Electric Double-layer Capacitor (EDLC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

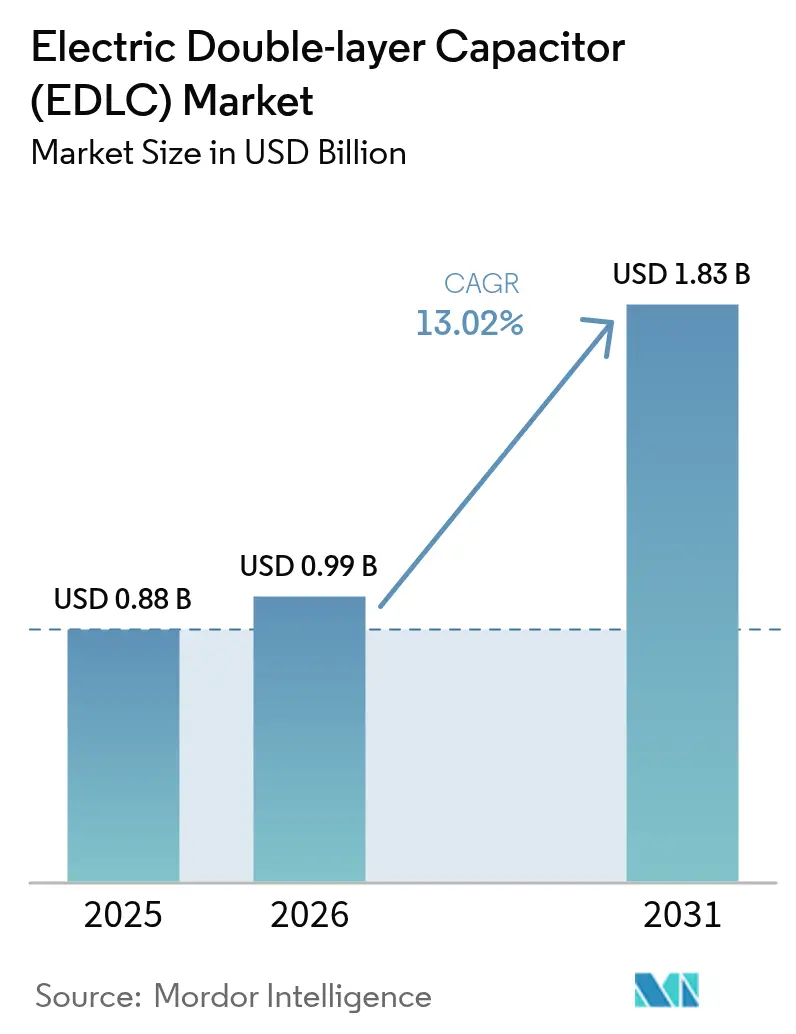

| Market Size (2026) | USD 0.99 Billion |

| Market Size (2031) | USD 1.83 Billion |

| Growth Rate (2026 - 2031) | 13.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Electric Double-layer Capacitor (EDLC) Market Analysis by Mordor Intelligence

The Electric Double-layer Capacitor market size was valued at USD 0.88 billion in 2025 and estimated to grow from USD 994.58 million in 2026 to reach USD 1.83 billion by 2031, at a CAGR of 13.02% during the forecast period (2026-2031). Demand acceleration stems from the convergence of transportation electrification, grid modernization goals, and edge-computing power spikes that conventional batteries cannot meet. Manufacturing scale-up across Asia-Pacific, advances in graphene-enhanced electrodes, and regulatory pressure for long-life, easily recyclable storage are reinforcing momentum. Grid operators value the technology’s sub-second response times, while automotive original equipment manufacturers integrate cylindrical EDLC modules to capture regenerative-braking energy and satisfy 48 V architecture requirements. Consumer electronics designers adopt coin and chip cells to support burst loads in wearables without compromising form factor. Simultaneously, the volatility of activated-carbon costs and fragmented global safety standards temper the pace of design wins, prompting suppliers to invest in supply-chain security and certification support.

Key Report Takeaways

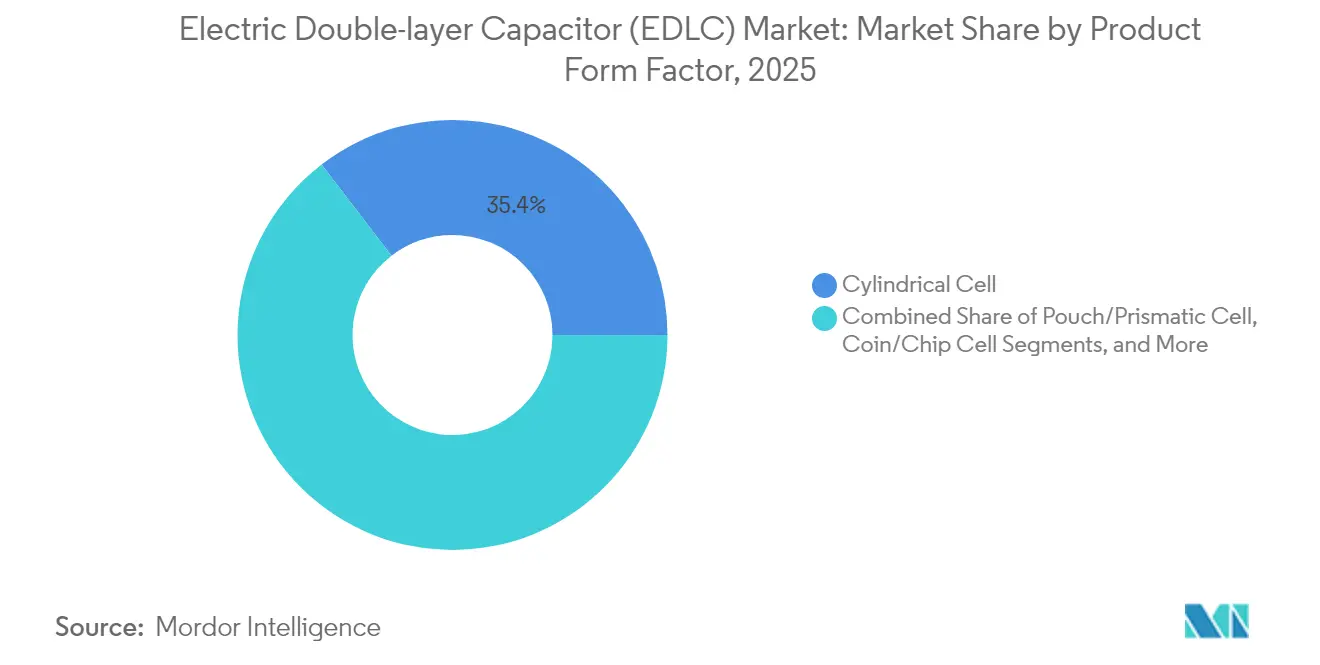

- By product form factor, cylindrical cells led the Electric Double-layer Capacitor market with a 35.42% revenue share in 2025; coin and chip cells are projected to expand at a 14.88% CAGR through 2031.

- By module voltage, the 10-25 V segment accounted for 40.12% of the Electric Double-layer Capacitor market share in 2025, while modules with voltages above 100 V are forecasted to grow at a 14.63% CAGR to 2031.

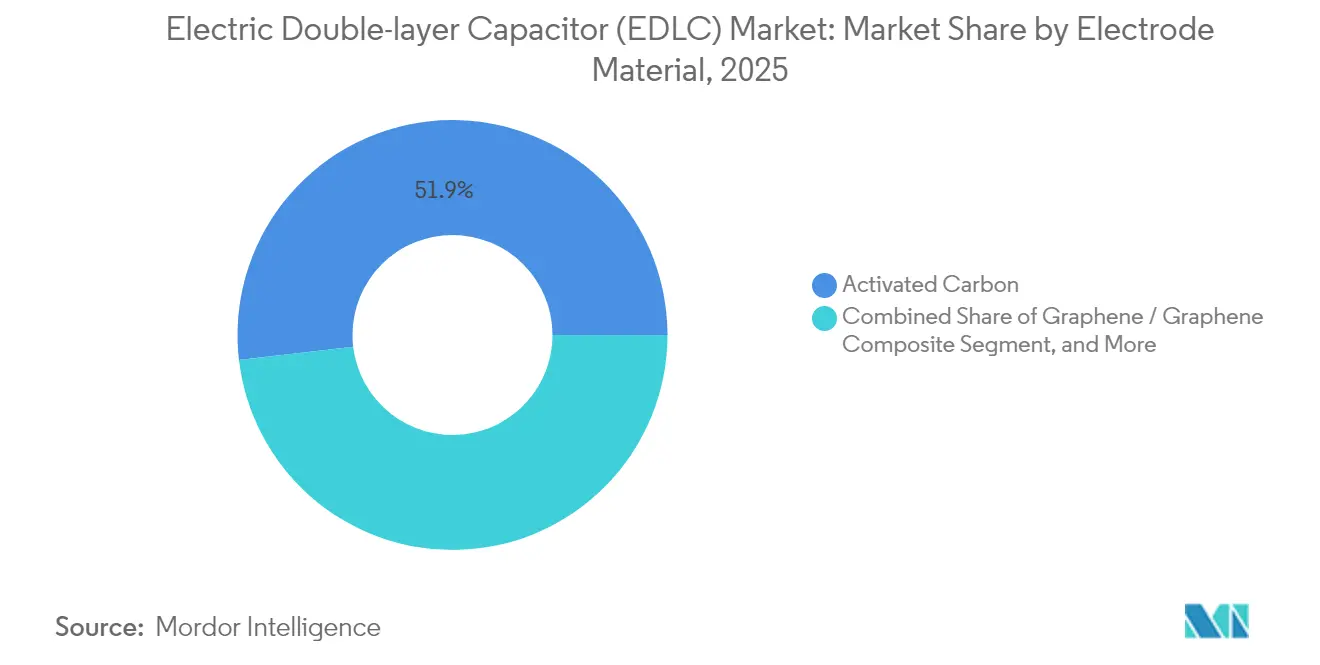

- By electrode material, activated carbon commanded a 51.86% share of the Electric Double-layer Capacitor market size in 2025, and graphene composites are projected to advance at a 14.31% CAGR through 2031.

- By end-user industry, consumer electronics captured 31.25% of the revenue share of the Electric Double-layer Capacitor market in 2025; the automotive and transportation segment is the fastest-growing, with a 13.96% CAGR to 2031.

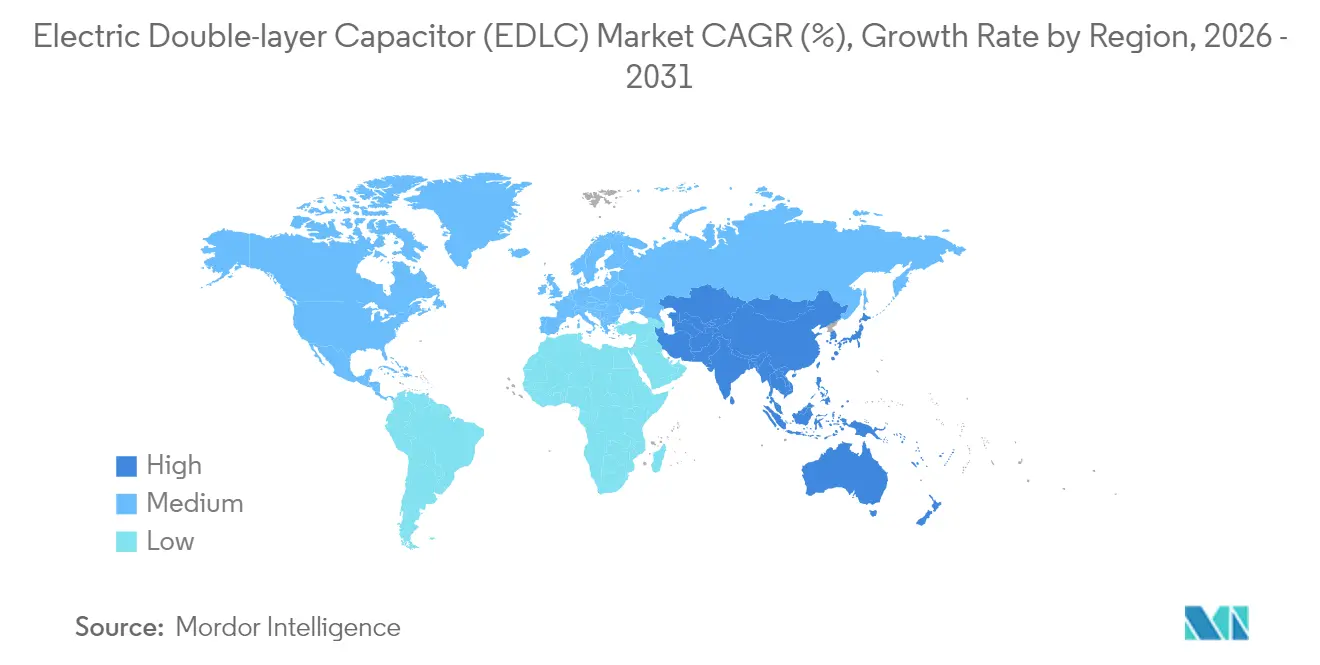

- Asia-Pacific held 42.10% of the revenue share of the Electric Double-layer Capacitor market in 2025 and is progressing at a 13.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electric Double-layer Capacitor (EDLC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging adoption of regenerative braking in EV/HEV | +3.2% | Global, led by APAC and Europe | Medium term (2-4 years) |

| Growing demand for grid-scale frequency regulation and renewable smoothing | +2.8% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Miniaturization trend in consumer electronics requiring burst-power buffers | +2.1% | APAC core, global spill-over | Short term (≤ 2 years) |

| Rapid roll-out of 5 G macro and micro-cells needing peak-power support | +1.9% | Global urban centers | Medium term (2-4 years) |

| Emergence of 48 V edge-data-center backup architectures | +1.6% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Defense transition to high-pulse directed-energy platforms | +1.3% | North America, EU, select APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging adoption of regenerative braking in EV/HEV

Automakers integrate Electric Double-layer Capacitor market solutions into 48V mild-hybrid platforms to harvest braking energy that lithium-ion cells cannot absorb quickly. EDLC modules capture millisecond-scale charge pulses, raising urban fuel efficiency by 15-20% and allowing compliance with European CO₂ targets without requiring a shift to full hybrids.[1]JYH HSU Electronics, “What Is a Supercapacitor?,” jeccapacitor.com Fleet operators of buses and light-rail vehicles prioritize technology to reduce brake-wear maintenance and unlock weight reductions that improve payload economics.

Growing demand for grid-scale frequency regulation and renewable smoothing

Utilities increase their share of solar and wind energy, lowering inertia and intensifying frequency volatility. Skeleton Technologies’ SkelGrid 2.0 cabinets supply up to 3 MW within one second, delivering synthetic inertia with 99% round-trip efficiency.[2]Skeleton Technologies, “Maximizing Grid Stability: How Supercapacitors Are Shaping Frequency Response,” skeletontech.com Ancillary-service auctions in the United States and Germany reward sub-second response, enabling paybacks under three years for EDLC-based fast-frequency-response assets.

Miniaturization trend in consumer electronics requiring burst-power buffers

Wearables and hearables integrate coin-type EDLCs to deliver peak currents for sensor bursts, Bluetooth transmissions, and haptic feedback without oversizing lithium-ion micro-cells. Laboratory microsupercapacitors fabricated on 200 mm wafers achieve cell densities of 54.9 units/cm², allowing direct embedding beside semiconductors.[3]Institute of Electrical and Electronics Engineers, “Toward Standardized High-Power On-Chip Devices,” ieee.org Device makers enhance the user experience by delivering brighter displays and faster gesture recognition while maintaining multi-day runtime.

Rapid roll-out of 5 G macro and micro-cells needing peak-power support

The average 5G base station consumption doubles that of 4G, with traffic spikes driving transient peaks of 300-400%. Shanghai Green Tech’s 48 V graphene supercapacitor racks shield radios from voltage sags, prevent reboot cycles, and support seamless switchover to diesel gensets during outages. Carriers prefer EDLC systems for outdoor cabinets that experience temperature swings ranging from −40 °C to +55 °C, whereas lithium-ion batteries require active thermal control.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher USD-per-Wh cost versus Li-ion batteries | −2.4% | Global, cost-sensitive markets | Medium term (2-4 years) |

| Design-in complexity owing to standards fragmentation | −1.8% | Global, multi-region deployments | Long term (≥ 4 years) |

| Volatile activated-carbon feedstock pricing | −1.3% | Global, APAC supply chain | Short term (≤ 2 years) |

| Prospective EU battery-take-back extension to EDLC modules | −0.9% | Europe, global spill-over | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher USD-per-Wh cost versus Li-ion batteries

EDLC packs remain priced at USD 800-1,200/kWh, compared with lithium-ion’s sub-USD 150/kWh benchmark, which restricts adoption where energy density dominates the economic calculus.[4]Raphael Areola et al., “Integrated Energy Storage Systems for Enhanced Grid Efficiency,” Energies, mdpi.com The total-cost-of-ownership argument only prevails in high-cycle applications, compelling suppliers to emphasize lifecycle maintenance savings and recycling credits under forthcoming EU regulations.

Design-in complexity owing to standards fragmentation

Absence of a harmonized global test protocol obliges vendors to navigate IEC, UL, IEEE, and regional automotive standards separately. Certification campaigns can stretch past 18 months, slowing multi-region product launches and disadvantaging resource-constrained startups. The draft IEEE P2976-2025 standard for supercapacitor performance aims to streamline compliance; however, its rollout lags behind market needs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form Factor: Cylindrical Cells Anchor High-Power Applications

Cylindrical units held 35.42% of 2025 revenue, underpinned by proven reliability in automotive starter modules and industrial UPS banks. The Electric Double-layer Capacitor market size for cylindrical designs is projected to reach USD 652 million by 2031, expanding in line with the adoption of 48 V mild-hybrid vehicles. Standardized mechanical dimensions simplify integration with existing battery trays, curbing engineering overhead. Meanwhile, coin and chip formats scale at a 14.88% CAGR as wearables, smart patches, and tire-pressure sensors require sub-millimeter profiles. Manufacturers deploy laser-patterned current collectors and solid-state electrolytes to elevate energy per cubic centimeter. Over the forecast horizon, form-factor boundaries blur as design-for-assembly shifts to co-packaged battery-capacitor hybrids that embed EDLC layers around prismatic lithium-ion cores.

Cylindrical suppliers focus on cooling innovations, such as aluminum extrusion housings, which reduce thermal resistance by 30%. Coin-cell innovators scale roll-to-roll electrode printing to control costs. Pouch and prismatic options play a bridging role where designers manage irregular cavities, notably in aerospace avionics and automated-guided vehicles navigating width constraints. Module and system integrators emphasize plug-and-play busbar layouts and fused cell-level protection to meet IEC 62040 class-C UPS safety levels.

By Module Voltage: Mid-Range Segments Balance Safety and Performance

Modules rated 10-25 V captured 40.12% 2025 share thanks to compatibility with 12 V automotive subsystems and 24 V industrial controls. Designers achieve leadership in the Electric Double-layer Capacitor market by leveraging existing wiring harness standards and avoiding high-voltage clearance requirements. Growth persists as commercial delivery vans migrate from lead-acid starting batteries to EDLC cranking boosters that survive million-cycle duty. High-voltage stacks above 100 V are expected to accelerate at a 14.63% CAGR to meet renewable grid buffers and support electric-bus traction. Skeleton’s 162 V modules highlight safe hot-swapping, galvanic isolation, and thermal-runaway-proof separators, addressing utility procurement specs.

Low-voltage (<10 V) micro-modules underpin smartcards, drug-delivery pumps, and implantables where safety dictates touch-safe limits. Mid-voltage (25-50 V) units populate data-center power distribution units, bridging 48 V busbars and server motherboards. The product roadmap focuses on integrating active balancing circuits and State-of-Health analytics via CANopen to support predictive maintenance.

By Electrode Material: Activated Carbon Retains Breadth of Adoption

Activated-carbon electrodes generated 51.86% of 2025 revenue, driven by mature coconut-shell-derived supply chains and well-characterized aging profiles. The Electric Double-layer Capacitor market size tied to activated carbon is set to surpass USD 948 million by 2031 as cost-sensitive segments predominate. Graphene and graphene-composite electrodes are projected to grow at a 14.31% CAGR, enticing automotive and aerospace engineers with doubled gravimetric energy and halved ESR. Yet, the costs of graphene feedstock purification delay mass rollouts. Carbon-nanotube (CNT) blends are finding niche adoption in defense pulse-energy weapons, where ultra-low inductance is critical.

Conductive-polymer coatings enhance the flexibility of rollable displays, while metal-oxide-enhanced electrodes introduce pseudocapacitive charge storage, increasing energy by 40% at the expense of reduced cycle life. Supply-risk mitigation becomes vital as APAC accounts for over 70% of high-surface-area carbon feedstock processing capacity. Leading OEMs negotiate multi-year offtake agreements with Indonesian coconut-charcoal producers and South-Korean graphene exfoliation start-ups to avert price spikes.

By End-user Industry: Consumer Electronics Dominates, Automotive Accelerates

Consumer electronics retained 31.25% 2025 revenue, leveraging coins and wafers in TWS earphones and fitness trackers. The upgrade cycle toward brighter microLED displays and gesture sensors maintains volume dominance despite declining average selling prices. The automotive sector emerges as the fastest-growing end-user, registering a 13.96% CAGR, fueled by 48V stop-start technology, e-turbo boosting, and energy-recovery rails on electric buses. Industrial automation continues to experience steady double-digit growth in servo drives and machine-tool voltage-sag compensators. Energy and utilities are broadening the adoption of fast frequency response and black-start support as regulator-defined response windows shrink to 500 milliseconds.

Fleet operators quantify paybacks from EDLC-assisted regenerative braking, noting brake-pad replacement intervals stretching from 50,000 km to 80,000 km and diesel consumption dips of 6-8% on urban bus routes. In data centers, rack-mount modules replace valve-regulated lead-acid batteries, freeing up floor space and eliminating the need for quarterly replacements. Medical equipment OEMs are exploring EDLC buffer packs in portable defibrillators to ensure shock delivery remains consistent even as primary lithium-ion cells age.

Geography Analysis

Asia-Pacific maintained 42.10% of global revenue in 2025, underpinned by China’s grid-scale frequency-regulation pilots, Japan’s consumer-electronics miniaturization, and South Korea’s battery-ecosystem clustering. Regional governments allocate capital-subsidy pools for domestic energy-storage value chains, reinforcing manufacturing cost leadership. Suppliers benefit from proximity to activated-carbon processing hubs in Indonesia and Vietnam, which streamlines logistics and reduces lead times. Local automakers anchor procurement volumes, fostering economies of scale that sustain price competitiveness for export markets.

North America is capturing a rising share as transmission operators deploy EDLC arrays to stabilize networks that are dealing with record solar installations. Data-center operators in the United States prefer 48 V EDLC racks over flywheels due to their zero maintenance requirements and lower standby losses. Defense procurement underpins R&D funding for CNT-loaded pulse-power modules used in directed-energy prototypes. Canada champions mining reforms to support domestic graphite purification, positioning itself as an alternative raw material source amid supply chain diversification strategies.

Europe advances adoption driven by stringent lifecycle compliance under Battery Regulation 2023/1542, which extends producer responsibility to Electric Double-layer Capacitor market products. Automakers incorporate EDLC modules to secure eco-design credits, while utilities pilot hybrid battery-supercapacitor storage blocks that satisfy both energy and power-quality mandates. Manufacturers invest in automated end-of-life disassembly lines to meet mandated 90% material-recovery targets by 2030. The Middle East and Africa present nascent potential, where high ambient temperatures make EDLC systems attractive for telecom tower backup, eliminating the need for HVAC-cooled containerized lithium-ion banks.

Regulatory Landscape

Electric double-layer capacitors (EDLCs) fall under multiple component, transport, and substance-compliance regimes, with IEC standards acting as a key technical reference point. IEC 62391-1:2022 serves as the generic specification for fixed EDLCs in electric and electronic equipment, while IEC 62391-2:2025 updates the power-application requirements, replacing earlier editions and tightening alignment for high-power modules used in automotive, grid, and UPS designs.

For logistics, the IATA Dangerous Goods Regulations (65th Edition) classify higher-energy EDLCs as regulated articles under UN3499 when the device energy exceeds 0.3 Wh. Units at or below 0.3 Wh are treated as exempt from special dangerous goods provisions, which affects packaging, labeling, and air-freight routing for global shipments. In Europe, compliance planning is shaped by the EU Battery Regulation (EU) 2023/1542 (extended producer responsibility and lifecycle disclosures) and RoHS Directive 2011/65/EU exemption management, including July 2026 consultation activity and July 2026 application timing of delegated updates affecting Annex III exemptions, which raises the priority of lead-free material substitutions in capacitor supply chains where applicable.

Value Chain Analysis

The EDLC value chain begins with upstream materials and chemicals, including activated carbon and emerging graphene or composite carbons, electrolyte solvents and salts, separators, current collectors, binders, and packaging metals. Production then moves through electrode mixing and coating (often via roll-to-roll processing), drying or calendering, winding or stacking, electrolyte filling, sealing, formation or aging, and end-of-line testing. Downstream, cells are assembled into modules and packs with balancing, protection, and mechanical housings, then integrated by OEMs and system providers into automotive 48 V architectures, grid and fast-frequency-response cabinets, telecom and 5G backup, industrial UPS, and compact consumer and IoT electronics.

Two constraint areas stand out: high-purity activated carbon availability and specialized electrolyte precursors, which can cap output even as assembly capacity expands. Regional standardization divergence also adds friction since qualification and documentation often need rework for multiple compliance pathways, extending design-in cycles for global product launches. The go-to-market structure remains two-track, with large OEM programs supplied directly under long-term agreements, while industrial and electronics demand is served through distributors and module integrators that provide reference designs, compliance support, and application engineering.

Competitive Landscape

Competition remains moderate, with the top five players accounting for around one-third of revenue. Skeleton Technologies leverages curved-graphene platforms and turnkey grid modules to secure utility contracts across Germany and Texas. Panasonic focuses on automotive joint ventures, codeveloping 48 V packs that integrate LIN-bus balancing and pressure-vent mechanisms for European OEMs. TDK accelerates materials integration after acquiring a South Korean graphene-electrode fab in late 2024, aiming to lift energy density to 18 Wh/kg by 2026. Shanghai Green Tech scales graphene-coated aluminum foil lines to supply 5 G-site powerbanks for Chinese mobile operators. CAP-XX captures IoT niches with sub-millimeter prismatic parts validated to IEC 62368-1.

Strategic moves center on vertical control of electrode materials, with long-term offtake deals for coconut-shell-based activated carbon and pilot plants for biomass-derived carbons. Partnerships with inverter and charger suppliers enable bundled solutions that raise switching-cost barriers. Patent filings cluster around low-resistance current collectors, solid-gel electrolytes, and self-diagnostic algorithms that track equivalent series resistance drift. Entrants targeting avionics and medical segments differentiate through biocompatible encapsulants and hermetic titanium housing.

Second-tier participants, including Nippon Chemi-Con and Cornell Dubilier, exploit brand reputations in aluminum electrolytic capacitors to cross-sell EDLC banks into legacy customer bases. Hybrid energy-storage developers combine lithium-iron-phosphate strings with supercapacitor front-ends, offering two-stage power delivery that optimizes both energy and peak-power metrics. Market-share shifts will hinge on suppliers’ aptitude for aligning with evolving international standards and demonstrating recyclability performance under EU audits.

Electric Double-layer Capacitor (EDLC) Industry Leaders

-

Maxwell Technologies (Tesla Inc.)

-

Skeleton Technologies OÜ

-

Eaton Corporation

-

Kyocera Corporation

-

Panasonic Holding Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Manufacturing localization and process innovation are a clear whitespace for EDLC and module suppliers as buyers look for resilient supply and a smaller lifecycle footprint. Capacity moves in 2025-2026 already show where procurement attention is shifting: Skeleton Technologies inaugurated a 220 million Euro SuperFactory in Markranstadt, Germany (12 million curved-graphene cells annually), while LiCAP Technologies secured a 40,500-square-foot facility in Sacramento to triple production capacity for its Activated Dry Electrode technology and ultracapacitor modules. These investments support faster qualification cycles for automotive, grid, and data-center programs, which increasingly require traceable supply chains and repeatable performance screening.

Co-located power-quality solutions around high-load infrastructure offer another active opportunity area for EDLC systems, especially where sub-second response is monetized or where power peaks stress upstream equipment. In July 2026, Lumcloon Energy and KEPCO announced Project Daejeon, a demonstration-scale supercapacitor energy storage system co-located with a liquid-cooled data center at Rhode Green Energy Park in County Offaly, Ireland, linking EDLC deployments to data-center-driven grid constraints. On the technology side, research momentum around aqueous and confined-water electrolytes and biomass-derived carbons, reported in 2026 studies demonstrating long cycle life and alternative electrode feedstocks, points to a roadmap that aligns performance with tightening substance and transport compliance needs, reinforcing development work on safer chemistries and recyclable bill-of-materials in modules and packs.

Recent Industry Developments

- June 2026: Skeleton Technologies reported a UL-certified peak current record of 3,500 amperes for its supercapacitors. The certification strengthens adoption in high-pulse applications that demand independently verified performance, such as grid support, industrial power buffering, and transportation energy recovery.

- November 2025: Skeleton Technologies opened its SuperFactory in Markranstadt near Leipzig, Germany, with an annual capacity stated at 12 million supercapacitor cells. The added manufacturing scale supports larger-volume module deliveries for grid stabilization and high-power infrastructure programs while improving supply assurance for European customers.

- July 2024: Skeleton Technologies supercapacitors were integrated into the NTT IndyCar Series hybrid Energy Recovery System using a 20-supercapacitor energy storage configuration. The deployment expanded the visibility of EDLCs in high-duty-cycle regenerative braking environments and validated hybridization use cases where batteries benefit from pulse-power buffering.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenue earned from electric double layer capacitors (EDLCs) sold as components or modules for energy storage and fast charge-discharge use cases across major end industries, tracked in USD.

Scope exclusions: Pure battery packs, lithium-ion capacitors, and other non-EDLC technologies are excluded unless they are explicitly sold and reported as EDLC products.

Segmentation Overview

-

By Product Form Factor

- Cylindrical Cell

- Pouch / Prismatic Cell

- Coin / Chip Cell

- Module (Greater than equal to 10 F)

- Pack / System

-

By Module Voltage

- Less than 10 V

- 10 - 25 V

- 25 - 50 V

- 50 - 100 V

- Greater than 100 V

-

By Electrode Material

- Activated Carbon

- Graphene / Graphene Composite

- Carbon Nanotube (CNT)

- Conductive Polymer

- Metal-Oxide-Enhanced

-

By End-user Industry

- Consumer Electronics

- Energy and Utilities

- Industrial

-

Automotive / Transportation

- Bus and Truck

- Rail and Tram

- 48 V Mild Hybrid Car

- Micro-hybrids and Other Cars

- Heavy Vehicles

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

-

Africa

- South Africa

- Rest of Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a factual backbone for demand and supply. We refer to public sources such as national energy statistics (for grid and storage additions), transportation agencies (for bus, rail, and fleet electrification indicators), customs and trade statistics for capacitor-related imports and exports, and standards bodies that publish safety and testing guidance for capacitors and electronic components.

To keep assumptions realistic, we also review company annual reports, earnings decks, and product brochures to see where EDLCs are actually deployed and how the value is described in financial disclosures. Patent databases are used selectively to sanity check material direction, for example activated carbon and emerging carbon materials, and the pace of new product filings. In addition, we use paid subscriptions for company financials and news intelligence, and where needed, shipment-level trade visibility for cross-checking flows. The sources listed here are illustrative, and many other public documents were used for data collection, clarification, and validation.

Primary Interviews and Surveys

Primary work is used to pressure test the desk view and fill gaps that public data does not explain well, especially pricing logic, adoption timing, and how EDLCs are specified in real projects. We speak with a mix of component suppliers, module assemblers, distributors, OEM engineering or sourcing teams, and system integrators across APAC, EMEA, and the Americas, so regional demand signals are not over-weighted from one geography.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 17% | APAC: 39% |

| Mid tier: 43% | Functional/Unit leaders: 24% | EMEA: 36% |

| Smaller Players: 22% | Managers: 59% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where electronics production indicators, vehicle electrification activity, and grid and industrial capex signals are translated into an EDLC demand pool, and then value is derived using realistic adoption ratios and price points. To keep the totals grounded, the outputs are corroborated with selective bottom-up approximations, such as sampling typical EDLC content in target applications, channel checks on module shipments, and vendor-reported revenue splits where disclosures are clear.

Inputs used in the model include indicators like EV and micro-hybrid production direction, rail and bus electrification activity, renewable integration and substation upgrade pace, and the mix shift between coin or chip formats and larger cylindrical modules that influences ASPs. Activated carbon input cost trends and yield impacts are treated as an important sensitivity because they can move selling prices and margins. Forecasts are produced using scenario analysis supported by expert views, where adoption speed and pricing progression are varied within plausible ranges and then reconciled back to the application demand indicators. Where bottom-up details are missing for smaller applications, we apply conservative penetration bands that are later rechecked during interviews.

Data Validation & Update Cycle

Validation happens in several steps so unusual numbers are caught early. We compare the modeled demand with independent signals such as electronics output trends, electrified fleet activity, and trade movement patterns for relevant component categories, and then we investigate variances that do not fit the story.

Before sign-off, the work goes through internal analyst reviews, and any large assumption changes trigger follow-up outreach to re-confirm the logic. Reports are refreshed annually, and interim adjustments are made when material events occur, such as sudden pricing shifts in key carbon inputs or meaningful demand changes in automotive and grid projects. Right before delivery, a final pass is completed so the view reflects the latest available data and interview learnings.

Mordor Intelligence's Electric Double Layer Capacitor Market Size Measured Against Other Published Estimates

Published market sizes for EDLCs can differ quite a bit, even when the topic name looks identical, because the counting boundary is not always the same. The biggest drivers are usually technology inclusion, the way modules versus cells are treated, the year chosen as the base, and how pricing is carried forward into the forecast.

Shipment signals from capacitor trade flows and application checkpoints like electrified transport build activity are two pieces of evidence that are used to keep Mordor Intelligence aligned to a practical EDLC demand pool in USD terms. When those signals are not used, it is easier for adjacent categories to be added in, for pricing to be pushed up too quickly, or for the timeline to drift from actual adoption cycles in automotive, industrial, and grid uses.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.88 B (2025) | |

| Industry Research Publisher A | USD 1.02 B (2025) | Uses a longer forecast window and can apply a higher early adoption curve, which tends to lift near-term value when pricing progression is not tightly tied back to module and cell mix shifts. |

| Global Research Publisher B | USD 2.66 B (2025) | Likely reflects a broader definition that can pull in non-EDLC supercapacitor types or adjacent energy storage products, and this expansion can inflate the counted revenue base for the same year. |

Taken together, the spread mainly comes from definition boundaries and how fast ASPs and adoption are assumed to move. By anchoring the model to observable demand indicators and then confirming assumptions with interviews, we end up with a market value that is traceable to clear steps and easier to reproduce across updates.

Key Questions Answered in the Report

How large will global Electric Double-layer Capacitor sales be in 2031?

Sales are projected to reach USD 1.83 billion by 2031, reflecting a 13.02% CAGR from 2026 levels.

Which end-user group is expanding fastest?

Automotive and transportation applications are growing at a 13.96% CAGR through 2031 as 48 V mild-hybrid and regenerative-braking designs proliferate.

Why do utilities favor supercapacitors for frequency response?

EDLC systems deliver full power within one second and can cycle more than 1 million times, making them ideal for sub-second frequency regulation markets that reward ultra-fast response.

What challenges limit wider EDLC deployment?

Higher USD-per-Wh cost versus lithium-ion and fragmented certification standards add upfront expense and design complexity.

Which geographic region leads manufacturing?

Asia-Pacific accounts for 42.10% of 2025 revenue due to concentrated supply chains, large domestic demand, and supportive industrial policies.

How are graphene electrodes influencing performance?

Graphene composites raise energy density and lower internal resistance, enabling modules that store more energy without sacrificing million-cycle durability.

Page last updated on: