UPS Battery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

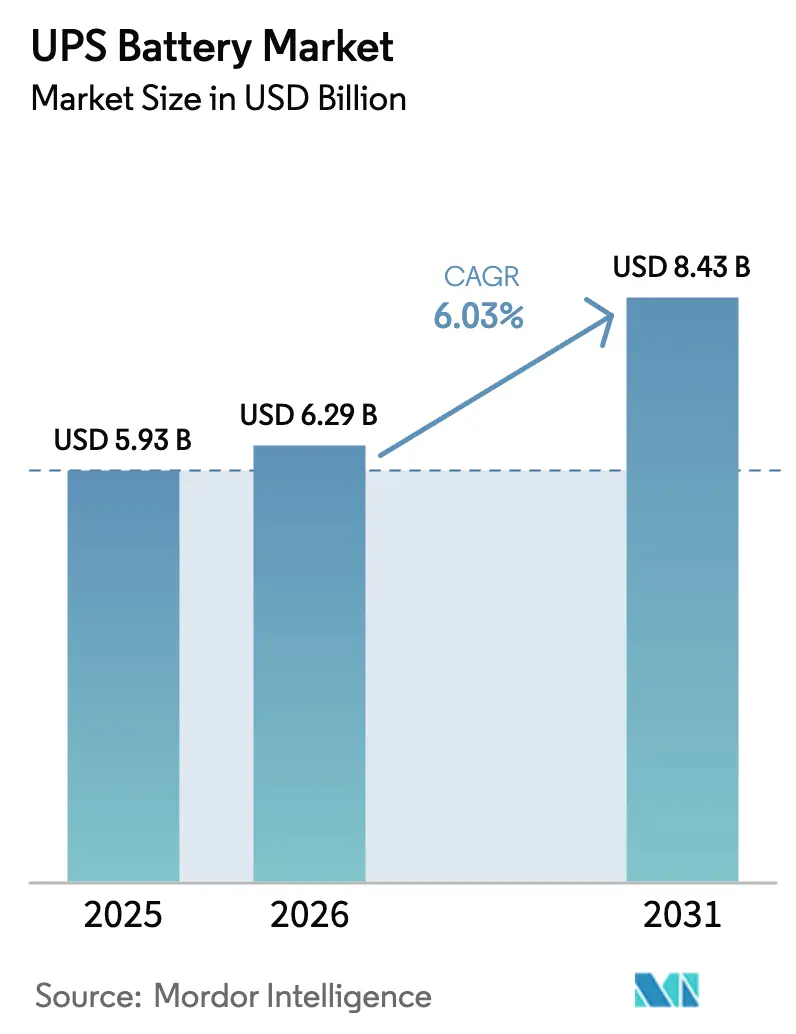

| Market Size (2026) | USD 6.29 Billion |

| Market Size (2031) | USD 8.43 Billion |

| Growth Rate (2026 - 2031) | 6.03% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UPS Battery Market Analysis by Mordor Intelligence

The UPS battery market size was valued at USD 5.93 billion in 2025 and estimated to grow from USD 6.29 billion in 2026 to reach USD 8.43 billion by 2031, at a CAGR of 6.03% during the forecast period (2026-2031). Strong hyperscale colocation demand, an accelerated migration from valve-regulated lead-acid to lithium-ion chemistries, and 5G densification programs anchor a more capital-efficient growth phase for the UPS battery market. Edge data center proliferation in North America and Europe, reinforced by carbon accounting mandates that penalize Scope 2 emissions, is catalyzing lithium-ion retrofits that lower cooling loads and reduce rack weight. Asia-Pacific remains pivotal as telecom-tower deployments in India, Indonesia, and Vietnam sustain volume momentum, while Africa’s secondary-life electric-vehicle battery repurposing agreements unlock micro-grid economics that were previously unattainable. Competitive intensity is rising as incumbents embed battery-management intelligence into proprietary UPS frames, while new chemistries such as nickel-zinc carve out safety-centric niches.

Key Report Takeaways

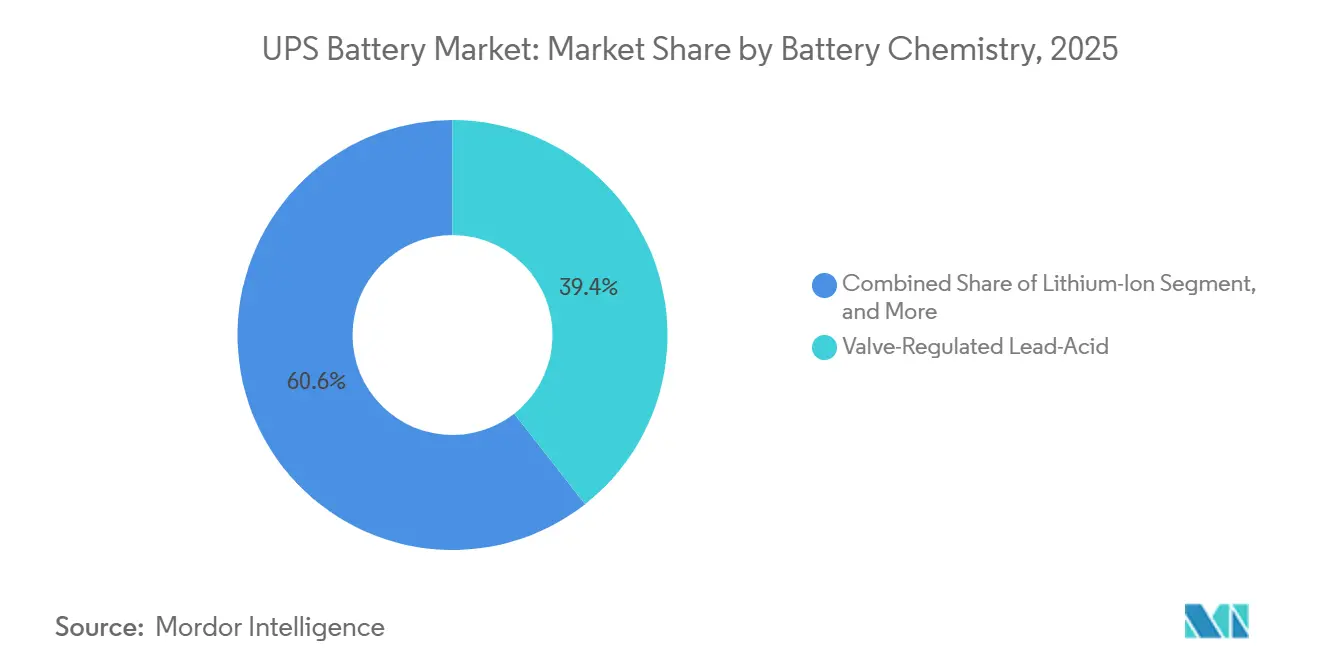

- By battery chemistry, valve-regulated lead-acid led with 39.41% of UPS battery market share in 2025; lithium-ion is forecast to expand at a 7.37% CAGR through 2031.

- By power rating, 10-100 kVA systems held a 34.73% share of the UPS battery market in 2025, whereas installations above 250 kVA are projected to grow at a 6.84% CAGR through 2031.

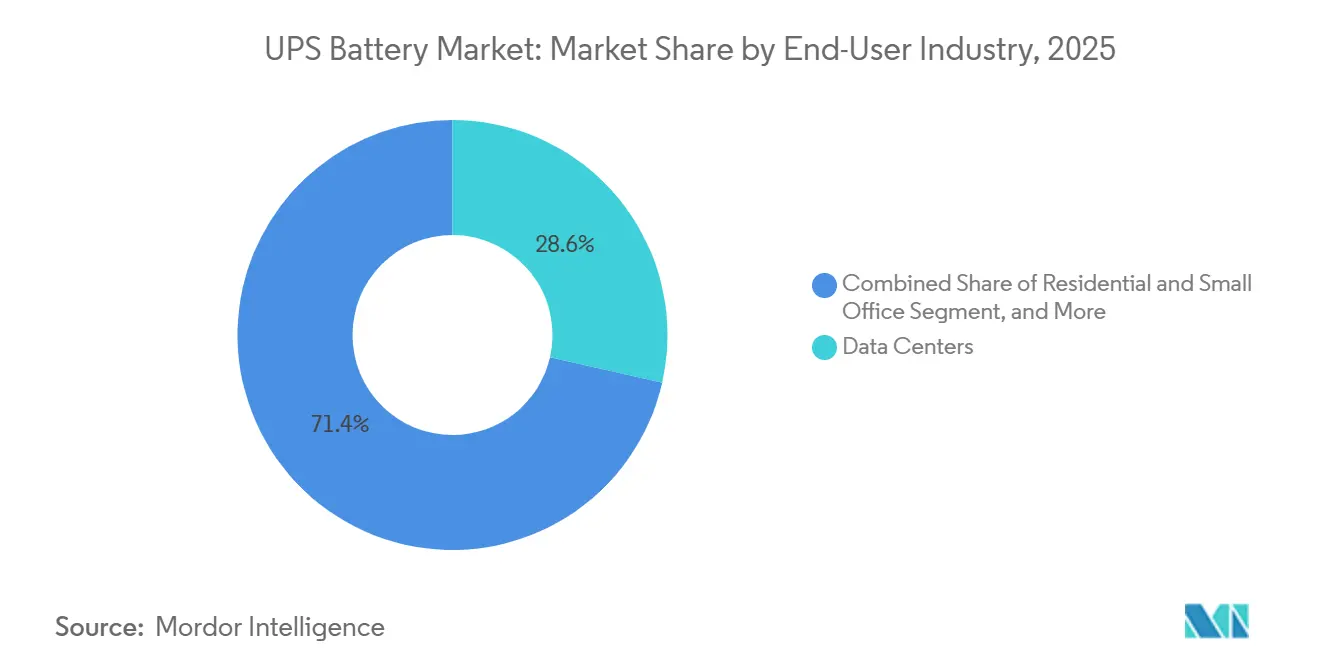

- By end user, data centers accounted for 28.56% of the UPS battery market in 2025, while residential and small-office deployments are advancing at a 7.89% CAGR between 2026-2031.

- By sales channel, original-equipment-manufacturer deliveries commanded 53.47% of UPS battery market share in 2025 and are expanding at a 6.44% CAGR through 2031.

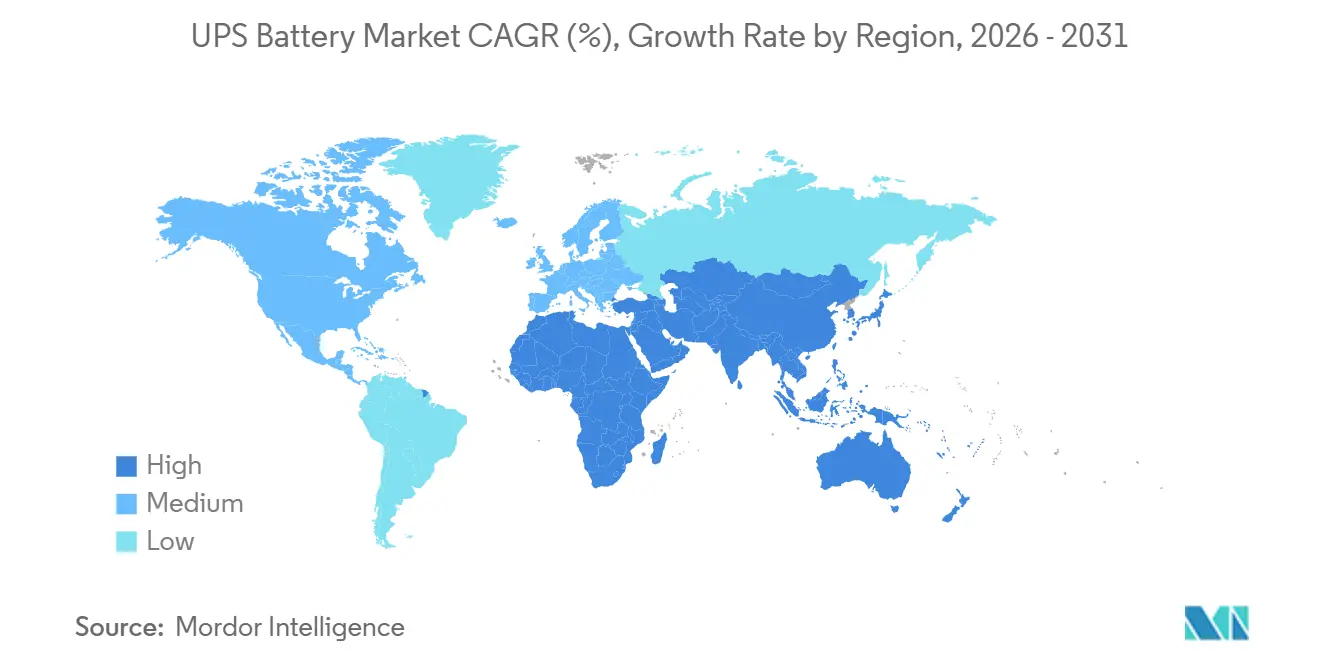

- By geography, Asia-Pacific captured 36.82% of the UPS battery market in 2025, and Africa is on track for the fastest regional growth at a 7.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global UPS Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising edge-data-center deployments driving compact lithium-ion UPS adoption | +1.2% | North America and Europe | Medium term (2-4 years) |

| 5G macro and micro-cell rollout accelerating telecom-tower backup demand | +1.1% | Asia-Pacific core, spill-over to Middle East and Africa | Short term (≤ 2 years) |

| Hyperscale colocation shift from VRLA to lithium-ion to cut TCO and rack weight | +1.0% | Global | Medium term (2-4 years) |

| Grid-outage frequency and hurricane-resilience programs boosting residential and commercial installations | +0.9% | US Gulf and Caribbean | Short term (≤ 2 years) |

| Carbon-accounting mandates incentivizing Scope 2 emission cuts through high-cycle LFP UPS retrofits | +0.7% | Europe, early adoption in North America | Long term (≥ 4 years) |

| Secondary-life EV battery repurposing lowering CAPEX for micro-grid UPS | +0.6% | Africa and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Edge-Data-Center Deployments Driving Compact Lithium-Ion UPS Adoption

Edge-computing facilities in North America and Europe expanded by more than 30% in 2025, putting pressure on floor-load limits that preclude installing heavy valve-regulated lead-acid strings. Lithium-ion UPS modules provide the same backup runtime while weighing roughly one-third as much, freeing critical rack space for high-density servers.[1]Schneider Electric SE, “Annual Report 2025,” se.com Schneider Electric reported that lithium-ion attachments to its Galaxy family rose 41% year over year as content-delivery and real-time analytics workloads migrated to edge nodes. The updated IEC 62040-3 standard now permits lithium-ion UPS without additional fire-suppression measures when cell-level monitoring is in place, removing a key regulatory hurdle. As a result, lithium-ion has become the default chemistry for latency-sensitive, metro-proximate data halls, accelerating its share gain in new edge builds.

5G Macro and Micro-Cell Rollout Accelerating Telecom-Tower Backup Demand Across Asia

Asia-Pacific operators installed about 1.2 million new 5G sites in 2025, each requiring 2-20 kWh of UPS capacity to bridge frequent grid interruptions. Huawei Digital Power alone shipped more than 340,000 lithium-ion UPS modules into this channel, with India accounting for the fastest growth as Reliance Jio and Bharti Airtel densified coverage in tier-2 and tier-3 cities.[2]Huawei Technologies, “Sustainability Report 2025,” huawei.com India’s IS 16046 Part 3 specification mandates 50 °C thermal tolerance, favoring lithium-iron-phosphate chemistries that outperform nickel-manganese-cobalt variants in hot climates. Vietnam earmarked USD 1.8 billion for rural 5G rollout, stipulating solar-hybrid UPS that reduce diesel runtime and open the door for secondary-life EV batteries. These dynamics give Asia-Pacific a durable runway for lithium-ion adoption, with spill-over demand expected in the Middle East and Africa over the next two years.

Hyperscale Colocation Shift from VRLA to Lithium-Ion to Cut Total Cost of Ownership

A 2025 Lawrence Berkeley National Laboratory study showed that lithium-ion UPS delivered 15-18% lower 10-year total cost of ownership than valve-regulated lead-acid batteries, thanks to longer cycle life and lower cooling overhead. Vertiv disclosed that lithium-ion accounted for 38% of hyperscale UPS orders in 2025, up from 22% in 2024, as operators sought to free up 180 kg per rack for denser GPU clusters. Rack-weight reduction reduces structural retrofit needs and accelerates time-to-revenue for data-center tenants. Colocation providers also favor eight-to-ten-year lithium-ion lifespans, which reduce mid-contract battery swaps and service disruptions. Together, these benefits are pushing hyperscale specifications to list lithium-ion as baseline, hastening chemistry transition in the world’s largest data centers.

Grid-Outage Frequency and Hurricane-Resilience Programs Boosting Residential and Commercial Installations

The United States recorded 14 hurricane-related disaster declarations in 2025, with Florida, Louisiana, and Texas enduring cumulative outages totaling more than 120 hours. State programs now reimburse up to 40% of residential UPS costs, provided systems comply with updated NFPA 855 safety standards.[3]National Fire Protection Association, “NFPA 855 (2024 Edition),” nfpa.org Eaton reported a 67% year-over-year jump in residential UPS sales across the Gulf Coast, with average system capacity climbing from 5 kWh in 2024 to 8 kWh in 2025. Caribbean islands, where grid reliability averages 92-94%, are adopting community-scale lithium-ion UPS to shore up hospitals and water plants during storm season. These incentives and reliability gaps make the sub-10 kVA bracket the fastest-growing slice of the UPS battery market through 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lead price volatility inflating VRLA UPS TCO | −0.8% | Emerging Asia, Africa, South America | Short term (≤ 2 years) |

| Thermal-runaway safety concerns delaying lithium-ion UPS certifications | −0.6% | Global, acute in India and Southeast Asia | Medium term (2-4 years) |

| Limited OEM warranty cover for lithium-ion retrofits in legacy frames | −0.4% | Global, concentrated in brownfield sites | Medium term (2-4 years) |

| Inadequate EU recycling streams for spent lithium-ion UPS modules | −0.3% | Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lead Price Volatility Inflating VRLA UPS Total Cost of Ownership

The London Metal Exchange lead average was USD 2,340 per ton in the first half of 2025, a 22% jump from 2024, squeezing raw-material margins for valve-regulated lead-acid manufacturers. Exide Industries stated that raw-material inflation cut gross margins on industrial UPS batteries from 28% to 23%, prompting price hikes that narrowed the upfront cost gap with lithium-ion alternatives. African and South American buyers, already coping with currency depreciation, face a USD 1,800-2,200 increase in five-year ownership cost for a 50 kWh system. Some regional telecom operators have begun pilot lithium-ion swaps after breakeven analyses showed payback periods of less than 4 years. Sustained commodity volatility could therefore accelerate the transition to chemistry in cost-sensitive markets sooner than expected.

Thermal-Runaway Safety Concerns Delaying Lithium-Ion UPS Certifications

Underwriters Laboratories’ UL 9540A fire-propagation test was adopted by 18 US states and three Canadian provinces during 2024-2025, yet only 40% of lithium-ion UPS models passed on first submission. India’s IS 17558 rule now requires cell-level temperature and voltage monitoring with automatic disconnect above 60 °C, delaying several product launches by four to six months. Healthcare and banking data centers, which favor worst-case safety margins, are deferring purchases until multiple vendors achieve multi-jurisdictional approval. Vendors must add inter-cell thermal barriers or aerosol suppression, which will raise bill-of-materials costs and elongate certification cycles. The backlog is restraining short-term lithium-ion growth in highly regulated verticals until certified product availability scales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: Lithium-Ion Gains Share as Lifecycle Economics Improve

Valve-regulated lead-acid maintained 39.41% UPS battery market share in 2025, underscoring its hold on cost-sensitive installations. However, the lithium-ion slice of the UPS battery market is projected to grow rapidly, with a 7.37% CAGR through 2031, as hyperscale data centers and telecom towers pivot toward high-cycle chemistries. Flooded lead-acid maintains a niche foothold in utility substations, while nickel-cadmium and emerging nickel-zinc variants prevail in temperature extremes or fire-code-restricted settings.

Lithium-ion’s eight-to-ten-year service life, coupled with a 40-50% reduction in capital expenditures when secondary-life electric-vehicle modules are used, is shrinking payback horizons in Africa and Southeast Asia. As recycling streams mature, operators anticipate residual-value credits that further sweeten the total cost of ownership. Together, these shifts position lithium-ion to capture incremental gains in UPS battery market share over the forecast period.

By Power Rating: Above-250 kVA Capacity Accelerates With Utility-Scale Projects

The 10-100 kVA tier captured 34.73% of the UPS battery market in 2025, satisfying mid-sized data center and telecom exchange demand. Looking ahead, above-250 kVA installations should outpace other brackets with a 6.84% CAGR through 2031, propelled by renewable-integration projects that require megawatt-hour buffering. Hospital campuses chasing N+1 redundancy after the 2024 Joint Commission update are also big adopters.

Demand for less than 10 kVA is rising in hurricane zones, where homeowners seek full-day autonomy, while 101-250 kVA systems attract banks and industrial lines upgrading legacy frames. ABB’s orders above 500 kVA underscore utilities’ preference for UPS that dovetail with grid-scale batteries. Collectively, the high-power segment is poised to expand its UPS battery market share, especially in regions with rapid adoption of renewable energy.

By End-User Industry: Residential and Small Offices Emerge as Fastest-Growing Segment

In 2025, data centers dominated the UPS battery market, capturing 28.56% share due to their critical need for uninterrupted power supply to support operations. However, as grid disruptions intensify, residential and small-office installations are poised to experience the sharpest growth, with a projected CAGR of 7.89% through 2031. This growth is driven by increasing power outages and the rising adoption of backup power solutions in smaller setups. Meanwhile, telecommunications infrastructure, bolstered by lithium-ion packs capable of operating at 50 °C, is driving volume growth across the Asia-Pacific region. The demand in this sector is further supported by the rapid expansion of 5G networks and the need for reliable power solutions in high-temperature environments.

Industrial and petrochemical sites still favor chemistries like nickel-cadmium or flywheel hybrids, prioritizing fire safety in explosive atmospheres. Healthcare facilities and BFSI institutions move at a measured pace, waiting for breadth in UL 9540A coverage before pivoting. The diversity of end-user needs keeps the UPS battery market resilient across economic cycles, with each vertical favoring the chemistry or power rating that best resolves its risk profile.

By Sales Channel: OEM Relationships Deepen With Predictive-Maintenance Platforms

In 2025, original-equipment-manufacturer shipments clinched a 53.47% share of the UPS battery market. They are poised to sustain this lead, projecting a 6.44% CAGR growth rate through 2031, thanks to integrated analytics enhancing lifecycle transparency. For instance, platforms like Schneider Electric’s EcoStruxure can forecast a cell's end-of-life 6-9 months ahead, facilitating timely swaps and minimizing downtime. This predictive capability not only ensures operational efficiency but also reduces maintenance costs, making OEM solutions increasingly attractive to large-scale enterprises.

While independent distributors cater to small businesses seeking lower upfront costs, their sway diminishes in hyperscale and telecom sectors, where extended warranties and firmware support take precedence. These sectors demand reliability and advanced technological integration, areas where OEMs excel. As lithium-ion batteries see extended lifespans, aftermarket revenue per asset has seen a dip. However, this decline is partially countered by an uptick in per-unit prices. Additionally, the growing adoption of lithium-ion technology in critical applications further strengthens OEMs' market position. In the end, OEMs are strategically positioned to capitalize on the UPS battery market's value-added services, leveraging their expertise in innovation and customer-centric solutions.

Geography Analysis

Asia-Pacific accounted for 36.82% of UPS battery market share in 2025, supported by China’s data center build-out, which added 8.2 GW of IT capacity during the year. India’s 280,000 new 5G base stations require a lithium-ion UPS capable of operating at 50 °C ambient temperature without active cooling, reinforcing the region’s demand pull. Japan’s push for distributed energy resources lifted residential UPS sales, as Panasonic reported 41% domestic growth for its Eneloop systems. Secondary-life electric-vehicle battery programs in Indonesia and Vietnam cut capital costs by up to 45%, accelerating brownfield tower upgrades. Southeast Asia’s policy preference for solar-hybrid sites ensures that Asia-Pacific remains the largest contributor to UPS battery market size through 2031.

North America ranked second in 2025, driven by edge data center clusters around major metropolitan areas and storm-resilience incentives in hurricane-prone states. The Federal Emergency Management Agency’s Building Resilient Infrastructure and Communities program disbursed USD 2.3 billion that year, with Florida, Louisiana, and Texas receiving 52% of the funds. These grants, coupled with updated NFPA 855 safety rules, boosted residential UPS installations by 67% for Eaton in the Gulf Coast. Canada’s remote-community electrification projects and Mexico’s nearshoring-related factory builds add incremental demand for systems with ratings above 250 kVA that stabilize production lines. Europe follows closely, combining high lithium-ion adoption in data-center hubs with regulatory pressure from the EU Battery Regulation, which mandates a 70% collection rate for spent lithium-ion units by 2028.

Africa is projected to record a 7.11% CAGR between 2026-2031, the fastest regional pace, thanks to off-grid telecom rollouts and micro-grid pilots that rely on repurposed EV modules supplied under partnerships such as Renault’s agreement with MTN Group. South Africa’s load-shedding, totaling 6,947 outage hours in 2025, pushed commercial UPS purchases toward maintenance-free lithium-ion chemistries. The Middle East benefits from hyperscale data centers in the United Arab Emirates and Saudi Arabia that specify above-250 kVA lithium-ion solutions with N+1 redundancy. South America shows moderate but steady uptake, led by Brazilian data-center expansions and Argentine telecom upgrades; currency volatility constrains volumes yet leaves room for OEM-financed deployments. Together, these trends create a geographically diversified trajectory for UPS battery market size that buffers against slowdowns in a single region.

Competitive Landscape

The top five vendors, Schneider Electric, Eaton, Vertiv, ABB, and Huawei Digital Power, accounted for an estimated 42% of global revenue in 2025, suggesting a moderately concentrated UPS battery market. These incumbents embed proprietary battery-management firmware into their UPS frames, locking in multi-year service contracts and ensuring captive replacement cycles; Schneider Electric’s Galaxy VS architecture, for example, only accepts its own lithium-ion cabinets. To widen moats, leaders are localizing cell production, as illustrated by Schneider’s USD 180 million Bangalore expansion, slated to reach 500 MWh of annual capacity by 2027.

Lithium-ion specialists such as LG Energy Solution and Contemporary Amperex Technology are bypassing traditional UPS integrators by shipping cells directly to hyperscale operators that assemble battery racks in-house, a shift that compresses OEM margins. Disruptors are also targeting safety-sensitive niches: ZincFive’s nickel-zinc modules satisfy high-rise fire codes without halon or water suppression, while Connected Energy aggregates second-life EV packs at 40-50% lower cost than new lithium-ion units. Patent filings confirm divergent R&D paths: lead-acid incumbents focusing on carbon-enhanced plates to extend cycle life, and lithium-ion players emphasizing AI-driven thermal runaway detection.

Regional manufacturers maintain footholds in valve-regulated lead-acid segments where price outweighs lifecycle economics; firms such as Amara Raja in India and Leoch in China leverage domestic supply chains to defend share against import competition. ABB’s USD 95 million contract to supply 18 MWh of UPS systems with above-500 kVA capacity to a European utility underscores the growing high-power opportunity. Huawei’s five-year pact with MTN Group to deploy 25,000 solar-hybrid lithium-ion UPS across Africa demonstrates how telecom channel partnerships can fast-track volume for vertically integrated vendors. As certification regimes like UL 9540A tighten, vendors that secure multi-jurisdictional approvals first are poised to capture share in healthcare and banking, cementing the competitive hierarchy over the next five years.

UPS Battery Industry Leaders

CSB Energy Technology Co. Ltd.

East Penn Manufacturing Co.

Eaton Corporation plc

Exide Industries Ltd.

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Schneider Electric announced a USD 180 million expansion of its lithium-ion UPS module plant in Bangalore, India, targeting 500 MWh annual capacity by Q4 2027.

- December 2025: Eaton completed the acquisition of a 60% stake in South Africa-based PowerSync, gaining secondary-life battery integration expertise.

- November 2025: Vertiv launched the UL 9540A-certified Liebert EXM LFP UPS, with first shipments totaling 22 MWh to 14 US hospital systems.

- October 2025: Huawei Digital Power signed a five-year pact with MTN Group to roll out 25,000 solar-hybrid lithium-ion UPS units across African tower sites.

Global UPS Battery Market Report Scope

The UPS Battery Market Report is Segmented by Battery Chemistry (Valve-Regulated Lead-Acid, Flooded Lead-Acid, Lithium-Ion, Nickel-Cadmium, Nickel-Zinc, Other Battery Chemistries), Power Rating (Less than 10 kVA, 10-100 kVA, 101-250 kVA, Above 250 kVA), End-User Industry (Data Centers, Telecommunications, Industrial Manufacturing, Oil, Gas and Petrochemicals, Commercial Buildings, Healthcare Facilities, Residential and Small Office, Banking Financial Services and Insurance, Utilities and Power Infrastructure), Sales Channel (Original Equipment Manufacturer, and After-Market / Replacement), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Valve-Regulated Lead-Acid |

| Flooded Lead-Acid |

| Lithium-Ion |

| Nickel-Cadmium |

| Nickel-Zinc |

| Other Battery Chemistries |

| Less than 10 kVA |

| 10 – 100 kVA |

| 101 – 250 kVA |

| Above 250 kVA |

| Data Centers |

| Telecommunications |

| Industrial Manufacturing |

| Oil, Gas and Petrochemicals |

| Commercial Buildings |

| Healthcare Facilities |

| Residential and Small Office |

| Banking, Financial Services, and Insurance |

| Utilities and Power Infrastructure |

| Original Equipment Manufacturer |

| After-Market / Replacement |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Battery Chemistry | Valve-Regulated Lead-Acid | ||

| Flooded Lead-Acid | |||

| Lithium-Ion | |||

| Nickel-Cadmium | |||

| Nickel-Zinc | |||

| Other Battery Chemistries | |||

| By Power Rating | Less than 10 kVA | ||

| 10 – 100 kVA | |||

| 101 – 250 kVA | |||

| Above 250 kVA | |||

| By End-User Industry | Data Centers | ||

| Telecommunications | |||

| Industrial Manufacturing | |||

| Oil, Gas and Petrochemicals | |||

| Commercial Buildings | |||

| Healthcare Facilities | |||

| Residential and Small Office | |||

| Banking, Financial Services, and Insurance | |||

| Utilities and Power Infrastructure | |||

| By Sales Channel | Original Equipment Manufacturer | ||

| After-Market / Replacement | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the UPS battery market by 2031?

The UPS battery market is forecast to reach USD 8.43 billion by 2031, expanding at a 6.03% CAGR from 2026-2031.

Which battery chemistry is growing fastest in UPS applications?

Lithium-ion is the fastest-rising chemistry, expected to post a 7.37% CAGR through 2031 as hyperscale operators emphasize longer cycle life and lower cooling loads.

Which power-rating segment is set to outpace others?

Above-250 kVA systems should record the highest growth, driven by renewable-integration projects and large hospital complexes seeking N+1 redundancy.

Why is Africa the fastest-growing regional market?

Secondary-life electric-vehicle battery repurposing deals and off-grid telecom expansion are lowering capital costs, producing a 7.11% regional CAGR through 2031.

How are OEMs maintaining an edge over independent distributors?

OEMs leverage predictive-maintenance platforms that forecast battery end-of-life, ensuring tighter service contracts and higher customer retention despite longer lithium-ion lifespans.

What is delaying lithium-ion UPS adoption in healthcare and banking?

Thermal-runaway safety concerns have slowed UL 9540A certifications, prompting risk-averse sectors to defer purchases until more models secure full approval.

Page last updated on: