Estonia Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

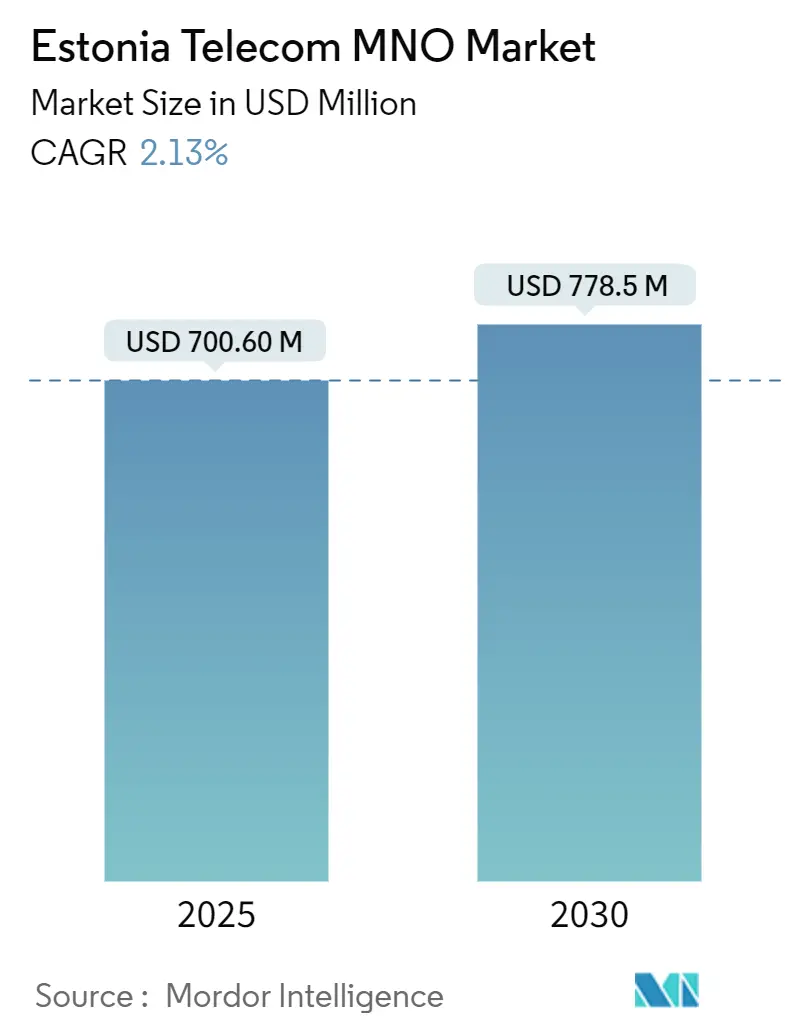

| Market Size (2025) | USD 700.60 Million |

| Market Size (2030) | USD 778.5 Million |

| Growth Rate (2025 - 2030) | 2.13% CAGR |

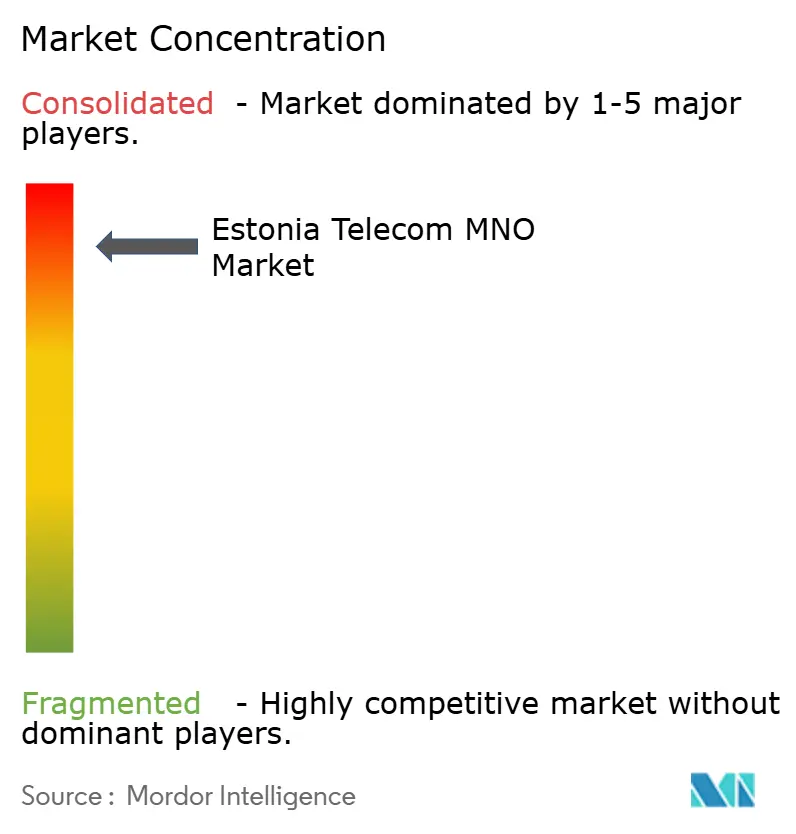

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Estonia Telecom MNO Market Analysis by Mordor Intelligence

The Estonian Telecom MNO Market size is estimated at USD 700.60 million in 2025, and is expected to reach USD 778.5 million by 2030, at a CAGR of 2.13% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 2.52 million subscribers in 2025 to 2.78 million subscribers by 2030, at a CAGR of 2.01% during the forecast period (2025-2030). Estonia's evolving role as a Baltic technology testbed is underscored by a shift towards high-value connectivity, even as headline growth remains steady. A confluence of factors, including enterprise digitalization, the accelerating rollout of 5G, and EU-backed fiber projects, is driving up demand for premium services. Simultaneously, the surge in video streaming and the establishment of cross-border data corridors are amplifying capacity needs. The competitive landscape is dominated by Telia Estonia, Elisa Eesti, and Tele2 Eesti, all of which are increasingly focusing on secure IoT and low-latency solutions to safeguard their profit margins. While challenges such as infrastructure cost inflation and rural last-mile constraints pose hurdles to expansion, the resilience of Estonia's telecom market is bolstered by ongoing government-industry collaboration and significant investments from major vendors.

Key Report Takeaways

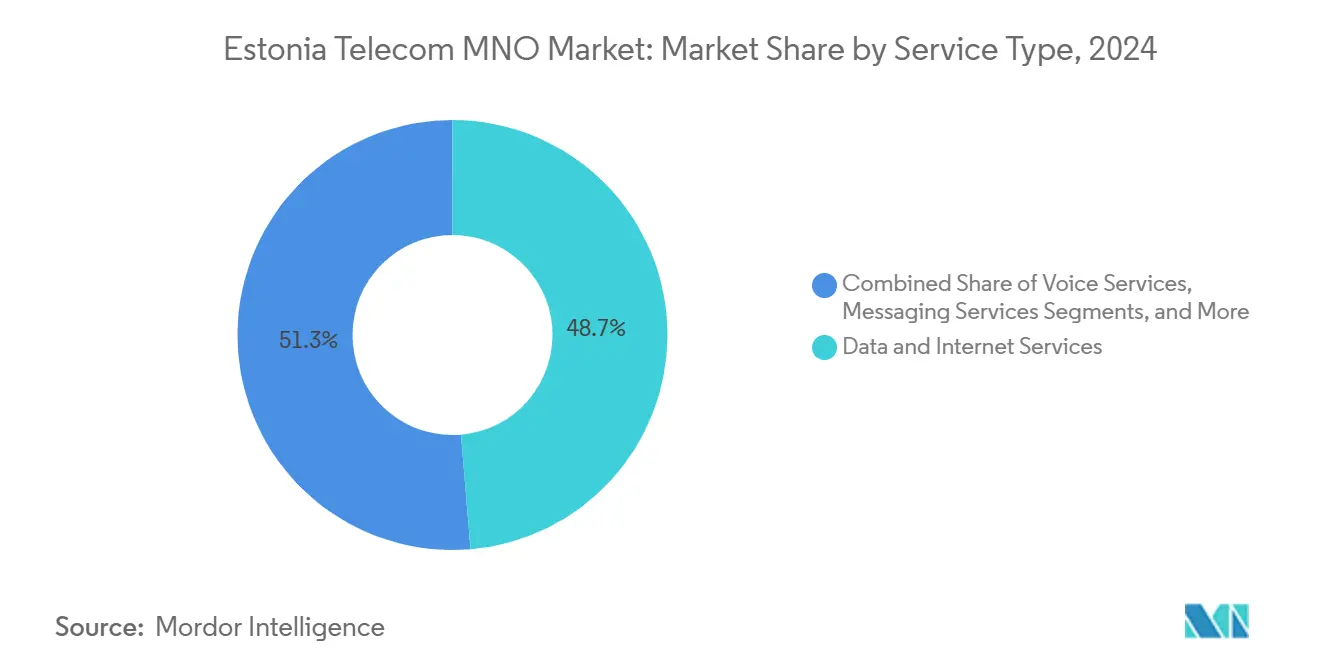

- By service type, data and internet services accounted for 48.66% of the Estonian telecom market share in 2024, whereas IoT and M2M services are projected to grow at a 2.57% CAGR through 2030.

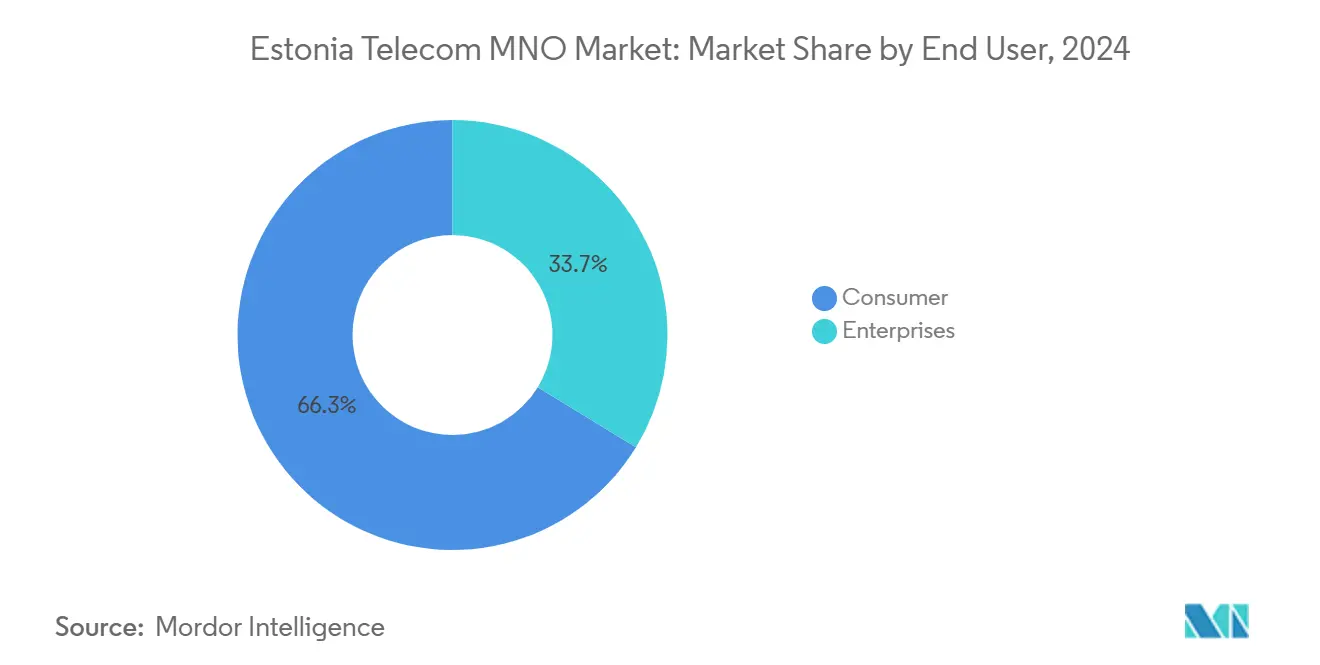

- By end user, the consumer segment commanded 66.26% of the Estonian telecom MNO market size in 2024, while the enterprise segment is expected to expand at a 2.22% CAGR through 2030.

Estonia Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained 5G Rollout and 77% Population Coverage | +0.8% | Tallinn, Tartu, Pärnu | Medium term (2-4 years) |

| EU-funded Rural Fiber Backbone (EstWin Phase III) | +0.6% | Rural Estonia | Long term (≥ 4 years) |

| Surging Enterprise Demand for Secure IoT Connectivity | +0.7% | Tallinn-Helsinki corridor | Medium term (2-4 years) |

| OTT Video Uptake Pushing >35 % Y-o-Y Data Traffic | +0.5% | Urban Estonia | Short term (≤ 2 years) |

| NATO Cyber-range Projects Requiring Ultra-low-latency Links | +0.3% | Defence sites | Long term (≥ 4 years) |

| Tallinn-Helsinki Submarine Cable Upgrade Enabling 400 Gbps Paths | +0.4% | Cross-border corridor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustained 5G Rollout and 77% Population Coverage

Rapid spectrum release, network-sharing accords and targeted urban builds drove Telia Estonia to reach 77% population coverage in 2024, with a 95% target by 2026. Elisa Eesti introduced 5.5G features that unlock industrial automation use-cases and augmented-reality services. Priority deployment along economic corridors builds premium ARPU streams from private networks and fixed wireless access. Densification spurs demand for micro-cells and edge compute nodes, attracting neutral-host infrastructure providers. The wider footprint allows operators to embed 5G into bundled consumer plans, stabilising churn even as price competition intensifies. [1]Telia Company, “2023 Annual and Sustainability Report,” TELIACOMPANY.COM

EU-funded Rural Fiber Backbone (EstWin Phase III)

EstWin III adds roughly 6,500 km of open-access fiber, cutting backhaul costs for rural base stations and pushing ultrafast internet to within 1.5 km of every household. Mobile network operators piggyback on the passive middle-mile to extend 5G far beyond commercially viable footprints. Wholesale access lowers capex, enabling voice-over-Wi-Fi, precision agriculture, and remote monitoring services that were previously unviable. Reduced satellite reliance improves latency and boosts customer satisfaction, shrinking the rural-urban digital gap. [2]European Commission, “Estonia 2025 Digital Decade Country Report,” DIGITAL-STRATEGY.EC.EUROPA.EU

Surging Enterprise Demand for Secure IoT Connectivity

Industry 4.0 agendas across manufacturing and logistics accelerate the adoption of NB-IoT and LTE-M. Elisa Eesti’s NB-IoT network now covers 95% of Estonia, while Sigfox low-power wide-area overlays from Telia provide complementary options. Enterprises pay premiums for encrypted, carrier-grade links that meet ISO 27001 and defense-related standards. Use cases range from predictive maintenance in smart factories to cross-border asset tracking between Tallinn and Helsinki. Estonia’s cyber-defense pedigree and supportive regulation attract multinational clients seeking trusted connectivity for mission-critical data flows.

OTT Video Uptake Pushing >35 % Y-o-Y Data Traffic

Streaming services drive 70% of mobile traffic, with average monthly usage climbing toward 75 GB by 2030. Telia’s Netflix bundles and zero-rating of local OTT platforms raise customer lifetime value, while higher video resolutions and short-form content compel operators to invest in carrier-grade CDN nodes. The data surge justifies unlimited plans and stimulates further 5G spectrum utilisation, yet also increases backhaul OPEX and heightens the need for network optimisation analytics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Retail Broadband Prices vs. Latvia and Lithuania | –0.4% | Nationwide | Short term (≤ 2 years) |

| Ageing Copper Last-mile in Small Municipalities | –0.3% | Rural Estonia | Medium term (2-4 years) |

| Scarcity of Skilled Tower-riggers Delaying 700 MHz Refarming | –0.2% | Nationwide | Short term (≤ 2 years) |

| Rising Electricity Costs Eroding 5G FWA Margins | –0.3% | Rural 5G sites | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Retail Broadband Prices vs. Latvia and Lithuania

Average 4G data costs of USD 1.50 PPP per GB outstrip neighbouring Baltic benchmarks, inviting cross-border price comparisons that intensify churn risk. Operators juggle higher power, spectrum, and labor costs, while limited network-sharing keeps per-site OPEX elevated. As 5G tariffs launch at premiums, price-sensitive segments may defer upgrades, nudging operators to explore flexible data-wallet models and family bundles. [3]Point Topic, “European Mobile Broadband Tariffs in Q4 2024,” POINT-TOPIC.COM

Ageing Copper Last-mile in Small Municipalities

Roughly 160,000 households remain tied to legacy DSL loops that cap speeds, constrain video quality, and stifle smart-home adoption. Fiber build-out economics deter private investment in sparsely populated areas, forcing reliance on public subsidies or fixed wireless alternatives. Service disparities risk widening the digital divide and blunt ARPU uplift from premium tiers until copper is fully retired or over-built. [4]Ivar Soopan, “Kiire internet on 160 000 perele vaid unistuseks,” MAALEHT.DELFI.EE

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: IoT and M2M Outpace Data Leadership

IoT and M2M services are forecast to grow at a 2.57% CAGR through 2030, spurred by demand for secure sensor connectivity across Estonia’s industrial base. Data and Internet services nevertheless retained 48.66% of the Estonia telecom MNO market share in 2024, supporting stable cash flows needed for 5G investment. Falling voice ARPU and messaging cannibalization by OTT platforms continue, but bundling strategies and OTT partnerships cushion revenue declines. Elisa Eesti’s cloud-based SIM management and Telia’s device-agnostic platforms deepen client lock-in and elevate average contract tenures. Diversified value-added services, including roaming hubs and wholesale transit, round out revenue portfolios and limit exposure to domestic price squeezes.

Operators leverage Estonia’s cybersecurity brand to position managed IoT connectivity at premium price points. Use-cases span predictive maintenance, cold-chain monitoring, and defense telemetry, with average ARPU far exceeding consumer smartphone lines. Edge analytics and private network offerings unlock incremental revenue, transforming connectivity from a commodity into an embedded component of digital transformation packages. As 3G sunsets and 2G exits post-2029, spectrum refarming will further expand narrow-band IoT capacity, supporting mass-device footprints without compromising headline speeds for mobile broadband users.

By End User: Enterprise Momentum Reshapes Revenue Mix

Consumer subscriptions accounted for 66.26% of the Estonia telecom MNO market size in 2024, yet enterprise lines are projected to rise at a 2.22% CAGR to 2030, signaling a gradual but decisive pivot toward business customers. Industrial clusters along the Tallinn-Tartu-Narva axis require deterministic latency and end-to-end encryption, catalyzing demand for bespoke SLA-backed packages. Cross-border manufacturers integrate Estonian plants with Nordic ERP platforms, adding to the need for seamless private WANs. Higher willingness to pay and low churn translate into margin uplift that offsets consumer price deflation.

Consumer demand nonetheless stays robust on the back of unlimited data plans, handset instalment schemes, and video-centric bundles. Average usage expands in lockstep with 5G coverage, while device penetration surpasses 140%, aided by secondary SIMs and IoT wearables. Operators safeguard consumer ARPU through loyalty programs, streaming add-ons, and fintech tie-ins, even as they channel incremental capex toward enterprise-grade network slices and campus deployments.

Geography Analysis

Urban centers generate the lion’s share of Estonia telecom MNO market revenue, with Tallinn alone contributing nearly half of mobile service income due to dense populations and affluent early adopters. The commercial triangle linking Tallinn, Tartu, and Pärnu secures rapid 5G deployment, enabling operators to market low-latency packages to tech firms and digital start-ups. International traffic along the Tallinn-Helsinki corridor benefits from the upgraded 400 Gbps submarine cable, allowing Estonian operators to sell resilient wholesale links to Nordic carriers and cloud providers.

Rural Estonia lags in last-mile quality but gains new prospects from EstWin III fiber backhaul. Operators thus extend 5G fixed wireless access to farmsteads and small enterprises, mitigating copper bottlenecks and capturing incremental service revenue. Government subsidies and open-access rules lower financial barriers, yet rising electricity costs elevate OPEX at sparsely populated macro-sites. Pilot precision-agriculture projects showcase 5G’s role in yield optimization, winning political support for accelerated rural roll-outs.

Cross-border spectrum coordination with Finland maintains seamless roaming and positions Estonia as a data turnkey for Nordic multinationals. Competitive tariffs for transit traffic boost non-core earnings and promote the Estonia telecom MNO market as a regional connectivity hub. The country’s compact geography compels aggressive network overlapping, fostering quality-of-service leadership but compressing retail prices in densely contested zones.

Competitive Landscape

The Estonia telecom MNO industry is an oligopoly led by Telia Estonia, Elisa Eesti, and Tele2 Eesti. Combined, the three account for virtually the entire subscriber base, enabling scale efficiencies yet locking the market in a perpetual contest over network quality and tariffs. Elisa tops Speedtest rankings at 100.13 Mbps download, leveraging early carrier aggregation on 3.5 GHz to win high-usage customers. Telia responds by pairing nationwide 5G coverage with solar-powered base stations to reduce energy overhead, echoing wider corporate sustainability goals. Tele2 targets cost-sensitive users, launching digital-only propositions and value bundles to defend its share.

Strategic focus shifts toward enterprise verticals, manufacturing, logistics, and defense, where secure IoT, private networks, and managed cloud edge services offer thicker margins. Ericsson’s EUR 150 million smart-manufacturing plant in Tallinn provides a local research and development ecosystem, catalyzing operator partnerships for 5G-enabled factory automation. Neutral-host tower companies eye build-to-suit opportunities in underserved rural areas, although entrenched ownership of passive assets keeps barriers to entry high.

Consolidation rumours ebb and flow, yet regulatory preference for three-player competition stalls mergers. Instead, network-sharing deals and infrastructure JVs emerge, balancing capex containment with service differentiation. Operators increasingly tap wholesale fibre and cross-border capacity to monetize excess backbone assets, smoothing revenue volatility in the maturing consumer segment. Innovation imperatives nudge all players toward AI-driven network optimization, green energy sourcing, and flexible product-bundling engines to maintain user experience leadership.

Estonia Telecom MNO Industry Leaders

Elisa Eesti AS

Telia Estonia

Tele2 Eesti AS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: European Space Agency selected Estonia to host a new space-cybersecurity test ground, backing national ambitions to lead secure connectivity research.

- October 2024: Telia Estonia confirmed its 2G switch-off will not occur before 2029, reassuring industrial telemetry users.

- March 2024: Telia Estonia advanced fiber builds to 9,000 new homes, bolstering fixed-broadband reach.

- February 2024: Estonia completed allocation of 700 MHz and 3.5 GHz pioneer bands, clearing the runway for expanded 5G deployments.

Estonia Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the current value of the Estonia telecom MNO market?

The Estonia telecom MNO market size is USD 0.70 billion in 2025.

How fast is the market expected to grow?

It is forecast to expand at a 2.13% CAGR, reaching USD 0.77 billion by 2030.

Which service segment is growing the quickest?

IoT and M2M services are projected to post the fastest growth, with a 2.57% CAGR through 2030.

What share do consumers hold in the market?

Consumers accounted for 66.26% of the Estonia telecom MNO market size in 2024.

Who are the main players in the Estonia telecom MNO industry?

Telia Estonia, Elisa Eesti and Tele2 Eesti collectively dominate the market, with Elisa currently leading on mobile data speeds.

Page last updated on: