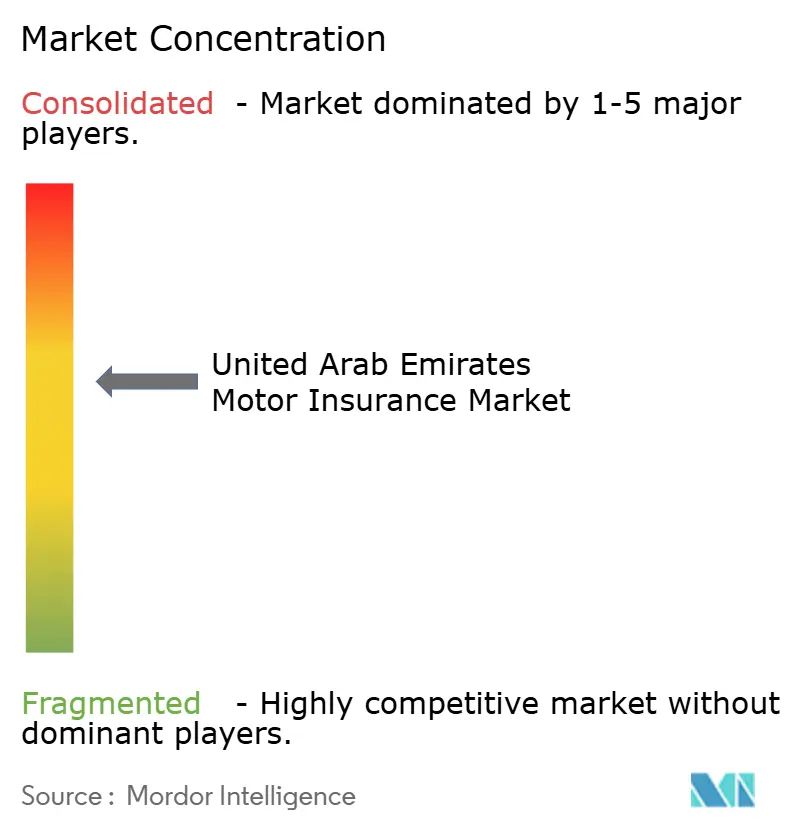

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Motor Insurance Market Analysis by Mordor Intelligence

The United Arab Emirates Motor Insurance Market size in terms of premium value is projected to be USD 1.78 billion in 2025, USD 1.93 billion in 2026, and reach USD 2.86 billion by 2031, growing at a CAGR of 8.25% from 2026 to 2031.

The growth path is anchored in consistent enforcement of third-party liability at registration and renewal, climate-linked repricing that tilts portfolios toward comprehensive cover, and digital onboarding that shortens quote and bind to under a minute on leading platforms. Risk awareness after the April 2024 flood event has accelerated a lasting shift from TPL-only policies to comprehensive coverage that includes natural perils, and carriers have added parametric triggers to speed settlement in severe rainfall episodes. Distribution economics are changing as aggregators and embedded channels expand reach to younger and price-sensitive buyers, even as broker regulation now requires direct remittance of premiums to insurers to reduce counterparty risk. AI-enabled claims triage, digital identity for instant policy issuance, and product innovations like parametric motor policies are improving customer experience and speeding cash cycles for carriers. Top carriers are also publishing record earnings on the back of faster settlements and tighter underwriting, confirming that the UAE motor insurance market has moved from pure premium growth to disciplined, technology-backed profitability.

Key Report Takeaways

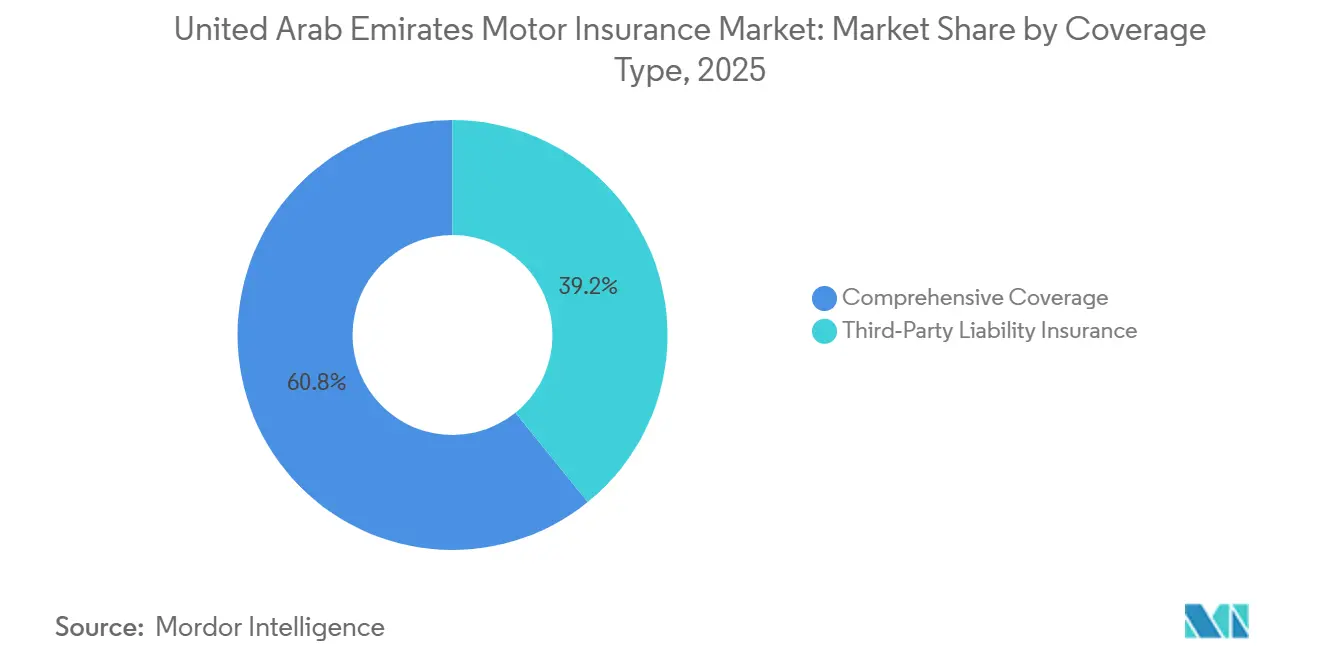

- By coverage type, comprehensive policies led with 60.84% of the UAE motor insurance market size in 2025 and are projected to grow at 8.78% through 2031, reflecting a durable post-flood preference for broader protection that includes natural perils.

- By distribution channel, insurance agents and brokers held 60.46% of the UAE motor insurance market size in 2025, while aggregators and comparison portals posted the fastest trajectory at 11.62% over 2026 to 2031 as regulated APIs enabled instant quotes and binding with verified identity.

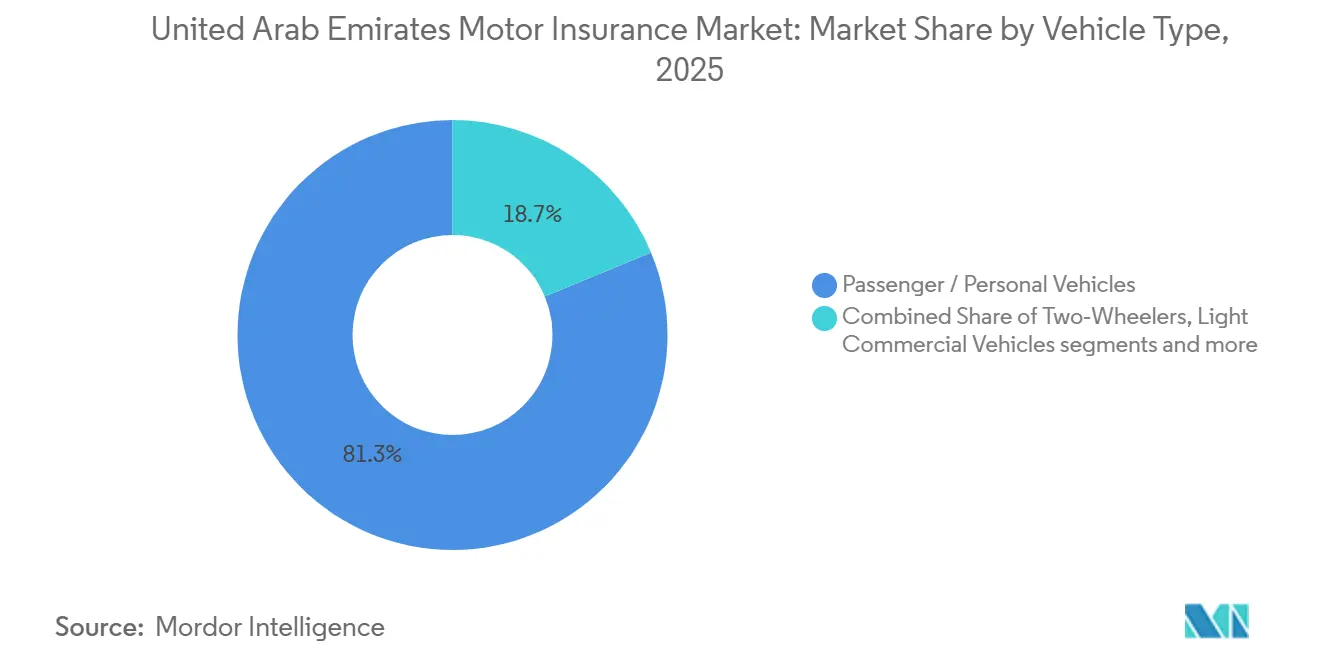

- By vehicle type, passenger cars accounted for 81.27% of the UAE motor insurance market share in 2025, while commercial vehicles, comprising LCVs and M/HCVs, are projected to expand at 9.14% CAGR through 2031 as platform fleets and advanced mobility use cases scale.

- By vehicle age, used vehicles represented 63.58% of the UAE motor insurance market size in 2025 and are forecast to advance at 9.74% CAGR through 2031, aided by affordability preferences and rising attachment of comprehensive cover in flood exposed areas.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Motor Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory TPL enforcement at registration and renewal | +1.8% | National, stronger checks in Dubai, Abu Dhabi, Sharjah | Short term (≤ 2 years) |

| Post‑2024 flood risk awareness sustains comprehensive demand | +2.1% | National, elevated in coastal and wadi‑adjacent zones | Medium term (2-4 years) |

| Broker‑led distribution at scale with faster digital quote and issue | +1.2% | National, concentrated in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Auto finance requirements for full cover on financed vehicles | +1.0% | National, earlier traction in key auto hubs | Short term (≤ 2 years) |

| Embedded B2B cover with ride‑hailing and logistics fleets | +0.9% | Dubai core with expansion in Abu Dhabi and Sharjah corridors | Medium term (2-4 years) |

| OEM ADAS and connected data enabling differentiated pricing | +0.7% | National, led by pilot zones and connected‑car cohorts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Broker Led Distribution Scale with Rising Digital Quote and Issue Speeds

Brokers remain the largest channel by share, and that position is supported by multilingual service and advisory needs across a diverse expatriate base that values guidance on options and endorsements. The channel is digitizing as regulators require brokers to remit premiums directly to insurers and set response standards for claims support, which removes float and compresses timelines from quote to bind. Open integration with insurers and biometric digital identity has enabled instant quote retrieval and near real-time policy issuance on carrier platforms as well as on aggregator portals, which is drawing new buyers and improving conversion. Large online platforms have reported seven-figure policy counts and multi-million user bases, which illustrates how price transparency and speed have broadened the addressable pool for motor products in the UAE. As digital origination rises, carriers are emphasizing AI-supported claims and post-bind servicing to defend margins in a more transparent pricing environment while preserving the advisory benefits of broker relationships.

Auto Finance Linked Requirements for Full Cover on Financed Vehicles

Bank and dealer finance for new purchases typically requires comprehensive coverage with the lender listed as loss payee, which locks in insurance attachment and stabilizes demand across cycles. The linkage is visible in consumer price data, where inflation eased in transport costs while insurance and financial services showed firm pricing tied to contractual coverage during 2025. As electric vehicles gain traction, the same finance coverage linkage ensures comprehensive attachment because lenders protect higher unit values and battery components through coverage that is broader than TPL. Carriers are building EV-specific packages in concert with OEMs and dealers to align coverage features, roadside support, and data-backed risk scoring that targets lower claim frequency on newer safety tech cohorts. The combined effect is a reliable pipeline of comprehensive policies tied to financed vehicles, which supports the quality and persistence of premiums in the UAE motor insurance market.

Embedded B2B Motor Cover with Ride Hailing and Logistics Platforms Expands Fleet Uptake

Mobility platforms have embedded commercial cover into onboarding, so driver partners bind compliant protection during sign-up, which limits leakage and speeds fleet activation. Digital wallets and per-trip micro deductions streamline premium collection for gig drivers, and the same model applies to logistics fleets that seek consolidated billing and predictable pricing. Autonomous pilots launched in Dubai as part of a robotaxi program have required bespoke liability structures that shift emphasis from driver negligence to software and sensor performance, which has led to co-underwriting arrangements with leading carriers. As these programs expand and as platform volumes grow, embedded B2B cover increases the commercial portion of the UAE motor insurance market while sharpening the technical pricing challenge for urban duty cycles. Insurers are responding with telematics, fleet performance dashboards, and negotiated service levels to keep loss costs and downtime in check as utilization intensifies.

OEM ADAS and Connected Data Enabling Differentiated Pricing and Lower Frequency

Connected vehicles and advanced driver assistance systems are improving risk profiling by supplying validated signals on speed, braking, trip counts, and alerts, which allows carriers to reward safer cohorts and disincentivize risky behavior. Early usage-based pilots in the UAE show that measurable safe driving can unlock material premium reductions under monitored programs, and carriers have reported strong customer interest tied to transparent scoring and mobile app dashboards. OEMs are also standardizing ADAS in popular models that now reach UAE showrooms, and they report material declines in certain low-speed collision claims for vehicles equipped with these safety suites. New entrants in compact EVs are delivering over-the-air updates that refine safety algorithms over a vehicle’s life, which opens a path to mid term repricing where telematics confirm improved risk signals. Parallel to vehicle data, geospatial analytics from local providers now map climate and theft exposure at fine resolution, which supports postal code-level pricing and has shown improvements in loss ratios for adopters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported parts and labor inflation elevate repair costs and severity | -0.5% | National, more acute where premium vehicles and EVs cluster | Short term (≤ 2 years) |

| Price transparency on aggregators compresses technical margins | -0.3% | National, most visible in large urban aggregator markets | Medium term (2-4 years) |

| Reinsurance hardening and tighter natural peril terms after 2024 | -0.4% | National, with capital‑market alternatives explored by hubs | Medium term (2-4 years) |

| Data consent and privacy frictions slow telematics scale‑up | -0.2% | National, with stricter controls in certain free zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Imported Parts and Labor Inflation Elevating Average Repair Cost and Severity

Commodity inflation, wage growth, and a high import share for spare parts combine to push average repair costs higher, pressuring severity and forcing carriers to pass through increases at renewal. The UAE relies on global supply chains for most components, which ties economics to freight and materials cycles as well as exchange rates. EVs add complexity because battery replacement and high voltage handling require certified centers, and transport to brand-authorized garages can raise claim totals even on minor incidents. To improve outcomes, carriers are expanding direct repair networks with negotiated labor rates and genuine parts access to shorten cycle times and reduce leakage. These elements continue into 2026 with inflation now moderating in the official data, while unit-level repair costs remain structurally higher than pre 2024 baselines, which keeps this restraint relevant to the UAE motor insurance market.

Data Consent and Privacy Frictions Slowing UBI and Telematics Scale Up

Telematics and usage-based programs depend on clear consent, stringent storage controls, and transparency in scoring logic to meet regulatory expectations for automated decisions. The UAE framework centers on explicit options for personal data processing and onshore storage, and it requires robust governance when models influence pricing or eligibility, which adds time and cost to program rollouts. Carriers that move first have invested in onshore data infrastructure and customer dashboards that explain trip scoring to encourage adoption and address privacy concerns. Uptake is rising yet below the most optimistic projections for 2026 as a notable share of customers hesitates to share location data, which makes incentives and clear controls critical. Over time, as consent flows improve and value is demonstrated through lower premiums for safe driving, UBI’s contribution to the UAE motor insurance market is likely to grow from a modest base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coverage Type: Comprehensive Dominance Post Flood Awareness

Comprehensive coverage held 60.84% of the UAE motor insurance market share in 2025, and the UAE motor insurance market size tied to this coverage is projected to expand at a 8.78% CAGR over 2026 to 2031 as buyers prioritize natural peril protection after the 2024 floods [1]Munich Re, “Natural Disaster Losses 2024,” Munich Re Media Centre, munichre.com. The April 2024 event drove a sustained reassessment of garage locations, basement parking, and low-lying neighborhoods, which shifted preferences from TPL only to comprehensive policies that include flood and water ingress cover in risk-sensitive zones. Carriers reinforced confidence by documenting high acceptance and rapid settlement of motor flood claims during 2024, which increased retention through 2025 and supported broader attachment of comprehensive endorsements at renewal. Product innovation also accelerated as parametric endorsements that trigger measured rainfall cleared regulatory approval, giving customers a faster, automated payout path for clearly defined weather events. Together, these dynamics are embedded comprehensively as the anchor of portfolio quality for 2026 and beyond, supported by better event analytics and reinsurer guidance on sub-limits and deductibles that balance protection with capital efficiency.

TPL remains the legal minimum and continues to add policies as verification at registration and renewal becomes embedded in the standard workflow across Emirates, lifting compliance and stabilizing premium flows for carriers. TPL growth in 2026 reflects both policy enforcement and the needs of price-sensitive drivers, although it does not address damage to the insured’s own vehicle during weather events or collisions, which preserves the demand gap that comprehensive cover fills in flood-affected districts. Carriers are also applying safer driving incentives and digital claims to keep comprehensive attractive in budget-constrained cohorts, and published case studies show cycle time reductions and high customer satisfaction where AI triage supports straight-through processing. The UAE motor insurance market size for comprehensive is therefore supported by both higher unit premiums where natural perils are relevant and by increased attachment among used vehicle owners who saw neighbor loss experiences firsthand in 2024. As reinsurers refine appetite and pricing for water-related exposure, carriers are calibrating endorsements and excess levels to maintain affordability, an approach that preserves growth while keeping solvency aligned with supervisory expectations.

By Distribution Channel: Aggregator Surge Reshapes Acquisition Economics

Insurance agents and brokers held 60.46% of the distribution in 2025, and the channel’s relevance is reinforced by multilingual service, claims guidance, and advisory on add-ons that matter for diverse expatriate buyers. Aggregators and comparison portals delivered the fastest growth at 11.62% CAGR over 2026 to 2031 as real-time APIs and digital identity compressed the time from quote to bind to under a minute for standard risks on leading platforms. Platform scale is visible in public metrics shared by one of the largest aggregators, which reports over 1 million cumulative policies and multi-million active users in the UAE. The combined result is a more efficient top of the funnel for the UAE motor insurance market, where digital channels now account for a growing portion of new business while brokers maintain a central role in advising on complex endorsements and claims support. Price transparency on aggregators continues to push carriers toward service differentiation and claims speed as a way to protect margins despite tighter technical pricing.

Over the forecast, direct and aggregator flows will likely keep rising as carriers invest in first-party digital journeys and expand embedded partnerships in mobility ecosystems. The UAE motor insurance market size captured by digital origination is therefore positioned to increase, aided by lower friction and instant verification that eliminates manual review for standard risks. Broker carrier collaboration remains critical for complex accounts and for resolving claims disputes quickly, which sustains a hybrid omnichannel model. Carriers that align channel economics with customer lifetime value and claims experience can offset aggregator margin pressure with higher retention and cross-sell. The UAE motor insurance industry will continue to blend relationship-led advice with platform-led speed, anchored by consistent broker rules and secure data exchange.

By Vehicle Type: Fleet Electrification Accelerates Commercial Growth

Passenger cars accounted for 81.27% of exposure by unit count in 2025, while commercial vehicles, consisting of LCVs and M/HCVs, form a smaller base but are projected to grow at 9.14% CAGR to 2031 as ride-hailing, logistics, and autonomous pilots scale in large metros. Embedded cover in mobility platforms and negotiated fleet discounts yield scale that pulls more commercial vehicles into the insured pool, and autonomous pilots require bespoke liability that shifts risk to software and hardware performance. The UAE motor insurance market size attributable to commercial classes is projected to expand faster than private passenger lines through 2031 as platforms and logistics continue to scale. OEMs are also deploying ADAS across trims, which can temper frequency in certain accident types for both passenger and commercial lines, and that supports carrier repricing where behavior and claims data confirm risk improvement. As EV penetration rises from a low base, battery and component coverage remain focal points for underwriting and claims, especially for vehicles used in intensive urban duty cycles.

Product and pricing strategies for fleets emphasize telematics, performance dashboards, and controlled repair networks to contain downtime and cost. Parametric options for water exposure and weather-driven hazards are being piloted, which may suit fleets that need predictable cash flows for severe but well-defined events. Insurers that integrate granular geospatial inputs into underwriting can refine commercial pricing by corridor and time of day, enhancing selection within the UAE motor insurance market. As autonomous features advance and pilot zones widen, liability frameworks will evolve and likely involve OEM warranties for software behaviors that affect underwriting assumptions. This shift creates new opportunities for specialist carriers and partnerships across the vehicle and technology value chain.

By Vehicle Age: Used-Vehicle Dominance Reflects Affordability Pressures

Used vehicles held 63.58% of exposure in 2025 and are forecast to grow at 9.74% CAGR through 2031, giving them the highest momentum by age band within the UAE motor insurance market. The April 2024 floods materially changed buyer behavior in older vehicle cohorts, leading to stronger attachment of comprehensive endorsements where owners weighed the risk of total loss against supplemental premium, and leading takaful carriers documented rapid settlement of flood claims that reinforced trust in broader coverage. Financing new purchases remains comprehensive non negotiable for many buyers since lenders require the insurer to list the financier as loss payee, which stabilizes demand for full cover during renewal windows. These patterns maintain the premium quality of the UAE motor insurance market size across both new and used segments, as comprehensive remains central to risk protection in flood-aware districts.

Insurers manage repair inflation for older vehicles by expanding direct repair networks that cap labor rates and ensure genuine parts, which reduces cycle time and leakage and has been highlighted by large carriers in their 2025 disclosures. Agency repair endorsements are gaining traction among used vehicle owners who want authorized garages and factory-trained technicians, and carriers combine these endorsements with roadside support and courtesy cars to protect mobility during repairs. Usage-based and connected car programs are also helping align premium to exposure for lower mileage used vehicles, and carriers are publishing customer-facing dashboards that explain trip scoring and data controls to encourage adoption under the UAE’s consent framework. For new vehicles, ADAS and connected features reduce certain low-speed collision types and support competitive pricing for safer cohorts while preserving full reimbursement features through zero depreciation options on parts in early years. The UAE motor insurance market share of used vehicles is likely to remain high through 2031 as installment payment options, clearer product features, and faster digital claims keep protection accessible for price-sensitive owners under consistent supervisory oversight.

Geography Analysis

The UAE motor insurance market is national in scope and regulated under a single supervisory framework, yet product mix and technical pricing vary by emirate due to differences in urban density, mobility platforms, and infrastructure. Dubai and Abu Dhabi anchor the largest premium pools in 2026, with autonomous pilots and e-hailing shaping demand for commercial endorsements and advanced liability structures tied to software and sensors. Aggregator usage and instant policy issuance are more prevalent in large metro areas where digital identity and API integrations are a normal part of transactions, and this supports faster growth in online origination. Across the country, consistent enforcement and centralized verification are pushing TPL compliance to near universal levels at registration and renewal, which stabilizes the base for premium growth. Through the forecast, the UAE motor insurance market size in metro emirates is supported by platform fleets, luxury segments, and data-enabled products that raise average premiums per policy.

Sharjah and the Northern Emirates show growing attachment to comprehensive cover as climate-related investments and customer awareness bring flood risk into pricing conversations. Used vehicle density is high in these markets, and digital acquisition is increasing where aggregators surface competitively priced comprehensive options with verified add-ons and service features. Improved claims transparency and faster settlement times, published by several leading carriers, have reinforced trust, particularly after 2024 flood claims were settled at high acceptance rates by takaful and conventional players. For 2026 and beyond, the UAE motor insurance market size in these emirates is likely to expand as distribution becomes more convenient and as product features align with local risk. Collaboration between carriers and local repair networks will continue to matter because parts access and labor capacity constrain claim cycle times during event peaks.

Regulatory oversight and enforcement apply uniformly nationwide, and 2026 brought visible supervisory action on solvency and conduct that underscores capital strength as a policy goal. The rulebook clarifies conduct standards for brokers, premium remittance, and claims timelines, and this improves customer protection and reduces counterparty risk. As carriers lift investment in data, AI claims, and onshore storage to comply with consent requirements, the UAE motor insurance market can deploy usage-based and parametric options with clearer governance. Product and pricing innovation will remain most visible in larger emirates due to scale, although regulatory uniformity ensures benefits diffuse nationally with a short lag. The overall outcome is steady national growth with metro-led digital advances and broader access to comprehensive protection across all emirates.

Competitive Landscape

The UAE motor insurance market is moderately fragmented and led by scale carriers with strong capital and technology investment, while a long tail of mid-size players competes through niche positioning and digital speed. Leading companies published record 2025 earnings and highlighted AI-driven claims, portfolio repricing, and disciplined distribution as the drivers of improved profitability, which sets a high bar for service levels in 2026. Takaful operators posted double-digit growth and maintained strong financial strength ratings, reinforcing the appeal of Shariah-compliant structures to individuals and corporates that want profit sharing and ethical screens. Newer entrants have introduced parametric, and Web3-enabled policies that automate settlement when verified triggers are met, reducing both cost and cycle time, and these products have cleared regulatory approval in the UAE [2]Liva Insurance, “Parametric and Web3 Motor Insurance Approval,” Liva Insurance News, liva.ae. Carriers also report solvency well above minimum thresholds, adding resilience to portfolios that now include more climate-exposed risks than before 2024.

Strategic partnerships are central to distribution and claim modernization in 2026. Large aggregators supply reach and price transparency that expand the top of the funnel, while carriers integrate their quote engines and identity verification to bind policies in under a minute, where risk is standard. Partnerships with mobility platforms have embedded motor cover into onboarding flows and created tailored liability products for autonomous pilots, which reflects the UAE’s positioning on advanced mobility [3]Uber, “Uber and WeRide Launch Autonomous Robotaxi Service in Dubai,” Uber Investor Relations, investor.uber.com. Several carriers are publishing service innovations, including instant Orange Card issuance, and AI-assisted claims that cut settlement from a week to a few days or less, and those features are increasingly visible to consumers on aggregator comparison pages. As margins face pressure from transparent pricing, carriers are leaning on customer experience and fast claims to defend renewal rates and cross-sell affinity products.

Technology investment is now a budgeted priority across the sector and concentrates on three areas, namely telematics and data governance, AI claims engines, and front-end digital experiences. Insurers highlight reduced process times, better fraud detection, and improved Net Promoter Scores where these tools are in production. Capital allocation to onshore data storage and consent management is rising as usage-based options grow, and compliance is a shared priority among large carriers and takaful operators. Beyond core products, some carriers are testing crypto-enabled wallets for premium payment and claims disbursement to serve specific customer communities, and these initiatives are live in 2026 with specialist custody partners. The resulting landscape rewards scale, speed, and solvency, which together improve the customer proposition and keep the UAE motor insurance market on an innovation track.

United Arab Emirates Motor Insurance Industry Leaders

Orient Insurance PJSC

Sukoon Insurance

GIG Gulf

Abu Dhabi National Insurance Company (ADNIC)

Emirates Insurance Company (EIC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Policybazaar.ae and Watania Takaful launched PB Auto Care Advantage with garage backed repairs and roadside assistance as bundled value additions. The plan addresses customer pain points on claim settlement and out of pocket repair risk. The partners highlighted an authorized garage network to support service levels on a scale.

- January 2026: Dubai Insurance Company launched a crypto enabled wallet in partnership with Zodia Custody to support premium payments and claims payouts in select digital assets. The initiative targets customers in financial centers that use blockchain technologies. The deployment adds a new payment option within a regulated framework.

- December 2025: Liva Insurance announced a one year partnership with Salik that delivered instant motor insurance quotes to a large toll gate user base. The tie up generated significant quotations and sped renewals with a full digital flow. The partnership showcases cross ecosystem distribution innovation.

- March 2025: GIG Gulf launched instant Orange Card access with UAE PASS login on its MyGIG Car platform. The release enables customers to quote, bind, and download cross border cards in under a minute. The update illustrates how identity and API connectivity transform the customer journey.

United Arab Emirates Motor Insurance Market Report Scope

Motor insurance is a financial product that provides coverage for vehicles, including cars, trucks, and motorcycles, against physical damage or injuries to drivers and passengers resulting from traffic accidents, offering financial protection and reducing risks associated with road transportation.

The UAE motor insurance market report is segmented by coverage type (third-party liability insurance, comprehensive coverage), distribution channel (insurance agents/brokers, direct sales, bancassurance, embedded/platform partnerships, aggregators & comparison portals), vehicle type (passenger cars, two-wheelers, light commercial vehicles, medium & heavy commercial vehicles), and vehicle age (new vehicles, used vehicles). The market forecasts are provided in terms of value (USD).

By Coverage Type

| Third-Party Liability Insurance |

| Comprehensive Coverage |

By Distribution Channel

| Insurance Agents / Brokers |

| Direct Sales |

| Bancassurance |

| Embedded / Platform Partnerships |

| Aggregators & Comparison Portals |

By Vehicle Type

| Passenger Cars |

| Two-Wheelers |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

By Vehicle Age

| New Vehicles |

| Used Vehicles |

| By Coverage Type | Third-Party Liability Insurance |

| Comprehensive Coverage | |

| By Distribution Channel | Insurance Agents / Brokers |

| Direct Sales | |

| Bancassurance | |

| Embedded / Platform Partnerships | |

| Aggregators & Comparison Portals | |

| By Vehicle Type | Passenger Cars |

| Two-Wheelers | |

| Light Commercial Vehicles | |

| Medium & Heavy Commercial Vehicles | |

| By Vehicle Age | New Vehicles |

| Used Vehicles |

Key Questions Answered in the Report

What is the UAE motor insurance market outlook to 2031?

The UAE motor insurance market size is set to rise from USD 1.78 billion in 2025 to USD 2.86 billion by 2031 at an 8.25% CAGR, supported by stronger enforcement, comprehensive coverage adoption, and digital origination.

Which coverage category leads and why in the UAE motor insurance market?

Comprehensive policies lead due to post flood risk awareness and product innovation, such as parametric triggers for water events, supported by fast claims handling, documented by leading takaful and conventional carriers.

How is regulation shaping distribution in the UAE motor insurance market?

Broker regulation requires direct premium remittance to insurers and faster client response, while digital identity enables instant online binding, which together expand safe and efficient origination.

What role do mobility platforms play in the UAE motor insurance market?

Platforms embed commercial cover during onboarding for gig drivers and fleets, and autonomous pilots in Dubai require bespoke liability structures codeveloped with leading carriers.

How are claims processes evolving in the UAE motor insurance market?

Carriers are deploying AI‑assisted triage and direct repair networks that reduce settlement times from days to hours in simple cases, and identity‑enabled journeys now issue key documents instantly.

What constrains growth in the UAE motor insurance market in 2026?

Repair‑cost inflation, reinsurance hardening after 2024 floods, and privacy and consent hurdles for telematics adoption moderate growth, although steady enforcement and innovation keep the trajectory positive.

Page last updated on: