Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.39 Billion |

| Market Size (2031) | USD 7.03 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

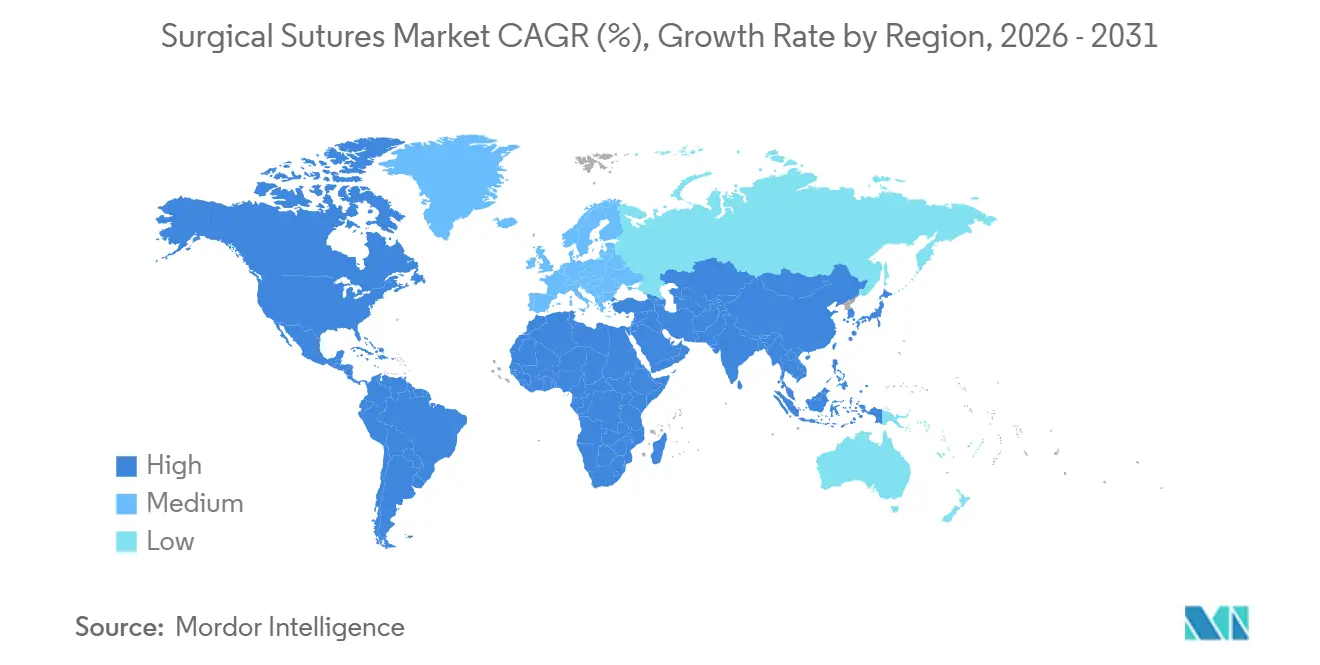

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

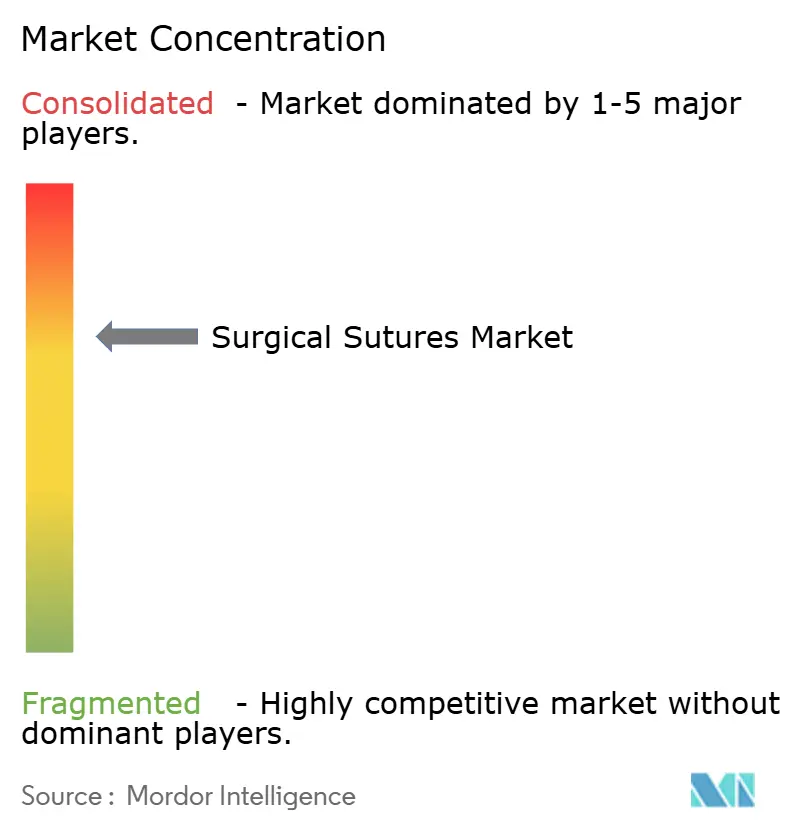

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surgical Sutures Market Analysis by Mordor Intelligence

The Surgical Sutures Market size is expected to increase from USD 5.16 billion in 2025 to USD 5.39 billion in 2026 and reach USD 7.03 billion by 2031, growing at a CAGR of 5.47% over 2026-2031.

The market’s growth is tied to hospitals and ambulatory surgical centers adopting absorbable, antimicrobial-coated, fast-absorbing filaments that lower infection-monitoring costs and shorten operating-room turnover times. Absorbable polyglycolic-acid and polydioxanone sutures, single-strand monofilaments, and predictable synthetic polymers are displacing legacy options because they eliminate suture-removal visits, cut infection risks, and fit value-based care models. At the same time, elective-surgery volumes tied to chronic conditions, an aging global population, and robust investment in private-sector hospital capacity in Asia-Pacific continue to expand the addressable base for the surgical suture market. Supply-chain consolidation in North America and Europe pushes vendors toward bundled contracts that pair sutures with staplers and hemostats, squeezing standalone margins yet encouraging product innovation to protect pricing power. Countervailing pressures stem from robotic stapling platforms, tissue adhesives, and raw-material volatility, but these forces have not derailed the surgical suture market’s overall expansion trajectory.

Key Report Takeaways

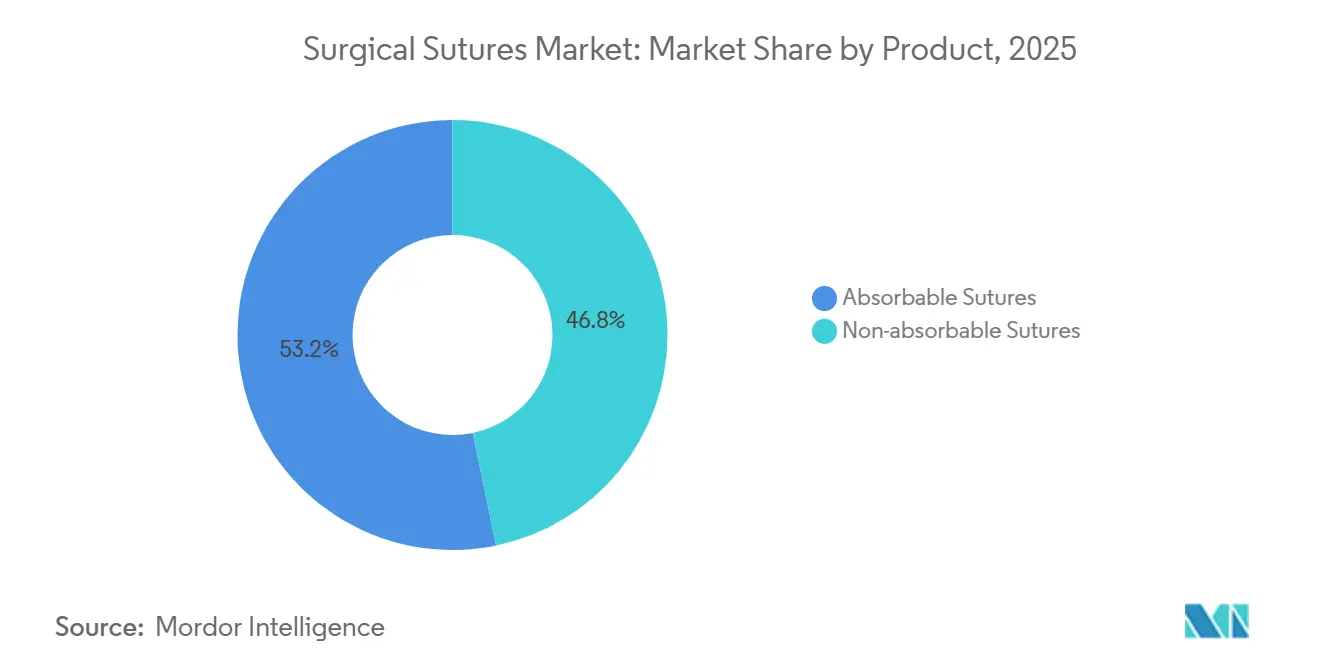

- By product, absorbable sutures captured 53.24% of the surgical suture market share in 2025 and are projected to expand at a 7.56% CAGR through 2031.

- By filament structure, monofilament designs held 58.46% revenue share in 2025 and are advancing at an 8.02% CAGR over the forecast horizon.

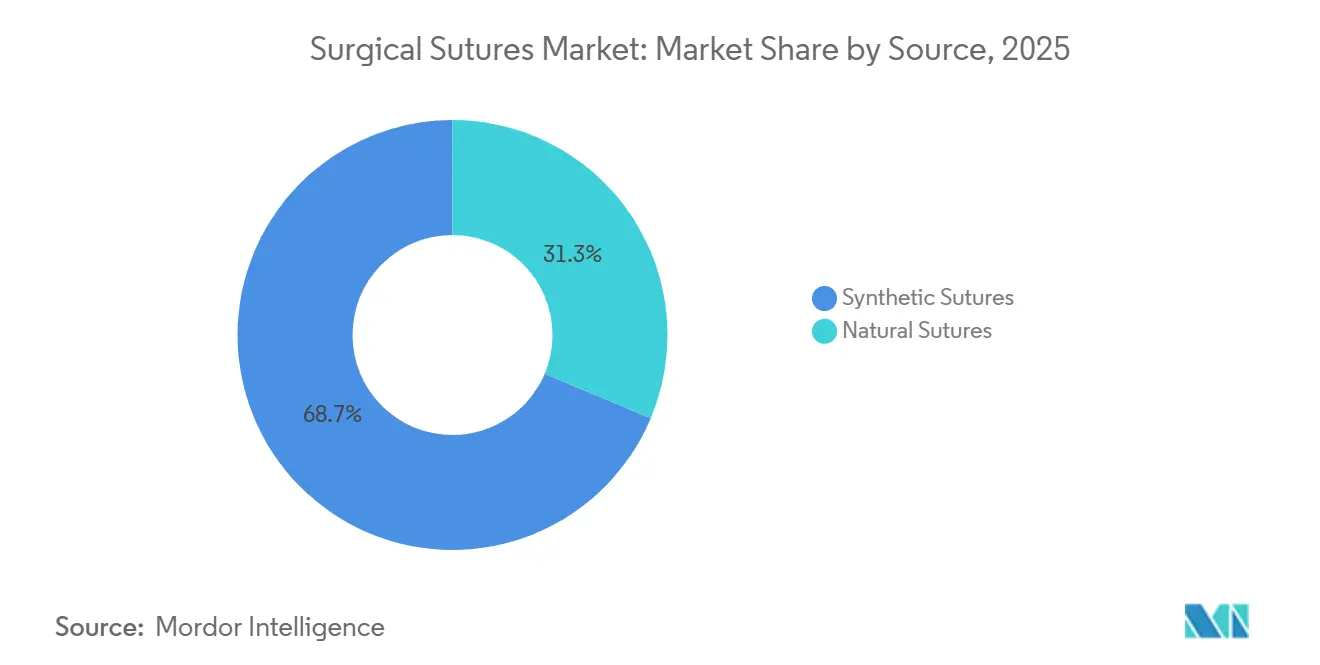

- By source, synthetic polymers commanded 68.68% revenue in 2025 and remain the fastest-growing category at a 6.46% CAGR to 2031.

- By coating, antimicrobial-coated sutures accounted for 64.24% of 2025 revenue and are progressing at a 7.01% CAGR across the projection period.

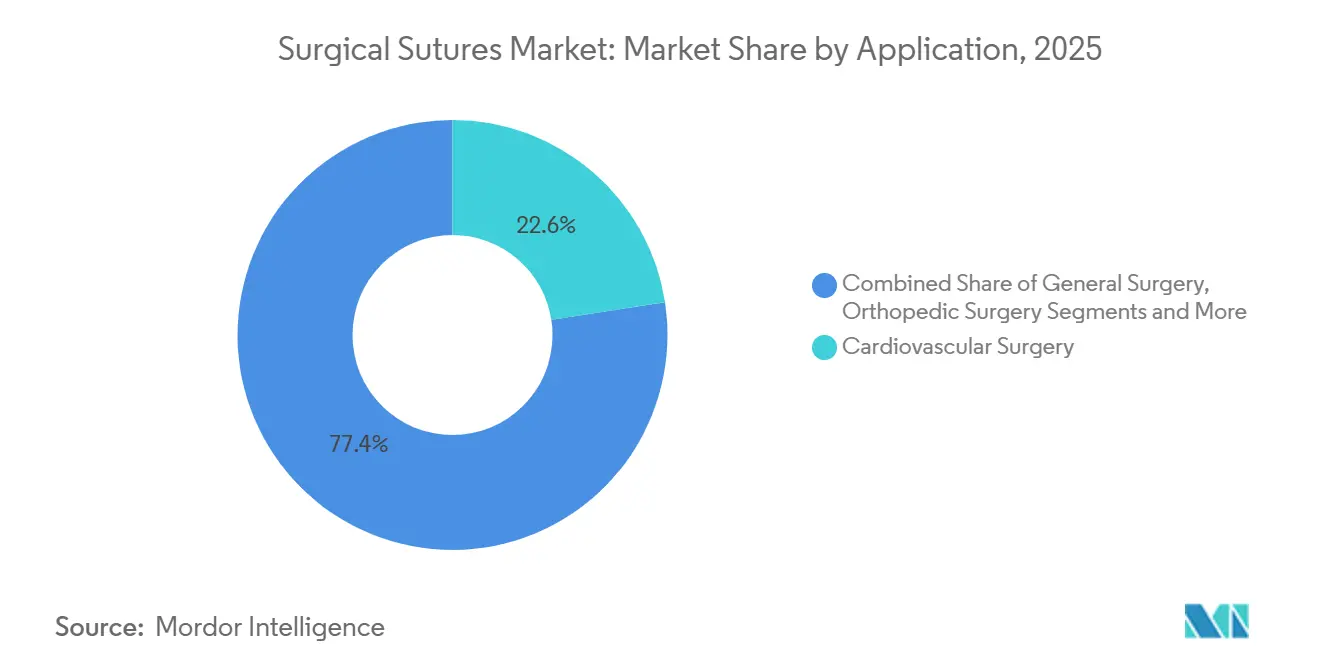

- By application, cardiovascular surgery led with a 22.57% share in 2025, while plastic and reconstructive surgery records the strongest 8.73% CAGR through 2031.

- By end user, hospitals retained 65.36% share in 2025, whereas ambulatory surgical centers post the highest 8.46% CAGR toward 2031.

- By geography, North America dominated with 37.47% revenue share in 2025, yet Asia-Pacific registers the quickest 7.36% CAGR heading to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Surgical Sutures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising surgical procedure volumes among aging populations | +1.2% | North America, Europe, Japan | Long term (≥4 years) |

| Growing chronic-disease burden driving elective surgeries | +0.9% | North America, Western Europe | Medium term (2-4 years) |

| Technological advances in bio-absorbable & antimicrobial yarns | +0.8% | North America, Europe, spill-over Asia-Pacific | Medium term (2-4 years) |

| Expansion of healthcare infrastructure in emerging economies | +1.0% | China, India, MEA, South America | Long term (≥4 years) |

| Boom in ambulatory surgeries demanding fast-absorbing sutures | +0.7% | North America, Europe, urban Asia-Pacific | Short term (≤2 years) |

| Early R&D in smart sensor-enabled sutures | +0.3% | North America, Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Procedure Volumes Among Ageing Populations

Geriatric demographics are reshaping suture demand by boosting orthopedic, spinal, and cardiovascular case volumes while requiring longer-lasting absorbable filaments that retain tensile strength for 60–90 days. U.S. adults aged ≥65 will constitute 21.6% of the population by 2040, increasing annual hip and knee arthroplasties toward 4.7 million procedures. Over 90% of arthroplasty patients during the study period were aged 50 and above. The average age for total hip replacement (THR) patients was 70, and for total knee replacement (TKR) patients, it was 67. Projections indicate a 65% rise in total hip arthroplasties and a 49% increase in knee arthroplasties by 2036.[1]Katie St John, Andrew Hughes, and Joseph Queally, “A Study of Population Trends and Future Projections for the Hip and Knee Arthroplasty Service in the Republic of Ireland,” The Surgeon, sciencedirect.com In 2023, Japan's National Clinical Database recorded 895,606 gastroenterological and abdominal surgical procedures. Laparoscopic cholecystectomy led with 118,825 procedures, followed by laparoscopic inguinal hernia surgery (82,669) and open inguinal hernia surgery (63,234).[2]Takehito Yamamoto et al., “2023 National Clinical Database Annual Report by the Japan Surgical Society,” Surgery Today, ncbi.nlm.nih.gov Infection rates double in patients over 75, prompting hospitals to mandate triclosan-coated sutures for high-risk geriatric procedures.

Growing Chronic-Disease Burden Driving Elective Surgeries

Diabetes, obesity, cardiovascular disease, and cancer are pushing predictable high-volume surgeries that favor standardized suture lines. Bariatric procedures in the United States reached 270,089 in 2023, consuming 30% more suture material than standard abdominal cases.[3]American Society for Metabolic and Bariatric Surgery, “Estimate of Bariatric Surgery Numbers, 2011–2023,” American Society for Metabolic and Bariatric Surgery, asmbs.org Coronary artery bypass grafts totaled 371,000 in 2024, anchoring demand for braided polyester vascular sutures. Oncology resections increasingly rely on absorbable subcuticular closures that avoid follow-up removal in immunosuppressed patients.

Technological Advances in Bio-Absorbable & Antimicrobial Yarns

Silver-nanoparticle-doped poly(3-hydroxybutyrate-co-4-hydroxybutyrate) sutures cut Staphylococcus aureus colonization by 94% while retaining 80% tensile strength at 28 days. Faropenem-eluting threads release bactericidal levels for 14 days, extending antimicrobial windows beyond first-generation triclosan coatings. Polybutylene succinate formulations under clinical evaluation promise carbon-neutral footprints that satisfy hospital sustainability mandates.

Expansion of Healthcare Infrastructure in Emerging Economies

India added 10,000 private hospital beds in 2024 and streamlined device approvals through the MedTech Mitra program. Saudi Arabia’s Vision 2030 privatization of 290 hospitals requires USD 65 billion in device procurement, including sutures. China’s 14th Five-Year Plan budgets USD 75 billion for new county-level hospitals and approved 23 domestic suture manufacturers in 2024, intensifying price competition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward staplers, sealants & robotic closure systems | -0.6% | North America, Europe | Medium term (2-4 years) |

| Infection risks prompting switch to adhesive dressings | -0.3% | Global pediatric and ophthalmic surgery | Short term (≤2 years) |

| Heightened scrutiny of antimicrobial-coated filaments | -0.2% | North America, Europe | Short term (≤2 years) |

| Geopolitical raw-material supply disruptions | -0.4% | Global single-source regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Staplers, Sealants & Robotic Closure Systems

Robotic stapling on da Vinci platforms cut suture use 20% per colorectal case in 2024 as procedure counts hit 2.289 million. Fibrin sealants and cyanoacrylate adhesives replace sutures in pediatric and hepatic cases, aided by FDA clearances of eight new tissue-adhesive variants in 2024. CMS raised stapled bariatric surgery reimbursements by USD 220, reinforcing substitution economics.

Infection Risks Prompting Switch to Adhesive Dressings

CDC surveillance logged 157,500 surgical-site infections in 2024, with sutures implicated in 18%. Multifilament threads carry a 2.3-fold higher infection-risk profile, motivating guideline revisions that prefer monofilaments in contaminated wounds. JAMA Surgery showed clean-contaminated abdominal cases closed with adhesives reduced infections from 4.7% to 2.9% versus absorbable sutures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Absorbables Dominate as Reimbursement Favors Elimination Visits

Absorbable sutures’ 53.24% share in 2025 underscores a structural reimbursement shift. Medicare’s 2024 Physician Fee Schedule cut payments for suture-removal visits, driving surgeons toward polyglycolic-acid and polydioxanone options. Within the surgical suture market size for absorbables, barbed designs shortened OR time 6–9 minutes, and adoption in orthopedic repairs rose 14%. Non-absorbables persist in vascular and corneal applications demanding permanent tensile strength, but their 3.12% CAGR lags as payors reward elimination of follow-up appointments.

ISO 13485 certifications climbed 9% year-on-year to 1,247 suture manufacturers in 2024, making quality compliance a threshold for GPO contracts. Carbon-neutral bio-based absorbables could rewrite purchasing criteria despite 40%–60% price premiums, limiting early uptake to academic centers.

By Filament Structure: Monofilament Gains on Infection-Control Mandates

Monofilament sutures seized 58.46% revenue in 2025 and pace at an 8.02% CAGR as hospital protocols ban multifilaments in contaminated settings. A Lancet meta-analysis covering 47,000 patients proved single-strand closures cut infections by 52% in colorectal and biliary surgeries. Multifilaments still appeal for knot security in microsurgery, yet antimicrobial coatings on braided threads are stop-gap solutions amid infection-control mandates. Barbed designs blur structural lines by offering knotless closures that shave OR minutes and reduce glove fatigue in repetitive closures.

By Source: Synthetic Polymers Marginalize Natural Materials

Synthetic sutures occupy 68.68% of 2025 revenue and expand at 6.46% CAGR, thanks to engineered hydrolysis that matches tissue-healing timelines. Polydioxanone maintains 70% tensile strength at 28 days, perfect for fascial repairs. Natural catgut, still favored for mucosal layers, faces 18% supply contraction amid EU sourcing bans, limiting its 3.87% CAGR. Silk’s high tissue reactivity also advances its gradual displacement by braided polyester.

By Coating: Antimicrobial Formulations Face Regulatory Headwinds

Coated sutures held 64.24% revenue share in 2025, and their 7.01% CAGR persists as hospitals tie reimbursements to infection-rate metrics. Triclosan-coated formulations reduced infection risk 31% across 15,000 patients in a 2024 Cochrane meta-analysis. Yet FDA resistance warnings are prompting next-generation coatings such as silver nanoparticles and faropenem-eluting layers designed to mitigate long-term antimicrobial exposure.

By Application: Plastic Surgery Surges as Aesthetics Normalize

Cardiovascular surgery’s 22.57% share remains anchored by 371,000 annual CABG cases requiring polyester sutures. Plastic and reconstructive surgery accelerates at 8.73% CAGR on 28.2 million U.S. procedures in 2024. Barbed polydioxanone facilitates knotless facelifts, while absorbable subcuticular closures minimize scarring in breast reconstructions. Orthopedic surgeries ride joint-replacement momentum at 6.89% CAGR in Japan and the United States.

By End User: ASCs Gain as Outpatient Migration Accelerates

Hospitals hold 65.36% share but face margin compression from bundled purchasing agreements. ASCs grow 8.46% CAGR, demanding pre-sterilized packs and 90-day payment terms. Specialty clinics expand 5.23% CAGR on in-office dermatologic and varicose-vein interventions.

Geography Analysis

North America’s 37.47% share stems from 51 million annual procedures and premium adoption of coated and barbed sutures. GPOs controlling USD 84 billion in contracts enforce bundled deals that shaved 200–300 basis points off standalone suture margins by 2025.

Asia-Pacific posts a 7.36% CAGR, lifted by India’s bed count expansion, China’s hospital build-out, and Japan’s aging orthopedic demand. Europe is tempered by MDR recertification hurdles that sidelined 14% of manufacturers and by EMA reviews restricting triclosan usage. The Middle East and Africa grows as Saudi Arabia’s Vision 2030 privatization drives centralized procurement. South America’s share remains price-sensitive under Brazil’s SUS tenders that emphasize lowest-cost supply.

Competitive Landscape

Ethicon, Medtronic, and B. Braun command nearly half of global revenue, yet local manufacturers in India and China underprice imports by 30%–40% in public tenders, preserving fragmentation. Ethicon’s raw-material integration supports 15%–20% margin premiums, while Medtronic’s Covidien acquisition bolstered cardiovascular niche breadth. B. Braun’s Malaysian plant trims 25% landed costs for Asia-Pacific demand. Surgical Specialties’ Sharpoint dominates ultra-fine ophthalmic categories on ±2 µm tolerances, and DemeTech’s direct-to-ASC model holds 8% U.S. ambulatory share. Forty-seven new 510(k) clearances in 2024 signal fast innovation cycles, but six Class II recalls expose manufacturing risks.

Surgical Sutures Industry Leaders

B. Braun Melsungen AG

Johnson & Johnson Services, Inc.

Medtronic plc

Smith & Nephew plc

Teleflex Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Mesh Suture, Inc. secured EU MDR and MDSAP certifications for DURAMESH

- July 2025: Corza Medical broadened its Onatec ophthalmic suture line to improve surgeon choice.

Global Surgical Sutures Market Report Scope

As per the scope of the report, a suture refers to any strand of material used to litigate blood vessels or tissues to close a surgical site. They play a crucial role in the healing process.

The surgical sutures market is segmented by product, filament structure, source, coating, application, end user, and geography. By Product, the market is segmented into Absorbable and Non-absorbable. By Filament Structure, the market is segmented into Monofilament and Multifilament. By Source, the market is segmented into Natural and synthetic. By Coating, the market is segmented into Coated and Uncoated. By Application, the market is segmented into Cardiovascular, General, Orthopedic, Gynecology & Obstetrics, Ophthalmic, Dental, Plastic & Reconstructive, and Other. By End User, the market is segmented into Hospitals, ASCs, Specialty Clinics, and Other. By Geography, market is segmented into North America, Europe, Asia-Pacific, MEA, South America. The report also covers the market size and forecasts for the surgical sutures market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Product

| Absorbable Sutures |

| Non-absorbable Sutures |

By Filament Structure

| Monofilament Sutures |

| Multifilament Sutures |

By Source

| Natural Sutures |

| Synthetic Sutures |

By Coating

| Coated Sutures |

| Uncoated Sutures |

By Application

| Cardiovascular Surgery |

| General Surgery |

| Orthopedic Surgery |

| Gynecology & Obstetrics |

| Ophthalmic Surgery |

| Dental Surgery |

| Plastic & Reconstructive Surgery |

| Other Applications |

By End User

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Other End Users |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Absorbable Sutures | |

| Non-absorbable Sutures | ||

| By Filament Structure | Monofilament Sutures | |

| Multifilament Sutures | ||

| By Source | Natural Sutures | |

| Synthetic Sutures | ||

| By Coating | Coated Sutures | |

| Uncoated Sutures | ||

| By Application | Cardiovascular Surgery | |

| General Surgery | ||

| Orthopedic Surgery | ||

| Gynecology & Obstetrics | ||

| Ophthalmic Surgery | ||

| Dental Surgery | ||

| Plastic & Reconstructive Surgery | ||

| Other Applications | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the surgical suture market?

The surgical suture market size stands at USD 5.39 billion in 2026.

How fast is global revenue expected to grow?

Revenue is projected to reach USD 7.03 billion by 2031, reflecting a 5.47% CAGR.

Which product type leads sales?

Absorbable sutures held a 53.24% share in 2025 and are projected to outpace non-absorbables at a 7.56% CAGR through 2031.

Why are monofilament sutures gaining traction?

Monofilaments reduce surgical-site infections by more than 50% versus braided alternatives.

Which application area is growing the fastest?

Plastic and reconstructive surgeries are forecast to expand at an 8.73% CAGR through 2031.

What region offers the strongest growth outlook?

Asia-Pacific is expected to advance at a 7.36% CAGR through 2031 on hospital-capacity expansion.

Page last updated on: