Stretchable Conductive Material Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

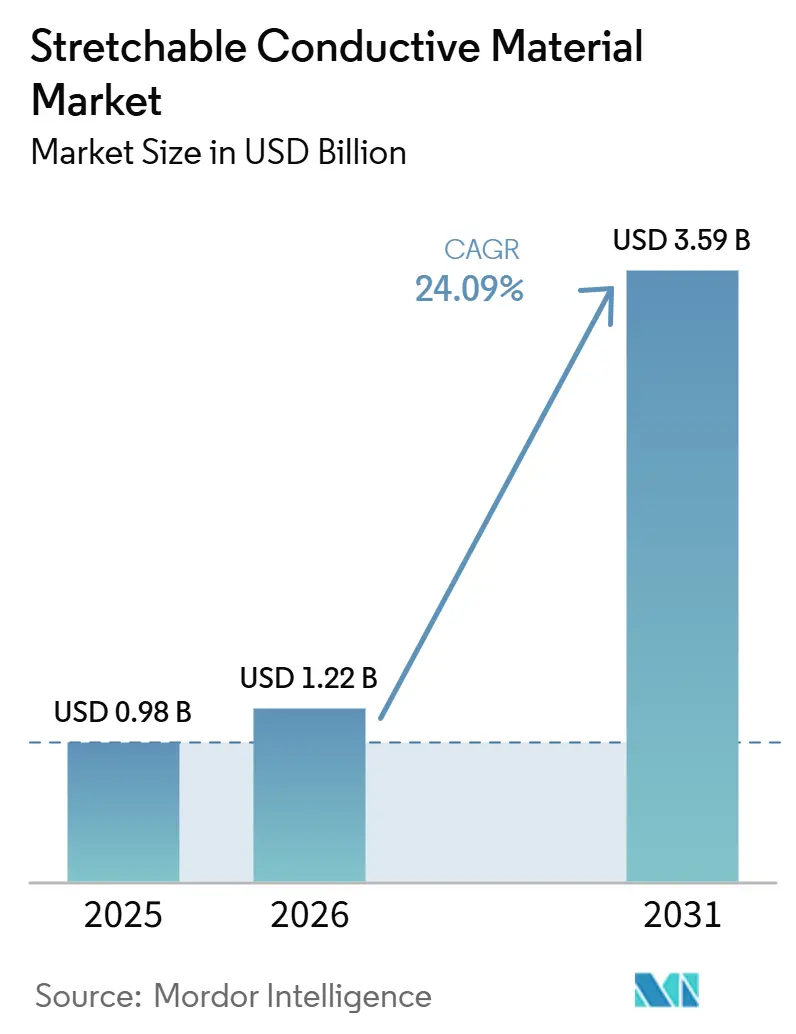

| Market Size (2026) | USD 1.22 Billion |

| Market Size (2031) | USD 3.59 Billion |

| Growth Rate (2026 - 2031) | 24.09% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stretchable Conductive Material Market Analysis by Mordor Intelligence

The Stretchable Conductive Material Market size was valued at USD 0.98 billion in 2025 and is estimated to grow from USD 1.22 billion in 2026 to reach USD 3.59 billion by 2031, at a CAGR of 24.09% during the forecast period (2026-2031). Sovereign-AI mandates are pushing edge inference into garments, while automotive battery-swelling sensors call for real-time strain feedback, collectively accelerating the commercialization of materials that retain conductivity under 200% strain. Defense agencies are fast-tracking electronic-skin prototypes, and healthcare regulators have cleared wearable biopotential monitors embedding silver nanowire inks, reinforcing demand for high-reliability stretchable interconnects. Subsidies for flexible-display fabs across Asia-Pacific and DARPA-funded soldier-healing programs in North America are shifting production lines from pilot to volume scale. Raw-material recycling breakthroughs in Europe promise 87% silver recovery, aligning the stretchable conductive material market with emerging circular-economy mandates.

Key Report Takeaways

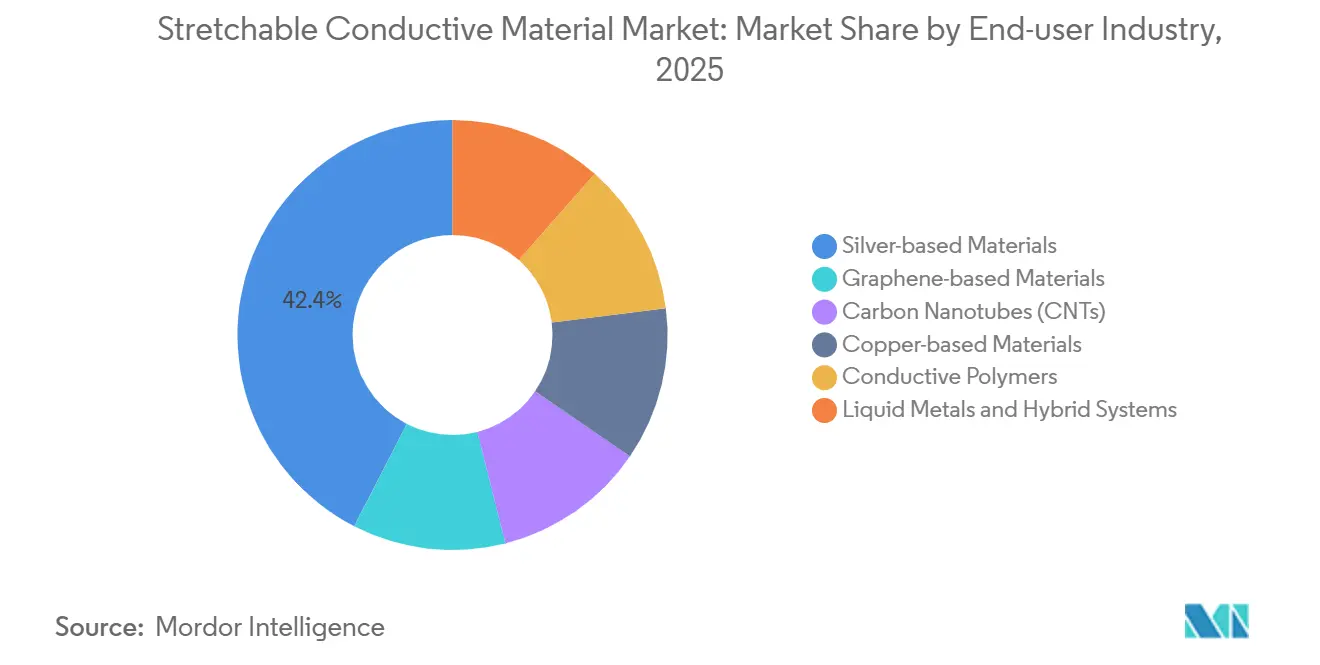

- By type of material, silver-based materials led with 42.44% of the stretchable conductive material market share in 2025, while liquid metals and hybrids are forecast to post the fastest 25.67% CAGR through 2031.

- By form, inks accounted for 51.50% share of the stretchable conductive material market size in 2025, whereas elastomeric composites are projected to advance at a 25.74% CAGR to 2031.

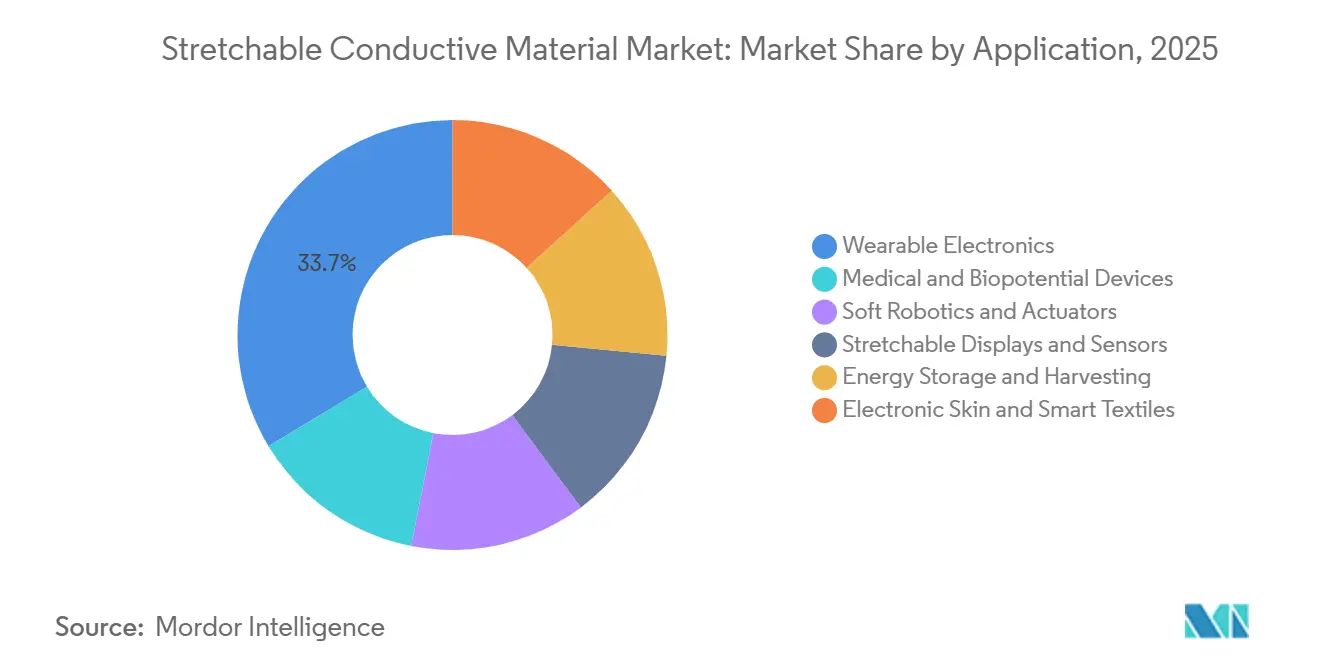

- By application, wearable electronics captured 33.65% revenue in 2025; medical and biopotential devices are poised for the highest 25.83% CAGR through 2031.

- By end-user, consumer electronics held 38.40% share in 2025, but healthcare spending is set to grow fastest at a 25.71% CAGR through 2031 on expanding reimbursement for remote patient monitoring.

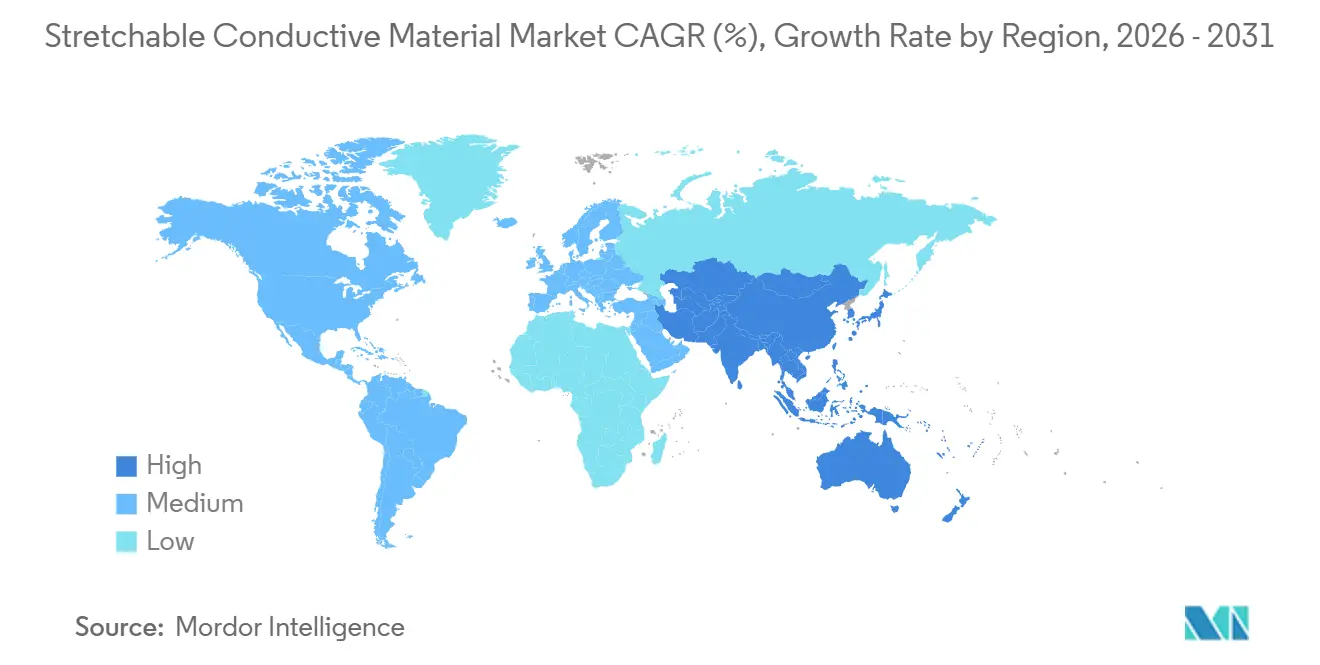

- By geography, Asia-Pacific commanded 41.60% of 2025 revenue and is expected to sustain the quickest 25.45% CAGR through 2031, buoyed by China’s flexible-display subsidies and South Korea’s stretchable OLED breakthroughs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Stretchable Conductive Material Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for wearable electronics and smart textiles | +6.2% | Global, with APAC core and North America early adoption | Medium term (2-4 years) |

| Advancements in flexible and stretchable electronics | +5.8% | Global, led by South Korea, China, and United States | Long term (≥ 4 years) |

| Healthcare monitoring devices proliferation | +5.3% | North America and EU regulatory markets, spillover to APAC | Short term (≤ 2 years) |

| Defense-funded electronic skin research and development programs | +3.1% | United States, with secondary interest in EU and Israel | Medium term (2-4 years) |

| Sustainability push toward recyclable printed electronics | +2.9% | EU core, expanding to North America and select APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Wearable Electronics and Smart Textiles

Mass-market acceptance of continuous health tracking is elevating stretchable conductors from specialty research to consumer staples, with FDA clearances in 2025 validating silver-nanowire electrodes for clinical-grade patches[1]U.S. Food and Drug Administration, “Medical Devices,” fda.gov. Silver-nanowire inks printed on thermoplastic polyurethane survive 100,000 flex cycles, enabling garment-integrated sensors that withstand industrial laundry. Industrial safety mandates are adding smart-textile demand, illustrated by Panasonic’s Copper Clad Stretch material launched in late 2025 for 6G antenna garments[2]Panasonic Corporation, “Copper Clad Stretch Material,” panasonic.com. The rise of 5G edge computing requires stretchable interconnects that maintain gigahertz integrity, a task rigid copper foils cannot meet beyond 10% elongation. ISO 13485 compliance is guiding material selection toward proven biocompatibility and wash durability, embedding quality benchmarks into design workflows.

Advancements in Flexible and Stretchable Electronics

Material-science milestones are closing the gap between rigid silicon and stretchable organics. EPFL demonstrated liquid-metal fibers retaining 95% conductivity at 300% strain, opening a path to prosthetic skin with tactile fidelity. MXene-based strain-invariant devices sustain stable resistance across 0-50% strain, reducing electromechanical hysteresis to 2%. South Korea’s KAIST-POSTECH consortium achieved 25% external quantum efficiency in stretchable OLEDs at 30% strain, pivoting flexible displays toward automotive dashboards and AR visors. Commercial viability hinges on roll-to-roll printing at sub-10 µm features under USD 5 per m², targets Henkel and DuPont pursue via AI-optimized inks. These developments collectively expand the stretchable conductive material market beyond low-current sensors to power-dense actuators and energy-harvesting modules.

Healthcare Monitoring Devices Proliferation

Regulatory pathways and reimbursement codes are shifting care from episodic visits to remote monitoring. FDA approvals for LifeSignals and Cardiosense patches in 2025 confirmed the clinical accuracy of polymer electrodes that conform to skin without irritation. Disposable 30-day cardiac monitors now qualify for insurance billing, scaling demand for low-cost gravure-printed PEDOT:PSS sensors. Stretchable electrodes must handle skin-impedance swings from 1kΩ to 100kΩ, and silver-chloride coatings stabilize signals under ambulation. DARPA’s MASH initiative integrates wound-oxygenation and drug-delivery on a single stretchable substrate, creating defense-to-healthcare spillovers. Supply-chain barriers rise as FDA-compliant cleanrooms and ISO 13485 certification become prerequisites, favoring incumbents with regulatory infrastructure.

Defense-Funded Electronic Skin Research and Development Programs

DARPA’s 2024 AFR awards target electronic skin that withstands ballistic impact and temperature swings from -40°C to 60°C. Liquid Wire’s Metal Gel delivers self-healing conductors that reroute current around punctures, aligning with defense redundancy specs. The U.S. Army’s conformal casualty-care RFI signals field deployment of sensor arrays that monitor vitals and trigger automated tourniquets. Carbon-nanotube actuators with sub-1 ms response enable soft exoskeletons for load carriage; Harvard’s Biodesign Lab validated a pneumatic rehabilitation suit in 2024. NextFlex partnerships adapt military-grade processes for automotive and industrial use, reinforcing the stretchable conductive material market’s dual-use trajectory.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced nanomaterials and production technology | -3.7% | Global, with acute pressure in cost-sensitive APAC and South America | Short term (≤ 2 years) |

| Performance fatigue under cyclic strain | -2.1% | Global, affecting high-reliability applications in automotive and medical | Medium term (2-4 years) |

| Electromechanical hysteresis limiting sensor precision | -1.8% | North America and EU precision-instrumentation markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Nanomaterials and Production Technology

Single-walled carbon nanotubes at USD 500 per kg and graphene above USD 200 per kg confine usage to premium sectors. Automotive Tier 1 suppliers target sub-USD 2 sensor modules, a hurdle current nanomaterial pricing cannot meet. Roll-to-roll printers with sub-5 µm registration exceed USD 10 million CAPEX, deterring entrants. DexMat’s continuous CNT synthesis cut costs to USD 150 per kg in 2024, yet adoption lags as converters lack ink-rheology expertise. Price pressure will relax post-2028 when large-scale Chinese and Korean fabs reach multi-ton capacities.

Performance Fatigue Under Cyclic Strain

Peer-reviewed work shows 20-50% conductivity loss after 10,000 cycles at 30% strain. Automotive life-span requirements of 1 million cycles demand 5 times safety margins, inflating BOM costs. Liquid metals self-heal but corrode aluminum and raise indium-toxicity concerns. Hybrid rigid-island designs reduce local strain yet increase assembly cost by 40%. Fatigue risk confines current deployments to disposable patches and low-strain garments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Material: Liquid Metals Gain as Silver Leads

Liquid metals and hybrid systems are projected to grow at 25.67% CAGR during 2026-2031 and will capture an incremental stretchable conductive material market size as gallium-indium alloys overcome humidity-induced oxidation failures in nanowire films. Silver-based materials maintain dominance with a 42.44% 2025 share, supported by Nitto Denko’s USD 15 million capacity investment in C3Nano. Graphene-metal nanomembranes demonstrated gigahertz-level stability under 100% strain, advancing 6G wearable antennas. CNTs benefit from OCSiAl’s 150-ton TUBALL output, enabling battery-swelling sensors that demand 15-year reliability.

Material choice now segments by end-use: medical devices prefer biocompatible silver; defense favors liquid metals for self-healing; consumer electronics default to copper for cost; soft robotics adopts CNT-polymer composites for compliance. The stretchable conductive material market share of hybrid architectures combining rigid-island chips with stretchable interconnects will widen post-2027 as Panasonic’s Copper Clad Stretch formalizes manufacturing design-rules.

By Form: Elastomeric Composites Accelerate Past Inks

Inks retained 51.50% of 2025 revenue owing to low-cost screen printing that delivers sub-USD 0.10 medical patches. Yet elastomeric composites will log the highest 25.74% CAGR through 2031 as OEMs seek laminate-ready modules that bypass printer investment. Films and foils such as Panasonic’s FineX provide foldable-display hinges with less than 10 Ω/sq resistance at 50% elongation. Tapes and coatings serve research and development, with 3M’s 2025 conductive-tape expansion keeping less than 1Ω contact resistance under 20% shear. As roll-to-roll capacity scales, the stretchable conductive material market size for elastomeric composites in soft-robotic actuators and automotive sensors will increasingly outpace inks.

By Application: Medical Devices Surpass Wearables

Wearables dominated 2025 with 33.65% share, but medical and biopotential devices are set to grow faster at a 25.83% CAGR through 2031, moving the stretchable conductive material market toward regulated healthcare revenue. Continuous glucose monitors and cardiac patches validate polymer electrodes, steering demand for ISO 13485 production lines. Soft-robotic grippers like Festo’s Bionic SoftHand highlight emerging high-margin niches. Energy-harvesting nanogenerators generating 1.2 mW/cm² aim to eliminate batteries in IoT, broadening application footprints. Automotive and e-mobility will join the mainstream once recycled nanowire costs fall below USD 50 per kg after 2028.

By End-User Industry: Healthcare Overtakes Consumer Electronics

Consumer electronics held 38.40% of 2025 spending, yet healthcare is forecast to lead at a 25.71% CAGR during 2026-2031 as reimbursement models favor 30-day wearable patches. Aerospace and defense research and development funnels into rugged sensors resilient to ballistic impact, driving dual-use adoption cycles. Automotive demand hinges on sub-USD 2 module costs for battery-swelling detection, pressing suppliers to scale recycled silver nanowire capacity. Industrial automation and sports analytics form niche opportunities, exploiting stretchable sensors for real-time process feedback and injury prevention.

Geography Analysis

Asia-Pacific generated 41.6% of 2025 revenue and is projected to achieve a 25.45% CAGR through 2031, driven by China’s flexible-display subsidies, South Korea’s 25%-efficient stretchable OLEDs, and Panasonic’s CCS launch in Japan. Vertically integrated supply chains, such as Jiangsu Cnano’s 500-ton graphene output and Taiwan PCB investments topping USD 2 billion, anchor regional leadership. India and ASEAN nations emerge as low-cost assembly hubs, although material innovation remains Northeast-Asian-centric.

North America benefits from DARPA and U.S. Army funding of electronic-skin prototypes, pulling technologies into commercial healthcare and automotive by 2028. FDA pathways and ISO 13485 plants attract premium suppliers like 3M and DuPont, both channeling multibillion-dollar research and development to defend shares. Canada and Mexico follow U.S. automotive adoption curves, evaluating stretchable sensors for EV battery monitoring.

Europe’s growth aligns with recyclability mandates; IEC TC-111’s 2025 update embeds material-recovery metrics in procurement, advantaging Henkel’s debonding adhesives and Heraeus’s recyclable pastes. Germany and France drive academic breakthroughs, while Nordic pilots in occupational safety offer early-adopter demand for industrial-laundry-proof sensors. Sanctions limit Russia’s participation; South America and MEA remain nascent, with Brazil’s public health system and Saudi smart-city projects monitoring cost-down roadmaps for post-2028 uptake.

Competitive Landscape

The stretchable conductive material market is moderately fragmented. Vertical integration is intensifying: Nitto Denko’s USD 15 million equity stake in C3Nano secures silver-nanowire supply, while 3M’s USD 3.5 billion research and development plan covers 1,000 new products across electronics and optics. Henkel’s debonding adhesives create recurring battery-repair revenue, and DuPont’s Pyralux laminates leverage polyimide heritage to meet automotive reliability at consumer prices.

Disruptors like Liquid Wire and DexMat target self-healing and cost reductions, respectively. EPFL spinouts advance liquid-metal fibers, and MXene innovators chase sub-2% hysteresis, threatening legacy silver-nanowire incumbents if costs dip below USD 100 per kg. Patent clustering around hybrid rigid-island designs, led by NextFlex consortia, is accelerating standardization. Consolidation is expected post-2028 as automotive and medical volumes scale, favoring ISO 13485-certified producers able to fund cleanroom expansions, while niche startups pivot to defense and industrial specialties.

Stretchable Conductive Material Industry Leaders

3M

DuPont

Henkel AG & Co. KGaA

Rogers Corporation

Nitto Denko Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Panasonic released FineX transparent conductive film supporting 50% elongation with 85% optical transparency .

- April 2025: Henkel showcased battery-debonding adhesives, cutting lifecycle carbon 40% versus welded assemblies.

Global Stretchable Conductive Material Market Report Scope

Stretchable conductive materials are specialized composites or polymers engineered to maintain electrical conductivity under mechanical deformation, such as stretching, bending, or twisting. These materials provide flexible alternatives to conventional rigid metal wires.

The stretchable conductive materials market is segmented by type of material, form, application, end-user industry, and geography. By type of material, the market is segmented into graphene-based materials, silver-based materials, carbon nanotubes (CNTs), copper-based materials, conductive polymers, and liquid metals and hybrid systems. By form, the market is segmented into inks, films and foils, elastomeric composites, and tapes and coatings. By application, the market is segmented into wearable electronics, medical and biopotential devices, soft robotics and actuators, stretchable displays and sensors, energy storage and harvesting, and electronic skin and smart textiles. By end-user industry, the market is segmented into consumer electronics, healthcare, aerospace and defense, automotive and e-mobility, energy and utilities, and industrial automation and sports/fitness. The report also covers the market size and forecasts for the stretchable conductive material market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done based on value (USD).

| Graphene-based Materials |

| Silver-based Materials |

| Carbon Nanotubes (CNTs) |

| Copper-based Materials |

| Conductive Polymers |

| Liquid Metals and Hybrid Systems |

| Inks |

| Films and Foils |

| Elastomeric Composites |

| Tapes and Coatings |

| Wearable Electronics |

| Medical and Biopotential Devices |

| Soft Robotics and Actuators |

| Stretchable Displays and Sensors |

| Energy Storage and Harvesting |

| Electronic Skin and Smart Textiles |

| Consumer Electronics |

| Healthcare |

| Aerospace and Defense |

| Automotive and e-Mobility |

| Energy and Utilities |

| Industrial Automation and Sports/Fitness |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type of Material | Graphene-based Materials | |

| Silver-based Materials | ||

| Carbon Nanotubes (CNTs) | ||

| Copper-based Materials | ||

| Conductive Polymers | ||

| Liquid Metals and Hybrid Systems | ||

| By Form | Inks | |

| Films and Foils | ||

| Elastomeric Composites | ||

| Tapes and Coatings | ||

| By Application | Wearable Electronics | |

| Medical and Biopotential Devices | ||

| Soft Robotics and Actuators | ||

| Stretchable Displays and Sensors | ||

| Energy Storage and Harvesting | ||

| Electronic Skin and Smart Textiles | ||

| By End-user Industry | Consumer Electronics | |

| Healthcare | ||

| Aerospace and Defense | ||

| Automotive and e-Mobility | ||

| Energy and Utilities | ||

| Industrial Automation and Sports/Fitness | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the stretchable conductive material market in 2031?

It is forecast to reach USD 3.59 billion by 2031, expanding at a 24.09% CAGR from 2026.

Which material currently dominates commercial use?

Silver-based compositions led with 42.44% market share in 2025 due to proven printability and biocompatibility.

Why are liquid metals gaining attention?

Gallium-indium alloys self-heal and resist humidity-driven oxidation, driving the fastest 25.67% CAGR through 2031 among material types.

How are healthcare regulations influencing adoption?

FDA clearances for stretchable cardiac and glucose-monitoring patches are accelerating medical uptake while requiring ISO 13485 production lines.

What regional factors favor Asia-Pacific growth?

Government subsidies for flexible displays, large-scale nanomaterial capacity, and vertically integrated electronics supply chains underpin a 25.45% CAGR during 2026-2031.

Page last updated on: