Food Grade Alcohol Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.62 Billion |

| Market Size (2031) | USD 5.49 Billion |

| Growth Rate (2026 - 2031) | 3.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

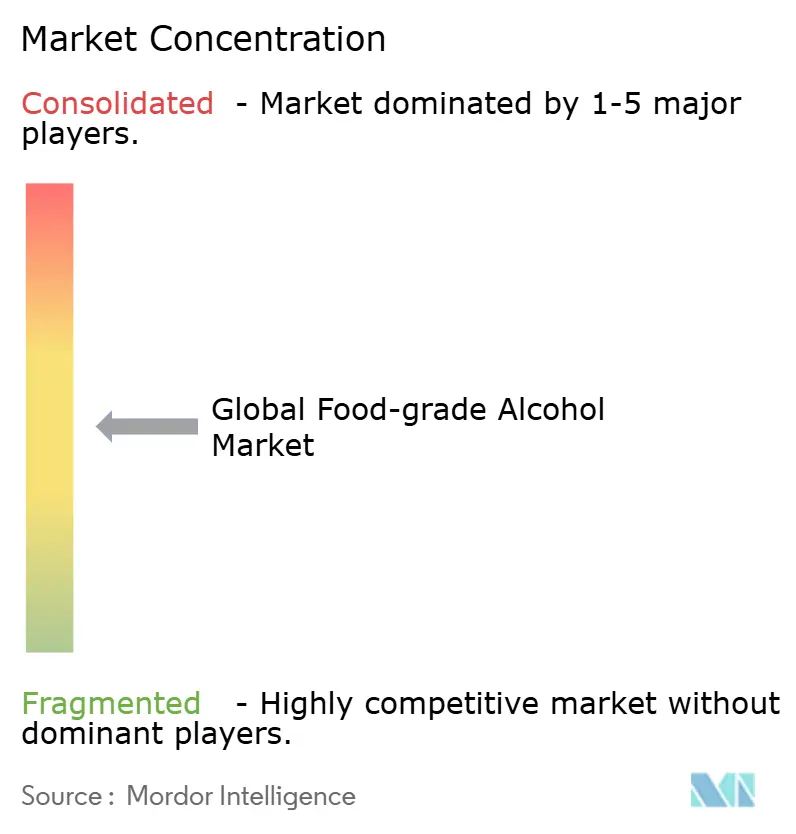

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Grade Alcohol Market Analysis by Mordor Intelligence

The food grade alcohol market size is expected to grow from USD 4.46 billion in 2025 to USD 4.62 billion in 2026 and is forecast to reach USD 5.49 billion by 2031 at 3.51% CAGR over 2026-2031. The market demonstrates stability through its diverse applications in food processing, beverages, dietary supplements, and pharmaceutical excipients. The Food and Drug Administration's (FDA) classification of ethanol as Generally Recognized as Safe (GRAS) provides manufacturers with clear regulatory compliance frameworks. The market growth is supported by the increasing adoption of clean-label ingredients, with food manufacturers replacing synthetic solvents with natural alternatives to address consumer demand for ingredient transparency. The growth of ready-to-drink beverages and hard seltzers creates additional demand, while the rise of plant-based and vegan products requires food-grade alcohol for extraction processes instead of conventional chemical solvents.

Key Report Takeaways

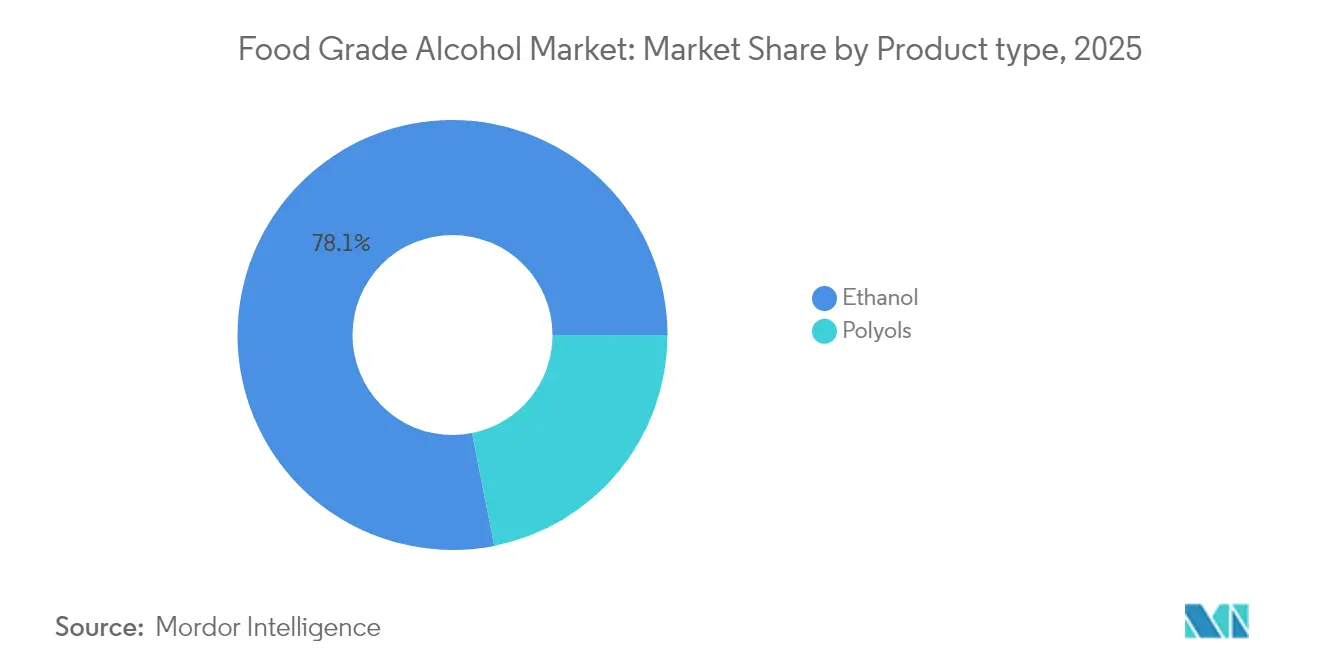

- By product type, ethanol commanded 78.12% of the food grade alcohol market share in 2025; polyols are forecast to rise at a 5.23% CAGR through 2031.

- By source, sugarcane and molasses led with 32.55% revenue in 2025, while corn-based output is poised for a 4.89% CAGR to 2031.

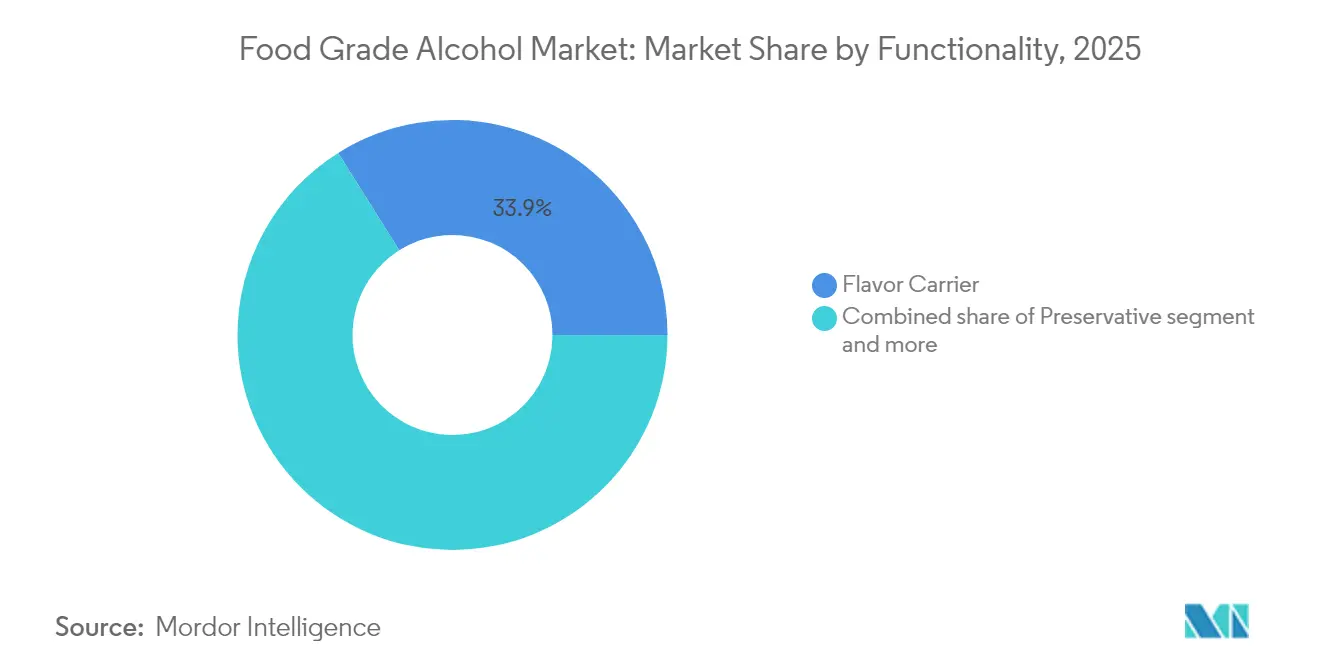

- By functionality, flavor carriers held 33.92% of the food grade alcohol market size in 2025; solvent and extraction roles show the fastest 5.05% CAGR through 2031.

- By application, food processing delivered 29.12% of 2025 revenue; dietary supplements represent the fastest 5.48% CAGR through 2031.

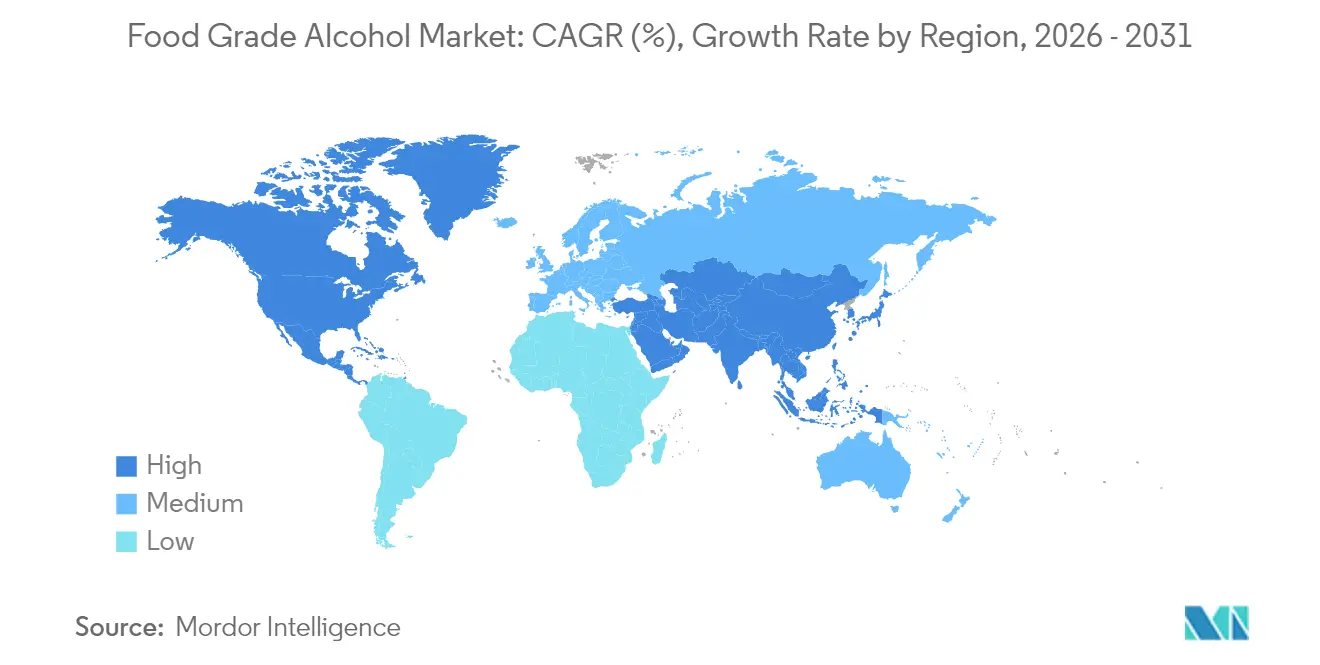

- By geography, Europe captured 33.05% of 2025 revenue; Asia-Pacific advances at a 5.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food Grade Alcohol Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for clean-label solvents in food and beverages | +0.8% | Global, with strongest adoption in North America and European Union | Medium term (2-4 years) |

| Expansion of ready-to-drink (RTD) and hard-seltzer categories | +0.6% | North America and the Europe core, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Rising Consumer preference for Non-GMO and natural ingredients | +0.5% | Global, led by developed markets | Long term (≥ 4 years) |

| Growth of the functional foods and beverages market | +0.4% | APAC core, spill-over to North America and European Union | Medium term (2-4 years) |

| Use of food-grade alcohol in insect Protein extraction processes | +0.2% | European Union and North America early adoption, Asia-Pacific emerging | Long term (≥ 4 years) |

| Growing use of food-grade alcohol in plant-based and vegan product formulations | +0.3% | Global, concentrated in urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Clean-label Solvents in Food and Beverages

The shift toward clean-label solvents in food processing is driven by increased consumer demand for ingredient transparency and stricter regulations on chemical usage. The European Union's reclassification of hexane as a neurotoxicant has led manufacturers to adopt safer alternatives, particularly food-grade ethanol for extraction processes. This regulatory change influences global markets as multinational food companies align their formulations across regions to maintain product consistency. Clean-label reformulations command higher prices while reducing manufacturers' exposure to health-related liability claims. The Generally Recognized as Safe (GRAS) status of food-grade alcohol eliminates the need for extensive safety testing required for new solvents. The adoption of clean-label specifications by private-label retailers has created supply chain requirements that benefit established food-grade alcohol manufacturers.

Expansion of Ready to Drink (RTD) and Hard-Seltzer Categories

The Ready-to-Drink (RTD) and hard-seltzer segments have transformed alcohol consumption patterns, generating new demand for high-purity food-grade alcohol. These products appeal to health-conscious consumers by offering lower-calorie options, with hard seltzers containing approximately 100 calories per serving compared to 150-200 calories in beer. The production of these beverages requires high-purity ethanol to maintain their characteristic clean, neutral taste profiles, which has increased the premium pricing for food-grade alcohol suppliers. Asahi's strategic focus on health and wellness business expansion, including alcohol alternatives and functional ingredients, demonstrates the broader industry shift toward these trends. Despite market saturation concerns, the category continues to grow through innovations in flavors and functional additives. The production requirements create significant barriers to entry, benefiting established food-grade alcohol suppliers with existing purification infrastructure and consolidating market share among current manufacturers.

Rising Consumer Preference for Non-GMO and Natural Ingredients

Consumer preference for non-GMO and natural ingredients has shifted from niche demand to mainstream expectation, transforming sourcing strategies across the food industry. According to the International Food Information Council (IFIC), in 2023, 28% of respondents in the United States reported regularly purchasing food and beverages labeled as non-GMO [1]Source: International Food Information Council (IFIC), "2023 Food and Health Survey", foodinsight.org. This change significantly affects food-grade alcohol production, as feedstock selection influences product positioning and pricing. Organic and non-GMO certified ethanol commands higher prices compared to conventional alternatives, creating opportunities for producers who invest in supply chain verification and certification processes. The trend extends beyond food applications into pharmaceutical excipients and cosmetic ingredients, where natural origin claims provide differentiation in premium markets. Regulatory frameworks support this transition by emphasizing natural ingredient sourcing. The economic impact is significant, as non-GMO verification requires extensive supply chain documentation and third-party auditing. This creates operational complexity that benefits larger producers with established quality management systems while potentially limiting smaller competitors who lack certification resources.

Growth of the Functional Foods and Beverages Market

The growth of the functional foods and beverages market drives the food-grade alcohol market, as ethanol and other food-grade alcohols are essential in formulating, stabilizing, and delivering bioactive ingredients. These functional products require high-purity solvents to extract, preserve, and integrate active compounds. Food-grade ethanol serves as the primary solvent due to its safety for human consumption, effectiveness in dissolving both water- and fat-soluble components, and compliance with clean-label and organic certification requirements. The alcohol-based extraction method maintains the integrity and bioavailability of polyphenols, alkaloids, and flavonoids from herbal ingredients used in immunity boosters, energy drinks, nootropics, and digestive products. According to the China Nutrition and Health Food Association, China's functional food production reached 852,000 metric tons in 2023, increasing from 787,000 metric tons in the previous year [2]Source: China Nutrition and Health Food Association, "Total production volume of health and functional food in China", cnhfa.org.cn. This production increase aligns with China's focus on preventive health and nutraceutical development, generating higher demand for botanical extracts and natural bioactive delivery systems that utilize food-grade ethanol.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High taxation and excise duties on alcohol | -0.9% | Global, particularly severe in Australia an European Union | Short term (≤ 2 years) |

| Cultural, ethical, and religious restrictions | -0.4% | Middle East, South Asia, select regions | Long term (≥ 4 years) |

| Stringent regulatory frameworks for food-grade alcohol | -0.6% | Global, with varying intensity by jurisdiction | Medium term (2-4 years) |

| Volatility in aw material prices | -0.7% | Global, concentrated in agricultural regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Taxation and Excise Duties on Alcohol

The increasing alcohol taxation across major markets poses a significant challenge to the food-grade alcohol market growth. Government policies prioritize revenue generation through higher taxes, impacting industry operations. In FY2023, the United States federal excise tax structure generated USD 11.1 billion annually, with spirits accounting for 61% of the total alcohol tax. [3]Source: Library of Congress, "Alcohol Excise Taxes", www.congress.gov. These tax increases affect the entire supply chain as food manufacturers experience higher input costs, which they must either absorb or transfer to consumers, potentially reducing the demand for alcohol-containing products. The varying tax rates across jurisdictions and evolving reporting requirements add regulatory complexity for manufacturers. For instance, New Zealand's recent adjustment of excise rates from 49.855 cents to 53.170 cents per liter demonstrates the ongoing trend of increasing alcohol taxation globally.

Stringent Regulatory Frameworks for Food-Grade Alcohol

Regulatory complexity in the food-grade alcohol industry continues to increase as jurisdictions implement comprehensive food safety frameworks. The Food Safety Modernization Act requires distilleries to implement preventive controls and hazard analysis protocols, which creates significant operational costs, particularly affecting smaller producers. The Current Good Manufacturing Practice regulations under 21 CFR Part 110 require extensive documentation, personnel training, and facility maintenance standards, necessitating substantial investment in quality management systems. International regulations add further complexity, as producers must comply with multiple frameworks to access global markets. For instance, the European Union's spirit drinks regulations mandate the use of agricultural-origin ethyl alcohol and prohibit synthetic alternatives, restricting supply chain flexibility. The evolving nature of food safety standards requires continuous monitoring and adaptation, resulting in ongoing compliance costs that typically favor larger producers with established regulatory affairs departments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ethanol Dominance Faces Polyol Innovation

Ethanol holds a dominant 78.12% market share in 2025, supported by its established regulatory framework and diverse applications in food processing, beverages, and pharmaceutical excipients. Polyols represent the fastest-growing segment, with a 5.23% compound annual growth rate (CAGR) through 2031, driven by increased adoption in sugar-free and diabetic-friendly products. This growth pattern indicates a market shift, as traditional ethanol applications stabilize while polyol applications expand to meet demand from health-conscious consumers and functional food manufacturers. Polyols offer distinct advantages, including lower caloric content and enhanced stability in specific formulations, making them suitable for specialized dietary products.

The regulatory framework offers advantages for polyols, particularly in applications where ethanol faces limitations due to its psychoactive properties, especially in products intended for children and health-conscious consumers. The Food and Drug Administration's guidelines under 21 CFR Part 172 provide specific parameters for polyol use in food applications, reducing compliance uncertainties for manufacturers. The production of polyols involves fewer regulatory requirements compared to ethanol distillation, which must comply with both food safety standards and alcohol taxation rules. In international trade, polyol-based products encounter fewer import barriers and tax complications than ethanol-containing products.

By Sources: Feedstock Diversification Accelerates

Sugarcane and molasses hold a 32.55% market share in 2025, maintaining their position as primary feedstocks due to established supply chains and economic advantages in tropical regions, particularly in Brazil's ethanol industry. Corn-based production demonstrates the highest growth rate at 4.89% CAGR, driven by North American agricultural strengths and improved corn-to-ethanol conversion efficiencies. Wheat and cassava serve as alternative feedstocks, each leveraging regional agricultural advantages. Alternative feedstocks, including agricultural waste and cellulosic materials, occupy niche segments with potential for expansion as sustainability requirements increase.

Brazil produced 35.3 billion liters of ethanol in 2023, a 15.3% increase from 2022, processing 713 million tons of sugarcane according to the Energy Research Office. This production volume provides cost advantages for sugarcane-based ethanol, especially in food-grade applications where established processes meet strict purity standards. Corn-based production operates under distinct economic conditions, primarily influenced by corn prices. The concentration of feedstock production in specific regions creates supply vulnerabilities, as adverse weather or regulatory changes in major producing areas can affect food-grade alcohol supply and prices.

By Functionality: Extraction Applications Drive Innovation

The food-grade alcohol market demonstrates significant segmentation across functional applications, with flavor carriers maintaining the dominant position at 33.92% market share in 2025. This prominence stems from the fundamental role of food-grade alcohol in the extraction and delivery of taste compounds throughout the food and beverage manufacturing sector. The solvent and extraction agent applications exhibit substantial growth potential, projecting a 5.05% CAGR through 2031, primarily attributed to the increasing adoption in nutraceutical production and botanical extract manufacturing processes.

In the global market landscape, preservative applications continue to generate steady demand from food manufacturers, while texturizer and humectant functions demonstrate growth patterns that align with the overall food industry expansion. The diversification across functional applications positions food-grade alcohol as a versatile ingredient in the global food processing sector, establishing multiple revenue channels and reducing market susceptibility to disruptions within individual application segments.

By Application: Dietary Supplements Lead Growth

Food processing maintains the largest application segment with a 29.12% market share in 2025, as food-grade alcohol serves as a key component in manufacturing processes across multiple food categories. Dietary supplements represent the fastest-growing application with a 5.48% CAGR through 2031, supported by expanding nutraceutical markets and increased consumer focus on preventive healthcare. The growth in dietary supplements stems from aging populations, higher healthcare costs, and greater consumer awareness of nutritional supplementation. Food-grade alcohol serves both in direct formulation and in the extraction and purification of botanical ingredients, where its safety profile and regulatory compliance make it preferable to alternative solvents.

Beverages constitute a significant and stable application segment, while pharmaceutical excipients demonstrate consistent growth in line with pharmaceutical sector expansion. The pharmaceutical excipients segment benefits from strict quality requirements, favoring established food-grade alcohol manufacturers with strong quality management systems and regulatory compliance. Manufacturers meeting both food and pharmaceutical quality standards can potentially secure premium pricing for pharmaceutical-grade food alcohol products. Additional applications in cosmetics and personal care products contribute to market diversity, though these remain smaller by volume.

Geography Analysis

Europe holds 33.05% of the global market share in 2025, driven by EU Regulation 2019/787 that requires agricultural-origin ethanol for spirit drinks. This regulation ensures consistent demand for food-grade alcohol while prohibiting synthetic alternatives. The region's market dominance is supported by its established distillation industries, advanced food processing sectors, and consumer demand for natural ingredients. The unified regulations across EU member states enable producers to achieve operational efficiencies while maintaining strict quality standards. European demand continues to grow through applications in plant-based and organic food products, aligned with the region's focus on sustainability.

Asia-Pacific shows the highest growth rate at 5.11% CAGR through 2031. This growth is attributed to the expansion of food processing industries, higher disposable incomes, and increased adoption of Western consumption patterns. The region's market potential is enhanced by its large population, urban development, and changing dietary preferences toward processed and convenience foods. China's regulatory environment continues to develop, with the State Administration for Market Regulation implementing new labeling requirements for alcohol-containing food products. Japan and Australia's regulatory standards align with global requirements, supporting international trade and investment in food-grade alcohol production.

North America maintains a strong market position through its developed ethanol production infrastructure and food processing industries, despite showing moderate growth in mature markets. The region leverages its abundant corn resources and efficient supply chains for food-grade alcohol production. In South America, Brazil's significant ethanol production capacity contributes to global supply while developing local food processing applications that incorporate food-grade alcohol.

Competitive Landscape

The food-grade alcohol market demonstrates moderate fragmentation with a concentration, reflecting balanced competition between multinational corporations and regional producers. This market structure enables both cost leadership strategies through scale and niche differentiation approaches across various market segments. Companies like Archer-Daniels-Midland Company, Cargill, Incorporated, Wilmar International Limited, and Roquette Frères leverage their vertical integration and global distribution networks to achieve economies of scale.

The market favors companies with strong regulatory compliance capabilities, as international food safety requirements create entry barriers for smaller producers without dedicated quality management systems. Companies increasingly prioritize sustainability credentials and clean-label positioning to support food manufacturers' sustainability commitments and transparency initiatives across global markets. Major producers focus on technology adoption for process optimization and quality enhancement, investing in advanced purification technologies and analytical capabilities to meet pharmaceutical-grade standards.

The food-grade alcohol industry presents opportunities in emerging applications such as insect protein processing and botanical extractions, where early market entry can establish leadership positions. The industry structure supports both acquisition-based consolidation and organic growth, particularly in developing regions. Regulatory requirements and capital investments create entry barriers while rewarding operational efficiency and strong international customer relationships, shaping the competitive landscape across different geographical markets.

Food Grade Alcohol Industry Leaders

-

Archer-Daniels-Midland Company

-

Cargill, Incorporated

-

Wilmar International Limited

-

Roquette Frères

-

Manildra Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Godavari Biorefineries announced an investment in grain/corn-based ethanol production. The company plans to invest INR 130 crore to establish a new 200 KLPD corn/grain-based distillery alongside its existing operations. This expansion will enhance operational flexibility through dual-feedstock capability.

- January 2024: Associated Alcohols and Breweries Limited (AABL) has commenced commercial production at its ethanol plant in Barwaha, near Indore, Madhya Pradesh. The grain-based ethanol facility has a capacity of 130 KLPD and was established with an investment of approximately INR 150 crore.

- September 2023: Greenfield Global Inc. and REMET Alcohols, Inc. formed a partnership to address rising demand for high-purity and denatured alcohol in California and Western United States. Greenfield maintains direct customer supply while REMET handles its own client base through Greenfield ethanol procurement.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the food-grade alcohol market as all ethanol and polyol alcohols that are produced under food-safety regulations (for instance, FDA GRAS and equivalent EU directives) and then sold for use as solvents, preservatives, flavor carriers, texturizers, or extraction media in packaged foods, beverages, dietary supplements, and pharmaceutical excipients.

Scope exclusion: fuel, industrial, or denatured alcohol streams are left outside the boundary so that our baseline only reflects volumes legally permitted for human consumption.

Segmentation Overview

-

By Proudct Type

- Ethanol

- Polyols

-

By Sources

- Sugarcane and Molasses

- Corn

- Wheat

- Cassava

- Other Feedstocks

-

By Functionality

- Preservative

- Flavor Carrier

- Solvent and Extraction Agent

- Texturizer and Humectant

-

By Application

- Food Processing

- Beverages

- Dietary Supplements

- Pharmaceutical Excipients

- Other Applications

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts run structured interviews and short surveys with regional grain spirits producers, ingredient blenders, craft-beverage formulators, and regulatory compliance officers across North America, Europe, Asia-Pacific, and Latin America. Their insights validate purity cut-offs, prevailing average selling prices, and the share of food-grade output that flows into beverages versus nutraceuticals, filling gaps that desk work alone cannot close.

Desk Research

We start with public datasets that track raw material and finished-alcohol flows, such as FAOSTAT crop balances, USDA Foreign Agricultural Service trade briefs, Eurostat COMEXT customs codes, and the International Sugar Organization's quarterly bulletins. Production and sales disclosures drawn from listed distilleries' 10-Ks, distilled-spirits association white papers, and filings captured through D&B Hoovers further anchor supplier revenue and capacity. News and price snapshots are screened in Dow Jones Factiva, while patent clusters on extraction processes are sampled in Questel to spot emerging demand niches. This list is illustrative; many additional publications are tapped to confirm and clarify numbers before modeling.

Market-Sizing & Forecasting

A top-down model converts country-level beverage and pharmaceutical output into potential demand pools and then applies food-grade penetration ratios that we refined during primary calls. Supplier roll-ups of reported revenue and sampled ASP multiplied by volume checks act as a bottom-up cross-check. Key variables tracked include sugarcane and corn feedstock availability, ethanol yield per ton, per-capita spirits intake, polyol export volumes, regulatory purity shifts, and substitution toward plant-based extracts. Forecasts to 2030 rely on a multivariate regression that links those drivers to historical volume swings, with scenario cushions for policy or crop shocks. Where bottom-up data are thin, interpolation uses three-year moving averages and nearest-neighbor pricing.

Data Validation & Update Cycle

Triangulation across the two model views highlights outliers, which our review panel revisits before sign-off. Outputs are compared with independent trade and consumption indicators; material variances trigger re-work. Reports refresh each year, and an interim update is issued when feedstock price spikes, tariff actions, or regulatory amendments could shift the baseline.

Why Mordor's Food Grade Alcohol Baseline Earns Trust

Published estimates often diverge because firms pick different purity thresholds, bundle or strip out polyols, and refresh at uneven intervals.

Key gap drivers include, first, variations in product scope; second, whether value-added taxes or excise duties are netted; and third, the cadence with which exchange rates and ASP drift are re-benchmarked. Mordor's disciplined scope definition, annual refresh policy, and dual-view modeling help decision-makers rely on a figure that is neither overstated nor unduly conservative.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.46 B (2025) | Mordor Intelligence | - |

| USD 6.70 B (2024) | Global Consultancy A | Includes non-food industrial ethanol and sugar alcohol sweeteners |

| USD 3.59 B (2024) | Regional Consultancy B | Excludes polyols and counts only beverage-grade ethanol |

| USD 9.20 B (2024) | Trade Journal C | Bundles personal-care alcohols and applies higher ASP without currency realignment |

In short, the comparison shows that once scope, purity, and pricing assumptions are aligned, Mordor's figure sits near the midpoint, offering a balanced and transparent baseline that users can retrace to clearly documented inputs and repeatable steps.

Key Questions Answered in the Report

What is the current value of the food grade alcohol market?

In 2026 the food grade alcohol market is valued at USD 4.62 billion and is projected to reach USD 5.49 billion by 2031.

Which product type dominates the food grade alcohol market?

Ethanol dominates with a 78.12% share in 2025, while polyols are growing fastest at a 5.23% CAGR.

Why is Asia-Pacific the fastest-growing region?

Rapid expansion of food processing facilities, higher disposable incomes, and evolving dietary patterns push Asia-Pacific to a 5.11% CAGR through 2031.

How do excise taxes affect the food grade alcohol market?

Rising excise taxes, such as Australia’s above-inflation hikes and the US federal levy, raise input costs and can dampen demand in downstream food and beverage sectors.

Page last updated on: