Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

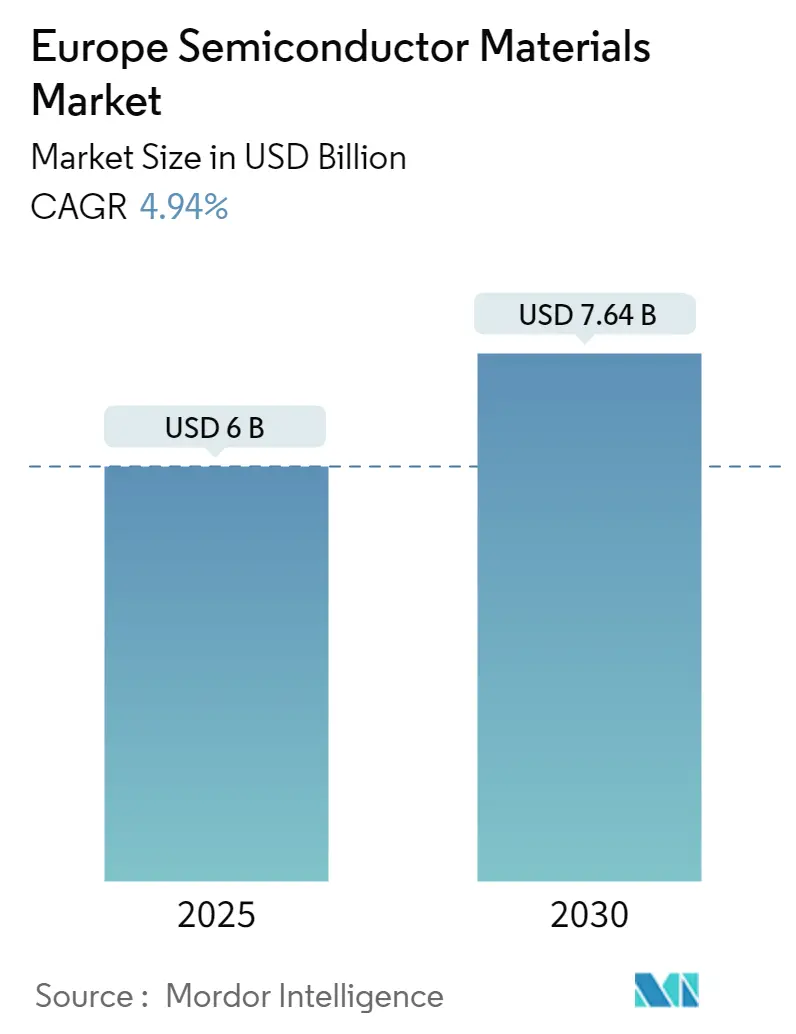

| Market Size (2025) | USD 6.00 Billion |

| Market Size (2030) | USD 7.64 Billion |

| Growth Rate (2025 - 2030) | 4.94% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Semiconductor Materials Market Analysis by Mordor Intelligence

The Europe Semiconductor Materials Market size is estimated at USD 6.00 billion in 2025, and is expected to reach USD 7.64 billion by 2030, at a CAGR of 4.94% during the forecast period (2025-2030).

The European semiconductor materials landscape is undergoing a significant transformation driven by strategic initiatives to strengthen regional semiconductor sovereignty. Through the EU Chips Act announced in February 2022, the European Union aims to double its global market share in semiconductors from 10% to approximately 20% by 2030, backed by substantial financial support for advanced chip production and electronic materials research. This strategic push has catalyzed unprecedented investments in manufacturing capacity, with the Europe and Middle Eastern region recording USD 9.3 billion in fab equipment spending in 2022, representing a remarkable 176% growth over the previous year.

The industry is witnessing a substantial shift in manufacturing capabilities and infrastructure development across the region. Major semiconductor companies are establishing new production facilities, exemplified by STMicroelectronics' announcement in October 2022 to construct a EUR 730 million silicon carbide wafer plant in Italy, marking the first approved project under the EU's initiative to localize chip production. This trend is further reinforced by Wolfspeed's February 2023 announcement to build a highly automated 200mm wafer fabrication facility in Saarland, Germany, demonstrating the industry's commitment to expanding European manufacturing capabilities.

The market is experiencing a rapid evolution in technological applications, particularly in the telecommunications sector. As of January 2023, Deutsche Telekom reported that over 80,000 base stations have been upgraded to 5G, achieving 94% population coverage in Germany, with aims to reach 99% coverage by 2025. This deployment of advanced telecommunications infrastructure is driving demand for specialized semiconductor materials, particularly in power amplifiers and RF components essential for 5G network expansion.

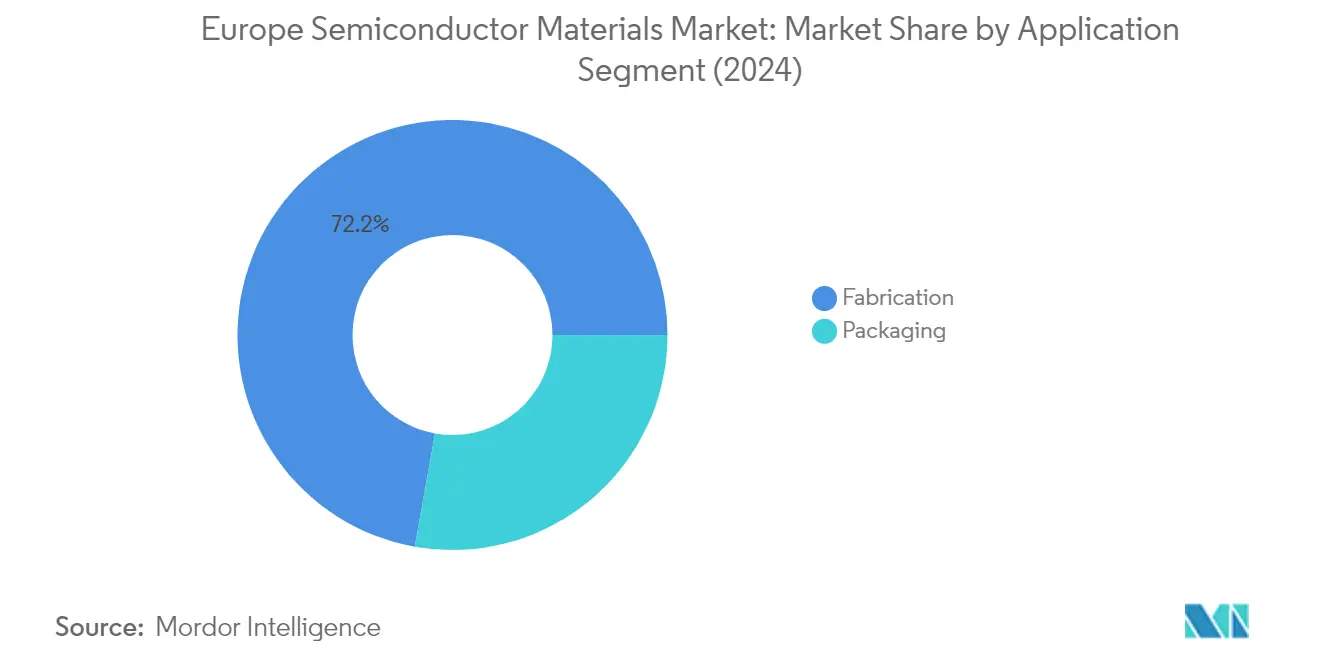

The industry structure continues to evolve with fabrication processes dominating the value chain, accounting for 71.6% of the market share in 2022. This dominance reflects the increasing complexity of semiconductor manufacturing processes, with modern fabrication requiring up to 1,400 process steps for semiconductor wafers alone. The industry is witnessing a shift toward advanced materials and manufacturing techniques, with companies investing in research and development of new semiconductor substrate materials to overcome the limitations of traditional silicon semiconductor technologies, particularly in meeting the demands for smaller, faster-integrated circuits that are pushing current materials to their theoretical limits.

Europe Semiconductor Materials Market Trends and Insights

Technical Advancement and Product Innovation of the Semiconductor Materials

The semiconductor industry is witnessing a revolutionary shift from traditional rigid substrates to more flexible and innovative semiconductor materials, driving significant technological advancement. A notable example is the December 2022 development by Pragmatic Semiconductor Ltd, which secured USD 35 million in funding to manufacture flexible processors that can bend without breaking and operate without silicon. This innovation, demonstrated through their collaboration with Arm Ltd on the PlasticArm project, represents a breakthrough in semiconductor material technology by implementing metal-oxide transistors on a plastic substrate. The trend toward flexible substrates has enabled the development of various devices, from advanced light-emitting diodes to high-efficiency solar cells and next-generation transistors.

The European Union's FACIT (Fast Annealing of Compound Semiconductors for Integration of New Technologies) project has achieved significant progress in combining III-V materials with silicon germanium technology. Scientists have successfully integrated indium, gallium, and arsenide (InGaAs) with silicon germanium (SiGe) technology to create advanced CMOS chips, compatible with high-volume chip fabrication. This breakthrough allows the integration of InGaAs, SiGe, and Si CMOS layers using large-sized Si wafers of 350-400 mm, enabling further miniaturization of semiconductor technology at the nanometer scale and addressing the ongoing challenges of Moore's Law in making computing devices smaller, faster, and more cost-effective.

Understand The Key Trends Shaping This Market

Download PDF

Rising Demand for Consumer Electronics Goods

The increasing sophistication of consumer electronics is driving unprecedented demand for advanced semiconductor materials, particularly in power electronics applications. Silicon carbide (SiC) has emerged as a crucial material due to its superior characteristics, enabling operation at higher temperatures and electrical potentials while delivering greater power conversion efficiency. This advancement is particularly evident in the evolution of charging technology, where current ratings have increased from 0.5 milliamps to 5 milliamps, necessitating SiC semiconductors in USB-C and onboard adapters to maintain required current and voltage levels.

Major consumer electronics manufacturers are actively incorporating advanced semiconductor materials to enhance product performance and meet consumer demands for faster charging and extended battery life. Companies like OPPO, OnePlus, Motorola, Samsung, and Apple are leveraging GaN and SiC devices in their next-generation onboard chargers and USB-C adapters to achieve ultra-high power density. The European Union's recent mandate requiring all cell phones, tablets, and cameras sold in the EU to include USB Type-C charging ports by the end of 2024, with laptops following by spring 2026, is further accelerating the adoption of advanced semiconductor materials in consumer electronics.

Increased Demand from OSAT/Packaging Companies

The semiconductor packaging industry is experiencing substantial growth in demand for advanced materials, driven by the increasing complexity of semiconductor devices and the need for innovative packaging solutions. In February 2023, Intel announced plans to build an advanced semiconductor packaging and assembly plant in Italy as part of its EUR 80 billion investment strategy in the European Union. This investment demonstrates the growing importance of packaging technologies in the semiconductor value chain and the increasing demand for specialized semiconductor packaging materials in packaging applications.

The evolution of packaging technologies is creating new requirements for semiconductor materials, particularly in areas such as die attachment, encapsulation, and thermal management. For instance, in March 2022, Intel announced the first phase of its plans to invest around EUR 80 billion in the European Union over the next decade along the entire semiconductor value chain, from R&D to manufacturing to state-of-the-art packaging technologies. This comprehensive investment approach highlights the critical role of packaging companies in driving demand for specialized semiconductor packaging materials and the industry's commitment to advancing packaging technologies to support next-generation semiconductor devices.

Segment Analysis: By Application

Fabrication Segment in Europe Semiconductor Materials Market

The fabrication segment dominates the European semiconductor materials market, commanding approximately 72% market share in 2024. This segment encompasses crucial materials such as process chemicals, photomasks, electronic gases, photoresist materials, sputtering targets, and silicon, with silicon being the most significant component, accounting for about 36% of fabrication materials. The segment's dominance is primarily driven by the increasing complexity of semiconductor manufacturing processes and the growing demand for advanced semiconductor devices across various industries. The fabrication segment is also experiencing the highest growth rate in the market, driven by technical advancements in semiconductor materials and the rising adoption of advanced manufacturing processes. The European Union's Chips Act and various government initiatives to strengthen domestic semiconductor manufacturing capabilities are further boosting the demand for fabrication materials.

Packaging Segment in Europe Semiconductor Materials Market

The packaging segment plays a vital role in the semiconductor materials market, encompassing materials such as substrates, lead frames, ceramic packages, bonding wire, encapsulation resins, and die attach materials. This segment is essential for protecting semiconductor devices and enabling their integration into various electronic systems. The growth in this segment is driven by the increasing demand for advanced packaging solutions, particularly in emerging applications such as 5G technology, automotive electronics, and Internet of Things (IoT) devices. The segment is benefiting from ongoing innovations in packaging technologies and materials, which are crucial for improving the performance and reliability of semiconductor devices while reducing their size and cost.

Segment Analysis: By End-User Industry

Consumer Electronics Segment in Europe Semiconductor Materials Market

The consumer electronics segment dominates the European semiconductor materials market, holding approximately 38% market share in 2024. This significant market position is driven by the increasing adoption of advanced electronic devices, including smartphones, tablets, smart home appliances, and wearable electronics across European countries. The segment's growth is further supported by the European Union's initiatives to strengthen domestic semiconductor production capabilities, particularly for consumer electronics applications. The rising demand for semiconductor materials in this segment is also fueled by technological advancements in consumer devices, such as the integration of artificial intelligence, IoT connectivity, and enhanced processing capabilities, which require more sophisticated semiconductor components.

Automotive Segment in Europe Semiconductor Materials Market

The automotive segment is emerging as the fastest-growing sector in the European semiconductor materials market, with projections indicating robust growth between 2024 and 2029. This accelerated growth is primarily driven by the rapid electrification of vehicles across European markets and the increasing integration of advanced driver assistance systems (ADAS). The segment's expansion is further supported by stringent European regulations promoting electric vehicle adoption and the growing implementation of autonomous driving technologies. European automotive manufacturers are increasingly incorporating sophisticated semiconductor materials in their vehicles for applications ranging from power management and battery systems to advanced safety features and infotainment systems.

Remaining Segments in Europe Semiconductor Materials Market

The telecommunications segment maintains a strong presence in the market, driven by the ongoing deployment of 5G infrastructure and network modernization initiatives across Europe. The manufacturing sector continues to evolve with the implementation of Industry 4.0 technologies and automation systems requiring specialized semiconductor materials. The energy and utility segment focuses on power management applications and smart grid technologies, while other end-user industries encompass diverse applications, including aerospace, defense, and healthcare sectors. Each of these segments contributes uniquely to the market's dynamics, with varying requirements for semiconductor materials based on their specific applications and technological needs.

Segment Analysis: By Type

Silicon Carbide (SiC) Segment in Global Compound Semiconductor Materials Market

Silicon Carbide (SiC) dominates the global compound semiconductor materials market, holding approximately 48% market share in 2024. This significant market position is driven by SiC's superior properties as a wide bandgap semiconductor material, including its ability to operate at very high junction temperatures exceeding 200°C and its low resistance in high-voltage applications. The material has become particularly crucial in power electronics applications, especially for electric vehicles, solar power inverters, and data center power supplies. Major European manufacturers are heavily investing in SiC facilities, with companies like STMicroelectronics and Wolfspeed establishing new production plants to meet the growing demand from automotive and industrial customers. The material's excellent efficiency in power conversion and control makes it ideal for applications ranging from photovoltaic energy storage inverters to data center server UPS power supplies and smart grid charging stations.

Growth Trajectory of SiC Segment in Global Compound Semiconductor Materials Market

The Silicon Carbide segment is experiencing remarkable growth, projected to expand at approximately 13% between 2024 and 2029. This exceptional growth rate is driven by several factors, including the increasing adoption of electric vehicles, the expansion of renewable energy infrastructure, and the growing demand for high-efficiency power electronics. The European Union's push towards semiconductor independence through initiatives like the EU Chips Act has led to significant investments in SiC manufacturing capabilities. The material's superior thermal conductivity, electron mobility, and lower power losses make it particularly attractive for next-generation applications in automotive, industrial, and energy sectors. The ongoing transition towards electrification and the need for more efficient power conversion systems continue to fuel the demand for SiC-based semiconductor devices.

Remaining Segments in Global Compound Semiconductor Materials Market

The compound semiconductor materials market encompasses several other significant segments, including Gallium Arsenide (GaAs), which plays a crucial role in RF applications and optoelectronics; Copper Indium Gallium Selenide (CIGS), primarily used in thin-film solar cells; Molybdenum Disulfide (MoS2), valued for its unique electronic properties and potential in next-generation devices; and Bismuth Telluride (Bi2Te3), important for thermoelectric applications. Each of these materials brings unique properties and advantages to specific applications, from high-frequency communications to renewable energy solutions. The diversity of these materials enables a wide range of applications across various industries, from telecommunications and consumer electronics to aerospace and defense, contributing to the overall growth and innovation in the semiconductor industry.

Europe Semiconductor Materials Market Geography Segment Analysis

Semiconductor Materials Market in North America

North America represents a significant hub for semiconductor materials, holding approximately 22% of the global market share in 2024. The region's prominence is driven by its robust semiconductor manufacturing ecosystem, particularly in the United States, which maintains its competitiveness through high-value design and production capabilities. The presence of leading semiconductor manufacturers, research institutions, and universities, especially in key areas like Silicon Valley, the Pacific Northwest, and the Northeast, strengthens the region's position. The automotive sector's transformation towards electric vehicles has created substantial demand for semiconductor materials, particularly in power electronics applications. The region's focus on technological innovation, coupled with substantial private and public investments in semiconductor research and development, continues to drive market growth. Additionally, the strong presence of end-user industries, including consumer electronics, telecommunications, and aerospace, further supports the market's expansion in North America.

Semiconductor Materials Market in Europe

The European semiconductor materials market has demonstrated robust growth, achieving approximately 13% annual growth from 2019 to 2024. The region's market is characterized by its strong focus on automotive and industrial applications, with Germany playing a leading role in microelectronics production. The European semiconductor ecosystem encompasses over 470 companies across 18 countries, with significant concentration in Germany, Austria, and other key markets. The region's strategic emphasis on developing domestic semiconductor capabilities is evident through initiatives like the European Chips Act and various national investment programs. The market benefits from strong research and development capabilities, particularly in advanced materials like silicon carbide and gallium arsenide. Europe's commitment to electric vehicle production and renewable energy adoption continues to drive demand for specialized semiconductor materials. The region's focus on creating a resilient semiconductor supply chain, coupled with substantial investments in manufacturing capabilities, positions it for sustained growth in the semiconductor materials sector.

Semiconductor Materials Market in Asia-Pacific

The Asia-Pacific region dominates the global semiconductor materials market, with a projected growth rate of approximately 11% from 2024 to 2029. The region's market leadership is anchored by the "Big 4" semiconductor players: China, Japan, South Korea, and Taiwan, which collectively form the backbone of global semiconductor production. The market benefits from extensive manufacturing infrastructure, advanced technological capabilities, and strong government support across key markets. Japan maintains its position as a crucial supplier of critical semiconductor materials, while South Korea excels in memory chip production and related materials. China's rapid expansion in semiconductor capabilities, coupled with Taiwan's advanced manufacturing expertise, creates a robust ecosystem for semiconductor materials. The region's market is further strengthened by the presence of major end-user electronics manufacturers, extensive research and development activities, and continuous technological innovations in semiconductor materials and applications.

Semiconductor Materials Market in Rest of the World

The Rest of the World region, encompassing Latin America, the Middle East, and Africa, represents an emerging market for semiconductor materials with significant growth potential. Latin America, particularly Mexico and Brazil, is experiencing increased activity in semiconductor-related industries, driven by strategic proximity to North American markets and favorable trade agreements. The Middle East is making strategic investments in semiconductor capabilities, particularly in countries like Saudi Arabia and the United Arab Emirates, focusing on supporting their digital transformation initiatives. The region's growing renewable energy sector, expanding 5G infrastructure, and increasing electric vehicle adoption create new opportunities for semiconductor materials. African nations are gradually developing their semiconductor capabilities, with countries like Kenya taking initial steps in semiconductor manufacturing. The region's market is characterized by increasing investments in digital infrastructure, growing automotive sector requirements, and rising demand for consumer electronics, all contributing to the expanding semiconductor materials market.

Competitive Landscape

Top Companies in Europe Semiconductor Materials Market

The European semiconductor materials market features established players like Solvay SA, Messer SE & Co. KGaA, Air Liquide SA, and BASF SE leading the industry through continuous innovation and strategic expansion. These companies demonstrate a strong commitment to research and development, focusing on creating advanced materials for next-generation semiconductor applications while maintaining operational excellence through digitalization and process optimization. Market leaders are increasingly emphasizing sustainable manufacturing practices and developing environmentally friendly material solutions to align with European regulations. The competitive landscape is characterized by strategic partnerships and collaborations across the value chain, particularly in emerging technologies like 5G, artificial intelligence, and autonomous vehicles. Companies are also investing heavily in expanding their manufacturing capabilities, strengthening their distribution networks, and establishing innovation centers across Europe to better serve the growing demand from various end-user industries.

Consolidated Market with Strong Regional Players

The European semiconductor materials market exhibits a relatively consolidated structure dominated by large chemical conglomerates with diverse product portfolios and strong manufacturing capabilities. These established players leverage their extensive research facilities, technical expertise, and long-standing customer relationships to maintain their market positions. The market also features specialized companies focusing on specific material segments such as specialty gases, photomasks, and advanced semiconductor packaging materials, who compete through technical differentiation and customized solutions. The presence of both global chemical giants and specialized regional players creates a dynamic competitive environment where companies must continuously innovate to maintain their market share.

The market has witnessed strategic mergers and acquisitions aimed at expanding product portfolios, accessing new technologies, and strengthening regional presence. Companies are increasingly focusing on vertical integration strategies to ensure supply chain stability and maintain quality control over critical materials. The industry structure is further shaped by long-term partnerships between material suppliers and semiconductor manufacturers, creating high barriers to entry for new players. Regional players are strengthening their positions through strategic alliances with global technology companies and investments in advanced manufacturing capabilities.

Innovation and Sustainability Drive Future Success

Success in the European semiconductor materials market increasingly depends on companies' ability to develop innovative materials that meet the evolving requirements of advanced semiconductor manufacturing processes. Market leaders are investing in research and development to create materials with enhanced performance characteristics while focusing on sustainability and environmental compliance. Companies are also strengthening their technical support capabilities and establishing closer collaborations with customers to develop customized solutions. The ability to scale production while maintaining quality consistency and ensuring reliable supply chains has become crucial for maintaining a competitive advantage in the market.

Future market success will be determined by companies' ability to navigate stringent environmental regulations while meeting the increasing demand for advanced semiconductor materials. Players must focus on developing eco-friendly alternatives and implementing sustainable manufacturing processes to align with the European Union's environmental policies. The market also requires significant investment in digital technologies and automation to improve operational efficiency and reduce production costs. Companies need to maintain strong relationships with end-users across various industries while continuously monitoring and adapting to technological changes in the semiconductor industry. Additionally, the ability to provide comprehensive solution packages, including technical support and application expertise, will become increasingly important for maintaining market position.

Europe Semiconductor Materials Industry Leaders

Solvay SA

Messer SE & Co. KGaA

Air Liquide SA

Compugraphics (MacDermid Alpha Electronics Solutions)

International Quantum Epitaxy PLC (IQE PLC)

- *Disclaimer: Major Players sorted in no particular order

.webp)

Recent Industry Developments

- October 2022 - STMicroelectronics (ST) declared that it would construct a EUR 730 million (USD 728 million) silicon carbide wafer plant in Italy. This project is the first approved as part of an EU initiative to move chip production closer to consumers' homes. With the switch to electrification, the new integrated silicon carbide (SiC) substrate manufacturing plant would be able to handle the rising demand from automotive and industrial clients.

- June 2022 - BASF will build a commercial-scale battery recycling black mass plant in Schwarzheide, Germany. This investment strengthens BASF's cathode active materials (CAM) production and recycling hub in Schwarzheide. The site is an ideal location for the build-up of battery recycling activities, given the presence of many EV car manufacturers and cell producers in Central Europe. This investment is anticipated to create about 30 new production jobs, with a startup planned for early 2024. This helps to identify and define the output and application of lithium-ion batteries used in various semiconductors devices.

Europe Semiconductor Materials Market Report Scope

A semiconductor is a silicon-based material that conducts electricity better than an insulator like glass but not a pure conductor like copper or aluminum. Materials used to pattern the wafer are considered fabrication materials within the scope of the study. In contrast, materials used to protect or connect the die are called packing materials. Semiconductor fabrication is a set of operations that involves depositing a sequence of layers onto a substrate, most often silicon, to create a device structure. Various thin film layers are deposited and removed in this process. Photolithography is used to regulate the portions of the thin film that are to be applied or removed. Cleaning and inspection stages are usually performed after each deposition and removal operation.

The European semiconductor materials market is segmented by application (fabrication (process chemicals, photomasks, electronic gases, photoresists ancillaries, sputtering targets, silicon, and other fabrication applications), packaging (substrates, lead frames, ceramic packages, bonding wire, encapsulation resins (liquid), die-attach materials, and other packaging applications)), end-user industry (consumer electronics, telecommunication, manufacturing, automotive, energy and utility, and other end-user industries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Application

| Fabrication | Process Chemicals |

| Photomasks | |

| Electronic Gases | |

| Photoresists Ancillaries | |

| Sputtering Targets | |

| Silicon | |

| Other Fabrication Applications | |

| Packaging | Substrates |

| Lead Frames | |

| Ceramic Packages | |

| Bonding Wire | |

| Encapsulation Resins (Liquid) | |

| Die Attach Materials | |

| Other Packaging Applications |

By End-user Industry

| Consumer Electronics |

| Telecommunication |

| Manufacturing |

| Automotive |

| Energy and Utility |

| Other End-User Industries |

| By Application | Fabrication | Process Chemicals |

| Photomasks | ||

| Electronic Gases | ||

| Photoresists Ancillaries | ||

| Sputtering Targets | ||

| Silicon | ||

| Other Fabrication Applications | ||

| Packaging | Substrates | |

| Lead Frames | ||

| Ceramic Packages | ||

| Bonding Wire | ||

| Encapsulation Resins (Liquid) | ||

| Die Attach Materials | ||

| Other Packaging Applications | ||

| By End-user Industry | Consumer Electronics | |

| Telecommunication | ||

| Manufacturing | ||

| Automotive | ||

| Energy and Utility | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How big is the Europe Semiconductor Materials Market?

The Europe Semiconductor Materials Market size is expected to reach USD 6.00 billion in 2025 and grow at a CAGR of 4.94% to reach USD 7.64 billion by 2030.

What is the current Europe Semiconductor Materials Market size?

In 2025, the Europe Semiconductor Materials Market size is expected to reach USD 6.00 billion.

Who are the key players in Europe Semiconductor Materials Market?

Solvay SA, Messer SE & Co. KGaA, Air Liquide SA, Compugraphics (MacDermid Alpha Electronics Solutions) and International Quantum Epitaxy PLC (IQE PLC) are the major companies operating in the Europe Semiconductor Materials Market.

What years does this Europe Semiconductor Materials Market cover, and what was the market size in 2024?

In 2024, the Europe Semiconductor Materials Market size was estimated at USD 5.70 billion. The report covers the Europe Semiconductor Materials Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Europe Semiconductor Materials Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: