Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

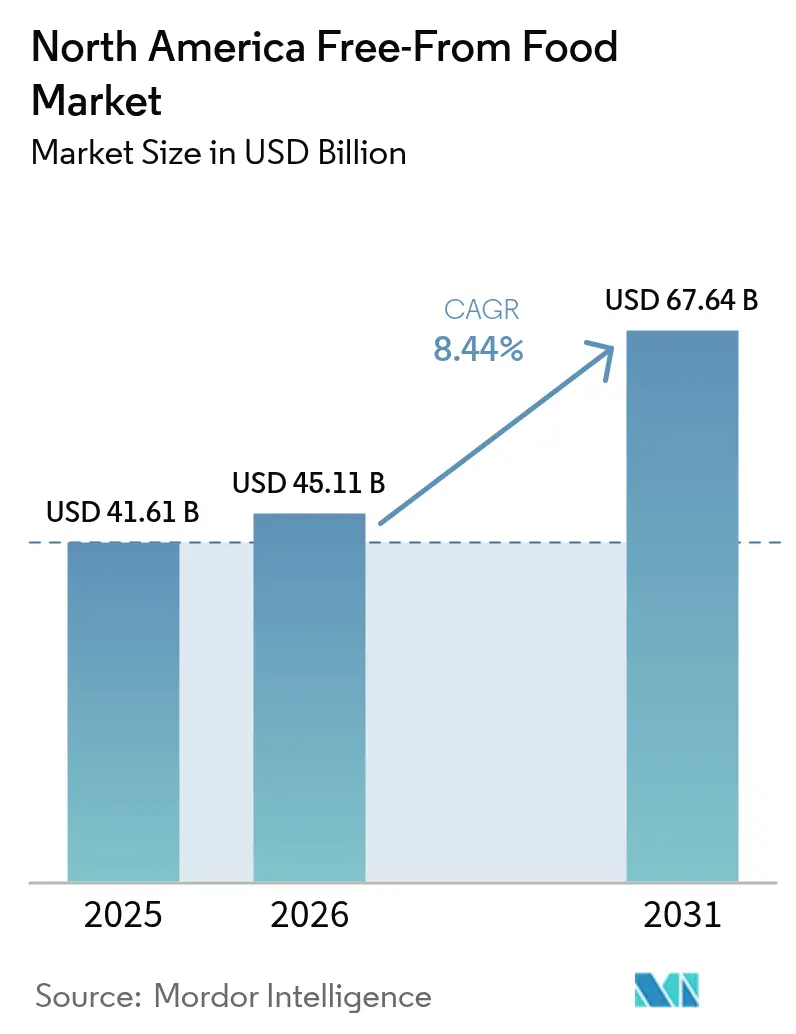

| Base Year Market Size (2025) | USD 41.61 Billion |

| Market Size (2026) | USD 45.11 Billion |

| Market Size (2031) | USD 67.64 Billion |

| Growth Rate (2026 - 2031) | 8.44% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Free-From Food Market Analysis by Mordor Intelligence

The North American free-from food market size is expected to increase from USD 41.61 billion in 2025 to USD 45.11 billion in 2026 and reach USD 67.64 billion by 2031, growing at a CAGR of 8.44% over 2026-2031. Consumer awareness of food allergies, rising household incomes, and stricter labeling laws are moving free-from products from specialty aisles to mainstream shelves, supporting steady value growth even when discretionary categories slow. Gluten-free bakery items are benefiting from enzyme-based dough conditioners that extend shelf life to 7-10 days, while dairy alternatives such as oat and almond milk have reached cost parity in many large retail chains. Certification costs that add 15-25% to production expenses are encouraging scale advantages for multinationals, yet mid-sized brands still gain shelf presence by emphasizing clean-label claims and first-party data from direct-to-consumer channels. Raw-material price spikes for almond flour and pea protein isolates continue to pressure margins, but manufacturers are partially offsetting these costs through hybrid formulation strategies and private-label collaborations.

Key Report Takeaways

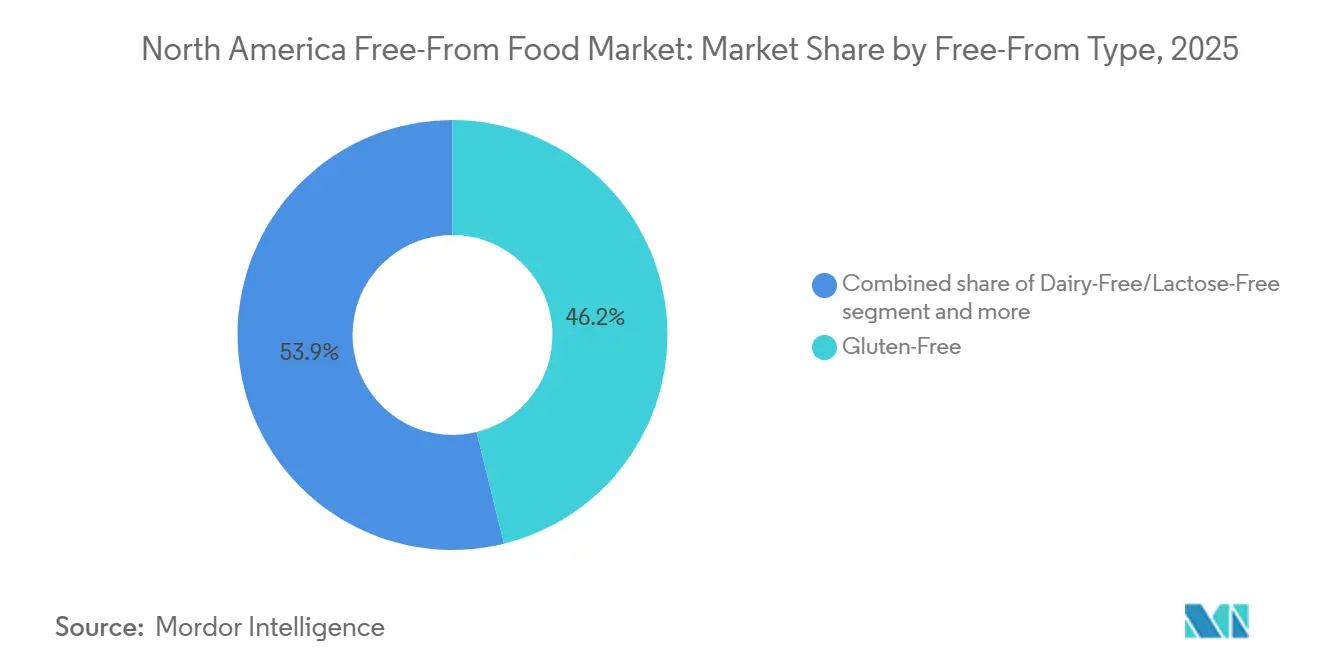

- By free-from type, gluten-free products captured 46.15% of the gluten-free market share in 2025 and meat-free plant-based alternatives are projected to record the fastest 9.26% CAGR through 2031.

- By end product, bakery and confectionery led with 29.77% revenue share in 2025, while dairy alternatives are forecast to expand at an 8.99% CAGR to 2031.

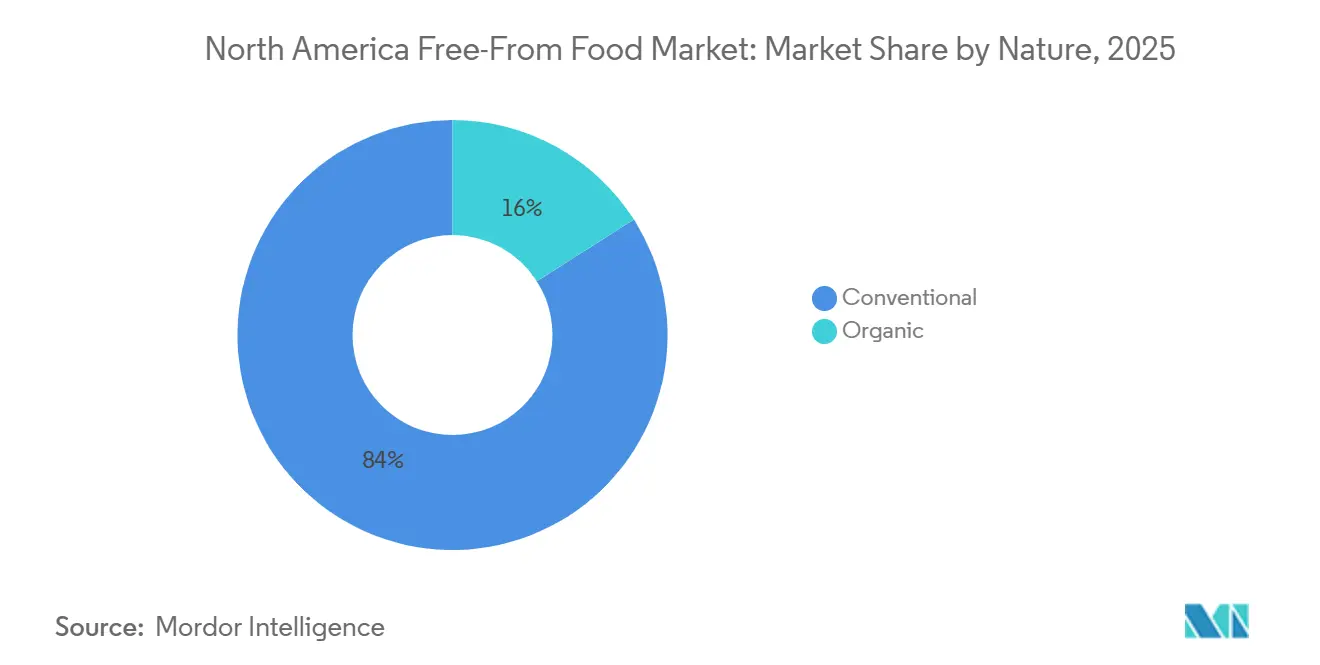

- By nature, conventional lines held 84.02% of the gluten-free market size in 2025 and organic variants are advancing at a 10.05% CAGR between 2026-2031.

- By distribution channel, off-trade outlets controlled 71.91% of sales in 2025, yet on-trade foodservice is accelerating at a 9.63% CAGR through 2031.

- By geography, the United States generated 79.89% of 2025 revenue, whereas Mexico is forecast to post the highest 9.84% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Free-From Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of food allergies and intolerance | +1.5% | Regional, with highest intensity in United States and Canada | Medium term (2-4 years) |

| Increasing demand for gluten-free and dairy-free products | +1.8% | North America, with spillover to Mexico urban centers | Short term (≤ 2 years) |

| Growing health and wellness awareness among consumers | +1.2% | United States, Canada, Mexico metropolitan areas | Long term (≥ 4 years) |

| Rising adoption of plant-based and allergen-free diets | +1.6% | United States and Canada, emerging in Mexico | Medium term (2-4 years) |

| Expansion of free-from products in mainstream retail channels | +1.0% | United States, Canada, with gradual Mexico penetration | Short term (≤ 2 years) |

| Growing demand for clean-label and minimally processed foods | +0.9% | United States and Canada, early adoption in Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of food allergies and intolerance

The rising prevalence of food allergies and intolerances is a major driver of the North America free-from food market. Increasing awareness of dietary restrictions and health concerns is encouraging consumers to seek products that are safe, allergen-free, and suitable for specific dietary needs. In 2024, 6.7% of U.S. adults were diagnosed with a food allergy, according to the Centers for Disease Control and Prevention (CDC), highlighting the growing portion of the population that requires allergen-conscious food options[1]Source: Centers for Disease Control and Prevention, “Diagnosed Allergic Conditions in Adults: United States, 2024”, cdc.gov. This trend is further supported by parents seeking safe, nutritious foods for children with allergies, as well as individuals managing lactose intolerance, gluten sensitivity, or other dietary restrictions. The demand for free-from products spans multiple categories, including bakery, dairy alternatives, snacks, and beverages, driving product innovation and diversification. With increasing health consciousness and stricter labeling regulations, the market for free-from foods is expected to continue expanding steadily across North America.

Increasing demand for gluten-free and dairy-free products

Increasing demand for gluten-free and dairy-free products is a key driver of the North America free-from food market. Consumers are becoming more health-conscious and actively seeking alternatives that align with dietary preferences, intolerances, or lifestyle choices. According to the 2024 IFIC Food & Health Survey, 66% of consumers reported limiting sugar consumption, up from 61% in 2023, reflecting a broader shift toward healthier eating habits[2]Source: International Food Information Council, "2024 IFIC Food & Health Survey", ific.org. This growing focus on nutrition and wellness is creating opportunities for gluten-free and dairy-free products to compete effectively with conventional foods in mainstream retail channels. Products such as plant-based milk, yogurt alternatives, and gluten-free bakery items are gaining traction as consumers look for options that are both safe and aligned with their health goals. The trend is further reinforced by increasing availability, product innovation, and clean-label claims that appeal to urban and millennial consumers.

Growing health and wellness awareness among consumers

Growing health and wellness awareness among consumers is a significant driver of the North America free-from food market. Increasing knowledge about diet-related health issues, such as obesity, diabetes, and food intolerances, has encouraged individuals to make more conscious food choices. In 2024, 56.2 million adults aged 20-79 in North America were reported to have diabetes, as per the International Diabetes Federation[3]Source: International Diabetes Federation, “Diabetes around the world - 2024”, diabetesatlas.org. Consumers are actively seeking products that are low in sugar, free from allergens, and minimally processed, aligning with broader wellness and clean-eating trends. This heightened focus on nutrition and preventive health has boosted demand for gluten-free, dairy-free, plant-based, and organic alternatives across multiple food categories. Retailers and foodservice providers are responding by expanding their free-from offerings, highlighting health benefits and clean-label claims to attract health-conscious buyers. Millennials and urban populations, in particular, are driving the adoption of functional foods, protein-rich snacks, and allergen-free products.

Rising adoption of plant-based and allergen-free diets

The rising adoption of plant-based and allergen-free diets is a key driver of the North America free-from food market. Growing awareness of health, environmental sustainability, and ethical eating is encouraging more consumers to embrace plant-based and allergen-conscious lifestyles. According to the Good Food Institute, 59% of U.S. households purchased plant-based foods in 2024, highlighting the expanding mainstream acceptance of alternative proteins and dairy-free options[4]Source: Good Food Institute, "U.S. Retail Market Insights for the Plant-Based Industry", gfi.org. This shift is driving demand across multiple product categories, including meat substitutes, plant-based dairy alternatives, and allergen-free snacks. Consumers are increasingly seeking foods that are not only nutritious and safe but also align with their personal values and lifestyle choices. The rise of clean-label, minimally processed products further reinforces this trend, appealing to health-conscious and ethically minded buyers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs due to strict certification requirements | -0.8% | United States and Canada, with emerging impact in Mexico | Short term (≤ 2 years) |

| Higher product prices compared to conventional foods | -1.0% | Regional, most acute in price-sensitive Mexico market | Medium term (2-4 years) |

| Complex formulation challenges affecting taste and texture | -0.6% | United States and Canada, where sensory expectations are highest | Long term (≥ 4 years) |

| Regulatory compliance and labeling requirements | -0.5% | United States, Canada, Mexico as regulations harmonize | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High production costs due to strict certification requirements

High production costs due to strict certification requirements act as a significant restraint on the North America free-from food market. Free-from products, including gluten-free, dairy-free, and allergen-free items, must comply with rigorous regulatory standards and labeling guidelines to ensure consumer safety and transparency. Obtaining certifications such as gluten-free verification, non-GMO, organic, or allergen-free can be expensive and time-consuming, requiring specialized testing, quality control measures, and compliance audits. These additional operational expenses often increase the final product cost, making free-from foods less affordable for price-sensitive consumers. Small and medium-sized manufacturers, in particular, may face challenges in scaling production while meeting certification standards. Furthermore, maintaining strict segregation of ingredients to avoid cross-contamination adds complexity and cost to manufacturing processes.

Higher product prices compared to conventional foods

Higher product prices compared to conventional foods represent a key restraint for the North America free-from food market. Free-from products, such as gluten-free, dairy-free, and allergen-free options, often require specialized ingredients, advanced processing techniques, and strict quality control measures, all of which increase production costs. These added expenses are reflected in retail prices, making free-from foods more expensive than standard alternatives and limiting their affordability for price-sensitive consumers. As a result, some households may opt for conventional products despite health or dietary concerns. The higher pricing also affects market penetration in value-conscious segments and can slow adoption among first-time buyers. Additionally, premium positioning of clean-label and certified allergen-free products contributes to the perception of free-from foods as niche or specialty items.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Free-From Type: Plant-Based Surge Reshapes Category Mix

Gluten-free products accounted for the largest share of the North America free-from food market in 2025, capturing 46.15% of total market revenue. The segment’s dominance is largely driven by increasing consumer awareness of gluten intolerance, celiac disease, and digestive health concerns, which has expanded demand beyond medically required diets to lifestyle-driven consumption. A growing number of consumers perceive gluten-free products as healthier alternatives, contributing to their widespread adoption across bakery, snacks, and packaged food categories. Major food manufacturers have significantly expanded their gluten-free product portfolios, improving product quality, taste, and availability across retail channels. In addition, strong distribution through supermarkets, specialty health stores, and online platforms has enhanced accessibility for consumers across the region.

Meat-free plant-based alternatives are projected to be the fastest-growing segment within the North America free-from food market, expected to register a CAGR of 9.26% through 2031. This growth is primarily driven by rising consumer interest in sustainable, ethical, and health-conscious food choices, alongside increasing awareness of environmental impacts associated with conventional meat production. The expansion of flexitarian and vegan dietary patterns has significantly boosted demand for plant-based meat substitutes across both retail and foodservice sectors. Food manufacturers are investing heavily in research and development to improve taste, texture, and nutritional profiles, making plant-based alternatives more appealing to mainstream consumers.

By End Product: Dairy Alternatives Accelerate as Bakery Matures

Bakery and confectionery products accounted for the largest share of the North America free-from food market in 2025, representing 29.77% of total revenue. The strong performance of this segment is primarily supported by high consumer demand for free-from alternatives in everyday food categories such as bread, cakes, cookies, and chocolate products. Increasing awareness of dietary sensitivities, including gluten and allergen intolerance, has encouraged manufacturers to expand free-from bakery offerings without compromising taste and texture. Continuous product innovation, including the use of alternative flours and natural sweeteners, has improved product acceptance among mainstream consumers. The segment also benefits from impulse purchasing behavior and frequent consumption patterns, sustaining its dominant position within the regional market.

Dairy alternatives are projected to be the fastest-growing segment in the North America free-from food market, expected to register a CAGR of 8.99% through 2031. Growth in this segment is largely driven by rising lactose intolerance awareness, increasing vegan and flexitarian lifestyles, and growing consumer preference for plant-based nutrition. Products such as plant-based milk, yogurt, cheese, and creamers are gaining popularity due to perceived health and environmental benefits. Manufacturers are actively introducing new formulations using ingredients such as almond, oat, soy, and coconut to enhance taste and nutritional value. Expansion of foodservice adoption, particularly in coffee chains and quick-service restaurants, has further accelerated consumption of dairy alternatives.

By Nature: Organic Premiumization Drives Margin Expansion

Conventional product lines accounted for the largest share of the North America free-from food market in 2025, representing 84.02% of the gluten-free market size. Their dominance is primarily attributed to broad affordability, extensive retail distribution, and strong brand recognition among mainstream consumers. Conventional free-from products are widely available across supermarkets, hypermarkets, and mass retail chains, ensuring higher visibility and accessibility compared to niche premium offerings. Large-scale production capabilities also enable manufacturers to maintain competitive pricing while meeting growing demand. In addition, continuous product reformulation and quality improvements have enhanced taste, texture, and nutritional value, reducing the perception gap between conventional and specialty products.

Organic variants, however, are emerging as the fastest-growing segment in the North America free-from food market, projected to expand at a CAGR of 10.05% between 2026 and 2031. Growth in this segment is driven by rising consumer preference for clean-label, non-GMO, and sustainably sourced ingredients. Health-conscious consumers increasingly associate organic certification with higher product quality, safety, and environmental responsibility. Expanding availability of organic free-from products across specialty health stores and premium retail chains has further supported market penetration. Manufacturers are responding by investing in certified organic supply chains and transparent sourcing practices to strengthen consumer trust.

By Distribution Channel: Foodservice Rebounds as On-Trade Accelerates

Off-trade outlets accounted for the largest share of the North America free-from food market in 2025, controlling 71.91% of total sales. The dominance of this segment is largely driven by strong consumer preference for purchasing free-from products through supermarkets, hypermarkets, convenience stores, and online retail platforms. These channels provide extensive product variety, competitive pricing, and easy accessibility, enabling consumers to compare brands and dietary options conveniently. The growing availability of private-label free-from products has further strengthened off-trade sales by offering affordable alternatives to premium brands. In addition, increasing at-home consumption trends and rising demand for packaged and ready-to-consume free-from foods have supported consistent retail growth.

On-trade foodservice is emerging as the fastest-growing distribution channel in the North America free-from food market, projected to expand at a CAGR of 9.63% through 2031. Growth in this segment is primarily supported by increasing consumer demand for allergen-friendly and dietary-specific menu options in restaurants, cafés, and quick-service outlets. Foodservice operators are increasingly incorporating gluten-free, dairy-free, and plant-based offerings to cater to evolving consumer preferences and dietary restrictions. Rising dining-out frequency and the expansion of health-focused restaurant concepts have further accelerated adoption of free-from ingredients in foodservice menus. Partnerships between food manufacturers and restaurant chains are also contributing to wider availability and visibility of free-from products.

Geography Analysis

The United States accounted for the largest share of the North America free-from food market in 2025, generating 79.89% of total regional revenue. The country’s dominance is supported by high consumer awareness regarding food allergies, dietary intolerances, and health-focused eating habits. A well-established retail infrastructure, combined with strong presence of leading food manufacturers and private-label brands, has enabled widespread availability of free-from products across multiple categories. Continuous product innovation, particularly in gluten-free, dairy-free, and plant-based segments, has further strengthened market expansion. In addition, rising demand for clean-label and functional food products among health-conscious consumers continues to support steady growth.

Mexico is projected to be the fastest-growing market in the North America free-from food sector, expected to register a CAGR of 9.84% through 2031. Growth in the country is driven by increasing urbanization, rising disposable incomes, and growing consumer awareness of healthier dietary alternatives. Expanding retail networks and the increasing presence of international food brands have improved access to free-from products across major cities. Changing lifestyle patterns and a gradual shift toward preventive healthcare are encouraging consumers to adopt gluten-free, lactose-free, and plant-based food options. Food manufacturers are also increasing investments in localized product offerings to cater to regional taste preferences.

Canada represents a steadily growing market within the North America free-from food landscape, supported by strong demand for premium, organic, and clean-label food products. High awareness of dietary sensitivities and increasing adoption of plant-based diets have encouraged consistent consumption of free-from alternatives across retail and foodservice channels. The country benefits from stringent food labeling regulations, which enhance consumer confidence and transparency in product selection. Growing interest in sustainability and ethically sourced ingredients has further supported demand for organic and allergen-free food options.

Competitive Landscape

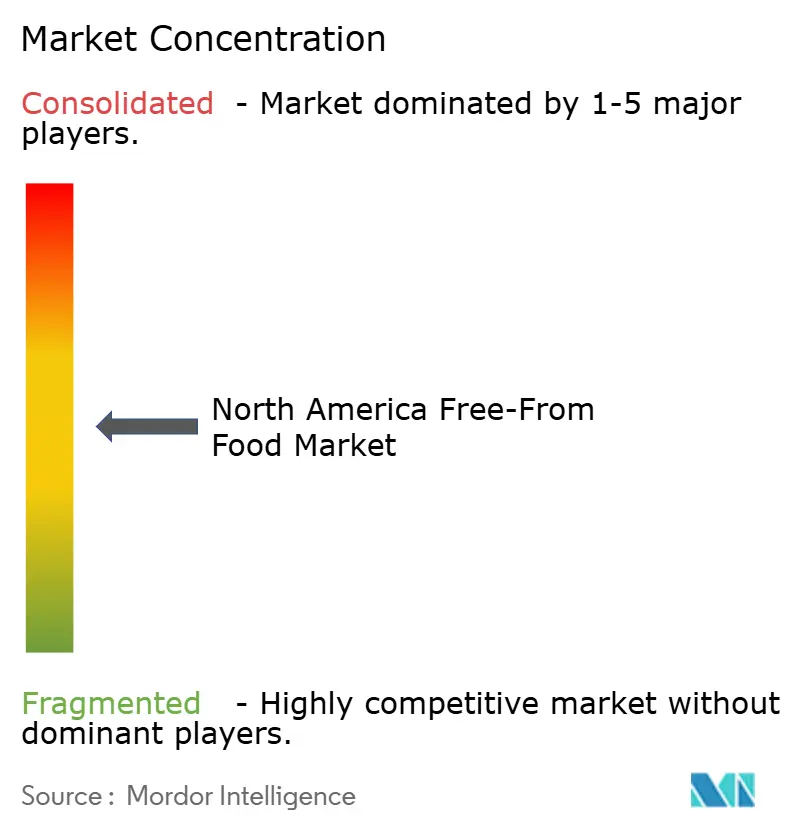

The North American free-from food market exhibits a moderately fragmented competitive landscape, characterized by the presence of large multinational food companies, specialized health-focused brands, and emerging niche players. While established manufacturers hold strong brand recognition and distribution networks, smaller companies continue to gain traction by targeting specific dietary needs such as gluten-free, dairy-free, allergen-free, and plant-based formulations. The diversity of product categories within the free-from segment allows multiple players to coexist without a single company dominating the overall market. Regional preferences, evolving consumer dietary trends, and rapid product innovation further contribute to market fragmentation. Retail private labels have also strengthened their presence by offering competitively priced free-from alternatives, intensifying competition across mainstream channels.

Competition in the market is largely driven by innovation, product quality, pricing strategies, and brand trust. Leading players invest heavily in research and development to improve taste, texture, and nutritional value, addressing earlier challenges associated with free-from products. Clean-label formulations, organic certifications, and non-GMO claims have become key differentiators as consumers increasingly prioritize health and sustainability. Companies are also expanding their distribution through e-commerce platforms and direct-to-consumer channels to strengthen market reach. Strategic partnerships with retailers and foodservice operators are becoming more common, allowing brands to enhance visibility and accessibility.

At the same time, smaller and innovative firms continue to introduce specialized products that cater to evolving consumer preferences, maintaining competitive diversity. Investments in advanced manufacturing technologies and sustainable sourcing practices are becoming increasingly important for long-term competitiveness. Companies are also focusing on supply chain optimization to manage ingredient sourcing challenges and cost pressures. The growing influence of health-conscious consumers and regulatory emphasis on clear labeling further encourages product innovation and compliance.

North America Free-From Food Industry Leaders

-

Conagra Brands Inc.

-

The Hain Celestial Group

-

General Mills Inc.

-

Danone S.A.

-

The Kraft Heinz Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Eshbal Functional Food Inc. has signed a binding agreement to acquire Gluten Free Nation. Based in Houston, Gluten Free Nation bakes gluten-free breads and other baked products. This acquisition aims to diversify Eshbal's product lineup and leverage Gluten Free Nation's established sales and distribution channels to accelerate Eshbal's market entry for its gluten-free offerings.

- May 2025: Beyond Meat, Inc. broadened its reach by rolling out Beyond Chicken Pieces in 1,900 Kroger stores nationwide. Infused with avocado oil rich in monounsaturated fats, these plant-based chicken pieces deliver 21g of protein per serving. They contain just 0.5g of saturated fat, are cholesterol-free, and boast no GMOs, added hormones, or antibiotics.

- April 2025: Maïzly made its debut in the U.S. plant-based milk market with a corn-based milk product. Available in both original and chocolate flavors, this dairy-free and gluten-free milk blends corn, chickpea protein, and coconut oil. Enhanced with vitamins D2, A, E, and calcium, it also boasts 75% less sugar than conventional dairy milk.

- March 2025: Juicy Marbles expanded its Meaty Meat range with the launch of a new pork alternative product. Named Pork-ish, this whole-cut pork analog boasts a high protein content and comes at a competitive price. Priced at USD 10 for a 180g pack, it stands out as the most budget-friendly option in the company's online store.

North America Free-From Food Market Report Scope

Free-from food refers to food products that are specifically formulated or processed to exclude certain ingredients that some consumers avoid due to allergies, intolerances, medical conditions, lifestyle choices, or personal health preferences. The North America free-from-food market is segmented by product type, end product, nature, distribution channel and geography. Based on free-from type, the market is segmented into gluten free, dairy-free, meat-free, sugar-free and other types. By end product the market is segmented into bakery and confectionery, products, meat substitutes and analogues, dairy alternatives, snacks, ready meals and meal kits and other products. By nature, the market is segmented into conventional and organic. By distribution channel, the market is segmented into on-trade and off-trade. By geography, the market is segmented into United States, Canada, Mexico and Rest of North America. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million) and volume (Tons).

By Free-From Type

| Gluten-Free |

| Dairy-Free/Lactose-Free |

| Meat-Free (Plant-based) |

| Sugar-Free/Low-GI |

| Other Types |

By End Product

| Bakery and Confectionery Products |

| Meat Substitutes and Analogues |

| Dairy Alternatives |

| Snacks |

| Ready Meals and Meal Kits |

| Other Products (Baby and Infant Foods, Sauces, Condiments) |

By Nature

| Conventional |

| Organic |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Free-From Type | Gluten-Free | |

| Dairy-Free/Lactose-Free | ||

| Meat-Free (Plant-based) | ||

| Sugar-Free/Low-GI | ||

| Other Types | ||

| By End Product | Bakery and Confectionery Products | |

| Meat Substitutes and Analogues | ||

| Dairy Alternatives | ||

| Snacks | ||

| Ready Meals and Meal Kits | ||

| Other Products (Baby and Infant Foods, Sauces, Condiments) | ||

| By Nature | Conventional | |

| Organic | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

What is the current market size of the market?

The market is valued at USD 45.11 billion in 2026 and projected to reach USD 67.64 billion in 2031.

Which sales channel currently moves the most free-from products?

Off-trade retail outlets, led by supermarkets and hypermarkets, captured 71.91% of 2025 revenue thanks to dedicated aisles and end-cap displays.

Where is the strongest geographic upside over the next five years?

Mexico is projected to post a 9.84% CAGR through 2031, outstripping the United States and Canada as middle-class spending and aligned labeling rules accelerate adoption.

How concentrated is supplier power in the category today?

The top five companies hold 55% of 2025 revenue, indicating moderate concentration that still leaves room for agile regional and direct-to-consumer brands.

Page last updated on: