Surgical Sealant And Adhesives Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

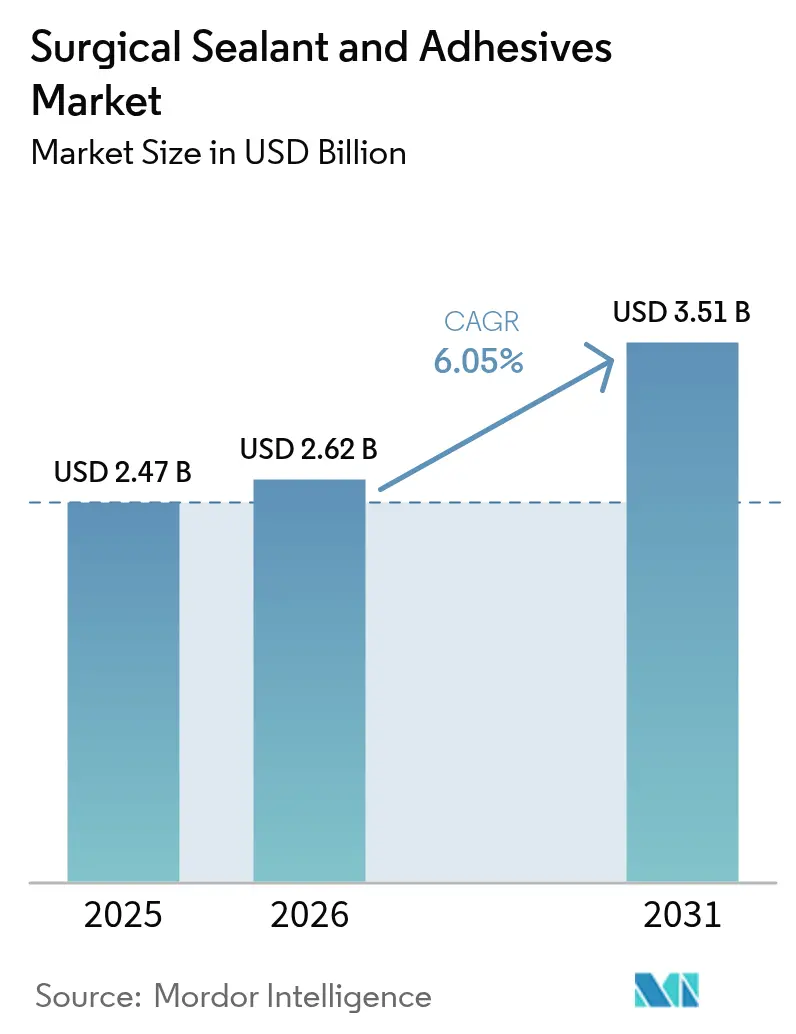

| Market Size (2026) | USD 2.62 Billion |

| Market Size (2031) | USD 3.51 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Sealant And Adhesives Market Analysis by Mordor Intelligence

surgical sealants and adhesives market size in 2026 is estimated at USD 2.62 billion, growing from 2025 value of USD 2.47 billion with 2031 projections showing USD 3.51 billion, growing at 6.05% CAGR over 2026-2031. Uptake is propelled by the steady return of elective procedures, the migration of high-volume cases to ambulatory surgical centers, and product innovations that simplify minimally invasive workflows. Natural and biological formulations continue to dominate hospital formularies, yet newer synthetic chemistries are gaining traction as cold-chain constraints and regulatory demands reshape purchasing criteria. Cardiovascular surgery remains the most significant clinical niche, while orthopedic indications post the fastest gains as same-day joint replacements expand. Regionally, North America holds the revenue lead, but Asia-Pacific is advancing more quickly thanks to significant procedure backlogs and expanding reimbursement access.

Key Report Takeaways

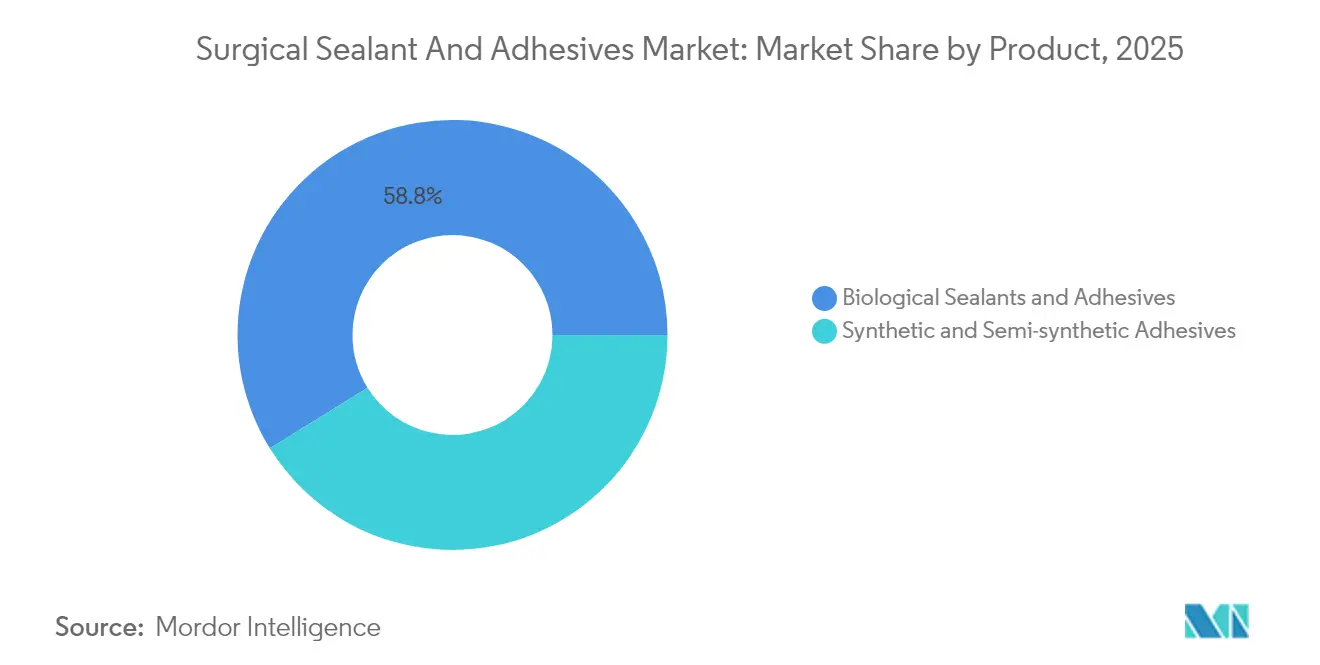

- By product category, natural and biological sealants accounted for 58.84% of the surgical sealants and adhesives market share in 2025.

- By product category, synthetic and semi-synthetic adhesives are forecast to grow at a 7.18% CAGR from 2026-2031.

- By application, cardiovascular surgery led with 28.45% share of the surgical sealants and adhesives market size in 2025.

- By application, orthopedic surgery is projected to advance at a 7.12% CAGR through 2031.

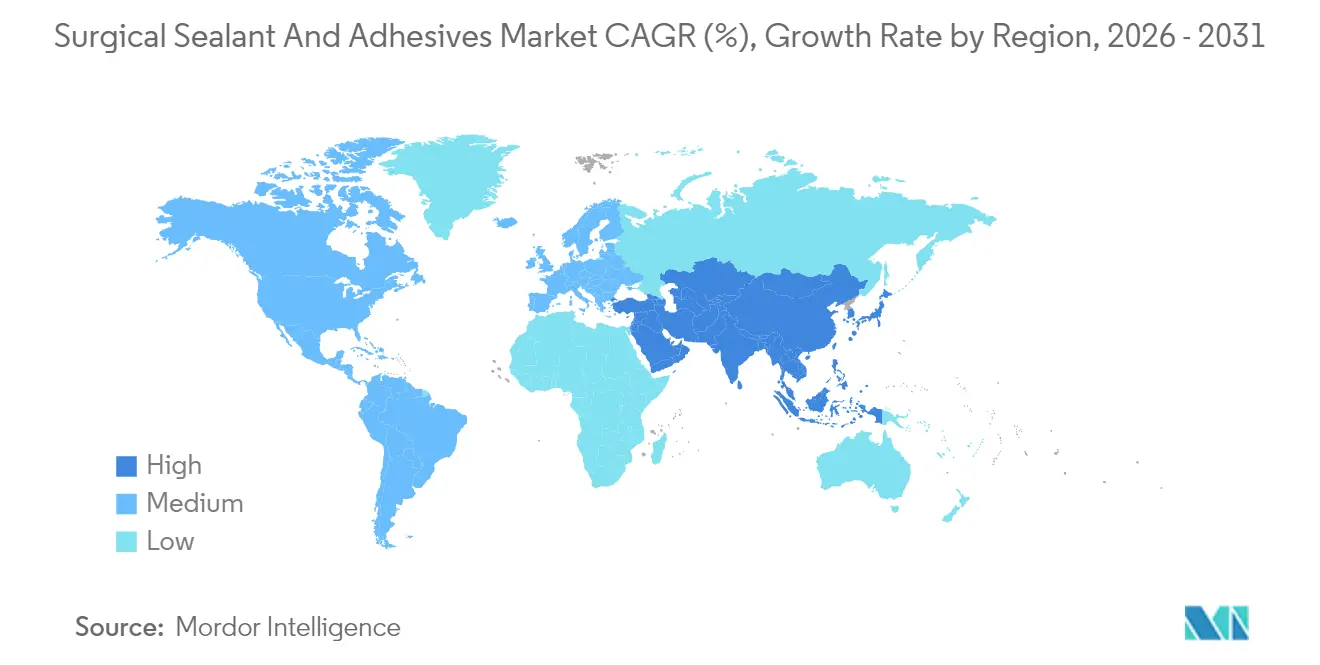

- By geography, North America commanded 38.55% revenue in 2025, whereas Asia-Pacific is set to expand at a 7.26% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Sealant And Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing surgical procedures | +1.2% | Global; strongest in APAC & MEA | Medium term (2-4 years) |

| Advances in minimally invasive surgery | +1.5% | North America & EU lead, APAC accelerating | Long term (≥ 4 years) |

| Aging population and chronic-disease burden | +1.8% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Shift to biocompatible / bio-resorbable materials | +1.0% | EU driven, expanding to US & APAC | Medium term (2-4 years) |

| Growth of ambulatory surgical centers | +0.9% | North America primary, spreading to Europe | Short term (≤ 2 years) |

| Robotic-surgery platform integration | +0.4% | North America & select EU centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Surgical Procedures

Ambulatory surgical centers (ASCs) already exceed pre-pandemic case volumes, and analysts expect 30% of large-joint reconstructions to transition to ASC settings by 2029. Higher throughput lifts unit demand for single-use sealants that shorten hemostasis time and cut readmission risk. Hospitals navigating value-based reimbursement increasingly specify products with demonstrated reductions in transfusion rates and post-operative drainage. Compliance with ISO 13485 and rapid 510(k) clearances further streamlines adoption. As procedure counts climb, the surgical sealants and adhesives market benefits from durable, volume-driven tailwinds.

Advances in Minimally Invasive Surgery

Robotic platforms create spatial constraints that legacy applicators cannot meet. Device makers now offer narrow, multi-directional nozzles and spray tips that interface with common end-effectors on da Vinci systems. Early-2025 sales spikes for LIQUIFIX internal adhesive highlight how robotics-ready designs accelerate contract wins with Group Purchasing Organizations. Flexible hydrogel patches and rapid-polymerizing cyanoacrylates allow surgeons to seal anastomoses through 8-mm ports, limiting leaks to 0.9% in recent colorectal series. The resulting efficiency gains keep the surgical sealants and adhesives market on an upward trajectory.

Aging Population and Chronic Disease Burden

Rising cardiovascular and metabolic comorbidities in older adults increase bleeding risk and slow tissue repair[1]Infection Control Today Editorial Team, “Economic Impact of Post-Operative Infections,” infectioncontroltoday.com. Topical hemostats now feature enhanced thrombin loads and resorbable scaffolds to control diffuse oozing in patients on antiplatelet therapy. Hospitals note that preventing a single post-operative infection can avoid USD 20,000-27,600 in added stay costs. These economics push purchasing committees toward advanced sealants that turn complicated patients into predictable same-day discharges. Such dynamics reinforce steady expansion for the surgical sealants and adhesives market.

Shift to Biocompatible and Bio-resorbable Materials

Europe’s Medical Device Regulation has catalyzed investment in fully resorbable chemistries that degrade within 12 months and eliminate the need for removal surgery. Integra’s DuraSorb scaffold and silk-elastin-based sealants from Japan recorded triple-digit growth in 2025. Research groups report slug-mucus-inspired formulations and recyclable poly(α-lipoic acid) films that meet performance benchmarks while addressing sustainability targets. As more payers tie approval to long-term histocompatibility data, adoption of next-gen materials should keep the surgical sealants and adhesives market growth curve intact.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement gaps in key markets | -0.8% | US Medicare and emerging markets | Medium term (2-4 years) |

| Availability of alternative closure methods | -0.5% | Global; dependent on surgeon preference | Short term (≤ 2 years) |

| Cold-chain fragility for plasma-derived fibrin sealants | -0.4% | Global | Medium term (2-4 years) |

| Regulatory ambiguity for next-gen bio-resorbable adhesives | -0.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Gaps Constrain Adoption

Many U.S. procedures bundle tissue adhesive costs into global surgical payments, limiting separate billing under G0168 and depressing uptake in price-sensitive hospitals. International health technology agencies request randomized data proving cost savings before funding premium devices. Nonetheless, a multicountry analysis showed DuraSeal reduced cerebrospinal fluid leak management expenses versus fibrin glue, providing new leverage for formulary bids. If value-based contracts expand, the surgical sealants and adhesives market could recapture some currently forgone volumes.

Availability of Alternative Closure Techniques

Sutures, staples, and electrocautery remain deeply embedded in surgeon training curricula. For many straightforward wounds, low-priced choices suffice, compelling adhesives to deliver clear clinical advantages. Comparative trials demonstrate benefit when managing diffuse bleeding or fragile tissues, yet day-to-day preference still skews toward familiar tools. Broad in-service education and data on reduced operative time will be crucial for the surgical sealants and adhesives market to displace incumbent methods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Biologics lead while synthetics accelerate growth

Natural and biological sealants retained a 58.84% share of the surgical sealants and adhesives market in 2025 . Fibrin matrices secure neurosurgical dura, collagen plugs patch vascular grafts, and gelatin-based powders control liver oozing. Long safety records and native clotting pathways sustain hospital loyalty. Supply disruptions in plasma sourcing, however, expose vulnerabilities. In parallel, synthetic and semi-synthetic lines are scaling quickly, posting a 7.18% CAGR outlook, as cyanoacrylate chemistries deliver room-temperature stability and antimicrobial barriers. PEG hydrogels with controlled degradation rates appeal to pediatric cardiothoracic teams seeking absorbable seals. Competitive bidding within Integrated Delivery Networks keeps pressure on price tiers, yet innovation in applicators and dual-chamber syringes supports steady margin retention across the broader surgical sealants and adhesives market.

Newer flexible films help laparoscopic teams secure stapled anastomoses without bulky patches. Spray atomizers cut waste by 20% versus traditional dual-syringe kits, an operational saving that resonates with procurement departments. Supplier diversification continued in 2025 as regional firms launched chitosan-based prototypes aimed at trauma centers in emerging markets. Although biologics will likely remain the revenue anchor, synthetics’ scalability and storage benefits should slowly rebalance mix in the surgical sealants and adhesives market.

By Application: Cardiovascular dominance with orthopedic momentum

Cardiovascular surgery generated 28.45% of global revenue in 2025 after surgeons integrated fibrin and gelatin sealants into standard bypass and aortic repair protocols. High anticoagulant use drives dependence on topical agents that secure hemostasis within minutes. Many centers mandate sealant kits on heart-lung machine carts to handle sudden suture-line leaks, locking in predictable consumption. Orthopedic surgery displays the fastest growth at a 7.12% CAGR, fueled by the shift of joint arthroplasty to ASCs and swelling sports-medicine caseloads. Bone void fillers impregnated with thrombin limit drain output, supporting same-day discharge and lowering opioid needs. As demographic shifts bring more active seniors to operating rooms, both segments together underpin durable expansion for the surgical sealants and adhesives market.

Plastic and reconstructive surgeons employ sprayable adhesives to shorten facelift closure times, while neurosurgeons rely on dural patches like DuraSeal to cap cerebrospinal fluid leaks. Dental implantologists increasingly choose flowable cyanoacrylate gels to seal soft-tissue flaps, avoiding membrane suturing. Each niche layers incremental volume onto the broader surgical sealants and adhesives market.

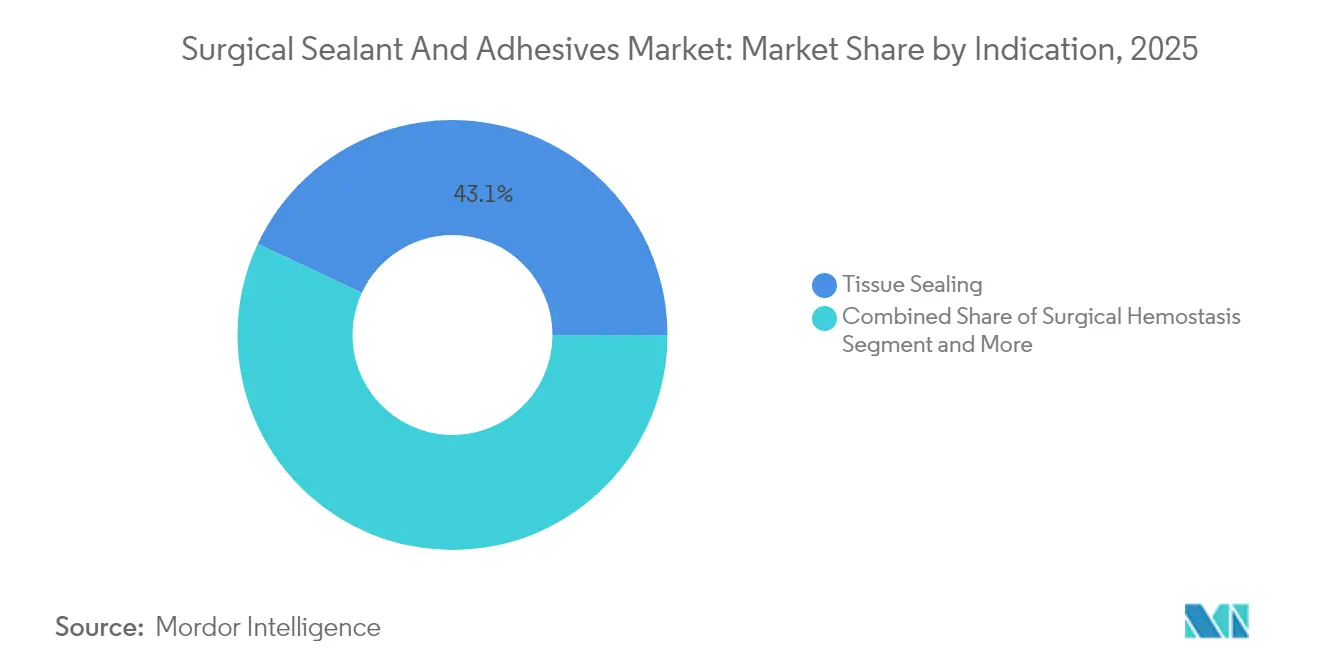

By Indication: Tissue sealing leads with regeneration accelerating

Tissue sealing held 43.05% of the market in 2025, serving as the workhorse across general, thoracic, and neurosurgical suites. Products ensure watertight closures that protect anastomoses and prevent seroma formation. Top-selling dural sealants lowered postoperative leak rates and trimmed ICU stays in posterior fossa cases. Hemostasis follows closely as surgeons deploy flowable matrices on spleen or liver parenchyma where sutures fail to gain purchase.

Regenerative indications are climbing at a 7.68% CAGR through 2031 as polymer science blends scaffolding with bioactive cues. DuraSorb’s fully resorbable mesh supports soft-tissue repair during staged breast reconstruction, yielding strong interest among plastic surgeons. Researchers test hydrogel “cornea-in-a-syringe” constructs that conform to ocular curvature while releasing anti-inflammatory drugs. Sustained clinical validation will decide how fast such technologies broaden addressable revenue inside the surgical sealants and adhesives market.

Geography Analysis

North America generated 38.55% of global sales in 2025, led by the United States, where ASC penetration topped 6,100 facilities and payers reimburse sealants that speed discharge. Route-to-market optimization and GPO contracts lifted LiquiBand topical adhesive revenue by more than 50% year-on-year. Canada’s health-technology assessment framework now endorses certain PEG hydrogels for cardiovascular repairs, while Mexico accelerates regulatory convergence to open import pathways. This demand sustains a steady cash engine for multinationals and props up overall valuations for the surgical sealants and adhesives market.

Europe mirrors mature growth, governed by the EU MDR regime that mandates clinical and post-market vigilance. Germany remains the continent’s largest adopter, supported by the Paul-Ehrlich-Institut’s long-standing familiarity with fibrin products. Favorable cost-utility analyses in France and Italy confirm that preventing cerebrospinal fluid leaks with dural sealants yields net savings even under Diagnosis-Related Group payments. Across the bloc, in-theater training programs now accompany most tenders, reducing skill barriers and protecting share for incumbents inside the surgical sealants and adhesives market.

Asia-Pacific posts the swiftest trajectory with a 7.26% CAGR to 2031 as Japan pioneers silk-elastin hemostats and China expands tertiary centers equipped for complex heart surgery. India’s procedure backlog encourages low-temperature cyanoacrylate adoption that bypasses cold-chain hurdles. Australia’s Therapeutic Goods Administration grants priority review to biodegradable PEG-based ocular sealants, sealing a route for rapid roll-out. While reimbursement heterogeneity persists, rising disposable incomes and government insurance schemes underpin a long runway for the surgical sealants and adhesives market.

Competitive Landscape

The field shows moderate concentration, with global leaders leveraging brand depth and manufacturing scale while smaller biotechs carve out niches. Ethicon, Baxter, and Medtronic safeguard formulary positions through bundled instrument deals and broad clinical-education programs. Ethicon’s VISTASEAL fibrin glue pairs with ENSEAL energy devices, offering integrated closure options across cardiac and oncologic surgeries[4]RevMedConnect, “Coding and Payment for Tissue Adhesives,” revmedconnect.com. Baxter capitalizes on plasma-derived supply chains to meet steady demand for TISSEEL and FLOSEAL.

Advanced Medical Solutions accelerated inorganic growth by acquiring Peters Surgical for EUR 132.5 million (USD 155.16 million), securing IFABOND internal cyanoacrylates and expanding its direct sales force in ten European countries. Integra LifeSciences confronted FDA quality-system findings in December 2024, temporarily pausing shipments while committing capital to a Braintree manufacturing hub slated for H1 2026. Such remediation underscores how compliance shapes both reputations and deal valuations within the surgical sealants and adhesives market.

Innovators pursue robotic-compatible applicators, spray atomizers that halve product waste, and bio-engineered polymers that break down into natural metabolites. Regional manufacturers in South Korea and Turkey now export chitosan sealants targeting trauma indications, elevating price competition in middle-income markets. Despite intensifying rivalry, IP portfolios and surgeon loyalty help incumbents maintain defensible share in the surgical sealants and adhesives market.

Surgical Sealant And Adhesives Industry Leaders

Becton, Dickinson and Company

Baxter International Inc

Johnson & Johnson

Medtronic PLC

B.Braun SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: The United States FDA issued a Warning Letter to Integra LifeSciences, citing quality-system deficiencies across three facilities and suspending PMA approvals for linked Class III devices.

- September 2024: ANZCTR cleared a pilot trial evaluating PYK-2101 biodegradable retinal sealant in 10 vitrectomy patients.

- July 2024: Advanced Medical Solutions completed the EUR 132.5 million acquisition of Peters Surgical, adding sutures and IFABOND internal adhesives to its European lineup.

- April 2024: Integra LifeSciences finalized the acquisition of Acclarent ENT technologies, adding USD 95 million in incremental revenue.

Global Surgical Sealant And Adhesives Market Report Scope

As per the report's scope, sealants and adhesives are substances used to block fluids' passage through the surface, joints, or openings in tissues.

The surgical sealants and adhesives market is segmented by product, application, and geography. The product segment is further divided into natural or biological sealants and adhesives and synthetic and semi-synthetic adhesives. By natural or biological sealants, the market is segmented into fibrin sealants, gelatin-based adhesives, and collagen-based adhesives. By synthetic and semi-synthetic adhesives, the market is segmented into cyanoacrylates, polymeric hydrogels, polyethylene glycol polymer, and other synthetic and semi-synthetic adhesives. The application segment is further segmented into general surgery, orthopedic surgery, dental surgery, cardiovascular surgery, cosmetic surgery, neurosurgery, and other applications. The geography segment is further bifurcated into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report offers the value (USD) for the abovementioned segments.

| Natural / Biological Sealants & Adhesives | Fibrin Sealant |

| Gelatin-based Adhesive | |

| Collagen-based Adhesive | |

| Synthetic & Semi-synthetic Adhesives | Cyanoacrylates |

| Polymeric Hydrogels | |

| PEG Polymer | |

| Other Synthetic & Semi-synthetic |

| General Surgery |

| Dental Surgery |

| Cardiovascular Surgery |

| Cosmetic Surgery |

| Neurosurgery |

| Orthopaedic Surgery |

| Other Applications |

| Tissue Sealing |

| Surgical Hemostasis |

| Tissue Engineering & Regeneration |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Products | Natural / Biological Sealants & Adhesives | Fibrin Sealant |

| Gelatin-based Adhesive | ||

| Collagen-based Adhesive | ||

| Synthetic & Semi-synthetic Adhesives | Cyanoacrylates | |

| Polymeric Hydrogels | ||

| PEG Polymer | ||

| Other Synthetic & Semi-synthetic | ||

| By Application | General Surgery | |

| Dental Surgery | ||

| Cardiovascular Surgery | ||

| Cosmetic Surgery | ||

| Neurosurgery | ||

| Orthopaedic Surgery | ||

| Other Applications | ||

| By Indication | Tissue Sealing | |

| Surgical Hemostasis | ||

| Tissue Engineering & Regeneration | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Which product type currently holds the largest share?

The market is forecast to reach USD 3.51 billion by 2031.

Which product type currently holds the largest share?

Natural and biological sealants command 58.84% of global revenue.

Which clinical application is expanding the fastest?

Orthopedic surgery is projected to grow at a 7.12% CAGR through 2031.

Which region offers the strongest growth outlook?

Asia-Pacific is anticipated to post a 7.26% CAGR between 2026 and 2031.

How are ambulatory surgical centers influencing demand?

ASCs favor rapid-deploy sealants that shorten turnover time, boosting volume purchases.

What regulatory trend is shaping product innovation?

Global emphasis on bio-resorbable materials under the EU MDR and similar frameworks is driving next-generation adhesive development.

Page last updated on: