Cutter Staplers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

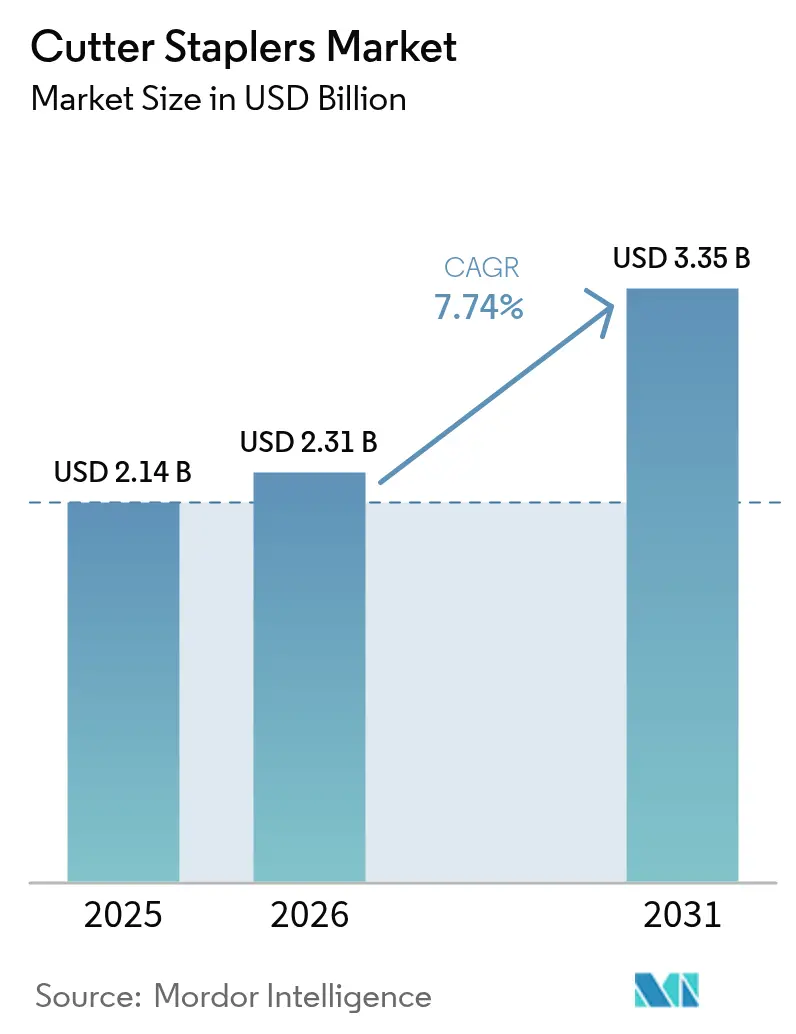

| Market Size (2026) | USD 2.31 Billion |

| Market Size (2031) | USD 3.35 Billion |

| Growth Rate (2026 - 2031) | 7.74% CAGR |

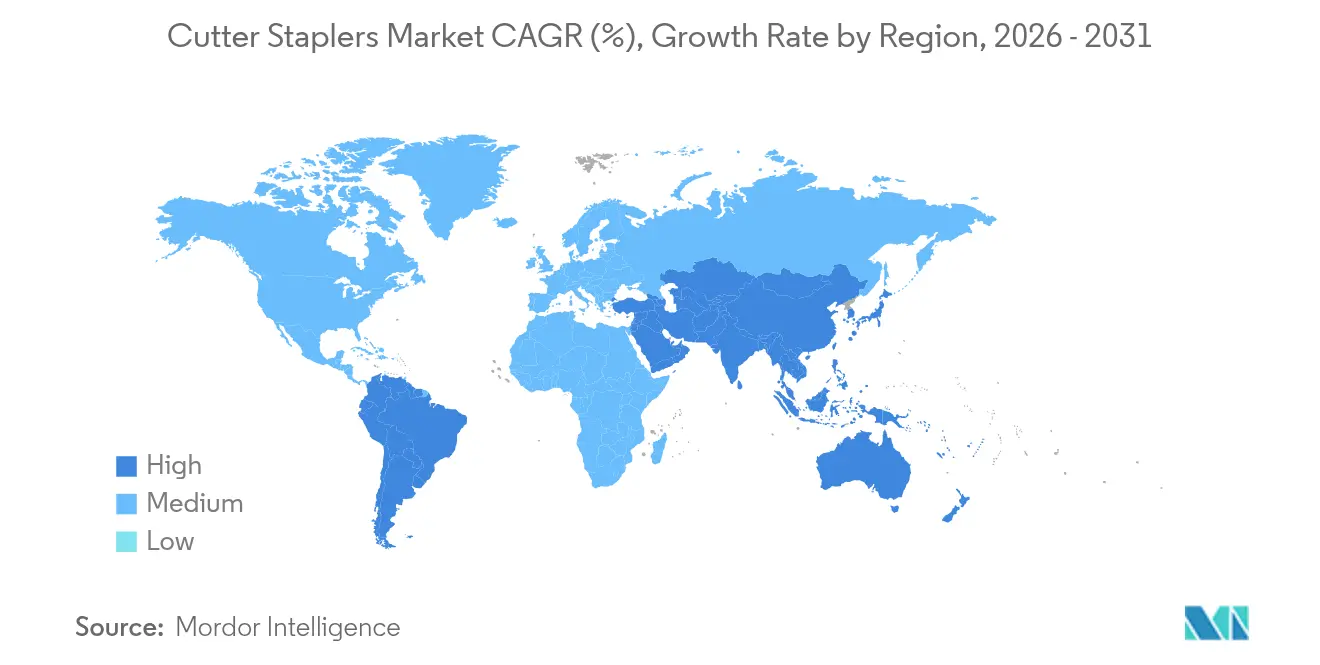

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

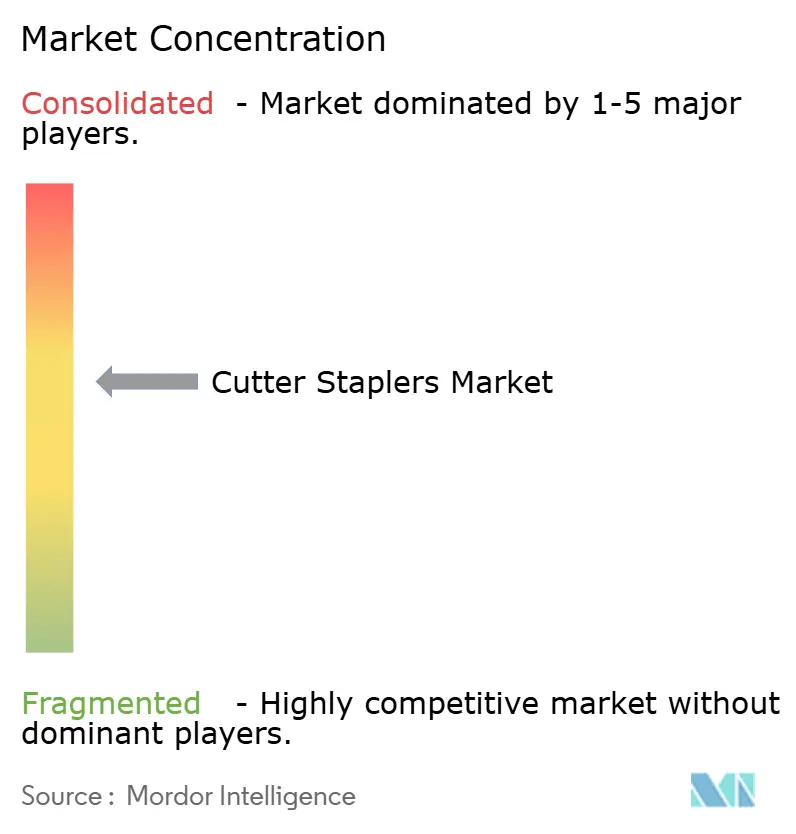

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cutter Staplers Market Analysis by Mordor Intelligence

The cutter staplers market size is expected to grow from USD 2.14 billion in 2025 to USD 2.31 billion in 2026 and is forecast to reach USD 3.35 billion by 2031 at 7.74% CAGR over 2026-2031. Elevated bariatric procedure volumes, robot-compatible instruments, and the universal shift to minimally invasive surgery stimulate demand for precision stapling devices. Hospitals and ambulatory surgical centers increasingly choose powered articulating platforms because these shorten operating times and lower complication costs. Yet single-use devices dominate procurement owing to strict infection-control protocols, even as physicians and regulators weigh sustainability concerns. North America maintains technological leadership through robust reimbursement and early adoption, while Asia-Pacific posts the fastest expansion as elective surgery access broadens. Heightened FDA oversight, including the move to Class II classification in 2026, is set to intensify competition around validated safety performance.

Key Report Takeaways

- By product type, endo cutters held 45.81% of cutter staplers market share in 2025 and are tracking an 7.92% CAGR to 2031.

- By mechanism, manual systems retained 62.55% share of the cutter staplers market size in 2025; powered variants are forecast to grow 8.64% annually.

- By surgical approach, minimally invasive procedures accounted for 60.02% of the cutter staplers market size in 2025 and will expand at an 7.98% CAGR.

- By usability, disposable platforms led with 70.21% share of the cutter staplers market size in 2025, although reusable devices face 7.81% growth.

- By end-user, hospitals commanded 60.42% of the cutter staplers market size in 2025, while ambulatory surgical centers record the highest 8.32% CAGR.

- By geography, North America captured 34.11% revenue in 2025; Asia-Pacific is advancing at an 8.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cutter Staplers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Minimally Invasive Surgery | +2.1% | Global, led by developed markets with spillover to emerging economies | Long term (≥ 4 years) |

| Rise in Bariatric & Metabolic Surgeries | +1.8% | Global, with concentration in North America and emerging APAC markets | Medium term (2-4 years) |

| Technological Advances in Powered & Articulating Staplers | +1.5% | North America & EU core markets, expanding to APAC | Medium term (2-4 years) |

| Shift Toward Outpatient GI Stapling in ASCs | +1.2% | North America primarily, with early adoption in select EU markets | Short term (≤ 2 years) |

| Integration with Surgical Robotics Platforms | +0.9% | High-income markets globally, concentrated in urban centers | Long term (≥ 4 years) |

| Demand for Reusable Staplers in Low-Resource Markets | +0.4% | APAC, MEA, and Latin America emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Minimally Invasive Surgery

Laparoscopic techniques now dominate many specialties, with appendicectomy utilization rising[1]Joshua Kirkpatrick, “The increasing use of minimally invasive surgery in acute general surgical conditions: A decade of results from a national data set,” Surgery, surgjournal.com from 83% to 95% between 2013 and 2022 in advanced markets. Surgeons prefer staplers over sutures because staple lines reduce tissue trauma and accelerate recovery. Powered platforms trim thoracic operating time by 21 minutes and save USD 8,249 per case, strengthening the economic argument. Robotics magnifies this benefit, demonstrated by FDA-cleared single-port staplers that resolve access limitations. Curriculum changes in residency programs reinforce device familiarity, cementing long-term growth prospects for the cutter staplers market.

Rise in Bariatric & Metabolic Surgeries

United States bariatric volumes climbed 6.5% from 2021 to 2022, surpassing 280,000 procedures[2]Benjamin Clapp, “American Society for Metabolic and Bariatric Surgery 2022 estimate of metabolic and bariatric procedures performed in the United States,” Surgery for Obesity and Related Diseases, soard.org. Sleeve gastrectomy now constitutes 57.4% of cases, standardizing stapler needs around gastric transection. Robot-assisted workflows, which already represent 30% of metabolic surgeries, demand staplers tailored to robotic articulation. Manufacturers profit from economies of scale as procedure uniformity allows high-volume reload production. With eligible surgical candidates treated at only 1%, the cutter staplers market retains vast expansion runway as payer approvals broaden.

Technological Advances in Powered & Articulating Staplers

Clinical trials show powered colorectal staplers cut anastomotic leak rates by 85% versus manual tools. Smart compression sensors, such as SmartFire, adjust firing force to tissue thickness in real time, improving staple formation consistency. Gripping Surface Technology halves intraoperative bleeding compared with conventional jaws, enhancing visualization. Hospitals reconcile higher acquisition costs with downstream savings from fewer complications, particularly in high-volume centers. Patent filings on AI-driven firing profiles indicate that real-time tissue analytics will anchor the next wave of cutter staplers market differentiation.

Shift Toward Outpatient GI Stapling in ASCs

Medicare boosted ASC payments 15.4% in 2023[3]MedPAC Report to Congress, “Ambulatory Surgical Center Payment Update,” medpac.gov , triggering rapid migration of gastroenterology procedures to outpatient suites. The nation hosts 6,308 ASCs treating 3.4 million Medicare beneficiaries, driving procurement toward dependable, multi-procedure staplers that streamline case turnover. Device versatility outweighs advanced analytics in this setting because staff training time is limited. Vendors that package intuitive reload color coding and simple articulation earn share. As ASC caseload complexity rises, demand shifts toward powered options that deliver hospital-grade outcomes without compromising workflow efficiency.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infection Risks & Product Recalls | -1.4% | Global, with heightened scrutiny in North America and EU | Short term (≤ 2 years) |

| Alternative Closure Technologies | -0.8% | Developed markets with advanced surgical capabilities | Medium term (2-4 years) |

| Titanium Price Volatility | -0.6% | Global manufacturing impact, concentrated in Asia-Pacific production | Short term (≤ 2 years) |

| Sustainability-Driven Scrutiny on Single-Use Devices | -0.5% | EU and North America leading, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infection Risks & Product Recalls

The FDA logged more than 41,000 stapler-related adverse events between 2011 and 2018, including 366 deaths. Recent Class I recalls, such as Covidien’s TriStaple 2.0 Black reload, underscore manufacturing vulnerabilities. Hidden malfunction reports stored in non-public databases erode clinician confidence and complicate purchasing decisions. Pending Class II requirements mandate pre-market submissions and performance testing, favoring companies with robust design-control systems. Market leaders channel R&D funds toward redundant safety sensors and user-alert features to rebuild trust.

Alternative Closure Technologies

Zip-type polymer devices and energy-based sealers compete for superficial and vascular closure, touting lower infection risk and foreign-body burden. Hospitals weigh total cost of care rather than device price alone, so staplers must demonstrate superior hemostasis and shorter room turnover. Where alternatives achieve parity, volume allocation shifts away from metal staples, trimming overall growth potential for the cutter staplers market. Manufacturers respond by integrating leak-test algorithms and adjunct sealants to reinforce comparative advantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Endo Cutters Lead Innovation Drive

Endo cutter staplers accounted for 45.81% of the cutter staplers market share in 2025 and are scaling at an 7.92% CAGR as laparoscopic and robotic procedures proliferate. Their slim, articulating jaws navigate confined pelvic and thoracic spaces, making them indispensable in bariatric, colorectal, and thoracic oncology cases. Open cutters remain essential for trauma surgery where speed trumps port access, but volume growth is subdued due to declining open case mix. Specialized circular and custom staplers serve niche reconstructions such as low rectal anastomoses, maintaining modest but stable demand.

Manufacturers race to differentiate endo models through torque-controlled firing and adaptive compression. Intuitive Surgical’s SP SureForm 45 integrates SmartFire sensors that adjust staple height 1,000 times per second, reducing leak risk. Johnson & Johnson data confirm a 47% leak reduction with the newest ECHELON Linear Cutter compared to previous generations. Hospitals value unified platforms that share reload colors and ergonomics across open and endo lines, simplifying staff training and inventory.

By Mechanism: Powered Technology Gains Momentum

Manual devices held 62.55% of the cutter staplers market size in 2025, reflecting decades of clinical familiarity and lower upfront cost. Yet powered units post the fastest 8.64% CAGR as surgeons prioritize reproducible staple formation in thick or variable tissue. A Chinese health-economic study showed powered reloads reduced adverse event management costs by ¥1,653 per case, outweighing higher purchase price. This evidence accelerates hospital conversion in high-acuity disciplines.

R&D efforts center on grip-enhancing tip designs and stepper-motor firing that delivers uniform compression. Trials reveal 73% fewer hemostasis-related complications with powered ECHELON devices relative to manual equivalents. As robotic consoles expand, powered handles with hands-free attachment further appeal to surgeons seeking ergonomic relief during lengthy procedures. Manual staplers continue serving low-resource environments and uncomplicated resections, preserving a sizeable yet shrinking portion of the cutter staplers market.

By Surgical Approach: Minimally Invasive Dominance Accelerates

Minimally invasive techniques captured 60.02% of the cutter staplers market share in 2025, advancing at an 7.98% CAGR, while open surgery proportionally recedes. Robot-assisted bariatric operations already comprise 30% of volume and spur demand for reloads capable of firing through 60° articulation without staple line thinning. Laparoscopic training modules embedded in residency curricula ensure a steady pipeline of surgeons fluent in port placement and stapler manipulation. Hospitals allocate capital budgets toward 4K laparoscopy towers and robotic arms, creating an ecosystem that intensifies stapler utilization.

Future growth hinges on single-port platforms that further reduce incision count. The FDA clearance of single-port staplers signals regulatory acceptance of these next-generation instruments. Open surgery retains necessity for emergent trauma and complex reconstructions where tactile feedback and wide exposure are pivotal. However, even hybrid approaches employ staplers to expedite bowel transection, maintaining relevance across techniques.

By Usability: Disposable Convenience Faces Sustainability Pressure

Disposable staplers dominated with 70.21% of the cutter staplers market size in 2025, bolstered by infection-control mandates that prohibit reprocessing in many jurisdictions. Their 7.81% CAGR persists as operating room managers favor ready-to-use instruments that eliminate sterilization queues. Nevertheless, environmental audits highlight 40% waste reduction and 99.7% lower greenhouse gas emissions when reusable platforms replace single-use equivalents. Cardinal Health’s reprocessing of 18 million single-use devices saved hospitals USD 412 million in 2022, evidencing an economic model for waste mitigation.

European tenders now include sustainability scoring, nudging buyers toward hybrid solutions where reusable handles mate with disposable reloads. Manufacturers compete by offering device-take-back programs and recycled-content packaging. As regulatory bodies in the EU and select US states contemplate single-use levies, vendors hedging with both categories protect share in the cutter staplers industry.

By End-User: ASCs Challenge Hospital Dominance

Hospitals retained 60.42% revenue in 2025 due to complex case handling and central purchasing. ASC volume, however, is expanding 8.32% annually, driven by favorable Medicare payment differentials and patient preference for outpatient recovery. Stapler procurement at ASCs prioritizes reliability, intuitive reload interchange, and compact tray sizes to fit smaller sterile cores. Vendors showcasing field-service programs and drop-shipment logistics win contracts.

As ASCs tackle higher-acuity cases such as laparoscopic colorectal resections, demand shifts toward powered articulating models once exclusive to tertiary hospitals. Suppliers aligning training resources and quick-connect reload designs position themselves to capture this ambulatory wave. International specialty clinics, especially in medical-tourism hubs, mirror ASC expectations, reinforcing the global impact on the cutter staplers market.

Geography Analysis

North America generated 34.11% of global revenue in 2025, supported by mature reimbursement and early technology adoption. Regional CAGR of 7.15% hinges on continued conversion to powered reloads and the Class II regulatory shift favoring quality-driven suppliers. Hospital consolidation amplifies purchasing leverage, prompting vendors to package multi-year service plans and training.

Asia-Pacific records the swiftest 8.41% CAGR, reflecting investments in surgical infrastructure across China, India, and ASEAN states. India’s medical device market is forecast at USD 50 billion by 2025, albeit 70% import-dependent, offering foreign manufacturers growth with appropriate price-tiering. China’s localization policies encourage joint ventures and technology transfer, while Japan’s hospitals prioritize premium-powered systems. Brazil, under ANVISA rules that accept certain US or EU approvals, streamlines entry for incumbents yet maintains stringent post-market audits.

Europe ranks second, with a 7.65% CAGR through 2031, propelled by aging demographics and evidence-based procurement. EU sustainability directives impose recycling targets that progressively influence single-use selection. Clinical societies publish guidance that emphasizes staple line integrity, raising the bar for post-market surveillance data. Suppliers fostering registries and real-world studies strengthen positioning. The Middle East and Africa lag but present pockets of demand aligned with national health insurance rollouts. Public tenders favor cost-effective reusable kits, compelling vendors to support regional refurbishing centers. Collectively, these dynamics ensure sustained global expansion for the cutter staplers market.

Regulatory Landscape

In the United States, internal-use surgical staplers are moving under tighter FDA oversight through reclassification actions that place certain surgical staplers into Class II with special controls, alongside FDA labeling recommendations for internal-use staplers and staples. This has raised expectations for performance testing, validated design controls, and post-market surveillance, particularly given the history of stapler-related adverse events and recalls referenced in the market context.

In Europe, Regulation (EU) 2017/745 (MDR) remains the central framework governing safety, performance, and technical documentation for market access, lifting the bar for clinical evaluation and vigilance activities across both disposable and reusable platforms. At the standards level, ISO 6335-2:2026 (published February 5, 2026) sets updated general requirements and testing guidance for single-use and reusable surgical staplers, creating a more uniform benchmark that manufacturers can map into design verification, sterilization and packaging validation, and supplier qualification programs.

Value Chain Analysis

The cutter staplers value chain starts with specialized raw materials and components, including titanium alloys for staples and high-spec stainless steels used in anvil and jaw structures, along with polymer housings and, for powered systems, motors, sensors, and electronics. Precision manufacturing and assembly rely on tightly controlled processes (for example, machining and forming of staple-forming pockets and anvils), followed by sterilization, packaging, and lot-level quality release, with verification work increasingly aligned to ISO 6335-2:2026 requirements for both single-use and reusable staplers.

Downstream, leading OEMs combine direct hospital selling with distributor networks and optimize access through large procurement channels such as Group Purchasing Organizations (GPOs), while also supporting clinical education and service. The business model is commonly anchored in proprietary reloads and cartridges that drive recurring revenue, making component qualification and continuity of supply critical. Switching to alternate materials or suppliers can trigger re-validation cycles that slow rapid reconfiguration after disruptions. Logistics and inventory execution are particularly important for high-turnover accounts such as hospitals and ambulatory surgical centers, where reliable availability of compatible reloads influences platform standardization decisions.

Competitive Landscape

Market leadership rests with Johnson & Johnson (Ethicon), Medtronic, and Intuitive Surgical, whose combined portfolios span manual, powered, and robotic formats. Ethicon’s ECHELON 3D stapling and Gripping Surface Technology delivered a 47% leak reduction, underpinning premium pricing. Medtronic’s acquisition of Fortimedix Surgical in 2024 broadened its advanced visualization and stapling toolkit. Intuitive Surgical’s SureForm family integrates SmartFire analytics for console-controlled tissue sensing, reinforcing its installed robotic base.

Competitive strategy emphasizes ecosystem lock-in through proprietary reloads and software updates. Patents on compression algorithms and AI feedback loops create barriers for late entrants. Sustainability emerges as a white-space where midsized players like Lexington Medical position reusable endo cutters while attracting private equity funding for scale. Alternative closure innovators threaten incumbent share in superficial and vascular niches, yet widespread surgeon retraining slows displacement.

Regulatory escalation heightens compliance costs, advantaging companies with established quality infrastructures. Recalls disproportionately harm smaller firms lacking redundancy in global inventory. Consequently, market concentration remains moderate, though adjacent technology entrants and sustainability disruptors keep competitive pressure high across the cutter staplers market.

Cutter Staplers Industry Leaders

B. Braun Melsungen AG

Intuitive Surgical Inc.

Johnson & Johnson Services, Inc.

Medtronic plc

Purple Surgical

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace sits at the intersection of powered stapling, higher articulation, and real-time feedback that supports consistent staple formation across variable tissue. Regulatory approvals and clearances are reinforcing this direction: Reach Surgical (Genesis MedTech) received CE Mark approval in April 2026 for the iREACH IRIS powered stapler featuring 90-degree articulation and Real-Time Firing Curve technology, and Fengh Medical received FDA 510(k) clearance (K242679) in October 2024 for disposable powered articulating endoscopic linear cutter staplers. These actions expand the set of commercially available powered options beyond the largest incumbents and give hospitals and ASCs more room to standardize minimally invasive and robotic-adjacent workflows.

A second opportunity area is portfolio design that reconciles infection-control preference for single-use with procurement pressure around sustainability and total cost. With disposable platforms holding 70.21% share in 2025 and purchasing committees increasingly scrutinizing waste, suppliers can differentiate via hybrid architectures (reusable handles with disposable reloads), validated reprocessing pathways, and packaging or take-back programs that fit tender scoring criteria. Broader adoption in cost-sensitive markets is also supported by price-tiered product families and localized supply arrangements, especially where import dependence is high and procurement favors reliable, simplified platforms as elective surgery capacity expands.

Recent Industry Developments

- May 2026: Meril Life Sciences registered multiple Mirus brand linear cutter and linear stapler reloads in the US FDA GUDID database. This expands the company's visible US device identification footprint for stapler consumables, supporting channel readiness and catalog-level adoption discussions with hospital supply teams. The move highlights how emerging manufacturers are building reload portfolios alongside compliance documentation to compete in recurring-consumables segments.

- April 2025: Intuitive Surgical received FDA clearance for the SP SureForm 45 single-port robotic stapler with SmartFire real-time tissue compression monitoring. The clearance strengthened Intuitive's stapling ecosystem around its single-port robotic workflow, increasing platform stickiness through integrated instrumentation. It also raised the competitive bar for sensor-enabled, robot-compatible stapling in minimally invasive procedures.

- November 2024: Medtronic acquired Fortimedix Surgical, adding capabilities in advanced surgical devices that complement its broader minimally invasive surgery portfolio. The transaction supported tighter integration across devices used in complex procedures where stapling, visualization, and access technologies are procured together. It also reinforced the industry trend toward portfolio breadth as a lever in hospital and IDN contracting.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers medical cutter staplers used in surgical procedures where tissue is cut and stapled in one step, and revenue is counted from product sales across hospitals and ambulatory surgical centers.

Scope exclusions: This sizing excludes non-medical office staplers, generic surgical sutures, and accessory items that are not part of the cutter stapler device sale.

Segmentation Overview

- By Product Type

- Endo Cutter Stapler

- Open Cutter Stapler

- Others

- By Mechanism

- Manual

- Powered

- By Surgical Approach

- Open Surgery

- Minimally Invasive Surgery

- By Usability

- Disposable

- Reusable

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public healthcare and procedure context so we could understand where cutter staplers are actually used and how demand moves. We reviewed sources such as the US FDA device and safety communications, the US CDC healthcare infection and surgery related publications, the World Health Organization health statistics, and OECD health expenditure and hospital activity indicators. We also used peer reviewed clinical journals to map common procedure areas where stapling is standard, and to check how adoption is shifting toward minimally invasive approaches.

To translate that context into a usable sizing model, we complemented it with manufacturer annual reports, investor presentations, and reputable press coverage of product launches and regulatory events. Where needed, paid subscriptions that track company financials, patents, and news were used to cross-check timelines, portfolio focus, and broad pricing direction. This list is illustrative, and many other public sources were reviewed to collect, validate, and clarify data points during the work.

Primary Interviews and Surveys

Primary inputs were gathered through expert interviews and structured surveys with a mix of device manufacturers, distributors, and clinical stakeholders who influence product choice, including procurement and operating room leaders. Because this is a global market, we balanced feedback across APAC, EMEA, and the Americas to confirm procedure mix, adoption of powered versus manual systems, and the pace of disposable versus reusable preference shifts.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 16% | APAC: 45% |

| Mid tier: 48% | Functional/Unit leaders: 40% | EMEA: 29% |

| Smaller Players: 17% | Managers: 44% | Americas: 26% |

Market-Sizing & Forecasting

The core model was built using a top-down approach where procedure demand and care setting activity are reconstructed by region, then converted into device value using adoption rates and typical pricing bands. We used bottom-up approximations as a check, including sampled price points by product class and a supplier and channel sense-check on relative revenue splits, and then totals were adjusted only when the two views stayed consistently apart.

Key inputs used in the model included surgical volume direction by major procedure families, the share of minimally invasive surgeries where cutter staplers are more common, the mix shift between powered and manual devices, the disposable versus reusable preference (often tied to infection control policies), and the effect of reimbursement and hospital budget cycles on purchasing behavior. Where a data gap existed, the assumption was kept conservative and was widened only after it was supported by multiple interview responses from different regions. Forecasting was done through scenario analysis tied to procedure growth, expected adoption changes, and price movement expectations, and then the final outlook was aligned to what experts described as the most likely base case.

Data Validation & Update Cycle

Outputs were validated through several checks so that the final number stays consistent with real world signals. We compared the model results against independent indicators such as procedure activity direction, hospital and ambulatory center utilization trends, and publicly visible regulatory or safety events that can shift demand. When a country or product mix result looked off, the drivers were rechecked, and follow-up calls were triggered to confirm whether the issue came from pricing, adoption, or a timing mismatch.

Before sign-off, the work goes through stepwise analyst reviews where assumptions, conversions, and regional splits are tested for variance and arithmetic errors. The report is refreshed annually, and we also do interim updates when a material event changes the demand picture. Right before delivery, a final pass is completed so clients receive the most current view based on the latest available signals.

Mordor Intelligence's Cutter Staplers Market Size Compared Against Other Published Estimates

Published market numbers for cutter staplers can look far apart even when they talk about similar devices, because the year basis, what is counted as a cutter stapler, and how powered and disposable mixes are treated are not always the same. Differences also show up when one estimate leans more on historical revenue narratives while another anchors more tightly to procedure driven demand and adoption levels.

The benchmark table shows a spread that is mainly explained by scope and base year choices, plus how fast pricing and mix are assumed to change after the historical period. In Mordor Intelligence's model, the 2026 value is built around cutter staplers used across key surgical applications and care settings, with explicit splits for mechanisms and usability, which can diverge from estimates that use an earlier base year or bundle adjacent stapling products without the same inclusion rules.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.31 B (2026) | |

| Global Research Publisher A | USD 2.93 B (2023) | Uses an earlier base year and a different forecast window, and the scope description is higher level, which can implicitly include adjacent stapling categories and a different powered and disposable mix, thereby lifting the starting value versus a procedure anchored 2026 build. |

| Industry Research Publisher B | USD 1.83 B (2024) | Runs a longer horizon with a lower growth path and broader segment labels, which can understate near term adoption shifts in minimally invasive surgeries and the associated price and mix effects, leading to a smaller mid-2020s market value. |

Taken together, the comparison points to year alignment and inclusion rules as the biggest drivers of the gap, followed by how quickly the model lets the mix move toward higher value configurations. By keeping assumptions tied to observable demand signals and then cross-checking them with on-the-ground feedback, we end up with a number that can be explained, traced, and repeated with the same steps.

Key Questions Answered in the Report

How are powered staplers influencing surgical outcomes?

Powered cutter staplers deliver consistent staple formation and have been linked to fewer leaks and bleeding events, which in turn reduces the need for costly post-operative interventions.

Why are endo cutter staplers considered strategic for minimally invasive procedures?

Their slim, articulating jaws navigate confined anatomical spaces, making them indispensable for laparoscopic and robotic surgery where precision and access are critical.

What drives hospitals and ambulatory surgical centers to favor disposable staplers despite sustainability debates?

Single-use staplers eliminate reprocessing steps, lower the risk of cross-contamination, and simplify operating-room workflows, benefits that often outweigh environmental concerns for high-volume facilities.

How is regulatory scrutiny shaping competitive dynamics among stapler manufacturers?

Heightened FDA oversight now demands more robust safety data and manufacturing controls, rewarding companies with mature quality systems and discouraging low-cost entrants lacking rigorous compliance.

In what ways are ambulatory surgical centers reshaping device procurement strategies?

ASCs prioritize reliability, intuitive use, and rapid turnover; suppliers that bundle versatile reload options and streamlined training resources gain preferred-vendor status in these outpatient settings.

What role do sustainability initiatives play in future stapler adoption?

Hospital purchasing committees increasingly factor in device life-cycle impact, opening opportunities for reusable handles and reprocessed reloads that deliver both cost savings and waste reduction.

Page last updated on: